In a Nutshell:

- USSD eWallets are growing really fast in Africa because they work on any mobile phone and do not need internet access. This makes digital payments possible for both the mobile phone and its users.

- Mobile money usage in Africa is rising quickly, with over 1 billion registered accounts and more than $1 trillion in yearly transactions. This shows the high demand for USSD-based payment solutions.

- USSD payments are low-cost, fast, and reliable compared to internet or app-based payments. This makes them best for money transfers, bill payments, and airtime purchases.

- USSD eWallet development includes planning, market research, backend setup, telecom and bank integration, security, testing, and ongoing maintenance to ensure smooth operations.

- The cost to build a USSD eWallet app can range from $25,000 to $100,000 or more, depending on features and complexity, usually ranging from basic solutions to advanced platforms with higher security and multi-service support.

- Nimble AppGenie supports end-to-end USSD eWallet app development that helps businesses build secure, scalable, and market-ready payment solutions for Africa.

Africa is growing, opening many opportunities, USSD-driven eWallets being one of them.

While the penetration of smartphones has improved the digital presence of the country, accessibility to the internet and knowledge of the features are still a challenge.

That is why USSD wallets present a great opportunity for enabling online payments for everyone. The service is highly usable as it does not require the internet and is user-friendly.

In this blog, we shall be discussing everything you need to know about the same.

Let’s get right into it

Mobile Payment Situation in Africa

Mobile payments have become a phenomenon across the world, including Africa.

The rise of mobile payments in Africa marks a transformative era in the continent’s economic landscape.

As digital financial services grow, understanding the current state of mobile payments in Africa is crucial for businesses and investors aiming to enter this dynamic market.

Here’s what eWallet statistics tell us about the African market.

- Mobile penetration in Sub-Saharan Africa exceeded 80%, with projections indicating a growth to 90% in the upcoming year. The widespread accessibility of mobile devices is a fundamental driver of mobile payment adoption.

- Kenya is the leading country with 90% of account ownership, followed by Mauritius (89.6%) and Ghana (81.2%), reflecting a robust market for digital mobile money services.

- There has been a significant increase in mobile money accounts, with more than 1 billion registered accounts across Africa by the end of 2024. This represents a nearly 19% increase from the previous year.

- Mobile money transactions in Africa reached $1.1 trillion, highlighting the critical role of mobile payments in daily transactions, from small-scale purchases to large transfers and bill payments.

- Mobile payments have played a pivotal role in enhancing financial inclusion, with the World Bank reporting that 40% of adults in Sub-Saharan Africa who pay their utility bills use a mobile phone, significantly reducing the unbanked population.

What is a USSD in eWallet Apps?

Want to start an eWallet business in Africa?

Well, if you are planning to develop a USSD eWallet, you need to understand the mobile payment technology and its implementations.

The USSD technology is not what you think it is. It has a lot of layers that you must familiarize yourself with before integrating them into your app.

That’s exactly what we shall be doing here:

What is USSD?

Unstructured Supplementary Service Data, commonly known as USSD, is a vital communication technology used across GSM networks to enable interactions between a mobile device and a merchant service provider platform.

This might sound a bit technical, but let’s break it down into simpler terms.

- USSD operates on all cellular phones that support GSM standards, meaning any mobile phone with a SIM card can utilize it.

- This technology enables users to perform transactions through simple shortcodes, all without the need for an internet connection.

- The beauty of USSD lies in its real-time capability, where commands start with an asterisk (*) and end with a hash (#).

- Mobile operators globally use USSD for a variety of services, including account top-ups and balance checks.

- More importantly, this technology has extended to include mobile money services, a key component in Africa’s move towards digital finance.

The best part about a USSD transaction is that it costs less than any other transaction and takes less time. If we compare, a crypto transaction costs up to 183 Naira (including transaction fees and data costs) and can take up to 4 minutes to complete.

Whereas a USSD transaction only costs 6.98 Naira (10 in some cases) and takes only 2 minutes. Not to mention the USSD transactions are definite, i.e., it is either completed or declined. Unlike different transactions that often trigger fear of losing money due to unstable connectivity.

An exemplary model of this is M-Pesa by Vodafone, utilized through Safaricom, which has revolutionized how financial transactions are conducted in Kenya.

