Banking Software Development

Banking Software Development Our Work Process

Our Work Process Awards

Awards

In a Nutshell:

- White label vs custom fintech solutions, let’s know which one to choose.

- White label fintech gets you to market in 2–8 weeks. Custom development takes 6–12 months minimum.

- Custom builds cost $30,000 to $300,000+ upfront. White label starts lower, but licensing fees compound $2,000/month over 5 years is $120,000 before extras.

- White label hands compliance and security to the vendor. Custom puts it entirely on your team, which is why the development partner you choose matters as much as the approach itself.

- Vendor dependency is the biggest white label risk. Cost overruns and compliance failures are the biggest custom risks, and both are significantly reduced when compliance is built into the architecture from day one, not added after.

- If you are pre-revenue and testing a market, white label makes sense. If you have a differentiated product vision and funding, custom is the better long-term call.

- The hybrid path, custom UX on white label infrastructure, works well for mid-stage companies that need both speed and differentiation.

- Migrating from white label to custom later costs more than starting custom from the beginning. Nimble AppGenie helps you make that decision before you have spent the budget twice, with a free consultation, no commitment required.

If you are building a fintech product in 2026, one of the first decisions you will face is whether to use a white label vs custom fintech solution. It sounds like an easy trade-off, speed versus control, but the reality is more complex. The real decision comes with three things: how much capital you are willing to invest, how fast you need to move, and how much risk you can tolerate.

This guide breaks down every factor without hype. No “best of both worlds” generalities, just direct answers to what white label and custom development cost, how long each takes, and where each one can hurt you.

White Label Vs Custom Fintech Solutions – Let’s Compare

► White Label Fintech

A white label fintech solution is a pre-built platform that a third-party vendor creates, which you license, rebrand, and launch under your own brand. You set up your domain, add your logo, configure the product flow, and you are operational. The underlying infrastructure (KYC, core banking, ledger management, payment rails) is already built and tested.

Examples include neobank infrastructure providers, digital wallet platforms, and payment gateway solutions that businesses can license and make live under their own brand.

► Custom Fintech Development

Custom means you develop from scratch. Every module, from your user authentication and transaction engine to your reporting dashboards and compliance stack, is designed, developed, tested, and deployed according to your unique requirements. You own the architecture, code, and roadmap.

This is what companies like Revolut, Stripe, and Cash App did before they became the top fintech apps. It’s a model that most fintech startups cannot afford to replicate from day one.

Custom fintech development is not only a longer path to the same destination. It leads to a basically different product – one you own, one your competitor can’t replicate, and one that doesn’t come with a vendor’s ceiling on what you can develop.

Security architecture in fintech is not a post-launch task; it needs to be built in from day one. This guide on fintech app security best practices covers what a genuinely secure fintech build looks like across encryption, access control, and compliance layers.

Cost Comparison: What You Actually Pay

Cost is where most fintech companies have confusion. They compare the upfront numbers without accounting for the ongoing costs. White label vs custom fintech solutions, whatever you choose, both have costs that compound over time, and neither is “cheap” if you don’t plan for it.

You would like to ask: Is white-label fintech cheaper than custom development? Yes, launching white-label fintech upfront is cheaper than custom development. Let’s look at both paths in more detail.

♦ Custom Fintech Development Costs

Custom fintech app development from scratch eats up the budget quickly. You need people who can manage frontend, backend, cloud infrastructure, compliance, and security, usually simultaneously. That’s not a job for a two-person team.

Fintech founders ask, “How much does it cost to build a custom fintech app?”

Costs vary depending on your team’s location and project scope.

- A basic custom fintech app starts at $30,000 to $80,000

- A mid-tier product with full compliance, KYC, and payment integrations runs $100,000 to $300,000

- Enterprise-grade platforms can exceed $500,000 to $1 million+

That’s only development. Add third-party API licensing (KYC providers, payment gateways, fraud detection), security penetration testing, cloud infrastructure, and PCI DSS compliance audits – your total fintech development cost can increase significantly.

According to Nimble AppGenie, a fintech app development company that has delivered 50+ payment-integrated applications, the cost to build a fintech app ranges from $30,000 to $300,000+, depending on compliance scope, feature complexity, and development team location.

