AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- Fraud losses are growing fast. Rule-based systems are falling behind. They catch what you define, miss what you don’t, generate too many false positives, and need manual updates every time fraud tactics change.

- AI fraud detection in fintech comes into play here. AI learns and adapts. It scores transactions in milliseconds, spots patterns across hundreds of signals at once, and updates as fraud evolves, without someone rewriting rules.

- False positives are a real cost, which blocks legitimate users, damages trust, and kills conversion. Danske Bank cut false positives by 60% after switching to AI. HSBC saw similar results.

- Behavioral analytics is one of the robust defenses. Even with correct credentials, an attacker’s behavior won’t match the real user’s pattern. That gap is what AI catches.

- Real-world results support the investment. PayPal reduced fraud losses by 40%. Commonwealth Bank cut scam losses by 50%. Mastercard’s AI screens 143 billion transactions a year.

- Compliance and fraud detection are linked. The same AI system that catches fraud also powers KYC, AML screening, SAR preparation, and sanctions checks.

- Build cost depends on the approach. A third-party API integration runs $15,000–$50,000. A fully custom enterprise system can exceed $500,000. Most early-stage apps should start with an API integration and build custom once volume grows.

- Ongoing costs are often underestimated. API fees, model retraining, AML software subscriptions, and analyst time add up. So, budget for the full lifecycle, not just the build.

- Nimble AppGenie builds fraud-resistant fintech apps, from payment apps and digital wallets to lending platforms with AI fraud detection, KYC/AML integration, and compliance-aware architecture built in from day one, not bolted on later.

AI fraud detection in fintech apps is no longer a choice. Fraud has become a serious business issue, and the figures make that clear. According to Deloitte, estimated authorized push payment fraud losses in the US may surge to $14.9 billion by 2028 from an anticipated $8.3 billion in 2024. By 2028, APP (Authorized Push Payment) fraud losses could reach $18.2 billion.

Fintech apps are the main target. They hold sensitive financial data, process high transaction volumes, and serve users who expect an immediate, frictionless experience. That combination is what fraudsters exploit.

The traditional approach, building a set of rules that flag suspicious behavior, no longer works. Fraud tactics evolve rapidly. Rule-based systems frustrate legitimate customers, generate too many false positives, and miss entirely new attack patterns.

AI changes how fraud detection works. 83% of industry leaders say AI has reduced churn and false positives, marking a new era in fraud prevention. AI doesn’t match transactions against fixed rules; it learns from data. It adapts to new threats, detects patterns humans miss, and makes decisions in milliseconds.

This blog explains how AI fraud detection works in fintech apps, where it adds real value, what it replaces, and how a fintech startup or product team can create it. We also cover what the cost looks like, where things go wrong, and how Nimble AppGenie helps clients build fraud-resistant fintech products.

Why Fraud Is a Growing Problem for Fintech?

Every connection point in fintech apps is a potential entry for fraud. How?

Fintech apps process transactions round-the-clock. They onboard users remotely, usually without face-to-face verifications, and integrate with payment networks, banks, and third-party APIs.

Let’s unveil the numbers reflecting this reality:

- According to KPMG’s survey, 81% of respondents witnessed attempted or successful AI-powered fraud, and 72% of those were impacted more than once. Also, 39% experienced AI-powered deepfake document fraud. Besides, 60% fell victim to fraudulent chat/email using AI agents or AI-generated content. 24% were victims of voice clone attacks.

- According to Mastercard, organizations lost $60 million to payment fraud in the past year.

- The 2025 State of Fraud Report reveals 60% of institutions report increased fraud attacks affecting consumer and business accounts.

- In the previous year, amid rising fraud attacks, about two-thirds of financial institutions experienced an increase in fraud events, led by enterprise banks at 67%, and 31% of organizations met complete fraud losses surpassing $1M.

- In IBM/Ponemon breach research, 16% of breaches include attackers using AI, with most AI-powered activity focused on manipulating humans rather than “hacking harder.”

- Recently, the FBI IC3 report showcases $16.6B in losses from 859,532 complaints (US reporting), and $2.77B in recorded losses tied to Business Email Compromise.

What are the biggest fraud risks for fintech apps? Fintech fraud is no longer limited to unauthorized transfers or stolen cards; it includes:

- Account Takeover (ATO): It’s when someone takes control of a legitimate user’s account.