In addition, banks and utility companies are adopting USSD to offer seamless, on-the-go services to their customers, enhancing the accessibility and convenience of financial transactions.

USSD Payment Explained

USSD payments function as a robust USSD payment gateway that streamlines the process of transferring funds directly from a user’s bank account without the need to visit a bank, ATM, or kiosk physically.

This gateway not only facilitates easy money transfers but also supports bill payments, mobile recharges, and checking bank balances, among other functionalities.

This method of payment is particularly advantageous in regions with limited access to traditional banking infrastructure or where internet connectivity is unreliable.

By simply dialing a USSD code, users can access a wide range of financial services instantly and securely.

Application of USSD in Mobile Wallets

The integration of USSD with mobile wallets is a game-changer in the financial landscape of Africa.

This synergy allows even the most basic mobile phone users to engage in digital financial transactions. By dialing an e-wallet USSD code, users can initiate transfers, make payments, and manage their accounts effortlessly.

USSD is certainly one of the most preferred payment methods in the African region, especially where internet connectivity is an issue. The convenience that it offers without asking for multiple IDs or verification helps unbanked users to use instant payment processes.

Future of USSD-Driven eWallets in Africa: An Opportunity for Fintech Startups

The landscape of financial services in Africa is ripe for innovation, especially with the integration of USSD technology into eWallet systems.

This presents a tremendous opportunity to start a fintech startup and tap into a growing market hungry for accessible, secure, and efficient digital financial services.

Here’s why fintech startups should consider developing USSD-based eWallet solutions for the African market:

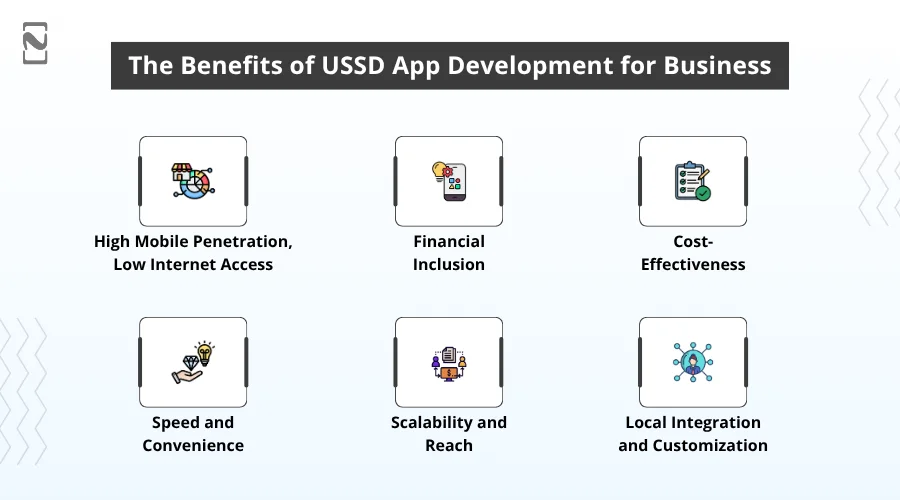

1. High Mobile Penetration, Low Internet Access

Africa boasts high mobile phone penetration, yet many regions suffer from limited internet access.

USSD eWallets operate on basic GSM technology and do not require internet connectivity, making them an ideal solution for widespread adoption of eWallet USSD without airtime across diverse demographic segments.

This is one of the big reasons to develop a USSD payment app.

2. Financial Inclusion

A significant portion of Africa’s population remains unbanked or underbanked.

USSD eWallets can bridge the financial gap by providing essential services like money transfers, bill payments, and savings directly on users’ mobile phones.

This inclusivity can propel economic empowerment and growth.

3. Cost-Effectiveness

For eWallet startups, USSD technology offers a cost-effective way to deploy financial services.

Since USSD sessions are low in data usage and cost, they can be a more affordable option for both the service provider and the user, compared to data-heavy applications..

4. Speed and Convenience

USSD codes allow for instant access to financial services, which is a critical factor in user satisfaction and retention.

Transactions via USSD are completed in seconds, which is essential in time-sensitive situations such as paying for services or transferring money to family and friends.

It’s a good alternative to contactless payments too.

5. Scalability and Reach

USSD technology is supported by nearly all mobile devices, providing startups with a vast potential user base.

