AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

In a Nutshell:

- A money transfer app lets users send, receive, and manage digital payments via digital wallets, bank integrations, and payment gateways.

- The global money transfer app market is valued at $25.88 billion in 2025 and is projected to reach $78.40 billion by 2032.

- Core features include user registration, transaction history, wallet integration, KYC verification, multi-currency support, and push notifications.

- Development follows 8 steps: market research, partner selection, planning, MVP, UI/UX design, development, testing, and deployment.

- Regulatory compliance requires KYC, AML, PCI DSS, EMI license, and GDPR/CCPA adherence, depending on your target market.

- Development cost ranges from $25,000 (basic) to $200,000+ (advanced), with a timeline of 3-12 months based on complexity.

- Common monetization models include currency exchange margins, transaction fees, premium subscriptions, and merchant service fees.

Creating a money transfer app demands developing a compliant, secure, and user-friendly platform that supports peer-to-peer transfers, real-time transaction processing, and multi-currency payments.

The core money transfer app development process covers five key areas: picking your app type, defining must-have features, choosing the right tech stack, fulfilling regulatory requirements (KYC, AML, and PCI DSS), and estimating costs, which generally range from $25,000 to $200,000 depending on the complexity.

The online money transfer app market was valued at US$25.88 billion in 2025 and is expected to reach US$78.40 billion by 2032, with a CAGR of 18.5%.

Whether you are investors, entrepreneurs, business owners, or product managers, you can capitalize on the surging market through fintech app development.

The guide walks you through a step-by-step process to create a money transfer app, from ideation to deployment and monetization, so you can make more-informed decisions and build an app that’s well-prepared for the 2026 fintech market.

What is a Money Transfer App?

A money transfer app is a mobile app that facilitates users to send, receive, and manage money digitally through payment gateways, bank account integrations, and digital wallets without physically visiting a bank or using cash.

Unlike traditional bank transfers that demand 1 to 3 business days, money transfer apps process bill payments, peer-to-peer payments, and cross-border remittances in real time, usually within seconds.

Apps like Wise, PayPal, and Venmo are widely used examples, each developed on the same core architecture but serving distinct user requirements and markets.

How Money Transfer Apps Work?

A money transfer app, at its core, acts as a secure bridge between two digital wallets or bank accounts.

Check how the process works from the moment you open the application to the point money lands in the recipient’s account.

Step 1: Download and install the app

Install the app from the App Store or Google Play Store. Most apps are free to download, and revenue comes from transaction fees or premium plans.

Step 2: Create an account and link your bank

Register using your email or phone number, then connect your bank account or debit card. This connection uses bank-level encryption (typically 256-bit SSL) to keep your credentials secure.

Step 3: Complete identity verification (KYC)

Most regulated money transfer apps demand identity verification – uploading a government ID and sometimes a selfie. This is a legal requirement under KYC (Know Your Customer) regulations, not just an app preference.

Step 4: Enter recipient details

Add the recipient’s phone number, email, or bank account details. Many applications let you save frequent recipients for faster future transfers.

Step 5: Enter the amount and review fees

Enter the transfer amount. The app will showcase any applicable fees and, for international transfers, the live exchange rate before you confirm.

Step 6: Authorize the transaction

Confirm the transfer using your PIN, face ID, or fingerprint. This triggers a two-factor authentication check in the background to verify the transaction is legitimate.

Step 7: Transfer is processed

The app communicates with your bank or payment gateway to start the fund movement. Domestic transfers generally settle within seconds to a few hours. International transfers may take 1 to 2 business days, depending on the corridor and the receiving bank.

Step 8: Both parties receive confirmation

Once the transfer is complete, both sender and recipient receive a real-time push notification and an in-app transaction receipt for their records.

Money Transfer App Market: Size, Growth & Key Stats (2026)

Before you invest in money transfer app development, understanding the scale of opportunity will help. Below, the numbers are drawn from several market research studies, and the differences in figures show distinct market scopes (app-only vs full money transfer services market).

► App Market Size

- The global money transfer app market was valued at $25.88 billion in 2025 and is projected to reach $78.40 billion by 2032, growing at a CAGR of 18.5% – Coherent Market Insights, 2025.

- The broader money transfer services market that includes wire transfers, remittance services, and agent networks is anticipated to reach $93.2 billion by 2032 at a CAGR of 16.2% – Dimension Market Research, 2025.

► Cross-Border Payments

- Global cross-border payment volumes are expected to surpass $250 trillion by 2027 and exceed $290 trillion by 2030, driven by e-commerce growth and international remittances (Bank for International Settlements, 2024).

- The international remittance market alone is projected to grow at a CAGR of 10.2% through 2030, with mobile-first platforms capturing an increasing share – World Bank, 2025.

► User Behaviour

In the United States and Germany, 70%+ of peer-to-peer (P2P) payments are made utilizing mobile digital wallets – PYMNTS, 2025.

Western Union processes about $150 billion alone in annual transfer volume, exhibiting the scale incumbents have developed and the gap that digital-first apps are rapidly filling.

What this means for builders

The shift from agent-based transfers to mobile-first apps is speeding up. Apps that fuse low fees, multi-currency support, and instant settlement are best placed to capture the growing base of underserved cross-border users.