- First-party Fraud: It’s a real user who commits fraud themselves, for example, chargeback abuse.

- Synthetic Identity Fraud: Fraudsters merge real and fake data to create a new identity.

- Money Mule Schemes: Networks of accounts used to layer and move fraudulent funds.

- Deepfake-enabled Fraud: AI-generated videos or documents used to fool verification systems.

These attacks are more automated, complex, and harder to identify with fixed rules. That’s why most fintech companies invest in AI.

Alloy’s fraud report 2025 says 99% of financial organizations are already leveraging some form of machine learning or AI to combat fraud. 93% of respondents hold trust in AI, believing it will revolutionize fraud detection.

Well, the examples are numerous; let’s look at the reasons behind the failure of rule-based fraud detection.

Why Rule-Based Fraud Detection Falls Short

Most fintech apps still start with rule-based fraud detection. Rules are simple: if a user attempts to log in from two countries in 30 minutes, block them. If a transaction exceeds $5,000 and comes from an unknown device, flag it.

Rules work for obvious fraud. But they have limits.

The problem with rules:

- They generate numerous false positives. This blocks real customers, which damages trust and hurts conversions.

- They are static. Fraudsters learn the rules and modify their behavior to avoid triggers.

- They struggle to scale as transaction volumes increase, and the rules become more challenging to maintain and coordinate.

- They miss new attack types. For example, a rule built for 2022 fraud patterns will fail to catch 2025 attacks.

- They demand manual updates as every rule change requires engineering time.

- AI-based fraud detection models attain accuracy between 87% to 96.8% in real-world deployments, notably outperforming traditional rule-based systems, which achieve 37.7% accuracy on average.

That’s a huge gap, explaining why companies like PayPal have reported 40% reductions in fraud losses after choosing AI in fintech fraud detection, and why the Commonwealth Bank of Australia cut scam losses by about half, leveraging the power of machine learning.

AI vs Rule-Based Fraud Detection Fintech

Is AI better than rule-based fraud detection? Let’s check.

| Dimension | AI-Based | Rule-Based |

| DETECTION | ||

| How it works | Learns from historical data; scores every transaction against a model | Analysts write if-then rules; fires when a fixed condition is met |

| New attack types | Catches them and flags deviates from normal, even without a named pattern | Misses them, no rule = no detection |

| False positives | Lower – Danske Bank saw 60% reduction after switching to AI | Higher – broad rules block too many real customers |

| Fraud rings | Strong – graph models map connected accounts, devices, IPs | Weak – evaluates transactions in isolation |

| OPERATIONS | ||

| Setup | Complex – needs data infra, model training, ML expertise | Simple – analysts write rules, no data science needed |

| Maintenance | Low long-term – model retrain on new data automatically | High ongoing – every new fraud type needs a new rule |

| Scales with volume | Yes, improves as more data accumulates | Degrades – more rules = harder to coordinate and audit |

| COMPLIANCE | ||

| Explainability | Needs work requires XAI tools (SHAP, LIME) for reason codes | Native – every flag traces to a named rule |

| AML / KYC | Strong – detects complex laundering patterns, can auto-draft SARs | Basic – threshold-based checks only |

| BEST FIT | ||

| Use when | Growing transaction volume, diverse fraud types, compliance-heavy market | Early stage, limited data, simple, well-defined fraud scenarios |