This scalability ensures that fintech ventures can rapidly expand their services to new regions and demographics without significant additional costs.

6. Local Integration and Customization

USSD platforms offer flexibility in terms of localization and customization.

This allows startups to tailor their services to meet specific market needs and regulatory requirements.

This includes integrating local languages and conforming to digital payment regulations in various African countries.

Fintech startups venturing into USSD-driven eWallet development are not just investing in a product but are contributing to a broader economic transformation.

By fostering financial inclusion, enhancing transactional efficiency, and ensuring service accessibility, these startups are positioned to lead the charge towards a cashless, digitally inclusive Africa.

What Are the USSD Codes for Existing Mobile Partners in Africa?

Before we jump into the technicalities of USSD codes and how they can be used in an eWallet, here is a list of all the popularly used USSD codes that currently exist.

Keep in mind that the following is not an exhaustive list.

| Country | Mobile Money Provider | Main USSD Code | Typical Function/Service |

| Kenya | M-Pesa (Safaricom) | *334# or older *234# | Money Transfer, Bill Payments (Pay Bill/Buy Goods), Airtime, Loans, Savings. |

| Airtel Money (Airtel) | *222# or *544# | Money Transfer, Airtime, Bill Payments. | |

| Ghana | MTN Mobile Money (MoMo) | *170# | Send Money, Airtime & Bundles, Pay Bills, Financial Services. |

| AirtelTigo Money | *110# | Money Transfer, Bill Payments, Airtime Purchase. | |

| Nigeria | PalmPay | *861# | Transfers, Airtime, Bill Payments (Also bank-specific USSD codes like GTBank *737#, Access Bank *901# are widely used). |

| Tanzania | M-Pesa (Vodacom) | *150*00# | Send Money, Withdraw, Pay Bills, Airtime. |

| Tigo Pesa (Tigo) | *150*01# | Send Money, Withdraw, Pay Bills, Airtime. | |

| Cameroon | MTN Mobile Money | *126# (Previously *126*7*2#) | Send Money, Withdraw, Airtime, Bill Payments. |

| Orange Money | #150*50# or *150# | Send Money, Withdraw, Bill Payments. | |

| Côte d’Ivoire | MTN MoMo | *133# or *123# | Send Money, Withdraw, Bill Payments. |

| Orange Money | #144# | Send Money, Withdraw, Bill Payments. | |

| Uganda | MTN Mobile Money | *165# | Send Money, Withdraw, Bill Payments, Airtime. |

| Airtel Money | *185# | Withdraw, Send Money, Bill Payments, Airtime. |

How to Develop a USSD eWallet Solution?

Knowing everything about how USSDs work and which are the existing players, it’s time to develop an eWallet app backed by USSD technology.

In this section, we shall be going through a step-by-step development process on how to do so.

So, with this being said, let’s get right into it:

