AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

In a Nutshell:

- The build vs buy threshold: Third-party processors make sense below $5M/month. Above $5M–$10M/month, or when your product needs payment flows, an off-the-shelf processor can’t support building your own, it pays off fast.

- What it costs to build: MVP $50,000–$120,000, 4–6 months. Full platform $250,000–$500,000+, 12–18 months. Compliance costs are separate.

- PCI DSS v4.0 is mandatory from March 2025. Compliance must start on day one, not after launch.

- US Licensing: Money Transmitter License needed in most states. Plan 6-12 months and $50,000–$200,000+ for full US coverage.

- AI fraud detection is a core requirement in 2026, not an optional add-on. Static rule sets alone won’t cut it.

- API quality drives merchant adoption. Poor documentation and a buggy sandbox will send merchants straight back to Stripe.

- Nimble AppGenie has built 50+ payment-integrated fintech products, custom gateways, eWallets, BNPL platforms, and P2P systems, from Houston, TX.

At $10 million in payment volume, standard third-party payment processor fees hit $290,000 every month. It’s around $3.5 million a year; for infrastructure you don’t own, can’t customize, and can’t control.

In the early days, third-party payment processors were the right call as they were quick to integrate, had solid documentation, no monthly fees, and zero compliance overhead on your side. They are not optimized specifically for one; they are built for everyone. When your payment volume or regulatory requirements outgrow, an off-the-shelf processor fails to meet your needs, but you are paying premium fees for a product that’s actively limiting you.

This guide is built for fintech founders and CTOs who are at that turning point. The real question is: does it make financial and strategic sense to build our own payment gateway, and if so, what does it actually cost, how long does it take, and what does compliance look like

We answer all of it. The full decision framework, the financial threshold, the cost breakdown, the tech stack, the compliance requirements by market, and the step-by-step process. Everything you need before you commit to a direction.

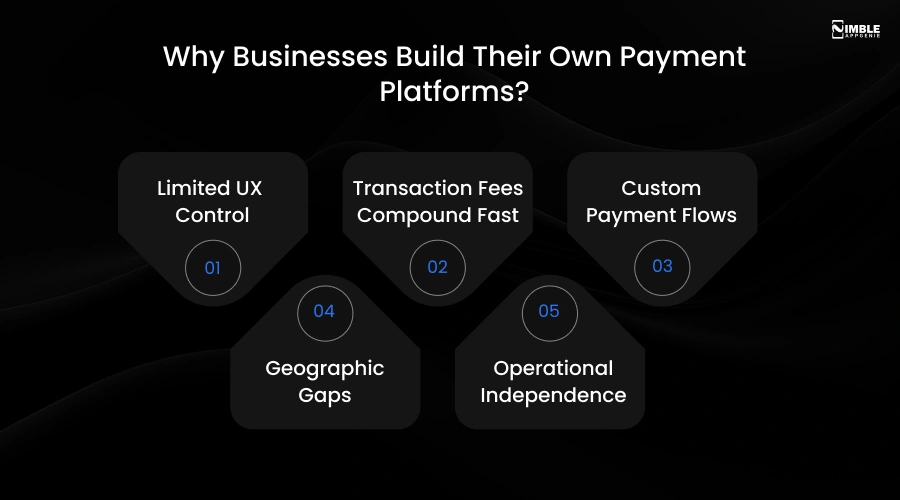

Why Businesses Build Their Own Payment Platforms?

Stripe is excellent, but it doesn’t mean it’s right for every business at every stage.

Check the following most common reasons fintech founders and CTOs decide to build a custom payment gateway:

1. Limited UX Control

Checkout flow, data ownership, and branding are all constrained on third-party platforms. Custom builds give you complete control.

2. Transaction Fees Compound Fast

Stripe charges 2.9% + $0.30 per transaction. On $10M/month, that’s over $290,000 in fees every month. You can eliminate this line item by owning your infrastructure.

3. Custom Payment Flows

Marketplaces and platforms usually need split-payment logic, payout structures, and escrow workflows that Stripe Connect doesn’t natively support.

4. Geographic Gaps

Stripe doesn’t support all regional payment methods or banking integrations, specifically in emerging markets across Southeast Asia, Africa, and the Middle East.