Types of Money Transfer Apps You Can Build

Well, not every money transfer app serves the same objective. The type you create decides your compliance needs, target audience, core feature set, and finally, your development cost.

Here are the four main types and what differentiates each.

1. Person-to-Person (P2P) Money Transfer Apps

P2P apps enable individuals to directly send money to other individuals – paying rent, splitting bills, or sending money to family.

For fintech startups, such apps are the most common entry point due to less regulatory complexity than business-facing products.

- Real-world examples: Venmo, Cash App, Zelle

- Best for: Consumer-facing startups, social payment features, and domestic markets.

- Key compliance requirement: KYC verification, transaction limits under AML thresholds

2. Business-to-Business (B2B) Money Transfer Apps

B2B platforms manage high-volume payments between businesses – payroll disbursements, invoice settlements, and supplier payments.

Such apps generally process huge transaction amounts and demand more powerful audit trails and fraud detection capabilities.

- Real-World Examples: Stripe, Payoneer, Tipalti

- Best for: SaaS platforms, procurement tools, and enterprise finance teams.

- Key Compliance Requirement: Improved due diligence (EDD), multi-jurisdiction licensing for cross-border B2B, and AML monitoring.

3. Individual-to-Business (I2B) Money Transfer Apps

Also termed as bill payment platforms, I2B applications allow consumers to directly pay businesses – school fees, utility bills, retail purchases, and insurance premiums.

These apps usually include cashback offers, loyalty programs, and scheduled payment features to drive repeat usage.

- Real-world Examples: Paytm (India), BillDesk, Google Pay (merchant payments)

- Best for: Markets with super-app strategies, high bill-payment volume, utility, and telecom sectors

- Key Compliance Requirement: Payment aggregator licensing, PCI DSS compliance

4. International Money Transfer Apps

Cross-border apps enable users to send money across currencies and countries. They are the most complex type of development due to differing regulatory requirements in every corridor, multi-currency handling, and exchange rate management, but simultaneously the most profitable with a $250 trillion cross-border payment market.

- Real-World Examples: Wise, Remitly, and WorldRemit

- Best for: Diaspora remittance markets, international e-commerce, and global freelancer payments.

- Key Compliance Eequirement: Money Transmitter Licenses (MTL) per state/country, SWIFT or local payment rail integration, and FX compliance.

Choosing the Right Type:

| Type | Complexity | Avg. Development Cost | Primary Revenue Model |

| P2P | Low–Medium | $25,000–$80,000 | Transaction fees |

| B2B | High | $80,000–$200,000+ | Subscription + transaction fees |

| I2B | Medium | $40,000–$100,000 | Merchant service fees |

| International | Very High | $100,000–$200,000+ | FX margins + transfer fees |

If you are unsure which money transfer app type fits your business model, begin with a P2P MVP to validate demand before scaling into cross-border or B2B functionality.

Must-Have Features of a Money Transfer App (Core + Advanced)

The features you include in your money transfer app directly decide the development cost, user retention, and compliance requirements.

Below is a breakdown of key features each money transfer app should have at launch, followed by advanced features that push competitive distinction in 2026.

► Core Features of a Money Transfer App

These are non-negotiable. An app missing any of these will fail app store submission, regulatory review, or basic user trust benchmarks.

| Features | What It Does | Why It Matters |

| User Registration & KYC | Onboards users with identity verification, government ID, selfie match, and address proof | Legal requirement in all regulated markets. Without KYC, your app cannot legally process transactions |

| Digital Wallet Integration | Allows users to store, load, and manage funds within the app | Reduces dependency on real-time bank connectivity, improves transaction speed and reliability |

| Fund Transfer (P2P) | Enables instant money transfers between users via phone number, email, or account ID | Core product functionality is the primary reason users download the app |

| Multi-Currency Support | Handles transactions in multiple currencies with live exchange rate conversion | Essential for any app targeting cross-border or international remittance use cases |

| Transaction History | Displays a detailed, searchable log of all past transfers, receipts, and failed attempts | Builds user trust and is required for AML audit trail compliance |

| Payment Gateway Integration | Connects with third-party processors (Stripe, Razorpay, Plaid) to execute bank-level transfers | Enables actual fund movement; without this, the app cannot process real money |

| Push Notifications | Sends real-time alerts for transaction success, failure, suspicious activity, and low balance | Directly impacts user engagement and fraud response time |

| Two-Factor Authentication (2FA) | Requires a second verification step (OTP, biometric, or authenticator app) at login and transfer | Reduces account takeover risk, now a baseline expectation for any financial app |

| Multi-Language Support | Displays the app interface in the user’s preferred language | Critical for international apps significantly improves conversion in non-English markets |

► Advanced Features of a Money Transfer App

These features are not needed at launch, but are more expected by users and are powerful drivers of trust, retention, and revenue growth. You can plan these for version 2.0 or later.

