AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

In a Nutshell:

- Fintech refers to financial startups (like Revolut) using technology to disrupt or improve traditional financial services.

- Techfin refers to established tech giants (like Google, Apple, or Amazon) using their massive data sets to offer financial products.

- The primary difference lies in the origin: Fintech starts with finance and adds tech, while Techfin starts with tech and adds finance.

- Fintechs focus on creating new customer experiences, whereas Techfins focus on leveraging existing user ecosystems to upsell financial services.

- Both models are driving the industry toward a future where financial services are more personalized, data-driven, and invisible.

The financial services industry has undergone a complex transformation in the past decade.

From brick-and-mortar institutions to going digital, financial services as we know them have come a long way.

Technology has had a significant role to play in this transformation, as it has continually evolved the way financial services are being offered.

From digitising payments to simplifying banking services, technology has given it all.

Another interesting thing that the combination of financial services and technology has given is the way these two niches come together to form a business.

Two terms, Fintech and Techfin. What are they? How are they different or related? Let’s explore them both in this post and understand the key differences.

Without further ado, let’s get started!

How are Fintech & Techfin Defined?

As the terms suggest, both fintech and techfin are formed by combining financial services and technology. The key difference between these two is what came first for a business.

Sounds confusing? Well, let’s dig a bit deeper by defining both terms individually.

• Fintech

The more popular term among the two, a solution or a company can be termed fintech if it was originally a financial institution that has layered its services with technology for greater convenience and wider reach.

• Techfin

On the other hand, if a tech giant has developed enough infrastructure to support financial services and added it to their product/service portfolio, it can be called a techfin company. The growing demand for financial services is definitely a trend that many tech giant companies have already leveraged.

So if we look closely and simplify things, the terms fintech and techfin are created on the basis of the chronology of the services. If a company was into financial services first and then came into tech solutions, it is a fintech, whereas if a company was into tech and came up with its financial services, it is a techfin.

A lot of doubts might have already been cleared with the definition of these terms. However, understanding them both, how they function, and what type of solutions they can offer is a different ballgame altogether.

In the upcoming sections, let’s explore both of them individually by following their journeys and where exactly they are heading to get a better understanding of fintech and techfin.

What is Fintech? An Overview

Financial technology is one of the fastest-growing fields of all time. Fintech services, though they have only emerged in the late 20th and early 21st century, have created a huge market with hundreds of big players generating billions of dollars.

The current fintech statistics state that the scope is certainly growing, with 10,264 fintech companies coming from the US alone.

Financial technology got really popular with the penetration of smartphones and seamless internet connectivity. Banks and financial service providers have gone digital by introducing their own technical solutions to reach the masses.

However, this digital transformation of financial services definitely took a bit of time, effort, and infrastructure. You see, fintech is not just about digitising money or financial services; it is changing the way people interact with financial services, how the money moves, and how investments and insurances are processed.

Today, fintech has its own branches that can be further explored for services that are not exactly banking or payment-related but do involve money transactions. The ecosystem of fintech services has grown exponentially.

To understand fintech in more detail, let’s explore it further by identifying the ecosystem that makes it all possible and its characteristics.

FinTech Ecosystem: What Makes it All Possible?

Fintech, while it seems like a single entity, works through a combination of several key players. There’s a complete ecosystem that makes it possible for a fintech company to survive and thrive.

Overall, the FinTech ecosystem consists of various players, including people who want to start a fintech startup, established financial institutions, technology providers, and regulatory bodies.

Key components include:

1. Startups

The first key player in the ecosystem is the startup or the business that takes the initiative of building the fintech solution. You see, without a company coming forward, there will be no product that you can trust. Also, startups today are more about technology and convenience than anything else, making them an important part of the fintech ecosystem.

2. Traditional Banks

Next up, we have traditional banks that play a crucial role in powering the financial side of a fintech solution. These banks are also coming forward to adapt to the rising needs of digital finance services. Either way, a traditional bank is a key player and plays a crucial role in enabling the ecosystem.

