Nimble AppGenie builds P2P lending platforms engineered for AI-powered credit decisioning, real-world compliance, and full loan lifecycle management. From borrower onboarding and lender dashboards to escrow, regulatory reporting, and secondary markets, we handle the full stack.

We help fintech startups, credit funds, neobanks, and financial institutions launch and scale P2P lending platforms across the US and UK. Our fintech software development practice covers the complete build - borrower UX, credit architecture, KYC/AML workflows, investor portals, and post-launch model iteration. Every platform we deliver is scalable, compliant, and production-ready.

150+ Fintech Apps Delivered

8+ Years of Experience

PCI-DSS Compliant

50+ Countries Served

Trusted By Fintech Leaders Worldwide

Our company is trusted by the leading fintech leaders worldwide. These people have trusted us with their resources, and we proved them right. Here is the list of top leaders:

The Window to Build a P2P Lending Platform Is Open - But Not Forever

Traditional banks reject almost 40-50% of SME loan applications. Borrowers want faster decisions, whereas investors want better returns than a savings account offers. P2P lending fills this gap directly.

Peer-to-peer lending platform development with the right credit infrastructure and compliance in the next 12-24 months will outshine to capture a disproportionate share of a quickly maturing market. Those fintech companies that cut corners on credit scoring and compliance pay for it later through defaults, regulatory action, or investor loss of confidence.

This is why the P2P lending platform development partner you choose matters as much as the product idea. We bring together fintech engineering, AI credit architecture, and regulatory-first design to help you launch with confidence.

The global P2P lending market is growing at a CAGR of 24.68%, from $222.90B in 2026 to an estimated $1.6T by 2035, reports Precedence Research. Business lending is the fastest-growing loan segment.

From consumer marketplace to white-label infrastructure, we build lending platforms tailored to your loan model, market, and compliance environment.

Custom P2P Lending Marketplace Development

We build custom P2P lending marketplaces from scratch, covering borrower application flows, auto-matching engines, lender investment dashboards, escrow management, KYC/AML pipelines, and admin controls. The architecture is designed for your borrower profile, loan product, and jurisdiction, not adapted from a generic template.

White Label P2P Lending Platform

Looking to launch fast without going ground up. Our white label P2P lending software gives you a pre-built, fully configurable lending marketplace you can brand, customize, and deploy quickly. Built on the same banking software development standards we apply to neobanks and financial institutions, it is ideal for credit unions, banks, and fintech startups.

SME & Business P2P Lending Platform

Business lending demands different underwriting logic - business credit history, cash flow analysis, director checks, and invoice verification alongside standard KYC. We build SME P2P lending platforms with lending criteria and risk grading models adjusted for business borrowers, including integration with open banking data for real-time financial visibility.

Consumer P2P Lending Platform

Personal loan P2P platforms need intuitive borrower experiences, automated decision engines, and soft-pull credit checks at application that reduce friction while maintaining underwriting accuracy. We help with consumer P2P lending platform development optimized for compliance, conversion, and scale, handling high loan volumes without degrading performance.

Secondary Market Development

A secondary market allows lenders to exit positions before loan maturity, enhancing platform liquidity and investment confidence. We build secondary market P2P lending modules with loan note listings, settlement flows, automated pricing logic, and regulatory-compliant transfer documentation, features most development shops don't include in a standard P2P build.

P2P Lending API Development

We build secure P2P lending APIs that integrate with credit bureaus, embedded finance providers, and open banking networks. Our solutions include REST APIs, OAuth 2.0 authentication, webhooks, sandbox environments, and developer documentation. Explore our lending software development services or read our loan origination software guide for origination-focused platforms.

Core Features We Build Into Every P2P Lending Platform

Every platform we deliver includes three layers of functionality: lender/investor tools, borrower-facing tools, and platform administration. Each layer covers the following features.

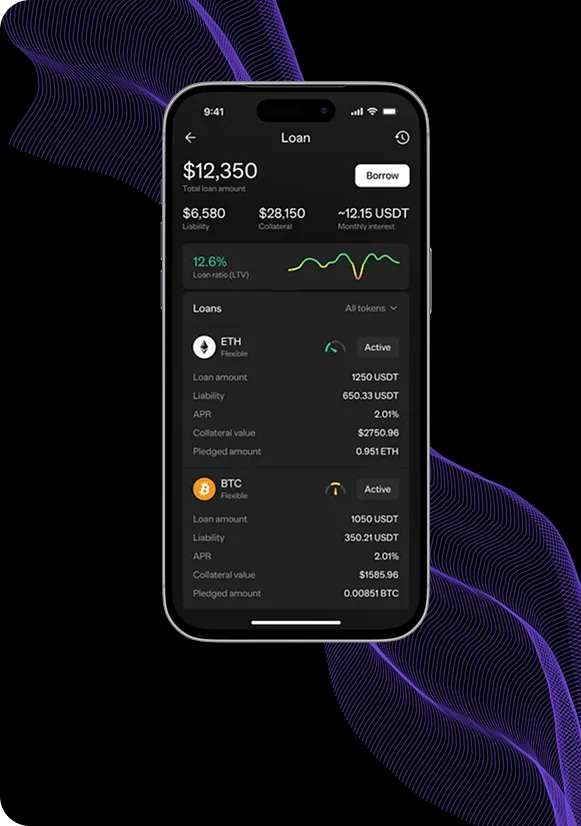

Digital Loan Application

Soft Credit Check at Application

AI Credit Scoring & Risk Grading

Loan Offer Comparison

eSign & Digital Documentation

Repayment Dashboard & EMI Tracker

Multi-step borrower application with income verification, document uploads, and real-time progress tracking. It’s mobile-optimized and built for high completion rates.