| Features | What It Does | Why It Matters |

| Fraud Detection | Uses machine learning to analyze transaction patterns and flag suspicious activity in real time | Reduces chargebacks and fraud losses — Mastercard reports AI-based fraud detection reduces false positives by up to 80% |

| Smart Transfer Suggestions | Recommends the fastest, cheapest, or most reliable transfer method based on the recipient and amount | Improves user experience and increases transfer completion rates |

| In-App Chat Support | Provides automated and live customer support directly within the app | Reduces churn from unresolved issues — critical for high-value or first-time users |

| Predictive Analytics Dashboard | Gives users insights into their spending and transfer patterns | Drives engagement and positions the app as a financial management tool, not just a transfer utility |

| Automated Compliance Monitoring | Continuously screens transactions against KYC/AML rules without manual review | Reduces compliance team overhead and speeds up regulatory reporting |

| Biometric Authentication | Uses facial recognition or fingerprint scanning for login and transaction authorization | Faster and more secure than PIN-based authentication — now expected on premium fintech apps |

| Loyalty & Rewards Engine | Tracks user activity and offers cashback, fee waivers, or transfer bonuses | Increases transaction frequency and reduces churn — used effectively by Revolut and Paytm |

| Scheduled & Recurring Transfers | Allows users to set up automatic transfers on a fixed schedule | High-value feature for bill payments, salary disbursements, and regular remittances |

► MVP vs Full Feature Set – What to Build First

If you are creating your first version, focus on the core features, biometric authentication, and fraud detection from the advanced list.

These three advanced features impact the user trust and regulatory approval excessively, making them worth focusing on even in an MVP.

| Build Phase | Features to Include |

| MVP (v1.0) | Registration & KYC, wallet, P2P transfer, payment gateway, 2FA, push notifications, and transaction history |

| Version 2.0 | Multi-currency, fraud detection, biometric auth, in-app support, and scheduled transfers |

| Version 3.0+ | Predictive analytics, loyalty engine, smart suggestions, and automated compliance |

Money Transfer App Architecture: How All the Layers Connect

A money transfer app is not a single system; it’s a heap of interdependent layers, each managing a particular responsibility.

From the start, you should get this architecture right, as it determines how well your application scales under load, how swiftly you can pass compliance audits, and how simply you can add features without recreating core infrastructure.

Here is how every layer is structured and what it does in practice:

Layer 1: Frontend Layer

The frontend is what the user interacts with directly – the screens, input fields, buttons, and navigation.

For a money transfer app, this embraces the transfer screen, onboarding flow, notification center, and transaction history.

- Key technologies: Swift (iOS), Kotlin (Android), React Native, or Flutter for cross-platform

- What good looks like: Sub-2-second screen load times, accessibility compliance (WCAG 2.1), and a transfer flow completable in under 4 taps

Layer 2: Backend Layer

The backend is acknowledged as the engine that processes each request the frontend sends, manages user sessions, applies business logic, and coordinates communication between every other layer.

Every time a user taps “Send Money”, the backend validates the request, checks balances, applies transfer rules, and decides whether to proceed.

- Key technologies: Node.js, Python (Django), Java (Spring Boot), or Go

- What good looks like: API response times under 300ms, horizontal scalability to manage transaction spikes, and full request logging for audit purposes

Layer 3: Payment Layer

The payment layer is where money actually moves. It connects your app to banking infrastructure – card networks, payment gateways, and interbank settlement systems. This layer handles the communication between your app and the financial institutions on both ends of a transfer.

- Key integrations: Stripe, Plaid (US), SWIFT (international), Razorpay (India), and Faster Payments (UK)

- What good looks like: Support for numerous payment rails, automatic retry logic on failed transfers, and real-time settlement status updates pushed back to the frontend

Layer 4: Security Layer

The security layer covers every other layer; it is not a separate module but a set of protocols implemented across the entire stack. It ensures that data is encrypted in transit and at rest, that every API call is authenticated, and that sessions are managed securely.

- Key technologies: AES-256 encryption, TLS 1.3, OAuth 2.0, JWT tokens, and tokenization for card data.

- What good looks like: Zero plaintext storage of sensitive data, automatic session expiry, and penetration testing passing OWASP Top 10 benchmarks.

Layer 5: Compliance Layer

With the compliance layer, your app will stay legally operational. It monitors transactions for suspicious patterns (AML), runs identity verification at onboarding (KYC), and generates the reports your regulators want.

In various markets, this layer should be operational before your app rolls out.

- Key integrations: Jumio, Onfido, or Sumsub for KYC; ComplyAdvantage or Refinitiv for AML screening

- What good looks like: Automated KYC approval in under 60 seconds, real-time transaction screening against global sanctions lists, and audit-ready compliance reports exportable on demand

Layer 6: Data Layer

The data layer stores and retrieves user profiles, compliance logs, transaction records, and analytics data, everything. For a money transfer app, data integrity is non-negotiable; each transaction should be recorded precisely, immutably, and in a manner that can be retrieved for regulatory audit or dispute resolution.

- Key technologies: PostgreSQL or MySQL for transactional data, Amazon RDS or Google Cloud SQL for managed cloud hosting, and MongoDB for flexible user data.

- What good looks like: 99.99% database uptime, data residency compliance per jurisdiction (e.g., EU data stored within EU for GDPR), and automatic backups every 24 hours.