3. Development & Tech Companies

Providing infrastructure and tools for innovation, fintech app development services and companies that provide technologies are also a key part of the ecosystem These are the backbone of the entire fintech ecosystem as it ensures that whatever type of solution is required can be developed and deployed.

4. Regulators

When dealing with financial services, people tend to worry about their funds being at risk. Not to forget, several fraudulent activities can be run from an unregulated finance app. Ensuring compliance with financial laws and protecting consumers, regulators play a super crucial role in enabling smooth functioning of the fintech ecosystem.

5. Investors

Funding for the growth and expansion of FinTech ventures, investors are the backbone of all the operations that enable a fintech solution to exist. These investors are highly invested in enabling the solutions and make it possible for a startup to stay put on their vision. This further allows all the parties to perform their functions better, keeping the ecosystem intact.

With the help of these contributing parties, a fintech company strives to attain certain characteristics that make it more appealing to investors and users.

FinTech is characterized by its focus on innovation and customer-centric solutions. Key characteristics include:

- User-Friendly Interfaces

- Accessibility

- Efficiency

- Security

- Personalization

Offering all these features and simplifying the way people fulfill their financial requirements makes fintech a complete hit among users. Fintech is more about upgrading existing financial services with the help of technology, giving convenience to the user, and making it instant.

What is Techfin?

The term emerged with the emergence of technology experts and companies that showed interest in developing infrastructure for financial services. While fintech is a wider term for the industry and a type of company, Techfin is only related to the type of company.

Made with two distinct terms, Technology and Finance, these are companies that are tech experts or have tech products in their DNA, and now have diversified their services into the financial sector. A prime example of the same is Google, which emerged as a tech company and now has a dedicated application, Google Pay, for financial services.

Though Techfin is also a part of the fintech market when it comes to revenue, it is a phenomenon that can be seen in existing players more than in startups. Tech companies from all around the globe have developed a financial solution of their own, expanding their horizon of services and the areas in which they operate.

What makes it easier for tech companies to explore finance is the fact that they already have a user base or data sets that help them understand what a user is looking for. This way, they can easily pave their way into the digital world of financial services.

TechFin Ecosystem: Key Stakeholders

Just like a fintech company, a techfin brand also has a set of key players that form an ecosystem. This ecosystem of players is important for a company to grow and expand into financial services.

The TechFin ecosystem is composed of various stakeholders, including:

1. Tech Giants

Leading the charge with their extensive tech infrastructure and user base, tech giants are those companies that have already made their name in the field of technology. Think of them like a widely spread tech business that now plans to enter the financial services industry.

2. FinTech Partnerships

For any tech company to be able to enter the financial services, they need a fintech to partner with them. Generally, tech giants acquire an NBFC or launch one of their own to gain access to the resources required to run a finance business more impactfully.

3. Regulators

They play the same role here as they do with fintechs. However, the role becomes quite crucial as these companies are not traditionally from financial backgrounds hence, ensuring that TechFin companies comply with financial regulations requires more diligence.

4. Consumers

Benefiting from the integrated and innovative financial services provided by TechFin companies, there are consumers who are directly in touch with the services that they offer. Fintech companies often target banks that are not digital to convert them into a digital solution. However, with tech giants, the service is directly targeted towards the consumer, allowing them to use services like wallets, online payments, etc.

5. Investors

Supporting the expansion and development of TechFin initiatives, investors are usually at the back of the operations. In the majority of techfin companies, the role of investor is played by the parent company as they already have enough infrastructure.

Looking at similar stakeholders, you might have understood that a techfin company works just like a fintech company, the key difference being the original niche of the company.

Another way to identify a techfin from fintech is by looking for the following attributes –

- Advanced tech infrastructure powering financial services.

- Leveraging big data and analytics for personalized services.

- Seamlessly incorporating financial services into existing tech platforms.

- Ability to rapidly scale services due to existing tech infrastructure.

- Emphasis on intuitive and efficient user interfaces.

Knowing all these attributes, the ecosystem, and the sheer meaning behind the term Techfin, you might have understood what exactly it means.

Now that we have successfully understood everything about both terms, let us move on to the comparison.