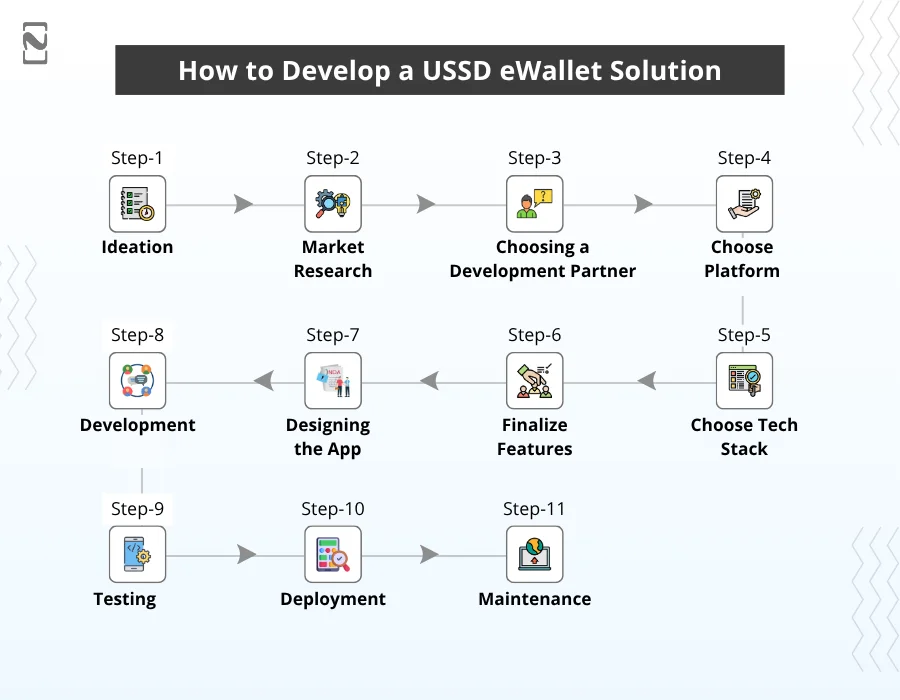

Step 1: Ideation

This initial phase involves defining the core concepts and objectives of the eWallet app. It’s crucial to clarify what problems the app will solve and how it will stand out in the market.

Once this is done, we move on.

Step 2: Market Research

Conducting thorough mobile app market research is essential to understanding the target audience, their needs, and the competitive landscape.

This step helps refine the app’s features based on user preferences and market demands.

Step 3: Choosing a Development Partner

Choosing the right app development partner is critical.

Look for a company with experience in app development and a proven track record in the fintech sector. This will ensure that you have expert guidance throughout the process.

There are various ways you can do this:

- Outsource to a fintech development

- Assemble a House team

- Or hire freelancers

Choosing the right one is very important for various reasons.

In any case, once this is done, it’s time to choose the platform.

Step 4: Choose Platform

Decide whether the app will be developed for iOS, Android app or both.

Considering the widespread use of Android in Africa, a cross-platform approach may be beneficial to reach a broader audience.

Done choosing a platform?

Let’s look at the fintech tech stack now:

Step 5: Choose Tech Stack

Selecting the right technology stack is crucial for building a robust and scalable eWallet app.

Below is a table outlining the typical tech stack for eWallet apps:

| Technology | Use Case |

| Node.js | Backend development |

| React Native | Cross-platform mobile app development |

| MongoDB | Database |

| Redis | Caching to enhance performance |

| AWS | Cloud services |

| Docker | Containerization |

Step 6: Finalize Features

Define key features of the eWallet app, such as user registration, USSD integration, transaction processing, and security measures.

Ensure that the features align with user needs and compliance requirements.

Here’s a list of potential features:

- User Registration and Authentication: Secure sign-up and login processes, with PIN or password protection.

- Balance Check: Allows users to quickly check their account balance through a simple USSD command.

- Money Transfer: Enables users to send money to other users or non-users (via a voucher system) within the network.

- Bill Payments: Facilitates the payment of utility bills, such as electricity, water, and telecommunications, directly from the eWallet.

- Airtime Purchase: Users can buy airtime for themselves or others directly from their eWallet balance.

- Transaction History: Provides users with access to their past transactions for monitoring and budgeting purposes.

- Savings Functionality: Offers an option to save money within the app, including setting up automatic savings plans.

- Loan Access: Integration with microfinance services for users to apply for and receive microloans directly through the app.

- Merchant Payments: Allows users to pay merchants directly using a USSD code at checkout.

- Multi-language Support: Offers multiple language options to cater to diverse user groups across different regions.

- Security Features: Includes end-to-end encryption, session timeouts, and real-time alerts for transactions to ensure user security.

- Customer Support Access: Direct USSD access to customer support for resolving issues or answering queries.

- Rewards and Incentives: Loyalty programs that reward users for frequent use or for referring new customers to the service.

- International Remittance: Facilitates cross-border money transfers, allowing users to send money to recipients in other countries.

- Group Wallets: Enable users to create joint wallets for purposes like group savings or splitting bills.

Also Read: How To Create A Money Transfer App?

Step 7: Designing the App

It’s time to focus on USSD eWallet’s app design.

The design phase focuses on creating an intuitive and user-friendly interface. This includes the layout, graphics, and user experience (UX) design, which are pivotal for user engagement.

Once done designing, it’s time to develop the app.

Step 8: Development

It’s time to develop the USSD app.

During this phase, developers build the application according to the design specifications and tech stack. It includes setting up the backend, integrating e-wallet APIs, and developing the frontend.

Truth be told, this is quite a long process.

Step 9: Testing

Once development is done, it’s time to test the app.

Rigorous mobile app testing is essential to ensure the app is secure, responsive, and user-friendly. This includes functional testing, usability testing, and security audits.