How All Six Layers Work Together

Here is a single transaction, sending $500 internationally, traced across all six layers:

| Step | Layer Involved | What Happens |

| 1 | Frontend | User enters amount, recipient, and taps “Send.” |

| 2 | Backend | Request validated, balance checked, transfer rules applied |

| 3 | Security | Payload encrypted, 2FA verified, session authenticated |

| 4 | Compliance | AML check run, transaction screened against sanctions list |

| 5 | Payment | Banking API called, funds debited, transfer initiated to the recipient’s bank |

| 6 | Data | Transaction logged, balances updated, push notification triggered |

Total time from tap to confirmation: 2 to 4 seconds for domestic transfers, up to 48 hours for international transfers, depending on the receiving bank’s settlement cycle.

How to Create a Money Transfer App: 8-Step Development Process (2026)

A money transfer app development is a compliance, product, and business decision launched into one.

The eight steps below cover the complete process from conception to live deployment, with practical timelines and key deliverables at every stage.

Step 1: Market Research and Idea Validation

Timeline: 2 – 4 weeks

Start by validating that your app idea meets a real, underserved need in the market.

The money transfer market is competitive; apps that win do the same by solving a particular issue better than existing solutions, not by creating a generic alternative to PayPal or Wise.

At this stage, answer these four questions:

- Who is your primary user – individuals, businesses, or both?

- What geography or payment corridor are you targeting?

- What is your core differentiator – lower fees, faster settlement, better UX, or a niche audience?

- Who are your top three competitors, and what do users complain about in their app store reviews?

Key Deliverable: A one-page market positioning document that defines your target user, geography, differentiator, and primary monetization model.

Step 2: Define Your App Type and Compliance Path

Timeline: 1-2 weeks

Whatever your app type (P2P, B2B, I2B, or international), it determines your compliance needs before development starts, not after.

Most fintech companies skip this step and face the most expensive mistake in fintech app development.

If you are planning to build a domestic P2P app, you must immediately begin your Money Transmitter License (MTL) applications, which take 6 to 18 months to develop in the US.

If you want to develop an international app, you should identify which payment corridors you will support at app launch and research the regulatory needs for each.

If time-to-market is your major concern, you must partner with a Banking-as-a-Service (BaaS) provider like Treezor or Railsbank to operate under their current licenses while you create your own.

Key Deliverable: A compliance checklist including the licenses needed, data residency needs per target market, and the selected provider.

Step 3: Choose Your Development Approach and Partner

Timeline: 2-3 weeks

You have three options for creating your team:

| Approach | Best For | Avg. Cost | Speed to Market |

| In-house team | Full control, long-term product | Highest | Slowest |

| Outsourced agency | Fixed scope, faster delivery | Medium | Fast |

| IT staff augmentation | Strengthening an existing team | Medium | Medium |

When you evaluate development partners, choose specifically those with fintech experience, not only those with mobile app experience.

A team with a proven track record of building a food delivery app is obviously not qualified to create a regulated financial product.

Ask for their previous fintech projects, their security testing process, and the compliance integration they handled.

Key Deliverable: Signed development agreement with clearly defined timeline, scope, milestone schedule, and IP ownership terms.

Step 4: Plan Your Tech Stack and Architecture

Timeline: 1-2 weeks

Once you finalize your development partner, make the technology decisions that will strengthen your app. Such choices impact performance, maintenance cost, scalability, and the developers’ availability you can hire afterwards.

| Component | Recommended Options |

| Frontend (iOS) | Swift, SwiftUI |

| Frontend (Android) | Kotlin |

| Cross-platform | React Native, Flutter |

| Backend | Node.js, Python (Django), Go |

| Database | PostgreSQL, MySQL, MongoDB |

| Payment APIs | Stripe, Plaid, Razorpay, SWIFT |

| KYC/AML | Jumio, Onfido, Sumsub, ComplyAdvantage |

| Cloud Infrastructure | AWS, Google Cloud, Microsoft Azure |

| Security | AES-256, TLS 1.3, OAuth 2.0, JWT |

Key Deliverable: A finalized tech stack document and system architecture diagram signed off by your lead developer and compliance advisor.

Step 5: Build an MVP First

Timeline: 3-4 months

Always build an MVP, unless you have a regulatory pre-approval or a confirmed enterprise client before you launch a full-fledged product.

A money transfer app MVP should incorporate:

- User registration and KYC verification

- One transfer method (P2P domestic is the simplest starting point)

- Basic transaction history

- Push notifications

- Two-factor authentication

The MVP serves three objectives:

- It gets real user feedback before you overload features nobody uses,

- It offers investors something concrete to evaluate, and

- It gives your compliance team a fully functional product to test against regulatory requirements.

Key Deliverable: A fully functional, testable MVP deployed to a staging environment, with 20-50 ETA users providing structured feedback.

Step 6: UI/UX Design

Timeline: 3-6 weeks (runs parallel to backend development)

UI/UX design for a money transfer app is not only about aesthetics, but it is a direct carrier of transaction completion rates.

Research from Baymard Institute reveals that unclear or complex checkout flows lead 70% of users to abandon a transaction mid-way.