What are the Differences between Fintech vs Techfin?

To compare fintech vs techfin, you first need to understand the basis of the comparison you plan to draw.

Since both terms are associated with the use of technology in offering financial services, we have identified a criterion on which they can be compared.

Here is the comparison criteria –

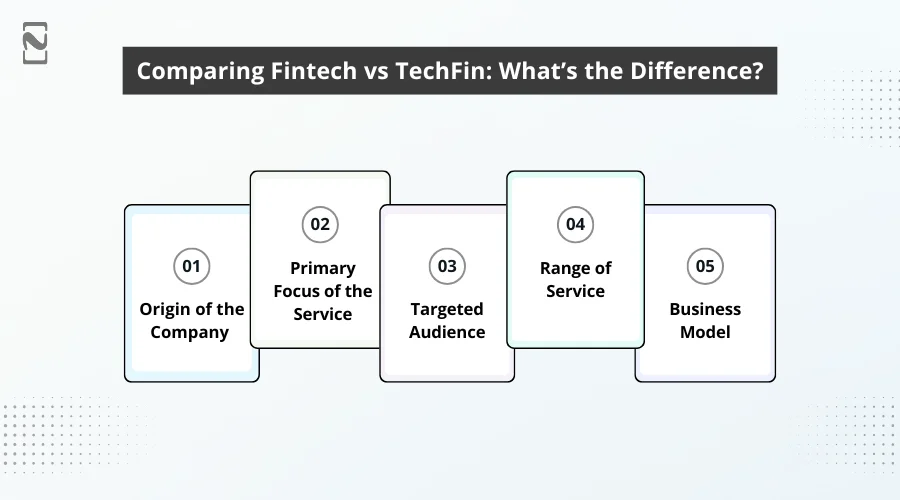

♦ Origin of the Company

One of the key criteria to draw a comparison between the two is the origin of these companies. Asking questions like How the term is defined, and how did it come into existence?, can help in clearing the doubts for many.

♦ Primary Focus of the Service

Finding out how the services are rolled out and what are the core principles of the company can be helpful in drawing the comparison. Asking questions like What sector does the company focus on primarily, and how does it identify the opportunity? It is also a great way to compare the two entities.

♦ Targeted Audience

What kind of audience does the platform target speaks volumes about the type of service. Keep in mind that while the target audience can align for both fintechs and techfins, however, there will always be some distinction that will help you identify the difference between them.

♦ Range of Service

This is a crucial criteria to keep in mind when planning a comparison between the two. What type of services are offered under the umbrella of their company? Asking this question can help in identifying what is the scope of the service and what markets does the company serve.

♦ Business Model

Understanding the revenue model or the business proposition of the company can also help in identifying a fintech or techfin. We have used questions like how exactly does the business make money, and what are the business objectives? To understand the business better.

Based on these 5 criteria, both techfin and fintech can be easily differentiated. Take a look at the following comparison table to identify the key differences between the two.

| Criteria | FinTech | TechFin |

| Origins | Starts with a financial background and integrates technology | Started with a tech background and moved into financial services |

| Primary Focus | Enhancing and innovating financial services through technology | Using technology to disrupt and provide financial services |

| Target Audience | Often targets individuals and small businesses initially | Leverages existing large tech customer base |

| Service Range | Digital payments, lending, investment, insurance, etc. | Digital wallets, loans, insurance, wealth management, etc. |

| Business Model | Fee-based services, subscriptions, and commissions | Monetizes through platform integration, data analytics, and commissions |

Based on these differences, you can simply identify the differences and answer the burning question: Fintech vs Techfin, which is better? But that is not the point of this comparison.

The point is to understand the exact meaning of these terms and how they differ.

