Fintech as an industry has seen immense growth over the past two decades. People from all walks of life, in one way or another, are using fintech services today.

The services are widely adopted by the users, making fintech a global phenomenon.

However, this acceptance and adaptation also brings along several challenges and risks. Especially when matters are associated with finances and money.

People using online services to manage their finances are directly prone to several security issues. That is because with a third-party platform being involved in the transactions, all your personal and banking data is up for exploitation.

However, that usually can’t happen thanks to fintech regulations and compliance that are put in place by respective bodies from around the globe, in different regions. These fintech regulations and compliances allow individuals to stay safe from all the possible scams.

In this post, let us take a look at fintech regulations and compliance and understand the different factors related to the same.

We will also be looking at the major risks in fintech that can be minimized using these compliances. And exactly which organizations are responsible for implementing these regulations in the wider field of fintech?

What is Meant by Fintech Regulations & Compliance?

Fintech regulations and compliance refer to the norms that allow fintech businesses to mitigate the risks and make the entire experience more secure than ever.

There are different entities involved in a fintech transaction. There are fintech app users, service providers, and then there are facilitators.

All of these have their respective limitations and standard risks that they have to manage. Fintechs should effectively manage arrears and take actions to mitigate risks.

When we talk about building a fintech solution, we often pay attention one features, design, and functionalities. One thing that often goes unnoticed is regulating fintech apps and how compliance will be implemented.

Fintech regulations and compliance serve as the key adhesive that keeps user trust and service integrity intact for any financial institution.

“Regulations and compliance are essential for fintech companies to ensure secure and trustworthy operations, helping them remain competitive in the market.”

Why are Fintech Regulations Important?

Fintech and regulation go hand in hand. Wherever there is financial technology involved, there will be a set of regulations that you must meet. These ensure that the integrity of each operation that involves your fintech solution, staff, and customers remains intact.

Here are some reasons why fintech regulations play a significant role:

1. Strengthens Consumer Protection

Fintech compliance regulations are super important for fintech app security.

You see, fintech compliance deals with fraud and abuse. Without regulations, bad actors could easily exploit digital tools for scams, money laundering, and other illegal activities.

Regulations help create safeguards, requiring KYC/AML measures and data security practices to protect consumers. Regulations also promote transparency and fairness. Complex financial products and services can be confusing for users.

Regulations ensure clear disclosure of terms, risks, and fees, empowering consumers to make informed decisions and avoid unfair practices.

2. Maintains Financial Sanctity

For financial businesses that are not regulated, it is very easy to exploit customers. This defies the whole purpose of offering financial services in the first place, as people look to fintech services when they are struggling.

Unregulated growth in certain areas of fintech could create bubbles with the potential to destabilize the broader financial system. Regulations set prudential standards for capital adequacy, risk management, and liquidity to prevent such crises.

In addition, global fintech regulations act as a barrier to such activities, ensuring the smooth flow of legitimate funds and fostering trust in the system.

3. Opening the Market for All

The financial services and fintech market is all about the funds you have and the type of interest rates you offer.

Unregulated factors can allow industry giants to dominate the market and create monopolies.

Which is why it is important to have regulations that stop the market from behaving in a certain way.

Small fintech companies can embrace new technologies to innovate how people use services.

Regulation and compliance create a fair playing field for all, allowing all types of financial institutions to offer services and grow.

Regulations are essential for addressing data privacy, security, and fair treatment, fostering trust, and encouraging the adoption of innovative fintech solutions.

Who Regulates Fintech Companies Around the World?

Looking at the crucial role that fintech compliance and regulations play, you may be wondering what regulatory bodies help in implementing them. Building regulations for fintech companies is not something that is done regularly, however, the amendments are a regular occurrence.

There are several authorities responsible for regulating tech companies. Some have global regulatory authority over these fintech companies, while others have authority only in their jurisdiction.