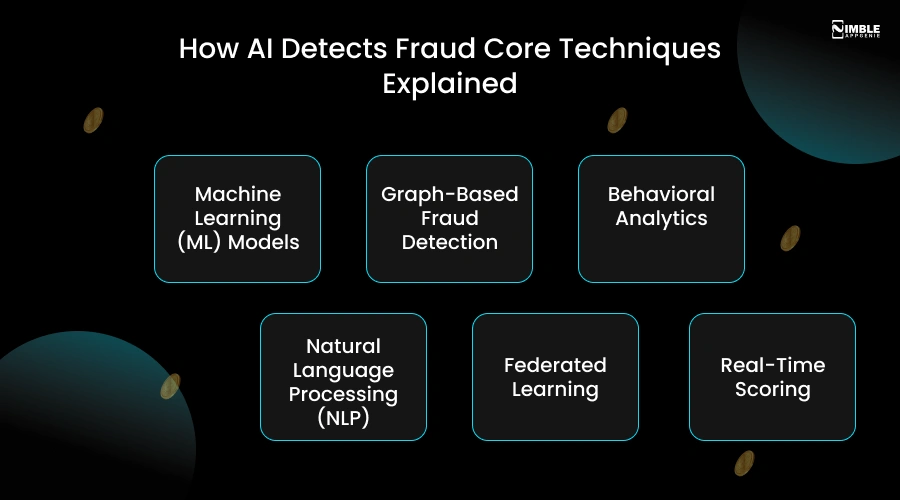

How AI Detects Fraud: Core Techniques Explained

Most people ask this question: how does AI detect fraud in fintech apps?

| 87% of global financial institutions use AI-driven fraud detection systems. |

AI doesn’t depend on rules. It learns from past transaction data, detects patterns, and flags new transactions that differ from what it has learnt. With the changing fraud patterns, the model updates.

Below are the main techniques used in production fintech systems:

1. Machine Learning (ML) Models

ML models are trained on labeled transaction data, marked as legitimate or fraudulent. The model learns which features identify fraud.

What machine learning models are used for fraud detection? Common models include:

- Gradient Boosting (XGBoost, LightGBM): Strong on tabular financial data.

- Isolation Forest: Useful for anomaly detection when labeled fraud data is scarce.

- Random Forest: Good for identifying complex combinations of risk factors.

- Neural Networks: Handle high-dimensional data and learn non-linear patterns.

| Also Read: Machine Learning in Banking: Use Cases, Benefits & More |

2. Graph-Based Fraud Detection

Fraudsters hardly operate alone. They use networks of devices, accounts, and IP addresses. Graph analytics evaluates relationships and detects clusters of accounts connected to known fraud. One confirmed fraudulent account can reveal dozens of linked suspicious accounts.

3. Behavioral Analytics

What is behavioral analytics in fraud detection? It’s a security approach that monitors how users interact with apps, websites, or financial systems to identify suspicious deviations from created baseline patterns.

Every user has a pattern, like how fast they type, when they often transact, how they scroll, and which devices they use. Behavioral analytics creates a baseline for each user. When something deviates from the baseline, the system raises an alert.

This is specifically effective to prevent account takeover fraud. Even if someone has the correct username and password, their behavioral fingerprint will not match the real user’s.

4. Natural Language Processing (NLP)

NLP is used to scan chat messages, transaction descriptions, and support tickets for fraud signals. During onboarding, it can also analyze documents, for example, detecting inconsistencies in proof-of-address documents and uploaded IDs.

5. Federated Learning

Fintech apps handle sensitive user data. Federated learning is a decentralized AI technique that allows financial institutions to train ML models across decentralized data sources without moving the data.

This permits better model performance without compromising user privacy, a growing need under GDPR and other regulations.

6. Real-Time Scoring

Each transaction gets a fraud risk score in milliseconds. Scores above a threshold are reviewed, flagged, or blocked automatically.

For example, Mastercard’s Decision Intelligence system screens 160 billion or more transactions per year using this approach, leading to fewer false declines and seamless customer experiences.

| Also Read: AI in Fintech: Benefits, Challenges, Role & Use Cases |

Key AI Fraud Detection Features Every Fintech App Needs

Most fintech apps need a core set of fraud detection features to handle payments, banking functions, or lending.

| Feature | What It Does |

| Real-Time Transaction Monitoring | Scores every transaction as it happens. Suspicious ones trigger a review, a block, or a step-up authentication request. |

| Device Fingerprinting | Identifies the device being used, including browser/app configuration, hardware identifiers, and behavioral signals. It flags new or suspicious devices. |

| Behavioral Biometrics | Tracks how users interact with the app, typing rhythm, tap patterns, and navigation speed to verify identity continuously. |

| Identity Verification (KYC) | AI-powered document checks and liveness detection during onboarding. Catches synthetic identities and deepfake-generated documents. |

| AML Screening | Monitors transaction flows against sanctions lists, PEP databases, and risk indicators. Flags unusual patterns that suggest money laundering. |

| Anomaly Detection | Flags any transaction or account action that deviates significantly from the user’s history, even without a specific fraud label. |

| Case Management Dashboard | A unified interface for fraud analysts to review flagged cases, view evidence, and take action. Reduces investigation time. |

| Explainable AI (XAI) | Every flag comes with a plain-language reason. Regulators want to know why a transaction was blocked; this satisfies that requirement. |

Real-World Results: What Companies Have Achieved

Let’s have a look at what actual companies have reported after deploying AI fraud detection in fintech.