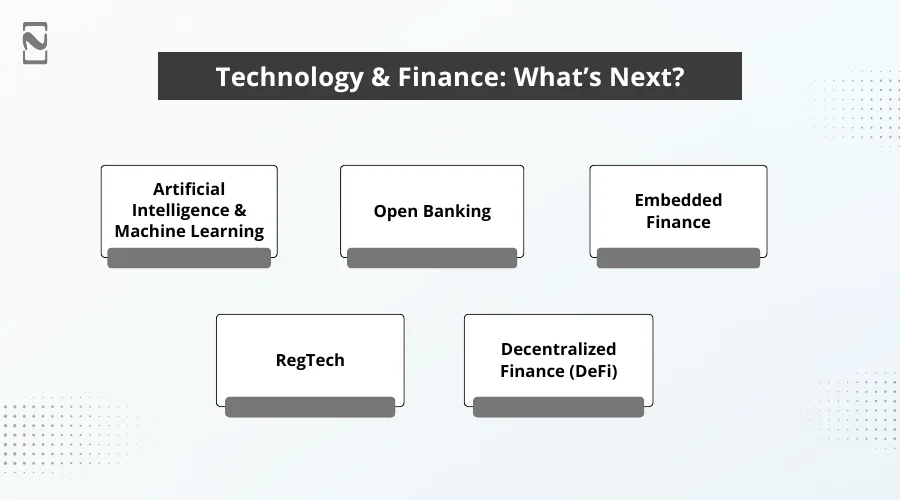

What’s Next for Finance & Technology? Future Trends

The intersection of technology and finance has paved the way for many different startups and opportunities. While the market is already thriving, the potential is endless as more and more tech companies are entering the fintech market.

The same goes for financial companies that started as a traditional finance institution, but have slowly turned into a fintech company with an added layer of technology that helps in spreading the service to a wider audience.

What’s interesting is the upcoming trends and technologies that further present a new opportunity for growth.

Here are some of the trends to look forward to –

• Artificial Intelligence and Machine Learning

AI and ML will play a crucial role in both FinTech and TechFin, enhancing capabilities like fraud detection, personalized financial advice, and predictive analytics.

These technologies will enable companies to provide more accurate and efficient services, improving customer experience and operational efficiency.

• Open Banking

Open banking, driven by regulatory changes and technological advancements, will become more prevalent.

This trend will allow third-party developers to build applications and services around financial institutions, fostering innovation and competition in both FinTech and TechFin.

• Embedded Finance

Embedded finance will see financial services integrated seamlessly into non-financial platforms, such as e-commerce sites and social media apps.

This trend will be particularly significant for TechFin companies, leveraging their tech infrastructure to offer financial services directly within their existing ecosystems.

• RegTech

Regulatory technology, or RegTech, will become increasingly important as financial regulations become more complex.

FinTech and TechFin companies will adopt RegTech solutions to ensure compliance, reduce regulatory risks, and automate compliance processes.

• Decentralized Finance (DeFi)

DeFi will continue to gain traction, offering decentralized financial services through blockchain technology.

This trend will democratize access to financial services, enabling peer-to-peer transactions and eliminating the need for traditional intermediaries, impacting both FinTech and TechFin.

Since all these trends impact both techfin and fintech companies, it is clear that the future for both is bright.

If you are planning to enter the market with a solution of your own, regardless of whether you are a financial company entering the tech industry or vice versa, it can be a game-changing step for you.

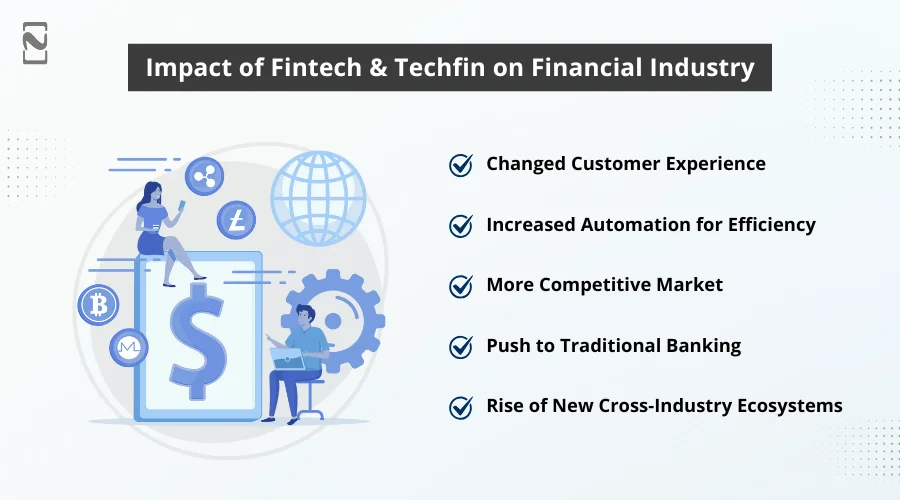

What is the impact of Fintech & Techfin on Financial Industry?