Design priorities for money transfer apps:

- Transfer flow: The route from opening the app to completing a transfer should demand no more than 4 to 5 taps.

- Error states: Every failed transaction requires a clear, plain-language explanation and a recovery approach.

- Trust signals: Display encryption notices, security badges, and regulatory license information, especially for first-time users.

- Accessibility: Support screen reader compatibility, dynamic text sizing, and sufficient colour contrast (WCAG 2.1 AA minimum)

Key Deliverable: A full set of high-fidelity Figma prototypes for every core user flow, reviewed and approved by not less than five representative users from your target audience.

Step 7: Development, Integration, and Testing

Timeline: 4-8 months, depending on complexity

Compared to others, this is the longest phase, where development and testing are carried parallelly, not sequentially.

You must use a CI/CD pipeline that ensures each code commit is tested automatically before it hits the main branch.

Testing for a money transfer app must cover:

| Test Type | What It Covers |

| Functional testing | Every feature works as specified |

| Security testing | Penetration testing, OWASP Top 10 vulnerabilities |

| Performance testing | App handles peak transaction load without degradation |

| Compliance testing | KYC flows, AML triggers, and data storage meet regulatory requirements |

| Payment testing | All transaction types succeed, fail gracefully, and reconcile correctly |

| Device testing | App performs consistently across iOS and Android versions and screen sizes |

Key Deliverable: A signed-off QA report wrapping all test types, with zero critical or high-severity bugs due before submission.

Step 8: Deployment and App Store Submission

Timeline: 2-4 weeks

Submitting a fintech app to the Google Play Store and App Store demands more preparation than a standard app. Both platforms have particular needs for financial applications.

Google Play Store:

- Needs a Financial Services declaration during submission.

- Typically faster review (3-7 days), but has been tightening policies on fintech apps since 2024.

- Demands a publicly accessible, compliant privacy policy and transparent disclosure of all fees.

Apple App Store:

- Requires proof of regulatory compliance or licensing in your target markets.

- A specialist team reviews financial apps – average review time is 7 to 14 days.

- Common rejection reasons can be unclear fee disclosure, missing KYC flow, and insufficient privacy policy.

Post-launch checklist:

- Monitor crash reports and ANRs (Application Not Responding) in the first 48 hours.

- Set up real-time transaction monitoring alerts for your first week of live payments.

- Have a rollback plan ready if a crucial payment processing bug is discovered post-launch.

Key Deliverable: Successfully published app on both stores, with a live transaction monitoring dashboard and an on-call engineering contact for the first 72 hours post-launch.

Development Timeline Summary

| Phase | Step | Timeline |

| Discovery | Market research + compliance planning | 3–6 weeks |

| Planning | Tech stack + partner selection | 3–5 weeks |

| Build | MVP + full development + testing | 4–12 months |

| Launch | UI/UX finalization + deployment | 5–10 weeks |

| Total | Basic app | ~6–8 months |

| Total | Advanced app | ~12–18 months |

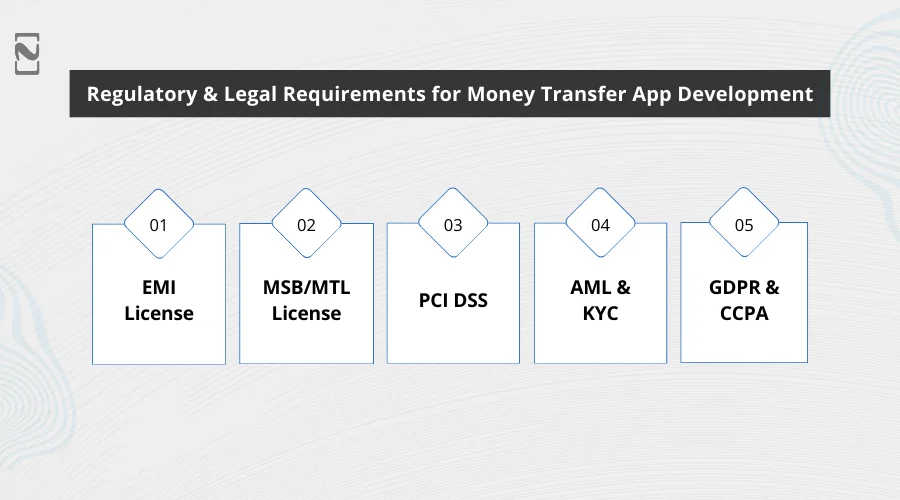

What are the Regulatory and Legal Requirements for Money Transfer App Development

You should create a money transfer app by strictly adhering to applicable compliance with KYC, AML, and data privacy regulations.

A legally compliant money transfer app development ensures proper licensing, safe, and secure payments.

While the above process gives you a sneak peek into how you can develop a money transfer app, it is important to understand the regulatory requirements. Especially when entering the rewarding yet complex fintech app market.

Executing a fintech application requires you to walk hand in hand with the compliance and regulations involved in developing a money transfer app or a digital wallet.

Regulators worldwide have tightened regulations with the rising use of online platforms and international flows.