Please see the detailed breakdown of the same below:

| Region | Country | Regulatory Body/Authority | Scope of Regulation |

| Global | International Organization for Standardization (ISO) | Data privacy | |

| International Telecommunication Union (ITU) | Data privacy | ||

| Financial Action Task Force (FATF) | Anti-Money Laundering (AML) | ||

| North America | United States | Securities & Exchange Commission (SEC) | Investments, crowdfunding, digital assets |

| Commodity Futures Trading Commission (CFTC) | Derivatives and futures | ||

| Consumer Financial Protection Bureau (CFPB) | Consumer protection | ||

| Office of the Comptroller of the Currency (OCC) | National banks and federal savings associations | ||

| State-level regulators | Specific activities, such as money transmission | ||

| Canada | Canadian Securities Administrators (CSA) | Investments and Securities | |

| Financial Consumer Agency of Canada (FCAC) | Consumer protection | ||

| Office of the Superintendent of Financial Institutions (OSFI) | Banks and financial institutions | ||

| South America | Brazil | Central Bank of Brazil (BCB) | Financial institutions and payment systems |

| Brazilian Securities and Exchange Commission (CVM) | Investments and Securities | ||

| Colombia | Superintendencia Financiera de Colombia (SFC) | Financial institutions | |

| Banco de la República (Central Bank) | Monetary policy and payment systems | ||

| Europe | European Union | European Banking Authority (EBA) | Banking and payments |

| European Securities and Markets Authority (ESMA) | Investments and Securities | ||

| National regulators within each member state | Various financial activities | ||

| Non-EU countries | Similar independent or centralized regulatory structures | Varies by country, e.g., FCA in the UK | |

| Asia | China | People’s Bank of China (PBOC) | Financial institutions and payment systems |

| China Securities Regulatory Commission (CSRC) | Investments and Securities | ||

| India | Reserve Bank of India (RBI) | Banks and payment systems | |

| Securities and Exchange Board of India (SEBI) | Investments and Securities | ||

| Japan | Financial Services Agency (FSA) | Financial institutions and activities | |

| Various structures by country | Varies, often central banks and finance ministries | ||

| Africa | South Africa | South African Reserve Bank (SARB) | Monetary policy and financial stability |

| Financial Sector Conduct Authority (FSCA) | Financial institutions and activities | ||

| Kenya | Central Bank of Kenya (CBK) | Monetary policy and financial stability | |

| Capital Markets Authority (CMA) | Investments and Securities | ||

| Nigeria | Central Bank of Nigeria (CBN) | Monetary policy and financial stability | |

| Securities and Exchange Commission (SEC) | Investments and Securities | ||

| Other countries | Similar structures emerging | Varies, often central banks and finance ministries | |

| Middle East | United Arab Emirates | Central Bank of the United Arab Emirates (CBUAE) | Monetary policy and financial stability |

| Securities and Commodities Authority (SCA) | Investments and Securities | ||

| Financial Services Regulatory Authority (FSRA) | Specific financial activities | ||

| Saudi Arabia | Saudi Arabian Monetary Authority (SAMA) | Monetary policy and financial stability | |

| Capital Markets Authority (CMA) | Investments and Securities |

Fintech Regulations & Compliance in the USA & Europe: An Overview

Regulatory bodies for fintech companies differ by region, resulting in varied compliance requirements.

People often get confused in the intricacies of fintech regulations US and fintech regulations UK, which in itself is a tough nut to crack. While that is a discussion for another day, this section highlights key regulations in the US and EU essential for fintech services.

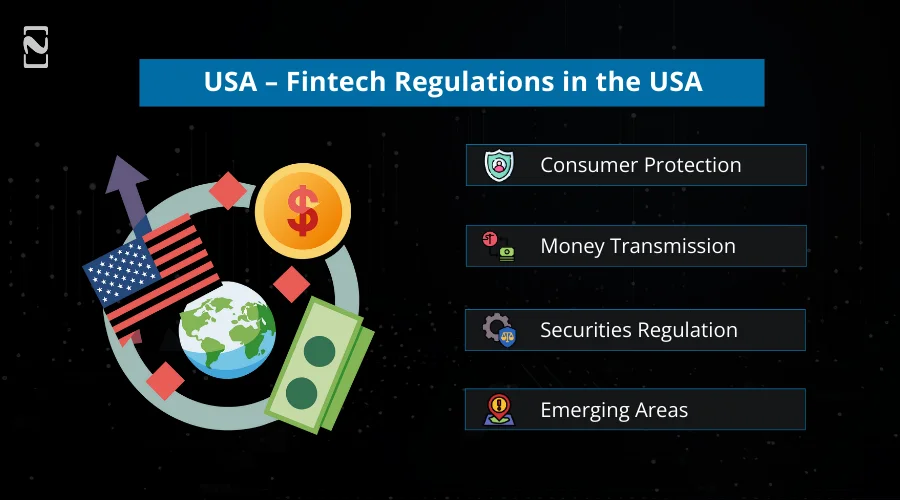

► USA – Fintech Regulations in the USA

Let’s start with Fintech regulation in the United States of America. Similar to the EU, navigating fintech regulations in the US involves understanding a complex patchwork of laws across different levels and agencies.