1. PayPal

PayPal deployed AI in fintech fraud detection system that analyzes 500+ data points per transaction across 400 million consumer accounts, prevents $500 million in fraud quarterly, and maintains fraud rates perfectly below industry averages while delivering smooth customer experiences.

2. Commonwealth Bank of Australia

CBA achieved a 50% reduction in customer scam losses after deploying AI-powered safety features, including CallerCheck, NameCheck, and CustomerCheck.

They also witnessed a 30% drop in customer-reported fraud leveraging Gen AI-powered suspicious transaction alerts. Recently, in April 2026, their new agentic AI system diminished fraud losses by an additional 20% in the first quarter of FY2026 compared to the previous year.

3. Mastercard

Mastercard’s Decision Intelligence processes 143 billion transactions a year in real time. Decision Intelligence Pro, its generative AI upgrade, boosted fraud detection rates on average by 20% and up to 300% in some cases.

The brand also reports that by deploying generative AI, they have increased the detection rate of compromised payment cards before they are used fraudulently.

4. Danske Bank

Danske Bank adopted an AI fraud detection system, replacing its rule-based one, and achieved a 60% reduction in false positives with a 50% boost in true detection rates.

5. HSBC

HSBC’s AI system reduced false positives by 60% while detecting 2-4x more suspicious activities simultaneously. The system analyzes 1.35 billion transactions monthly and has dropped the investigation review time from weeks to days

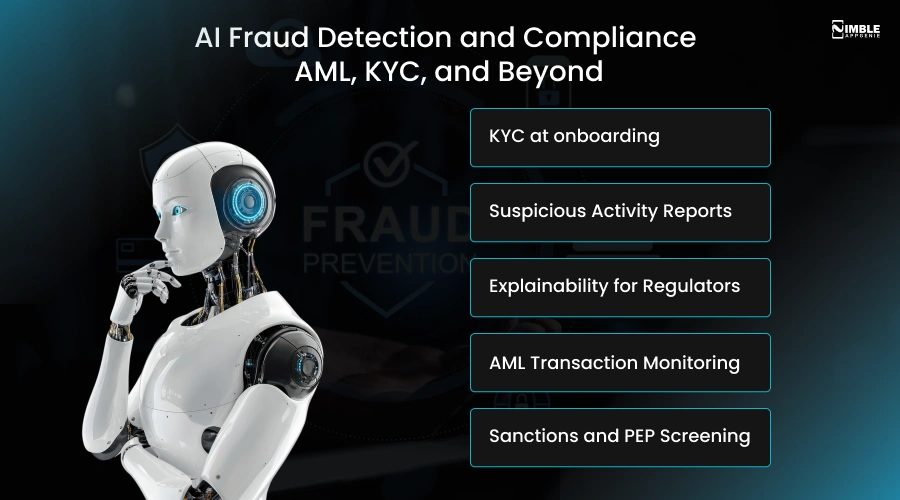

AI Fraud Detection and Compliance: AML, KYC, and Beyond

One of the biggest pain points in fintech is compliance. The rules are complex, mistakes are costly, and regulatory requirements vary across jurisdictions. AI fraud detection in fintech apps and compliance are closely linked. The same system that detects fraud also helps meet regulatory requirements.

As you are all set to kickstart fraud detection app development, you should know what compliance regulations does AI fraud detection help with?

Let’s get deeper to understand.

- KYC at onboarding: AI-powered identity verification runs liveness detection, checks documents, and screens against watchlists in seconds. Manual KYC, which used to take days, now occurs before the first session ends.

- Suspicious Activity Reports (SARs): AI can draft SARs automatically based on flagged transaction patterns, decreasing the compliance team’s manual workload.

- Explainability for Regulators: Regulators in the US, EU, and UK increasingly need institutions to explain why decisions were made. Explainable AI generates reason codes that meet this requirement.