♦ White Label Fintech Costs

A white label fintech platform typically includes:

- An upfront setup or licensing fee: Usually $15,000 to $50,000 for basic platforms

- Monthly or annual subscription fees: $500 to $5,000/month, depending on users and features

- Revenue-sharing in some cases (common in payment platforms, crypto solutions)

- Customization fees for any feature changes beyond standard configurations

The upfront cost is lower. But the long-term fees add up. A platform charging $2,000/month over 5 years adds $120,000 in licensing before you count integrations, setup, or usage-based pricing.

Hidden Costs You Should Know

White label vs custom fintech solutions, whichever you choose to build, both paths have hidden costs that often remain hidden in the initial quote.

Let’s check out the hidden cost of fintech software development.

| Cost Factor | White Label | Custom Development |

| Customization | Limited; extra charges apply | Fully flexible, but adds dev cost |

| Compliance Updates | Vendor handles (usually) | Your team’s responsibility |

| Infrastructure Scaling | Handled by the provider; usage fees | Rearchitecture may be needed |

| Security Patching | Covered by vendor SLAs | Ongoing internal effort |

| Vendor Lock-in Exit | High cost/data migration | N/A – you own everything |

| Long-term Licensing | Accumulates into high cost | No recurring license fees |

White-label costs less on day one. Custom costs seem less over five years. Which one wins depends completely on how long you plan to run the product.

Time to Market: The Real Numbers

Time is the factor where white label wins clearly – no debate. But “faster” doesn’t always mean “better,” depending on what you are building and who your users are.

➤ Custom Fintech Timeline

How long does it take to build a custom fintech app? Custom fintech product development takes, on average:

- MVP (basic features): 4 to 6 months

- Full-featured product (payments, KYC, compliance, reporting): 8 to 12 months

- Enterprise-grade platform: 12 to 24 months

During that time, you pay a fintech development partner, your infrastructure is running, and you are not generating revenue. For a startup running on seed funding, every month of development is spent without income.

As a mobile app development company, we typically build fintech apps in 6 to 12 months, based on design complexity, scope, and compliance requirements, with agile sprints to compress time-to-market where possible.

➤ White Label Timeline

A white label fintech solution can typically be deployed within:

- Basic deployment (branding + configuration): 2 to 8 weeks

- With custom UI and additional integrations: 2 to 3 months

That’s a notable difference. If you need to validate a market, respond to a competitive window, and onboard early users, a few weeks versus 12 months is a real advantage.

➤ Where the “Fast” Argument Breaks Down

Well, speed is not free. Launching quickly on a white-label platform means:

- You are building your brand on someone else’s infrastructure

- The “fast” deployment may need considerable rework to match your UX requirements

- Feature requests go through the vendor’s roadmap, not yours

- If the vendor changes pricing or shuts down, your fintech product is at risk

When fintech founders finally decide to move off a white label platform, they often discover the migration costs more in money and time than starting custom would have. That’s not an argument against white label banking solutions. It’s an argument for deciding with more caution.

Risk Comparison: What Could Go Wrong

Both white label and custom development carry risks; they are only different types of risk at different stages.