Here’s a closer look at specific regulations in key areas:

Consumer Protection :

- Gramm-Leach-Bliley Act (GLBA): Safeguards financial privacy and requires data security measures for customer information.

- Fair Credit Reporting Act (FCRA): Governs the collection, dissemination, and use of consumer credit information, impacting credit scoring, reporting, and lending practices.

- Fair Debt Collection Practices Act (FDCPA): Regulates debt collection activities, limiting harassment and unfair practices.

Money Transmission :

- Money Transmitter Licenses: Most states require a license to transfer money, with varying requirements depending on the specific activity and volume.

- Bank Secrecy Act (BSA) / Anti-Money Laundering (AML): Mandates Know Your Customer (KYC) procedures, transaction monitoring, and suspicious activity reporting to combat money laundering and terrorist financing.

Securities Regulation :

- Securities Act of 1933: requires registration and disclosure for offerings of securities, which applies to fintechs selling investment products or crowdfunding platforms.

- Securities Exchange Act of 1934: regulates trading activities and broker-dealers, impacting fintechs offering investment advice or trading platforms.

Emerging Areas :

- Consumer Financial Protection Bureau (CFPB): Issues regulations and enforces consumer protection laws impacting various fintech activities, including data privacy, fair lending, and unfair practices.

- Office of the Comptroller of the Currency (OCC): Proposes a “fintech charter” for specific types of fintech companies, aiming to create a dedicated regulatory framework.

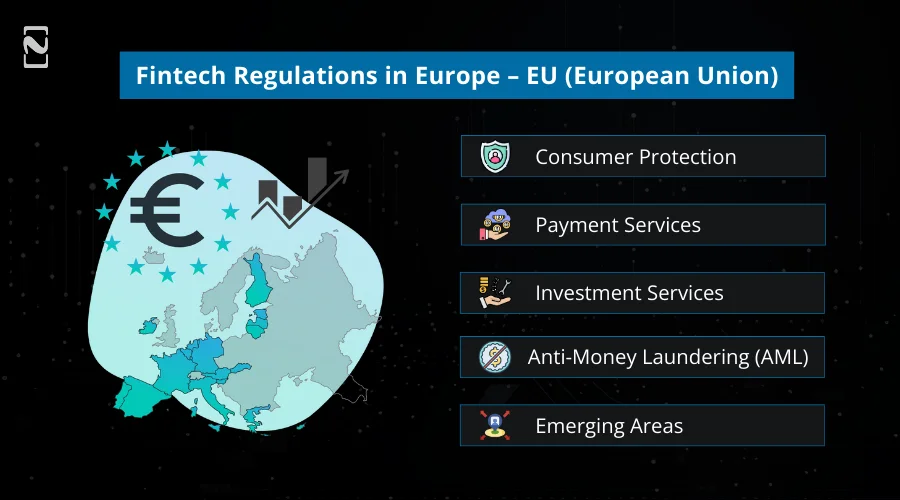

► Fintech Regulations in Europe – EU (European Union)

With U.S. fintech regulations out of the way, let’s look at fintech regulation for the European Union.

Let’s start with some of the generated ones, then we shall go with the ones from each section.

Consumer Protection :

- General Data Protection Regulation (GDPR): Requires strong data security and privacy measures, impacting data collection and usage practices across all fintech activities.

- Payment Account Directive (PAD): Ensures transparency and consumer protection for payment accounts, including basic bank accounts and e-wallets.

- Mortgage Credit Directive (MCD): Sets standards for fair mortgage lending practices, impacting fintechs offering mortgage-related services.

Payment Services :

- Payment Services Directive 2 (PSD2): Enables open banking by mandating banks to open up access to customer data with their consent, facilitating innovative payment solutions.