- AML Transaction Monitoring: AI tracks money flows and flags patterns consistent with structuring, layering, or rapid movement, the classic signals for money laundering.

- Sanctions and PEP Screening: Constant screening against sanctions lists and politically exposed persons databases, updated in real time.

| One Important Note: AI handles the detection, but humans are still responsible for the compliance. The Block Inc./Cash App AML failure, which resulted in an $80 million settlement with regulators across 48 U.S. states, demonstrates this. AI was in place, but the failure was in how it was implemented and monitored. You should know that technology alone doesn’t guarantee compliance. |

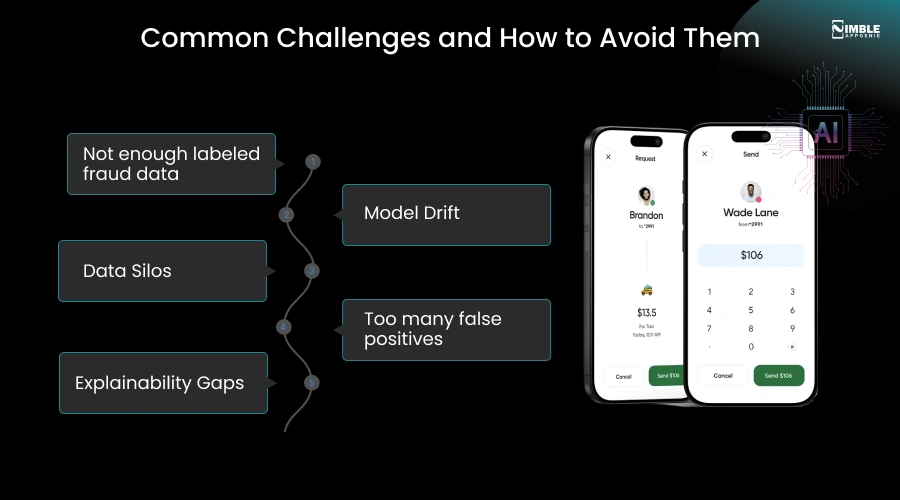

Common Challenges and How to Avoid Them

Embedding AI fraud detection in a fintech app is not easy. Problems will come in your way, and you should know how to handle them.

Let’s learn this.

1. Not enough labeled fraud data

ML models need training data. If your fraud rate is low or your app is new, you won’t have multiple confirmed fraud cases to train on.

Fix: Start with third-party risk engines or pre-trained models. Set up fraud labeling workflows from day one to enable expansion of your training dataset as your app grows. Synthetic data augmentation can fill early gaps.

2. Model Drift

Fraud patterns modify. A model trained on last year’s data will obviously miss new attack types.

Fix: Monitor model performance in production constantly, set up automated retraining pipelines, track key metrics, like recall, precision, and false positive rate, and alert when they drift outstripping acceptable thresholds.

3. Data Silos

According to the 2025 AI Trends in Fraud and Financial Crime Prevention report, 562 financial service professionals in the survey found that 87% cite accuracy and data management as their top AI challenge.

Legacy systems that operate in channel silos (mobile, card, and online separately) produce uneven data that builds an incomplete image of customer behavior.

Fix: Build a unified data layer before AI implementation, as it consolidates transaction history, behavioral signals, and customer profiles across all channels. This is architecture work that pays off in model quality.

| Also Read: Top FinTech Trends Transforming Financial Services |

4. Too many false positives

A model that blocks various legitimate transactions increases chargebacks, damages trust, and frustrates users. False positives in AI fraud detection fintech are a real cost.

How do fintech apps reduce false positives using AI?

Fix: Use step-up authentication despite hard blocks for medium-risk transactions. Ask for a biometric check or an OTP rather than outright blocking. Track false positives as a basic metric alongside fraud catch rate.

5. Explainability Gaps

Some AI models, especially deep neural networks, are hard to interpret. Regulators need to know the reason behind the blocked transaction. “The model flagged it” is not an acceptable answer.

Fix: Use explainable AI tools (LIME, SHAP) to generate reason codes for every decision. From the start, design explainability into the system architecture.