There are several licenses and regulatory requirements you must have to execute a money transfer app of your own. These include:

-

EMI License

EMI in money transfer app development refers to the Electronic Money Institute, which offers a direct license allowing your platform to offer an integrated digital wallet along with prepaid cards.

It is a must if you plan to develop a money transfer app with a provision to allow a user to store funds; you will need this license in the UK/EU region specifically.

-

MSB/MTL License

Money Service Business and Money Transmitter Licenses are a necessity when you have a mobile app that supports the transmission of funds.

These licenses are time-consuming to obtain; hence, you must apply for them firsthand, as

In the US, you should first register with FinCEN at the federal level, and then get individual Money Transmitter Licenses (MTLs) in each state where your users reside.

As of 2026, 49 states require separate MTLs, with New York’s BitLicense being the most strict, usually taking 12 to 18 months to obtain.

And, the complete multi-state licensing process on average takes 6 to 18 months and should begin well before your development stage starts.

-

PCI DSS

While going through money transfer app development, you must ensure that the solution you build is compatible with PCI DSS (Payment Card Industry Data Security Standard), which is a gold standard for keeping a user’s card data safe and secure across the globe.

This allows a user to rely on the security of your application, helping them feel confident in entering their credit and debit card details without worries.

-

AML & KYC

Anti Money Laundering and Know Your Customer are two of the most important regulatory requirements in today’s market when it comes to money transfer app development.

That is because online platforms are often considered a backdoor for money laundering through fake credentials. By implementing AML and KYC in your money transfer app, you assure the government that your app is legit.

-

GDPR & CCPA

Maintaining user data integrity is of high importance when planning a fintech application.

GDPR (General Data Protection Regulation) in Europe and CCPA (California Consumer Privacy Act) in the US are two primary compliance regulations that state that user data should be encrypted with AES-256 and, in some cases, should be stored on servers that exist in the jurisdiction of the respective government.

Note: If you find obtaining licenses upfront not feasible because of cost, time, or market uncertainty, you can consider partnering with a Banking-as-a-Service (BaaS) provider. BaaS platforms, such as Treezor, Railsbank, or Synapse Finance, permit you to operate under their existing regulatory licenses as a white-label solution, notably diminishing your time to market. This is acknowledged as a common approach for early-stage fintech startups, where they launch under a BaaS umbrella, validate their product with real users, and apply for their licenses once they have transaction volume and investors, supporting cost justification.

With that out of the way, let’s take a look at another crucial factor defining the money transfer app development process, i.e, cost, in the next section.

How Much Does it Cost to Build a Money Transfer App?

The cost to create a money transfer app typically ranges from $25,000 to $200,000 or more, depending on the features of the app.

An MVP is less costly compared to a full-functionality app. On the other hand, a unique app with extensive design and an advanced feature set is way higher than the average.

Therefore, if you want to learn the correct cost to develop a money transfer app, it is recommended to consult a mobile app development company.

To give you a better insight into the money transfer app development cost, let’s look at the major factors.

Factor 1. Complexity

The more features you include, the more complex your app will become and take more time to develop.

| Complexity Level | Estimated Development Cost |

| Basic App | $25,000 – $60,000 |

| Medium App | $60,000 – $120,000 |

| Advanced App | $120,000 – $200,000 |

If you want to build your app within budget, include only essential features to keep the fintech app development cost under control and ensure timely delivery.

Factor 2. Developer location

One of the major factors is the developer’s location. Location highly affects the cost of hiring mobile app developers.

| Location | Hourly Rate Range (USD) |

| United States (Tier 1 Cities) | $100–$250 |

| United States (Tier 2 Cities) | $70–$150 |

| Western Europe | $70–$130 |

| Eastern Europe | $45–$100 |

| South America | $35–$75 |

| South Asia (e.g., India) | $25–$70 |

| Southeast Asia (e.g., Philippines) | $25–$60 |

| Africa | $20–$45 |

In addition to this, the cost to hire Android app developers is very different from the cost to hire iOS app developers or hybrid app developers.

Factor 3. Tools and Technologies

Software development tools and technologies are other factors that add to the cost of building a money transfer app.

| Technology/Tools | Impact on Cost | Cost Range ($25,000 – $200,000) |

| Cross-platform development tools (e.g., React Native, Flutter) | Faster development and reduced codebase maintenance | Can reduce development time by 30-50%, potentially saving $7,500 – $40,000 |

| Pre-built APIs and SDKs | Faster integration with third-party services reduced development time | Can save $5,000 – $20,000 depending on API complexity |

| Cloud-based infrastructure | Scalable, flexible, and cost-effective | Can reduce upfront server costs, but ongoing cloud service fees can add $10,000 – $20,000 per year |

| Open-source libraries and frameworks | Reduced development time, free to use | Can save $5,000 – $15,000 depending on usage |

| Machine learning and AI features | Enhanced security and personalized experiences, but require specialized expertise | Can increase development costs by $20,000 – $50,000 |

| Blockchain integration | Secure and transparent transactions, but complex and expensive to carry out | Can add $30,000 – $80,000 to the development costs |

| Advanced security and compliance tools | Enhanced data protection and regulatory compliance, however, require added investment | Can add $10,000 – $30,000 to the development costs |

Cost estimates are based on average agency rates and vendor pricing as of 2026. Most third-party integrations also include ongoing per-transaction or monthly subscription fees; ensure factoring these into your operating budget, not just your development cost.