- Electronic Money Directive (EMD): Regulates the issuance and distribution of electronic money, relevant for fintechs offering e-money products or services.

Investment Services :

- Markets in Financial Instruments Directive II (MiFID II): Regulates investment firms and their activities, impacting fintechs offering investment advice, portfolio management, or securities trading.

- Prospectus Regulation: Sets requirements for prospectuses used to offer securities to the public, impacting crowdfunding platforms and investment token offerings.

Anti-Money Laundering (AML) :

- AML Directive 5: Requires customer due diligence, transaction monitoring, and reporting of suspicious activity to prevent money laundering and terrorist financing, applicable to all financial institutions, including fintechs.

- Upcoming AML Package 6: Expands AML/CFT regulations, potentially introducing stricter requirements for crypto-assets and virtual asset service providers.

Emerging Areas :

- Markets in Crypto-Assets Regulation (MiCA): Coming into effect in 2025, it will regulate crypto-asset issuances, trading platforms, and custodial wallets, providing clarity and harmonization for crypto-focused fintechs. It will also help provide a clear framework for how crypto taxes are handled, making things simpler for businesses and users involved in digital asset transactions.

- Digital Operational Resilience Act (DORA): Sets standards for digital resilience and incident response for financial institutions, impacting fintechs’ reliance on technology and their security practices.

Now that we are done with the fintech regulatory checklist for two of the most important fintech markets, it’s time to look at the specific regulations for fintech niches.

Regulations & Compliance for Different Fintech Businesses

Several fintech ideas branch into different niches or sectors. Each of them has different regulations and compliance for fintech. For instance, Banking apps are a perfect example of fintech and bank regulation clashing together.

You see, a bank wants the user to be physically present or verify a data again and again, while banking apps are all about going together. Hence it is definitely something you should take care of.

Let’s look at them with a few examples :

| Sector | Prominent Regulations | Examples |

| eWallet Apps | PSD2 (Europe), Payment Services Directive (PSD) (various countries), AML/KYC requirements | Mobile wallet apps, P2P payments, and online money transfer |

| Loan Lending Apps | Consumer Financial Protection Bureau (US), Fair Lending Act (US), Dodd-Frank Act (US) | Peer-to-peer lending apps, online loan platforms, and alternative lending solutions |

| Investment Platforms | Securities and Exchange Commission (SEC) regulations (US), MiFID II (Europe), crowdfunding regulations | Robo-advisers, online investment platforms and alternative investment platforms |

| InsurTech Apps | InsurTech regulations (varying by country) and AML/KYC requirements | InsurTech platforms offering parametric insurance and peer-to-peer insurance models |

| Wealth Management | Financial Industry Regulatory Authority (FINRA) regulations (US), Investment Advisers Act (US), GDPR (Europe) | Online wealth management platforms and digital asset advisors |

| Crowdfunding Platforms | Jumpstart Our Business Startups Act (JOBS Act) (US), crowdfunding regulations (varying by country) | Equity crowdfunding platforms, debt crowdfunding platforms, and reward-based crowdfunding platforms |

The main point is to recognize that all regulations are designed to ensure fairness in the fintech industry.

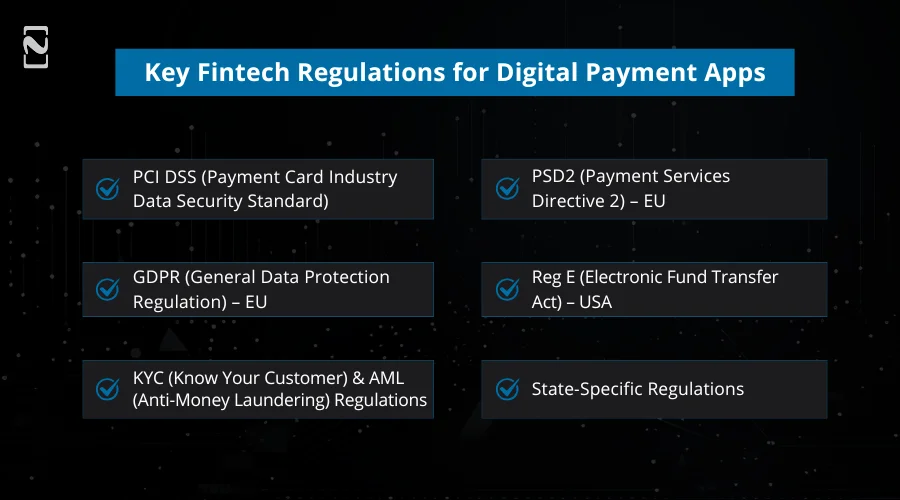

Key Fintech Regulations For Digital Payment Apps

Recently, one can easily observe the rising use of digital payments, which often raises the question of safety and security.