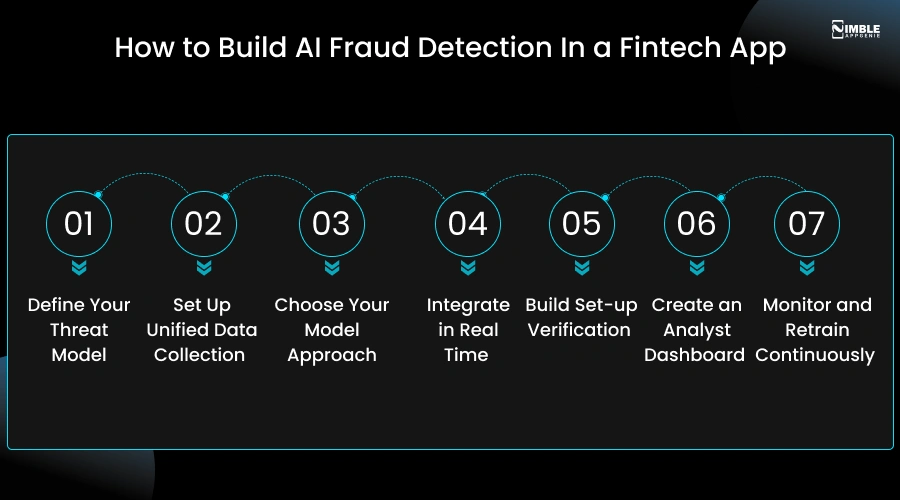

How to Build AI Fraud Detection In Fintech?

The steps below explain how to develop AI fintech fraud detection systems.

1. Define Your Threat Model

Account takeover, payment fraud, AML risk, and synthetic identity each have distinct signals. Know which threats are significant for your app type before choosing AI tools.

2. Set Up Unified Data Collection

Log transaction data, behavioral events, device signals, and user actions across all channels from day one. The foundation is clean, structural data.

3. Choose Your Model Approach

Use third-party APIs and pre-trained risk engines early. Once you have transaction volume and labeled fraud data, you can build custom models.

4. Integrate in Real-Time

Fraud scoring should happen before a transaction completes. Design for low latency, and the added time should be under 200ms.

5. Build Set-up Verification

For medium-risk scores, trigger a set-up check (biometrics, OTP, and ID selfie) rather than an outright block. This decreases false positives while still catching fraud.

6. Create an Analyst Dashboard

Flagged cases demand human review for edge cases. Your fraud team requires a case management tool to investigate, act, and feed outcomes back to the model.

7. Monitor and Retrain Continuously

Track false positive rate, recall, and accuracy in production. Regularly retrain as new fraud patterns emerge.

On Timeline: Integrating a third-party AI risk engine into a current fintech app usually takes 8-12 weeks. Building a completely custom system, the best AI fraud detection for fintech startups on your data takes 4-9 months, depending on compliance requirements, data readiness, and app complexity.

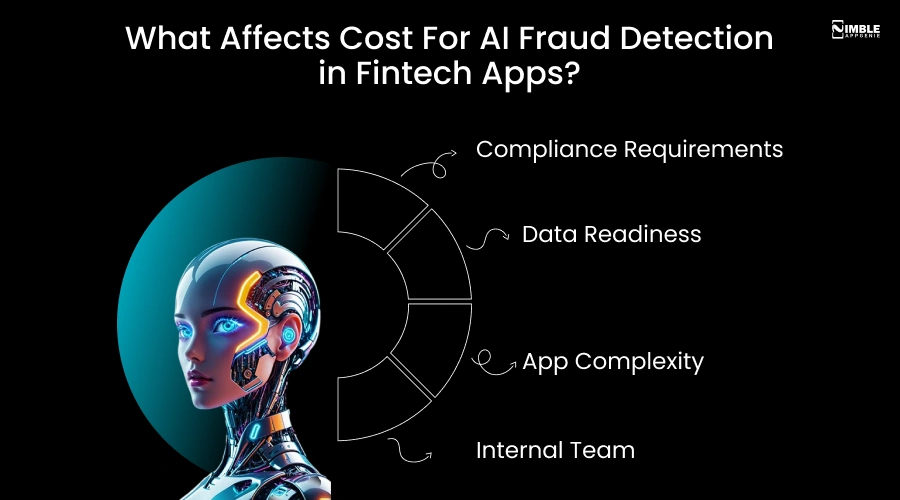

How Much Does AI Fraud Detection Cost for a Fintech App?