Overall, the money transfer app development will cost up to a minimum of $25,000 up to $200,000 or more, depending on the complexity of your app. Plus, the services you want to give to your audience.

Development Timeline Table

| App Complexity | Development Time |

| Basic P2P App | 3-4 months |

| Medium Complexity App | 5-7 months |

| Advanced Fintech App | 8-12 months |

Once you have a clear picture of your development costs, the next important decision is how your app will generate revenue to recover that investment.

How Money Transfer Apps Make Money

Money transfer apps generate revenue through various monetization models depending on their service offerings and target users.

Most fintech platforms integrate transaction-based income with additional premium services to maximize profitability.

Common monetization strategies include:

1. Transaction Fees

You charge a small percentage or flat fee for every transfer. For example, PayPal charges 2.9% + $0.30 per domestic transaction.

2. Currency Exchange Margins

It is the earnings from foreign exchange rate differences in international transfers. For example, Wise earns mainly through transparent FX margins rather than hidden fees.

3. Premium Subscription Plans

It offers businesses faster transfers, higher limits, or extra features. For example, Revolut’s premium plan at $9.99/month offers higher limits and fee-free currency exchange.

4. Merchant Service Fees

Charging businesses for payment processing services. For example, Stripe charges businesses 2.9% + $0.30 per successful card transaction.

5. API & Payment Infrastructure Services

Providing fintech APIs or payment rails to other businesses. For example, Plaid charges per API call for providing bank connectivity to other fintech apps.

6. Interest on Stored Balances

Apps that carry user funds in digital wallets can gain interest by putting those funds in interest-bearing accounts. Revolut and Wise both generate meaningful revenue through this model, making it increasingly significant as wallet adoption grows.

7. Data and Analytics Licensing

Aggregated, anonymised transaction data has important value for market researchers, financial institutions, and advertisers. This is a secondary revenue stream but scales with user volume.

These monetization models help money transfer apps maintain profitability while delivering secure and convenient digital payment services.

Why Choose Nimble AppGenie for Money Transfer App Development?

Since 2017, Nimble AppGenie has been delivering customized fintech solutions, showcasing a portfolio of 350+ completed projects across Android, iOS, and web platforms.

Below is a real example of what that looks like in practice.

Case Study: PayByCheck – Multi-Currency eWallet App

The Challenge: The client wanted a multi-currency eWallet platform that can work smoothly across Android, iOS, and web with real-time currency exchange, secure fund transfers, KYC onboarding, and compliance with financial regulations across various regions.

The biggest technical hindrances were ensuring seamless currency exchange functionality, maintaining powerful transaction security, and developing an intuitive interface that worked for a diverse worldwide user base.

What Nimble AppGenie Built:

- Multi-currency wallet supporting fund addition, transfer, and exchange across currencies

- Seamless KYC onboarding flow for fast, compliant user verification

- Secure transaction infrastructure built on Java (Android), Swift 4 (iOS), and PHP backend

- Commission and limit management system for platform-level control

- Invite and rewards engine to drive user growth organically

- Consistent cross-platform experience across Android, iOS, and web

Tech Stack Used: Java, Swift 4, PHP, MySQL, Adobe XD

Delivered: 5-member team, 3-month timeline

“Pay By Check has been praised for its user-friendly design, comprehensive features, and reliability, marking a milestone in the eWallet and fintech sector.”

– Nimble AppGenie Project Overview, full case study here

Ready to build your money transfer app? Nimble AppGenie brings the same fintech expertise, regulatory awareness, and delivery discipline to every project, whether you are developing a domestic P2P app or a full cross-border payment platform.

Talk to our fintech team

Future Trends in Money Transfer Apps

The future of money transfer apps will be guided by advanced technologies that boost transaction speed, security, and global payment accessibility.

As digital payments continue to evolve, fintech companies are adopting innovative solutions to deliver more seamless financial transactions.

1. AI-Powered Fraud Detection

In digital payment platforms, artificial intelligence is transforming fraud prevention.

AI systems analyze user behavior, transaction patterns, and device activity in real time to recognize and block suspicious transactions before they are processed.

AI adoption is also pacing. Mastercard reports that around 80% of false positives are reduced using AI-based fraud detection models compared to their traditional rule-based system. And this saved merchants billions in wrongly declined transactions yearly.

Integrating AI fraud detection in new money transfer apps from launch is increasingly a basic requirement, despite being a differentiator.

2. Blockchain-Based Cross-Border Payments

Blockchain technology is diminishing the cost and settlement time of international transfers by removing intermediaries and leveraging decentralized ledgers for transaction verification directly between parties.

Ripple’s On-Demand Liquidity (ODL) solution utilizes XRP as a bridge currency and has processed billions in cross-border transactions for financial institutions across 40+ countries.

Blockchain-based rails, for app builders, offer an effective alternative to SWIFT for corridors where traditional settlement is expensive or slow.

3. Biometric Authentication

Biometric technologies, like fingerprint scanning, voice authentication, and facial recognition, are becoming mandatory security features in fintech apps, replacing PIN-based authentication for transaction authorization and login.