There are several distinct mobile payment regulations that must be followed when building a fintech mobile payment platform.

These regulations include :

♦ PCI DSS (Payment Card Industry Data Security Standard)

Let’s start with PCI DSS.

It is a global standard that outlines security measures for handling cardholder data.

For digital wallet apps that store, process, or transmit credit card information, adherence to PCI DSS is mandatory.

This includes requirements for encryption, access control, and vulnerability management, ensuring that users’ payment information is protected at all times.

♦ PSD2 (Payment Services Directive 2) – EU

PSD2 is yet another important EU mobile payment regulation.

Specifically for the European market, there is a directive that regulates payment services and payment service providers.

It introduces stringent security requirements, including Strong Customer Authentication (SCA), and promotes the development of open banking.

This allows third-party developers to create financial services that work seamlessly with banks’ systems, thereby fostering innovation and competition.

♦ GDPR (General Data Protection Regulation) – EU

GDPR (General Data Protection Regulation) is a tricky one.

While not exclusively a mobile payment regulation, GDPR has significant implications for digital wallet apps in terms of how they collect, store, and use personal data.

It emphasizes user consent, data minimization, and the right to data portability, ensuring that users’ privacy is protected in all digital transactions.

♦ Reg E (Electronic Fund Transfer Act) – USA

In the United States, Regulation E outlines rules for electronic payments, including provisions for error resolution and consumer liabilities in case of unauthorized transfers.

For digital wallet providers, this means implementing systems that allow users to report issues promptly and ensuring that their rights are protected during electronic fund transfers.

This is what makes it one of the most important regulations in mobile payment.

♦ KYC (Know Your Customer) and AML (Anti-Money Laundering) Regulations

Globally, KYC and AML regulations are critical for preventing fraud and financial crimes.

Digital wallet apps are required to verify the identity of their users and monitor transactions for suspicious activity.

Compliance with these digital payment regulations not only safeguards the financial system but also builds trust with users by ensuring the legitimacy of transactions.

♦ State-Specific Regulations

Now, when we are speaking of not just eWallet, but building any fintech app, one must understand that there are a lot of state-specific online payment regulations.

In many countries, including the United States, individual states may have their own regulations governing mobile payments.

For instance, the New York Department of Financial Services has specific cybersecurity requirements for financial services companies.

Digital wallet developers must be aware of and comply with these local regulations, in addition to federal standards.

| State | Regulation/Compliance | Brief Description |

| California | California Consumer Privacy Act (CCPA) | Gives consumers more control over the personal information businesses collect about them. |

| New York | NYDFS Cybersecurity Regulation | Requires financial services institutions to establish and maintain a cybersecurity program. |

| Massachusetts | Standards for the Protection of Personal Information | Establishes minimum standards for safeguarding personal information contained in both paper and electronic records. |

| Illinois | Biometric Information Privacy Act (BIPA) | Regulates the collection, use, safeguarding, handling, storage, retention, and destruction of biometric identifiers and information. |

| Texas | Texas Business and Commerce Code Chapter 521 | The Act requires businesses to implement and maintain reasonable procedures to protect sensitive personal information. |

| Nevada | Nevada Revised Statutes Chapter 603A | The Act includes provisions on the protection of personal information and the requirements for data breaches. |

| Florida | Florida Information Protection Act of 2014 (FIPA) | Expands the requirements on businesses to protect personal information and to provide notice to individuals when there is a data breach. |

In navigating the landscape of mobile payment regulations, digital wallet app service providers must stay informed and proactive.

Ensuring compliance not only involves understanding these key regulations but also continuously adapting to new standards and legal requirements as the digital payment ecosystem evolves.

For users, the adherence of a digital wallet app to these fintech regulations is a hallmark of trustworthiness and reliability, making it an essential factor in choosing a digital payment service.