Step 10: Deployment

After testing, the app is deployed to the production environment, where it becomes available to users. This stage may also involve setting up support channels and marketing the app.

Keep in mind that the process to deploy an iOS app to the App Store and an Android App to the Google Play Store is two completely different processes.

Step 11: Maintenance

It’s time to invest in mobile app maintenance services.

Post-launch, it’s important to continually monitor the app for any issues and provide regular updates and improvements based on user feedback and evolving market trends.

How Much Does it Cost to Develop a USSD App?

How much does it cost to develop a USSD eWallet?

The average cost to develop an USSD app ranges from $25,000 to $100,000.

However, determining the cost to develop a USSD app involves considering various factors, including the app’s complexity, the chosen tech stack, the geographic location of the development team, and additional features like security measures or integration with existing systems.

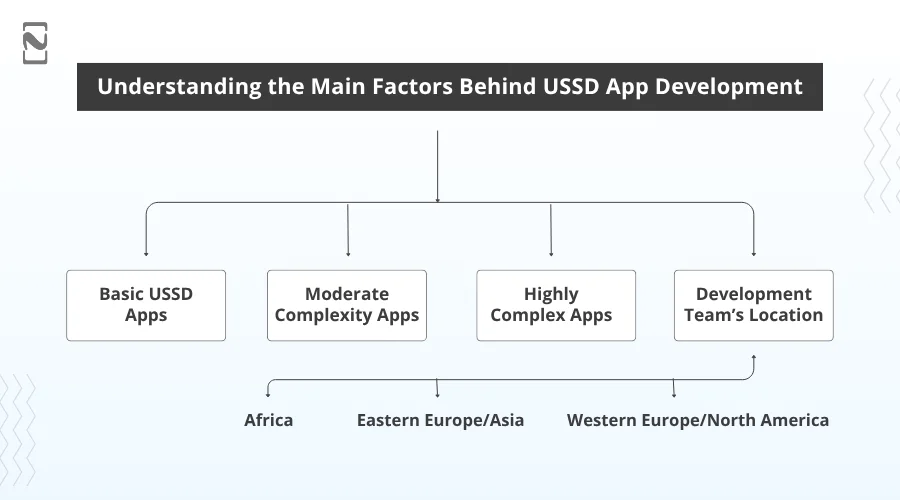

Understanding the Main Factors Behind USSD App Development:

1. Basic USSD Apps

For apps with fundamental functionality such as balance inquiry, mini statements, or basic transactional services, costs can start from $5,000 to $10,000.

These apps require simpler coding and less rigorous security protocols.

2. Moderate Complexity Apps

Apps that include additional features like linking bank accounts, conducting more complex transactions, or including multiple language options can range from $10,000 to $25,000.

This cost range accounts for the added complexity in coding and testing.

3. Highly Complex Apps

For USSD apps that require high-end security features, integration with multiple banking systems, advanced user interfaces, and extensive testing (including compliance with various financial regulations), costs can start at $25,000 and go upwards of $50,000 or more.

4. Development Team’s Location

- Western Europe/North America

Development teams in these regions typically charge higher rates. Therefore, the costs could be at the upper end of the estimates or even higher.

- Eastern Europe/Asia

Teams in these regions often offer more competitive rates without compromising on quality, which might fit mid-range budgets.

- Africa

Local developers familiar with the unique challenges and opportunities within their market might offer competitive rates tailored to the needs of the region, potentially lowering costs.

Startups need to consider these factors when budgeting for the development of a USSD app. Speaking of which, it’s time to look at how you can make money with this app.

How Does a USSD App Make Money?