5. Operational Independence

Stripe outages and policy changes directly impact your revenue. Owning the infrastructure removes that dependency.

Build vs. Use Stripe: The Simple Threshold

Under $5M/month in processing volume; Stripe almost always makes more sense. Above $5M–$10M/month, the math shifts. Owning your infrastructure starts to pay off fast. That said, volume is not the only trigger. See the full Build vs. Buy decision table below.

What You Are Actually Building: The Non-Negotiable Feature Set?

Before committing to a build, you need to know what “done” looks like. A production-grade custom payment gateway in 2026 requires developer-first REST APIs with sandbox environments, multi-method payment acceptance, multi-currency FX settlement, AI-powered fraud detection, PCI DSS v4.0 compliance, recurring billing logic, KYC/AML integration, real-time reporting and reconciliation, and white-label multi-tenant architecture if you plan to offer payments-as-a-service.

Each of these is a non-trivial engineering workload. The feature set is what drives your build timeline from 4–6 months for an MVP to 12–18 months for a full platform, and why the compliance work has to run in parallel from day one, not after launch.

The Third Option: Build on Existing Payment Infrastructure

Most founders either build everything from scratch or use Stripe and accept the fees. But there is also a third route that many of the fastest-growing payment companies are actually choosing in 2026.

The hybrid approach means leveraging battle-tested payment infrastructure as your base layer and building your UX, custom logic, and merchant experience on top of it.

| Infrastructure Layer | What It Handles | What You Build on Top |

| Stripe Connect | Merchant onboarding, card processing, payouts | Your marketplace UX, fee logic, and custom split payment rules |

| Adyen for Platforms | Acquiring, settlement, multi-currency | Your merchant dashboard, reporting, and routing rules |

| Marqeta | Card issuing, transaction controls | Your spend management UI, programme rules |

| Checkout.com APIs | Payment processing, risk scoring | Your checkout flow, retry logic, and reconciliation |

Hybrid makes sense when: You need split-payment flows or custom merchant UX but don’t yet have the volume ($5M–$10M+ monthly) to justify building your own networks. You want faster time-to-market – 4-6 months instead of 12-18. You want to avoid a full PCI DSS Level 1 scope on your first build.

Full custom makes sense when: You are processing $10M+ per month, and per-transaction fee savings justify the build cost. Your payment flows need architecture that no current infrastructure provider supports. You are operating in markets where Adyen, Stripe, and Checkout.com have no presence.

For most fintech startups in 2026, the hybrid route is the smarter first step. Full custom is typically a Year 2-3 decision once volume justifies the infrastructure investment.

Tech Stack For Building a Custom Payment Gateway

There’s no universal stack. The right choice depends on your compliance scope, transaction volume, and team expertise.

The right tech stack depends on your transaction volume, compliance scope, and team expertise – frontend, backend, database, message queue, security layer, fraud detection, and KYC integration all need to be chosen together, not in isolation.

A note on backend choice: Node.js is widely picked for its non-blocking I/O, perfect for payment APIs handling various concurrent requests. Go is preferred for high-volume transaction engines because of its raw performance and low memory footprint. For a deeper look at how these layers connect, see our fintech app architecture guide.

The Build Process: What You Are Actually Committing To

Building a custom payment gateway runs 8 different phases, from scoping and compliance mapping through architecture, core infrastructure, fraud integration, developer tooling, security testing, and controlled rollout.

The full step-by-step breakdown with timelines and technical decisions for each phase is covered in our guide to building a payment gateway from scratch.

What most teams underestimate going in: compliance work doesn’t start after your product is built; it runs in parallel from month one. In the US, money transmitter licenses take 3–12 months per state. PCI DSS Level 1 certification takes 6–12 months. The compliance timeline, not the development timeline, is usually what determines your actual launch date.