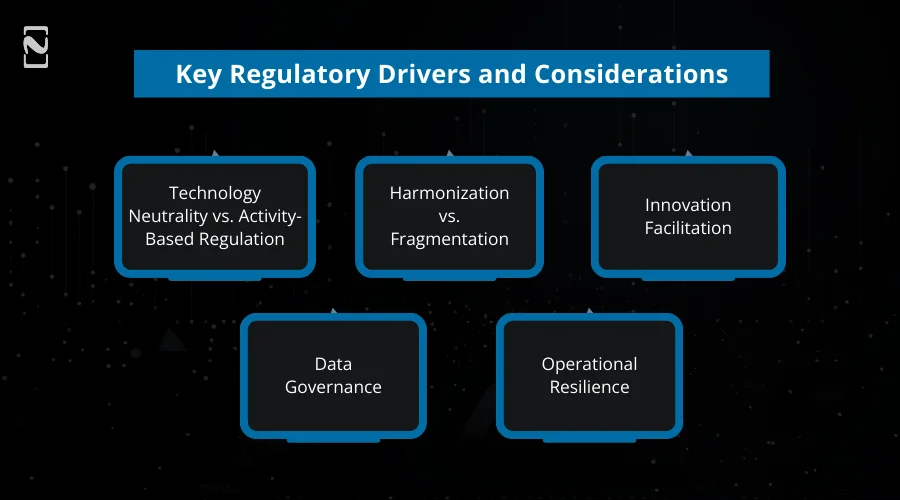

Key Regulatory Drivers and Considerations

Explore the essential compliance factors that influence fintech innovation, from consumer protection laws to digital finance regulations.

➤ Technology Neutrality vs. Activity-Based Regulation

Regulators increasingly focus on the activity a fintech company performs (e.g., lending, payments, investment advice) rather than the technology used, but new technologies (like AI, DLT/blockchain) often require specific considerations.

➤ Harmonization vs. Fragmentation

While regions like the EU strive for harmonization across member states, jurisdictions like the US maintain a more fragmented, multi-level regulatory approach.

➤ Innovation Facilitation

Regulators are exploring “sandboxes,” innovation hubs, and specific charters to allow new products and services to be tested in a controlled environment.

➤ Data Governance

The increasing use of data necessitates robust regulations around privacy, security, and ethical use of data.

➤ Operational Resilience

As financial services become more digital, ensuring the stability and resilience of technology systems is paramount.

All in all, if you plan to launch a fintech solution or any type of financial service of your own. Then you have to build an infrastructure that meets all the compliance requirements. If you plan to start a fintech company, it should be built in a way that meets all the regulatory requirements.

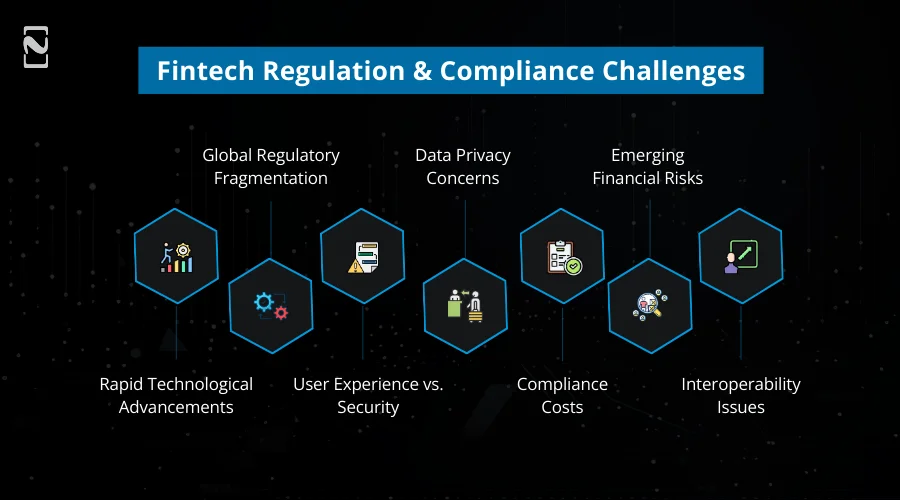

Fintech Regulation & Compliance Challenges

Navigating the regulatory landscape presents a unique set of challenges for fintech and mobile payment providers, as well as businesses that are planning to enter the market.