The first question that fintech founders and CTOs ask: “How Much Does AI Fraud Detection Cost for a Fintech App?” The answer depends on your build approach, compliance requirements, and transaction volume.

Two Main Approaches

- Third-party API integration: Connect to a platform like Sift, SEON, Sardine, or ComplyAdvantage. Pre-trained models, device intelligence, behavioral analytics, and AML screening are all out of the box. You pay per transaction or via a monthly subscription instead of building from scratch.

- Custom-built system: You own the model, the data, and the decision logic. That’s why the AI fraud detection cost for a fintech app is more upfront. This approach makes sense once transaction volume is high enough that per-transaction fees become expensive, or when your fraud profile is too specific for a general-purpose platform.

The best AI tools for fraud detection in banking are:

- Sift: Transaction fees start at 0.06 per transaction.

- AML and KYC compliance software subscriptions: Cover sanctions screening and PEP databases, typically run $15,000–$50,000 per year.

Cost By Build Complexity:

| System Type | Estimated Cost Range | Typical Scope |

| MVP AI Fraud Detection System | $40,000–$80,000 | Core compliance workflows, basic automation, limited integrations, and proof-of-concept AI capabilities. |

| Mid-Level AI Fraud Detection System | $90,000–$180,000 | Custom workflows, advanced integrations, enhanced reporting, role-based access controls, and scalable architecture. |

| Enterprise-Grade AI Fraud Detection Solution | $200,000–$500,000+ | Full ML pipelines, case management, explainable AI (XAI), advanced analytics, enterprise security, regulatory compliance, and multi-system integrations. |

Cost By Approach

| Approach | Best For | Dev Cost (Est.) | Timeline |

| 3rd-party API (Sift, SEON, Sardine, ComplyAdvantage) | Early-stage; limited data; fast to market | $15,000–$50,000 | 6–12 weeks |

| Pre-built + custom rules hybrid | Quick coverage with some tailoring | $40,000–$80,000 (MVP) | 2–4 months |

| Mid-level custom AI system | Growing fintech with transaction history | $90,000–$180,000 | 4–6 months |

| Enterprise custom AI (full ML pipeline) | High-volume, regulated, multi-product platforms | $200,000–$500,000+ | 6–12 months |

Ongoing Costs Teams Often Miss

The build cost is the visible part. These recurring costs are where teams get surprised:

| Cost Category | Typical Annual Cost |

| Cloud Infrastructure | $5,000–$100,000+ |

| AML/KYC Data Providers | $15,000–$50,000+ |

| Model Monitoring & Retraining | $10,000–$100,000+ |

| Fraud Operations Team | Varies by team size |

| Compliance Audits | $5,000–$50,000+ |

What Affects Cost For AI Fraud Detection in Fintech Apps?

- Compliance Requirements: KYC, AML, and multi-juridictions coverage add scope. Regulated markets need more audit trails and explainability.

- Data Readiness: Clean, perfectly labelled transaction data cuts development time. Siloed or messy data contributes to it.

- App Complexity: A single-product payment app costs less to protect than a multi-product platform.

- Internal Team: In-house ML engineers decrease build cost. If you don’t have them, that proficiency comes from hiring an AI app development company.

The ROI Case

Companies leveraging AI fraud prevention report 22% reduction in fraud-relevant costs and a 55% drop in detection and investigation expenses.

Every false positive stops a legitimate user, which is a lost transaction. Every fraud loss is a direct P&L case. And every compliance failure holds a fine risk. The real question is not what AI fraud detection costs. It’s whether the cost to create it is less than the cost of not adopting it.

Nimble AppGenie scopes custom build and API integration options. For a cost estimate suited to your app, contact us.

Read more: AI Fintech Fraud Detection System Development: Features, Architecture & Cost.