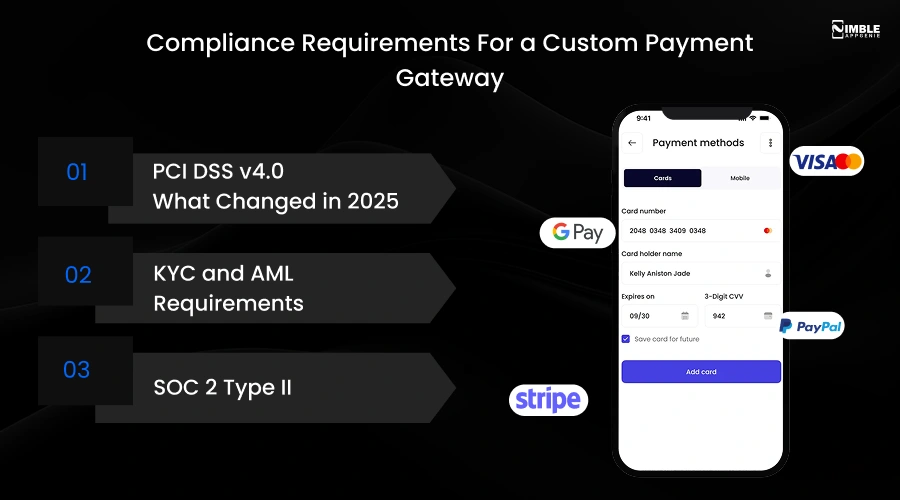

Compliance Requirements For a Custom Payment Gateway

Compliance is not paperwork; it determines your launch date.

Below is what you need, by market:

| Market | License Required | Who Issues It | Realistic Timeline |

| USA | Money Transmitter License (MTL) – required in most states individually + FinCEN MSB registration | State regulators (NYDFS, CA DFPI, etc.) | 3–12 months per state; FinCEN registration is faster |

| UK | Electronic Money Institution (EMI) license | Financial Conduct Authority (FCA) | 12–18 months; or partner with a licensed EMI to launch faster |

| EU | Payment Institution (PI) or EMI license | National regulator (BaFin, DNB, AMF, etc.) | 6–18 months; EU passporting available post-authorization |

| UAE | Payment Service Provider (PSP) license | Central Bank of UAE (CBUAE) | 3–12 months depending on activity scope |

| Global (card data) | PCI DSS Level 1 certification | QSA-certified auditor | 6–12 months for a new build to achieve Level 1 |

| The practical reality: If you are building a card-processing platform and launching in the US, you are looking at 12–24 months from decision to live when you factor in both development and licensing. Most fintech startups that want to move faster use the hybrid model or partner with a licensed institution for the first phase of their launch, then pursue their own licenses in parallel. |

► PCI DSS v4.0 – What Changed in 2025

PCI DSS v4.0 introduced 51 new requirements above the previous standard, entirely mandatory from March 2025. Key additions include multi-factor authentication across all non-console admin access, rigid controls on phishing protection and web skimming defenses, and improved requirements for targeted risk analysis. Non-compliance leads to fines up to $100,000 per month and risks having your card processing rights revoked completely.

► KYC and AML Requirements

In the US, the Bank Secrecy Act (BSA) requires identity verification, Suspicious Activity Reports (SARs), and ongoing transaction monitoring. The EU’s AML Directive (6AMLD) applies across EU member states. If you have EU users, GDPR supervises how you collect, process, and store personal data. These are not one-time checks – they need ongoing monitoring systems built into your platform architecture. See: Fintech Compliance Guide.

► SOC 2 Type II

Not legally needed, but increasingly expected by enterprise merchants and partners before they integrate. SOC 2 certification shows your security controls are audited and real. Plan 6-12 months to achieve it and begin the process earlier than you think you need to.

What the Build Actually Costs And When It Pays Off

The question is not only what it costs to build. It’s whether the build cost is cheaper than what you are paying in processor fees over 24-36 months.

At $10M/month in volume, third-party processor fees exceed $290,000 every month – $3.5M per year. A full custom platform at $250,000–$500,000 pays for itself inside six months at that volume. Below $5M/month, the math rarely works in favor of building.

| Build Type | Estimated Cost | Timeline |

| MVP — Core payment flows only | $50,000 – $120,000 | 4–6 months |

| Mid-tier — Multi-method, fraud detection, reporting | $120,000 – $250,000 | 8–12 months |

| Full platform — Multi-currency, white-label, KYC, subscriptions | $250,000 – $500,000+ | 12–18 months |

| Enterprise — Custom infra, proprietary rails, global scale | $500,000 – $1M+ | 18–24+ months |