Google’s biometric APIs and Apple’s Face ID have made device-level biometric authentication accessible to all mobile app developers with no need to create proprietary systems.

Apps that still depend only on PIN or password authentication are increasingly recognized as outdated by users familiarized with biometric-first experiences.

4. Embedded Finance Solutions

With embedded finance, non-financial businesses can integrate money transfer abilities directly into their platform to help users send money without even leaving the app they are currently using.

Uber’s driver payment system, Shopify Balance, and Amazon Pay are the top examples of embedded finance in action. This trend creates a notable B2B opportunity for money transfer app builders, offering white-label transfer infrastructure to platforms that want to offer financial services without developing them from the ground up.

5. Instant Global Payment Networks

Modern payment infrastructure is facilitating real-time money transfers across financial institutions and countries, replacing batch settlement systems that present delays of 1-3 business days.

In 2023, FedNow launched in 2023, well combined with the EU’s SEPA Instant scheme, and the expansion of UPI in India is creating a patchwork of real-time payment rails that progressive apps are already connecting to.

By 2026, apps that can’t offer instant or near-instant settlement will struggle to compete in markets where it has become the norm.

6. Central Bank Digital Currencies (CBDCs)

Central Bank Digital Currencies are government-issued digital versions of national currencies, and they are moving from pilot programmes to live deployment at pace.

As of 2026, over 130 countries are at some stage of CBDC exploration or development, with China’s digital yuan, India’s e-Rupee, and the EU’s digital euro among the most advanced.

For money transfer app developers, CBDCs portray an opportunity and a disruption risk. Apps that integrate CBDC rails early will get access to government-backed settlement infrastructure with near-zero transaction costs. Those that ignore the trend risk being sidestepped by government-backed payment apps in their core markets.

7. AI-Powered Regulatory Compliance (RegTech)

As global compliance requirements become more complex, a new category of AI-powered regulatory technology, RegTech, is coming forth to automate KYC verification, regulatory reporting, and AML monitoring in real time.

Platforms like Chainalysis, ComplyAdvantage, and Napier use machine learning to detect structuring patterns, screen transactions against global sanctions lists, and generate audit-ready compliance reports automatically.

RegTech integration is rapidly shifting from a nice-to-have to a cost-saving need for money transfer apps operating across multiple jurisdictions, lowering compliance team overhead by up to 50%.

Conclusion

In 2026, creating a money transfer app comes down to three crucial decisions: the type of app that fits your target market, the feature set that justifies your development investment, and the compliance path your geography needs.

This guide includes everything you need to finalize your decisions confidently, from understanding how money transfer apps work and what architecture empowers them, to the step-by-step development process, realistic cost ranges, regulatory requirements across key markets, and the monetization models that drive long-term profitability.

The market opportunity is real, as we discussed $78.40 billion by 2032, but so is the competition. The winning apps are not necessarily offering the most features.

Instead, they are built on the right architecture, designed around a particular user need that existing platforms serve inadequately, and compliant from day one.

If you are set to move from planning to development, Nimble AppGenie’s fintech team is always here to help, from initial scoping to deployment and beyond.

Start your project with Nimble AppGenie.

FAQs

Development timelines rely on complexity. A basic MVP with core features (P2P transfer, KYC, and transaction history) usually takes 3 to 4 months. A medium-complexity app takes 5 to 7 months.

A completely featured advanced app with multi-currency support, fraud detection, and cross-border payments takes 8 to 12 months. App store review and compliance setup add 2 to 4 weeks on top of development time.

The cost of developing a money transfer app varies depending on factors such as the features, technology stack, and the development team’s hourly rate. On average, the cost can range from $25,000 to $200,000 or more for a high-end app.

Money transfer apps generate revenue through 7 main models:

- Currency exchange margins (earning on FX rate differences)

- Transaction fees (a percentage or flat fee per transfer)

- Merchant service fees (charging businesses for payment processing)

- Premium subscription plans (higher limits and features for a monthly fee)

- Interest on stored wallet balances, API and payment infrastructure licensing

- Data and analytics licensing

Most successful apps combine two or more of these models.

A money transfer app works by linking your bank account or digital wallet to a secure payment infrastructure.

After registering and completing KYC verification, the user enters the recipient’s details, picks the amount and currency, and authorizes the transfer utilizing biometrics and PIN.

The app communicates with a user’s bank or payment gateway to move the funds, generally setting domestic transfers within seconds to a few hours and international transfers within 1-2 business days. Sender and recipient receive real-time confirmation on completion of the transfer.

Every money transfer app requires nine core features at launch:

- KYC verification and user registration

- Peer-to-peer fund transfer,

- Digital wallet integration,

- Transaction history,

- Multi-currency support,

- Push notifications,

- Payment gateway integration,

- Multi-language support for international markets,

- Two-factor authentication (2FA)

Advanced features like biometric authentication, fraud detection, and scheduled transfers should be prioritised for version 2.0.

Developers can use various technologies to ensure security in money transfer applications, such as biometric authentication, end-to-end encryption, tokenization, and blockchain integration.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.