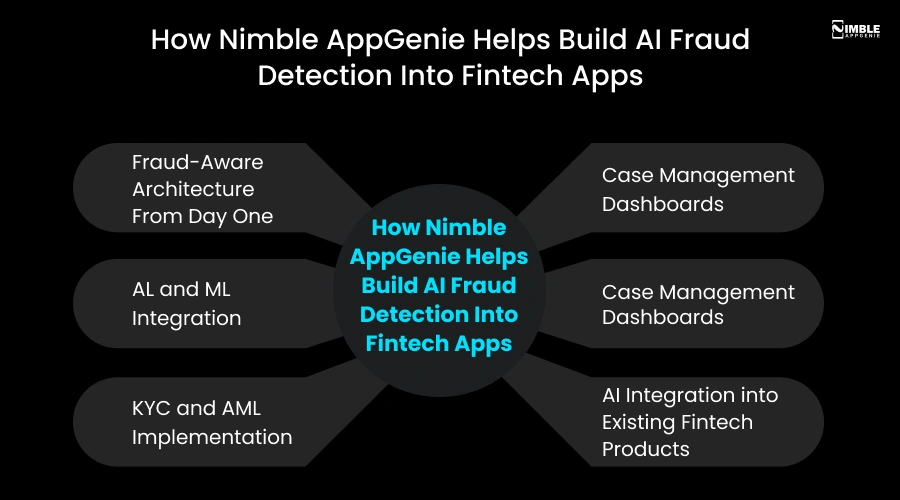

How Nimble AppGenie Helps Build AI Fraud Detection Into Fintech Apps

Nimble AppGenie, an experienced fintech app development company, build fintech apps from the ground up and integrate AI, compliance features, and fraud detection into both existing and new products.

We work with fintech startups, established companies, and scale-ups. Our work includes digital wallets, payment apps, lending apps, and mobile banking platforms across the US, Canada, UK, UAE, and other markets.

Our specifications on fintech app security AI, and fraud detection:

- Fraud-Aware Architecture From Day One: Fraud prevention is embedded into the system architecture, not retrofitted later.

- AL and ML Integration: We integrate real-time scoring engines, device fingerprinting, and behavioral analytics using third-party APIs and custom solutions depending on your budget and transaction volume.

- KYC and AML Implementation: We connect fintech apps to identify verification and AML screening providers and build the logic that manages the outcomes correctly within your onboarding flow.

- Case Management Dashboards: We create GDPR-ready, PCI-DSS-compliant AI fraud detection systems. Compliance is planned at the architecture stage.

- Case Management Dashboards: We build the internal tools your team needs to review, investigate, and resolve flagged transactions.

- AI Integration into Existing Fintech Products: If you already have a product and need to add real-time fraud detection fintech, we manage the integration without disrupting what you have built.

| Also Read: Fintech Security: Best Practices to Secure Financial Apps |

You can review our fintech app development services, our AI integration services, or our AI development capabilities for more details.

Final Thoughts

AI fraud detection in fintech apps is a practical need. The fraud problem is growing. Traditional rule-based fraud detection is not keeping pace. And the outcomes from leading fintech companies that have deployed AI accurately, like Mastercard, CBA, Danske Bank, PayPal, and HSBC, show that it works.

The gap between fintech companies with AI-powered fraud detection and those without it continues to widen. A fintech product that relies solely on static rules will eventually fall behind evolving fraud threats.

Building the right AI fintech fraud detection system needs the right architecture, data foundation, and AI team. If you are planning to embed AI fraud detection in fintech apps, new or existing, contact Nimble AppGenie for a scoping conversation.

FAQs

For most modern fintech apps, yes. Rule-based systems work for simple, well-understood fraud. But they cannot adapt to new attack types, generate too many false positives at volume, and require manual updates. The results from Danske Bank (60% fewer false positives, 50% more true detections) and HSBC (60% fewer false positives, 2–4x more suspicious activity detected) show the practical difference. Most experts recommend a hybrid: AI for pattern detection, rules for known triggers, and humans for borderline cases.

When a user initiates a payment, the app sends transaction data—amount, merchant, device, location, and behavioral signals—to the fraud scoring engine. The engine returns a risk score in milliseconds (Mastercard’s DI Pro generates a score in under 50ms). High scores block or step up authentication, while low scores pass. The process adds minimal latency to the payment experience.

A basic fraud detection MVP can be developed in 6–10 weeks, while an AI-powered system with machine learning, behavioral analytics, and real-time monitoring typically takes 3–6 months. Enterprise-grade fraud prevention platforms with advanced analytics, case management, and continuous model retraining can require 6–12 months or more.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.