The additional costs most teams don’t budget for are where projects go over:

- PCI DSS Level 1 audit and QSA fees: $15,000–$40,000+ per year

- Third-party KYC/AML API integrations: $5,000–$20,000

- Fraud detection ML model development: $20,000–$80,000

- Money transmitter licensing (US): $50,000–$200,000+, depending on the number of states

- Load testing and security penetration testing: $10,000–$30,000

For most fintech startups, the most cost-efficient model is a hybrid team – an in-house product lead paired with a specialized fintech development company. This keeps costs regulated without sacrificing the architecture and compliance expertise that payment platforms need. See: Offshore vs. Onshore Fintech Development.

The Biggest Challenges When Building a Custom Payment Platform

1. Security Is a First-Class Engineering Requirement

One of the highest-value targets for attackers is payment data. In 2026, data breaches in financial services cost an average of $5.56 million. AES-256 encryption, zero-trust architecture, multi-factor authentication, and quarterly penetration testing are foundations – not extras. The cost of getting this right is a fraction of the cost of a breach.

Solution: Use hardware security modules (HSMs) for cryptographic key management from the start.

2. Fraud Detection Needs Your Data, Not Generic Models

Fraud models trained on public datasets don’t perform on your particular transaction mix. In the starting phases, use rule-based detection (IP reputation scoring, velocity checks, and device fingerprinting) while you collect your own transaction data. Layer in custom ML models as volume grows.

Solution: Tools like TensorFlow, AWS Fraud Detector, and Sift give you a beginning point without building from scratch. For a full breakdown, see: AI Fraud Detection in Fintech.

3. Compliance Takes Longer Than Your Engineering Team Expects

Licensing and PCI DSS are not only paperwork. Start compliance work before you start coding. Hire a qualified security assessor (QSA) in month one. Map your licensing requirements by state before committing to your launch date.

Solution: Use hosted payment fields and tokenization to diminish your PCI scope; this cuts audit complexity notably and keeps your first build more manageable.

4. API Quality Determines Whether Merchants Choose You or Stay on Stripe

Developers choose payment platforms based on documentation quality before they evaluate anything else. If your sandbox behaves differently from production, if your documentation requires a support ticket to understand, and if your SDK is out of date, merchants will stay on Stripe.

Solution: Write documentation as you build. Publish a changelog and a clear API versioning policy. Maintain a public status page.

5. False Positives Kill Revenue as Much as Fraud Does

Excessively aggressive fraud rules block legitimate transactions. Track your false positives rate as a primary business metric alongside your fraud rate.

Solution: Use a tiered review system: route edge cases to manual review, auto-decline clear fraud, and auto-approve low-risk transactions. A/B test rule changes on a subset of traffic before rolling them out broadly.