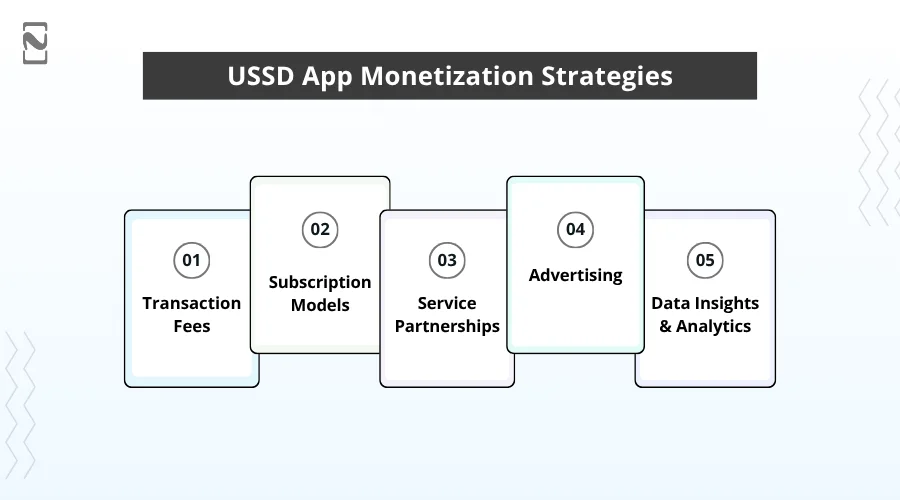

Monetizing a USSD eWallet app presents several viable strategies. These methods not only help generate revenue but also enhance user engagement and retention.

Here are five effective eWallet monetization methods along with their potential revenue implications:

1] Transaction Fees

Charging a small fee for each transaction processed through the app is a common method.

This can include fees for money transfers, bill payments, or airtime purchases. Depending on the volume of transactions, this can be highly lucrative.

For example, a fee of 1% on transactions in an app with $1 million in monthly transactions can generate $10,000 monthly.

2] Subscription Models

Offering premium features under a subscription model can attract more engaged users. Features might include higher transaction limits, lower fees, or access to exclusive services.

Pricing can vary, but a typical subscription might range from $1 to $5 per month, potentially generating substantial recurring revenue based on user base size.

3] Service Partnerships

Collaborating with banks, utility companies, and other service providers to facilitate their USSD-based services can open revenue streams.

Revenue can be earned through a commission for each transaction or through fixed monthly partnership fees.

The potential revenue here depends on the number of partnerships and the volume of transactions facilitated.

4] Advertising

Integrating targeted advertisements into the app can generate additional income. Revenue from advertisements depends on the app’s user base and engagement levels.

For a well-trafficked app, advertising can yield thousands of dollars per month.

5] Data Insights and Analytics

Selling anonymized data and insights about consumer behavior and spending patterns to market research companies or financial institutions can be another revenue stream.

Given the right volume and depth of data, this could potentially earn $1,000 to $10,000 a month, depending on the data’s value and exclusivity.

Case Study: Examples of Successful USSD eWallets in Africa

The adoption of USSD technology in eWallet applications has significantly transformed financial transactions across Africa.

Here are examples of top digital payment apps and how they use USSD technology in the African market:

1. M-Pesa (Kenya)

Launched in 2007 by Safaricom, M-Pesa is perhaps the most renowned USSD eWallet service in Africa.

It allows users to deposit, withdraw, and transfer money, and pay for goods and services through a simple USSD code.

With over 40 million active users, M-Pesa exemplifies the profound effect of mobile financial services on economic activities and financial inclusion with the help of USSD integration services in Kenya.

2. EcoCash (Zimbabwe)

EcoCash is an innovative mobile payment solution for Econet Wireless Zimbabwe subscribers. It supports transactions such as sending money, buying airtime, and paying for goods and services.

Since its launch in 2011, EcoCash has grown to become the dominant financial service in Zimbabwe, with over 6 million subscribers and accounting for the majority of the mobile money transactions in the country.

3. Orange Money (Multiple African Countries)

Orange Money offers a broad range of financial services, including money transfers, bill payments, and savings.

Available in several African countries like Botswana, Cameroon, and Côte d’Ivoire, Orange Money uses USSD technology to enable millions of users to conduct financial transactions conveniently and securely.

This service has become essential in providing access to financial services for people without traditional banking facilities.

With this out of the way, it’s time to look at why this is such a great opportunity.

Future of USSD-Driven eWallets in Africa: An Opportunity for Fintech Startups

The landscape of financial services in Africa is ripe for innovation, especially with the integration of USSD technology into eWallet systems.

This presents a tremendous opportunity to start a fintech startup and tap into a growing market hungry for accessible, secure, and efficient digital financial services.

Here’s why fintech startups should consider developing USSD-based eWallet solutions for the African market:

1. High Mobile Penetration, Low Internet Access

Africa boasts high mobile phone penetration, yet many regions suffer from limited internet access.