Knowing what both of these terms mean, you may be wondering how exactly they affect the overall financial industry.

Well, irrespective of whether a company is fintech or techfin, the industry grows when a new player emerges in the market that looks promising and promotes the core idea of financial inclusion.

Here’s what fintech and techfin companies have been able to achieve for the industry –

1. Changed Customer Experience

Both fintech and techfin allow users to change the way users interact with financial services. Even traditional services such as checking bank account balances have been digitised, giving them a much more convenient way of interacting with the services. Not to mention, personalizations and daily tech solutions further improve the solutions.

2. Increased Automation for Efficiency

Fintech platforms have certainly allowed a smoother implementation of automation in financial services. Both techfin and fintech companies use blockchain and AI for a smoother functioning of the services that they have to offer. Not only do these technologies allow more features to be added, but they also make it more secure for the users.

3. More Competitive Market

With the emergence of both fintech and techfin companies, the overall market has better competition. Which, if you look from the consumer perspective, is a great thing as they now have more options to choose from. Fintechs challenge traditional services directly, while techfin companies give direct access to the ecosystems that they control, reaching a wider audience.

4. Push to Traditional Banking

The way these services are working, they give a solid push to traditional banks to evolve and change their approach towards offering financial services. Several experts in the market have already seen the disruption of traditional banking services into more sophisticated solutions, all thanks to the rise of fintech and techfin platforms.

5. Rise of New Cross-Industry Ecosystems

Technicians have played a massive role in establishing the modern-day cross-industry ecosystems. Fintechs, on the other hand work on creating their own ecosystems where they are more into creating niche solutions. Leveraging embedded finance, techfins are truly changing the way ecosystems function in the long run.

The idea behind both of these terms related to one big and clear goal, changing the way people use financial services. Fintech is more of a known entity and can be considered the best for startups working their way into the sector. On the other hand, if a tech company is planning to diversify their services with a fintech solution, it falls in techfin.

Either way, the impact is massive and one can easily choose their path to enter the lucrative fintech market.

Conclusion

The market is ripe for both fintech and techfin companies right now.

The only thing you need to pay attention to is choosing the right app development partner that understands your origin and guides you accordingly. For instance, Nimble AppGenie can be a great fintech app development company to choose as your partner, as they have a lot of experience.

With that said, we have reached the end of this post. Hope you got all your queries cleared about fintech vs techfin. Both are involved in a similar space, and the key difference lies in their scalability as well as their origins.

That will be all for this one. Thanks for reading, good luck!

FAQs

FinTech companies originate from financial backgrounds, integrating technology to enhance financial services. TechFin, in contrast, begins as technology firms, extending into finance to revolutionize services leveraging their tech expertise.

FinTech emerges from financial backgrounds, while TechFin starts as technology firms and extends into finance.

FinTech enhances financial services through technology, focusing on efficiency and accessibility. TechFin disrupts finance by integrating financial services into existing tech platforms, leveraging advanced infrastructure.

FinTech targets individuals and small businesses initially, gradually expanding. TechFin leverages existing large tech customer bases for rapid scalability.

FinTech integrates new tech to enhance user experience. TechFin utilizes advanced infrastructure and data analytics for efficient financial services.

FinTech scales gradually as it grows, expanding services over time. TechFin, with its existing tech infrastructure, scales rapidly to vast user networks.

FinTech navigates complex financial regulations from inception. TechFin adapts to financial regulations as it enters the sector.

FinTech relies on fee-based services and commissions. TechFin monetizes through platform integration, data analytics, and service fees.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.