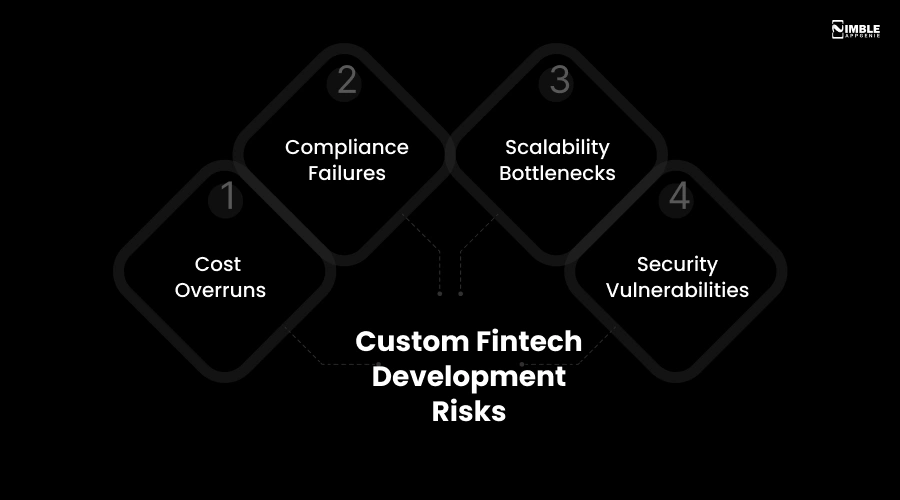

♦ Custom Fintech Development Risks

1. Cost Overruns

Custom builds rarely come in on budget. Regulatory surprises, scope creep, team changes, and integration complexity all contribute to the higher fintech software development cost. If you are working with an inexperienced vendor, this is a near-certainty.

2. Compliance Failures

In fintech, compliance is not optional. Getting PCI DSS, KYC/AML, GDPR, and PSD2 wrong can mean a complete shutdown or regulatory fines. Building compliance into a custom fintech app needs deep domain expertise, not just developers.

3. Scalability Bottlenecks

Systems developed for 1,000 users often need rearchitecting for 100,000. If scalability is not baked into the original fintech app design, you will hit walls, and rebuilding core architecture mid-growth is much more expensive.

4. Security Vulnerabilities

A custom-built system is only as secure as the team that creates it. Without ongoing penetration testing, patch management, and security audits, the platform remains exposed to risk. One breach in fintech can permanently destroy user trust.

Compliance is one of the most misunderstood cost drivers in fintech. Nimble AppGenie has a dedicated breakdown of fintech regulations and compliance that every founder building a custom product should read before writing a single line of code.

♦ White Label Fintech Risks

What are the risks of using a white label fintech platform? Here are the most common risks:

1. Limited Differentiation

If your competitor uses the exact white label platform, your product is almost identical internally. In competitive fintech markets, differentiation matters. White-label makes it difficult to build a competitive moat.

2. Vendor Dependency

Your complete product runs on a vendor’s infrastructure. If they change terms, raise prices, go under, or get acquired, you have a serious issue. Contracts help, but don’t eradicate this risk.

3. Customization Ceiling

Most white label fintech platforms cap what you can modify. At some point, your product needs will exceed what the platform allows. When that happens, you are either stuck or fully rebuilt, which may cost more than building custom from the start.

4. Hidden Technical Debt

You inherit whatever architecture the vendor develops, including its limitations and any vulnerabilities that haven’t been patched. In a regulated product, that’s not only a technical problem. It can become a compliance one.

If you are building a payment product specifically and need to understand what PCI DSS compliance actually requires in a build, this guide on developing a PCI-compliant mobile app is worth reading before you evaluate any vendor’s compliance claims.

| Risk Category | White Label | Custom Development |

| Vendor dependency | High | None |

| Security vulnerabilities | Low (vendor-managed) | Medium to High (team-dependent) |

| Compliance risk | Shared with vendor | Entirely your responsibility |

| Cost overrun | Low (predictable licensing) | Medium to High |

| Scalability limits | Platform-imposed ceiling | Architect-dependent |

| Competitive differentiation | Low | High |

| Exit/migration cost | High (data + rebuild) | Low (you own it) |

Which Is Better For A Fintech Startup: White Label Or Custom?

Well, there’s no universal right answer. Fintech companies come to us asking: white label vs custom fintech, which is better for startups, and we tell them that the right choice relies on your budget, stage, and what you are actually trying to create.

This decision framework surfaces the main point quickly.

| Your Situation | Recommended Approach |

| Early-stage startup validating a market hypothesis | White label to test, then migrate to custom |

| Startup with differentiated product vision and $300K+ budget | Custom from the start |

| Existing business adding financial services (BNPL, wallet, payments) | White label or hybrid |

| Building a neobank or complex lending platform | Custom with compliance specialists |

| The competitor is already on white label, you need to differentiate | Custom |

| Time to market is 60 days or less | White label only |

| Planning to scale internationally, with complex regulatory requirements | Custom with compliance built in |

The most common mistake fintech startups make is choosing white label because it’s comparatively cheaper to start, without planning for the migration cost when they expand it. That migration usually costs more than custom development would have from the start.

The Middle Path: Hybrid Fintech Development

There’s a third option that fintech startups opt for: building a custom product on top of white label or open infrastructure. It’s sometimes called a “hybrid” approach.