USSD eWallets operate on basic GSM technology and do not require internet connectivity, making them an ideal solution for widespread adoption of eWallet USSD without airtime across diverse demographic segments.

This is one of the big reasons to develop a USSD payment app.

2. Financial Inclusion

A significant portion of Africa’s population remains unbanked or underbanked.

USSD eWallets can bridge the financial gap by providing essential services like money transfers, bill payments, and savings directly on users’ mobile phones.

This inclusivity can propel economic empowerment and growth.

3. Cost-Effectiveness

For eWallet startups, USSD technology offers a cost-effective way to deploy financial services.

Since USSD sessions are low in data usage and cost, they can be a more affordable option for both the service provider and the user, compared to data-heavy applications..

4. Speed and Convenience

USSD codes allow for instant access to financial services, which is a critical factor in user satisfaction and retention.

Transactions via USSD are completed in seconds, which is essential in time-sensitive situations such as paying for services or transferring money to family and friends.

It’s a good alternative to contactless payments too.

5. Scalability and Reach

USSD technology is supported by nearly all mobile devices, providing startups with a vast potential user base.

This scalability ensures that fintech ventures can rapidly expand their services to new regions and demographics without high additional costs.

6. Local Integration and Customization

USSD platforms offer flexibility in terms of localization and customization.

This allows startups to tailor their services to meet specific market needs and regulatory requirements.

This includes integrating local languages and conforming to digital payment regulations in various African countries.

Fintech startups venturing into USSD-driven eWallet development are not just investing in a product but are contributing to a broader economic transformation.

By fostering financial inclusion, enhancing transactional efficiency, and ensuring service accessibility, these startups are positioned to lead the charge towards a cashless, digitally inclusive Africa.

Why Choose Nimble AppGenie for USSD Wallet Solutions?

Nimble AppGenie stands as a beacon of innovation in the eWallet apps landscape.

We are the eWallet app development company you are looking for.

With over seven years of experience and a robust portfolio of 350 projects, we have catered to 250+ clients worldwide, delivering platforms that redefine industry standards.

Our notable creations include Cut Wallet, SatPay, and DafriBank, which highlight our capability to transform visionary ideas into functional and impactful solutions.

Entrust us with your next project and join the ranks of our satisfied partners. Let’s innovate together and carve pathways to success in the digital world.

Choose Nimble AppGenie-where your vision meets our innovation.

Conclusion

USSD has been around for years now. Leveraging the same can be a game-changer for many digital payment apps and e-wallets.

Especially in the African region, where internet connectivity is not stable and the number of unbanked users is significant.

To capitalize on the growing number of smartphone users without having to worry about losing out on the existing USSD users, it is recommended that you integrate the shortcodes into your app and allow people to use USSD services through an e-wallet.

Hope these insights on USSD wallet development and implementation help you in the long run. For further services and clarity, feel free to reach out.

Thanks for reading, good luck!

FAQs

A USSD eWallet is a mobile service that enables financial transactions via USSD codes, functioning even without internet connectivity. It’s designed to work on all GSM-supported mobile devices, including basic feature phones.

USSD eWallets incorporate several security measures such as encryption, session timeouts, and two-factor authentication, making them secure for handling financial transactions.

Absolutely. USSD eWallets are specifically designed to operate on any mobile phone that supports GSM, which includes non-smartphones or feature phones.

Users can perform various transactions like sending money, paying bills, purchasing airtime, and checking account balances directly through simple USSD codes.

Fees for using USSD eWallets vary by provider and transaction type but are generally minimal compared to traditional banking methods, enhancing affordability.

To use a USSD eWallet, you must first register with a mobile money provider, set up your account by following the USSD prompts, and then secure your account with a PIN.

Most providers offer comprehensive customer support for their USSD eWallet services, including phone support, SMS inquiries, and sometimes online chat options.

While USSD eWallets are generally region-specific due to local partnerships and regulations, some providers may offer services that support international transactions.

Transactions via USSD eWallets are processed instantly, offering real-time financial interactions that are ideal for urgent payments and remittances.

Entering an incorrect USSD code typically results in an error message, prompting you to re-enter the correct code. Repeated errors may require you to restart the transaction process or contact customer support for assistance.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.