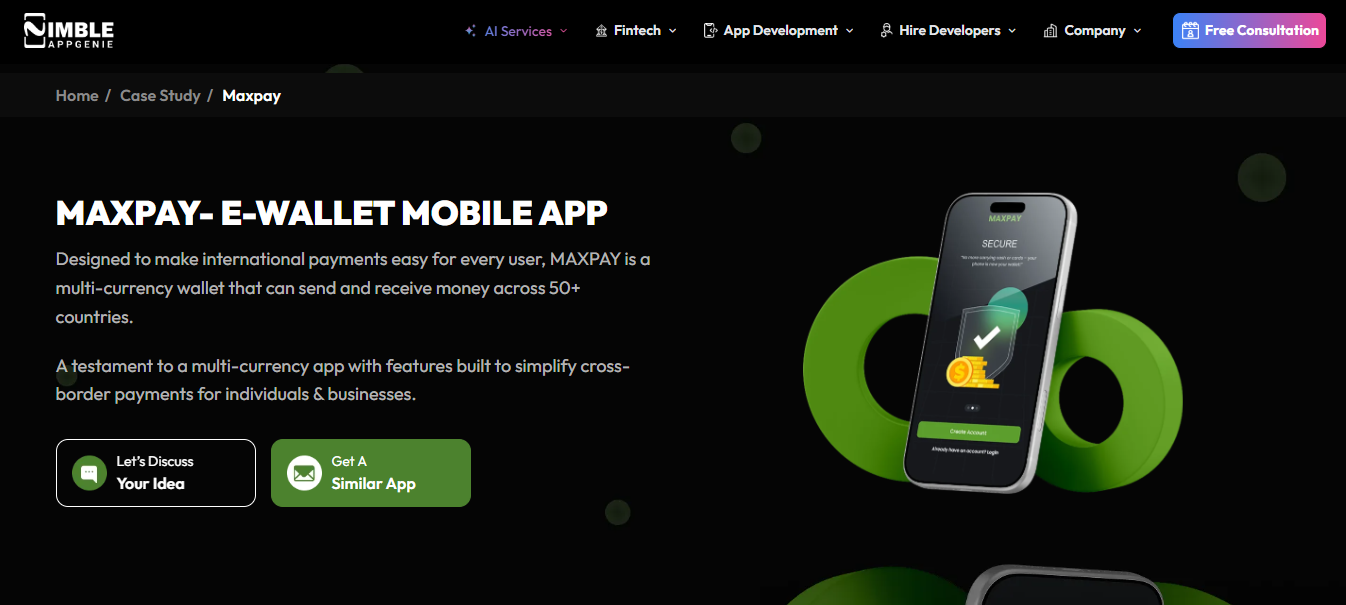

How Nimble AppGenie Builds Custom Payment Platforms?

Building a payment gateway needs fintech-specific experience across architecture, compliance, developer tooling, and fraud – all at the same time. A generic app development company doesn’t have this.

Below is one of our payment platforms:

♦ MaxPay – Custom Payment Gateway & Digital Wallet

The challenge: MaxPay needed a custom payment gateway and digital wallet for online betting and fantasy platforms with banking detail privacy, in-app payment flows, full PCI DSS compliance, and fraud detection built from the ground up.

What we built:

- Custom payment gateway with encrypted banking detail handling and seamless in-app payment flows.

- PCI DSS-compliant architecture from day one.

- AI-powered fraud detection with real-time transaction monitoring.

- Wallet management system with full audit trails.

Result: Launched on schedule with full compliance, now processing payments across a high-volume fantasy and betting platform.

Our fintech solution services cover the complete stack: architecture design, security implementation, compliance security, fraud system integration, custom payment gateway development, post-launch support, and SDK and API development. We work with enterprise clients, fintech startups, and mid-market businesses in the US, UK, Canada, and UAE.

50+ payment-integrated fintech products delivered. 8+ years of fintech development experience. 97% client retention rate.

Build vs. Buy: When Does Building Your Own Make Sense?

| Scenario | Use Stripe / Third-Party | Build Your Own |

| Transaction volume | Under $5M/month | Over $5–10M/month |

| Customization need | Standard checkout flows | Custom split payments, escrow, embedded finance |

| Geography | US / EU / major markets | Emerging markets or unsupported regions |

| Compliance resources | Limited compliance team | Full compliance team or specialist partner available |

| Long-term model | Early-stage startup | Scale-up, enterprise, payments-as-a-service |

| Development partner experience | First fintech build | Working with a partner who has built regulated payment products before |

| The real cost of starting with off-the-shelf: Most fintech startups that launch on third-party platforms outgrow them within 18–24 months. At that point, you are paying for a custom build and a full data migration, platform transition, and team retraining. Building custom from the start with the right partner is almost always cheaper over a three-year horizon, if your volume justifies it. |

A hybrid approach is also valid: start with Stripe integration for faster time to market, then migrate to a custom platform once revenue and volume justify the investment. Many successful fintech companies have followed exactly this path. See also: Payment Gateway Integration Guide.

Final Thoughts

Building a custom payment gateway is a serious technical and compliance undertaking. The timeline runs 6-18 months. The budget runs $50,000 to $500,000+, depending on scope and markets. Compliance adds both cost and time that most teams underestimate going in.

But for businesses processing at scale or businesses with payment requirements that third-party platforms simply can’t meet, building your own infrastructure is the right long-term decision. You own the UX, data, roadmap, and transaction costs.

The key is to choose a tech stack that suits your transaction volume, start compliance early, and work with a team experienced in regulated fintech products.

If you are evaluating whether to build or buy, or if you have already decided to build and want an experienced fintech engineer on your side, Nimble AppGenie is ready to help.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.