These fintech regulation challenges are not just about compliance; they also involve adapting to a rapidly changing technological environment, meeting user expectations, and ensuring the highest standards of security and privacy.

Let’s explore some of these key challenges in detail :

1. Rapid Technological Advancements

The pace at which mobile payment technology evolves often outstrips the speed at which regulations can be updated, creating a gap between innovation and legislation.

For digital wallet apps, this means constantly balancing between adopting the latest technologies, like blockchain or NFC mobile payments, and ensuring these innovations remain within regulatory boundaries.

2. Global Regulatory Fragmentation

With no universal standards for mobile payment regulations, companies face the daunting task of navigating a patchwork of international, national, and local regulations.

This fragmentation can significantly increase the complexity of developing and scaling digital wallet solutions across different markets, requiring a tailored approach to compliance in each jurisdiction.

3. User Experience vs. Security

Digital wallet regulations often mandate stringent security measures, like Strong Customer Authentication (SCA), which can sometimes be at odds with the seamless user experience digital wallet users have come to expect.

Striking the right balance between robust security protocols and a frictionless user experience is a continuous challenge for app developers.

4. Data Privacy Concerns

In an era where data is a valuable commodity, digital wallet apps must handle user data with the utmost care, complying with regulations like GDPR in the EU.

Ensuring user privacy while providing personalized and efficient services is a delicate balancing act, compounded by the risk of data breaches and cyberattacks.

5. Compliance Costs

The cost to develop an e-wallet app on its own is huge.

In addition to this, meeting regulatory requirements can be costly, especially for startups and smaller companies.

The costs associated with compliance, such as implementing secure payment infrastructure, conducting regular audits, and obtaining necessary certifications, can be significant.

These costs can impact innovation budgets and the overall affordability of digital wallet services.

6. Emerging Financial Risks

The digital payment ecosystem is susceptible to new and evolving financial risks, including fraud, money laundering, and cyber threats.

Staying ahead of these risks while ensuring compliance with AML and KYC regulations requires continuous vigilance, sophisticated risk management strategies, and often substantial investment in security technologies.

7. Interoperability Issues

As the digital payments ecosystem becomes more complex, ensuring interoperability among different payment systems, banks, and regulatory frameworks becomes increasingly challenging.

This not only affects the user experience but also complicates compliance efforts, as digital wallets must be designed to function seamlessly across diverse financial infrastructures.

How to Build a Fintech Solution that Adheres to all the Regulations & Compliance?

Curating an app that aligns with the demands of fintech law and regulations is certainly tricky. To have all these compliance requirements met, your solution should be designed and developed accordingly.

When your application collects data, it’s vital to ensure it is stored securely and used properly. Your solution must also comply with all relevant regulations regarding privacy and customer interactions. Being new in the industry, the majority of entrepreneurs are unaware of all the practices they have to comply with.

Hence, the ideal way to manage all the regulations and compliance is to hire a fintech app development company that has enough experience to guide you through.

At Nimble AppGenie, we often receive questions about our compliance and regulatory practices. We take pride in our highly stable solutions, designed to ensure easy regulatory compliance.

Our experience allows us to build precise fintech apps that support business growth while effectively managing compliance and regulations.

Conclusion

Compliance with fintech regulations is crucial for both industry integrity and your business operations, as government bodies oversee this process. These regulations prevent malpractice, discourage the misuse of power for unfair advantages, and promote innovation that improves services for all.

Different compliance and regulatory requirements depend on the region in which your fintech application is built and offered. Hence, you need to pay attention to how the application is developed. Hiring a team that understands compilation can help you achieve better results in no time.

I hope this information helps you understand the fintech regulations and digital payment compliance. That will be all for this post. Thanks for reading, good luck!

FAQs

Emerging trends in fintech regulation include :

- Consumer Protection: Safeguarding consumer rights in financial technology.

- Regulatory Convergence and Flexibility: Harmonizing and adapting regulations across jurisdictions.

- Open Banking and Data Sharing: Allowing consumers to share their financial data for improved competition.

- Addressing Regulatory Uncertainty: Managing the complexities of new technologies like decentralized finance (DeFi) and artificial intelligence (AI).

- Global Regulatory Collaboration: Enhancing cooperation among regulatory bodies worldwide.

These trends aim to support innovation while protecting consumers.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.