In practice, it looks like this:

- Build a fully custom frontend, user experience, and product logic on top

- Use a white label core for regulated infrastructure (banking rails, KYC, ledger)

- Own the customer-facing layer entirely while leveraging proven backend infrastructure

You choose the costly parts that are risky to build, like KYC, banking rails, and ledger management, from a proven vendor. Everything the user sees and interacts with is yours. That’s where differentiation lives anyway.

For an in-depth look at how neobanks are created, including architecture decisions, explore our neobank app development services.

The hybrid path is not right for everyone. requires a development team that understands both custom development and platform integration, which is rare. But for companies at the Series A stage or above, it usually delivers the best cost-to-differentiation ratio.

The hybrid path also applies to payment infrastructure. If you are evaluating building a custom ACH or payment layer on top of existing banking rails, our guide on custom ACH payment software development covers exactly what that build involves and where complexity spikes.

How Nimble AppGenie Helps – White Label Vs Custom Fintech Solutions Which is Better?

A lot of fintech founders come to us after struggling with a white label solution – they are stuck on the vendor’s roadmap, they have outgrown the platform’s capabilities, or they need features the platform just won’t support. Some tried to build a custom fintech app with a generalist team, which resulted in a compliance mess.

Nimble AppGenie is a fintech app development company based in Houston, Texas. We have developed 50+ payment-integrated applications, including custom payment gateways, eWallet solutions, P2P platforms, BNPL solutions, and AI-powered neobank cores, for startups and enterprises across the US, UAE, UK, and beyond.

If you want to understand what a real custom fintech product looks like end-to-end, our guide on building a payment platform like Stripe walks through the full architecture.

For lending-specific products, our P2P lending app development guide covers borrower-lender matching, credit scoring, and regulatory requirements specific to lending platforms, a use case where custom almost always beats white label.

If you are still in the early stage of deciding what type of fintech product to build, this post on fintech startup ideas covers the most viable product categories in 2025 with market data behind each one.

What we do differently:

- Fintech-Specific Security: Zero-trust architecture, regular penetration testing, and multi-layer encryption

- Compliance-First Development: PCI DSS, PSD2, GDPR, and KYC/AML built into the architecture, not added later.

- Scalable Foundations: Systems are architected to manage growth, not only MVP traffic.

- Transparent Costing: Cost ranges from $30,000 to $300,000+, depending on scope, with clear breakdowns upfront.

- Hybrid Capability: We can work with white label infrastructure if it’s already in place and create custom layers on top.

Our team covers lending software, eWallet apps, neobank development, DeFi, banking software, cross-border payment systems, and crypto wallets. If you are at the point of making the build vs buy fintech decision, we can help you with a technology stress-test of both options before you commit to a budget.

For businesses exploring the cost to build a banking app, specifically, our breakdown of mobile banking app development costs is a robust reference.

You can also scan our eWallet work, projects like MaxPay (a custom payment gateway for betting and fantasy platforms) and PayByWallet (multi-currency with real-time FX conversion) are good case studies of what custom fintech looks like in practice.

If your product is an eWallet or digital payment app specifically, the cost structure is different from a full banking platform. This eWallet app development cost breakdown gives a more targeted picture.

Our fintech API integrations guide at Top Fintech APIs Every Startup Should Know is worth a read if you are still scoping your project.

Conclusion

White label vs custom fintech solutions, which one to choose?

For specific scenarios, white label fintech is a practical option: limited budget, fast market entry, or adding financial features to an existing product. It’s not a shortcut to build a lasting product. Companies that succeed with white-label solutions are usually using them as a stepping stone, not a final fintech app architecture.

Custom fintech development is costly and slow, but it offers you ownership, control, and differentiation. If your product depends on tight compliance needs, unique features, or a specific user experience, custom is the only option that doesn’t create a ceiling; you will have to recreate it later.

The hybrid model combines a custom product layer with controlled white-label infrastructure, which is worth considering if you have moved beyond early validation but not at scale yet, where a complete custom build makes economic sense.

Well, whatever path you choose, the decision should clarify three factors: time, cost, and risk. Optimizing for only one of them is how companies end up redeveloping from scratch 18 months in.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.