Runs a soft inquiry at the pre-qualification stage so borrower credit scores are not affected until they accept a loan offer. It reduces abandonment from credit-shy applicants.

Machine learning models assess creditworthiness beyond bureau scores, incorporating transaction history, income stability, and repayment behavior. Gives a risk grade used for rate-setting and lender matching.

Borrowers see multiple loan offers in a clear comparison view, including rate, term, monthly EMI, and total repayable before committing. It improves transparency and regulatory compliance.

Integrated e-signature for loan agreements, direct debit mandates, and consent forms. It’s legally compliant across UK and US jurisdictions with a full audit trail.

Borrowers track outstanding balance, upcoming payments, and payment history in a clean dashboard. Automated reminders reduce late payments before they become defaults.

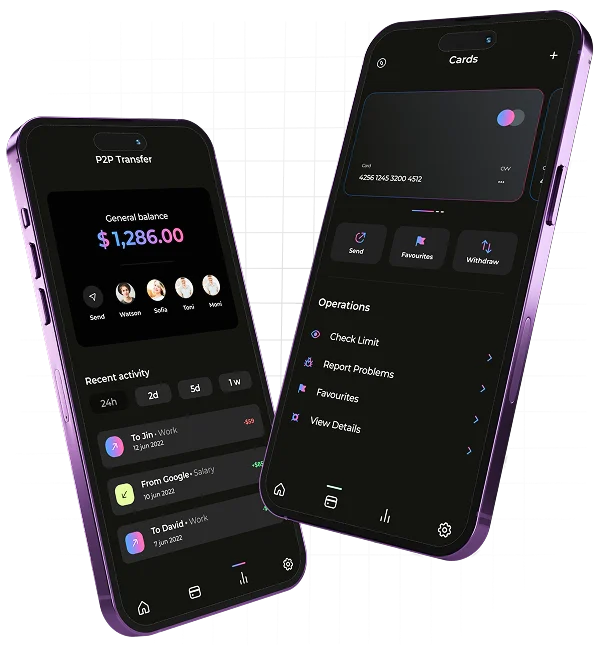

Lender Marketplace & Loan Browsing

Auto-Invest Engine

Portfolio Dashboard

Secondary Market Access

Investment Returns Reporting

Investors browse available loan listings with full borrower risk profiles, loan purpose, risk grade, and expected return. It filters by loan type, risk band, term, and geography.

Lenders set investment criteria - risk grade, loan type, maximum exposure per borrower, and the engine allocates funds automatically as new loans become available. It reduces manual effort and improves capital deployment speed.

Real-time view of active loans, expected returns, repayment status, and exposure by risk grade. Designed for retail investors and institutional lenders alike.

Lenders list loan parts for sale before maturity. The secondary market module handles pricing, buyer matching, settlement, and documentation transfer compliantly.

Tax-ready statements, IFISA-compatible reporting (UK), and downloadable transaction histories. It integrates with accounting tools where required.

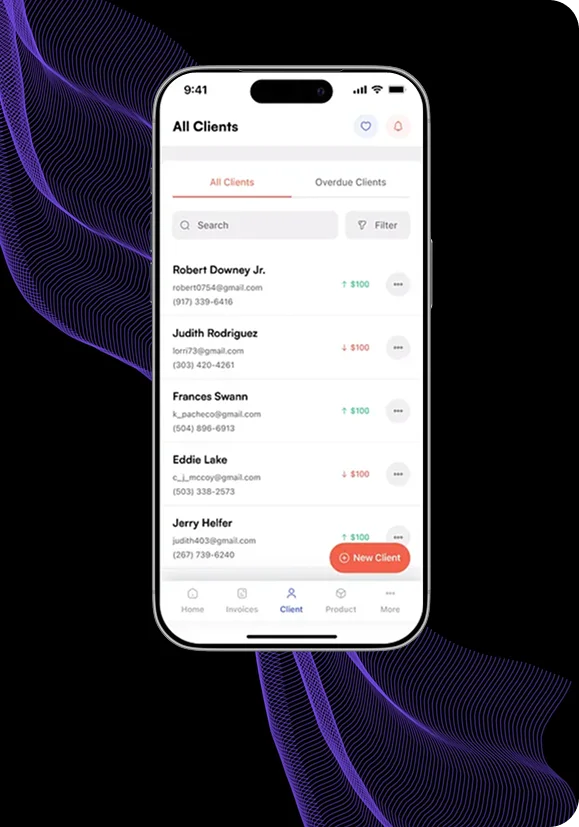

Borrower KYC & AML Verification

Lender Accreditation & KYC

Loan Matching Engine

Escrow & Fund Management

Collections & Default Management

Admin Risk Dashboard

Regulatory Reporting

Automated identity verification, sanctions screening, document checks, and PEP (Politically Exposed Person) checks. It integrates with leading providers, including Jumio, Onfido, and Sumsub.

Investor onboarding with identity verification, accredited investor checks (US), and appropriateness assessments (UK FCA). It stores documentation with a full audit trail.

Rules-based and AI-assisted matching of loan demand to available lender capital. It is configurable for your platform's risk model and loan product structure.

Segregated client accounts, ring-fenced fund flows, and automated disbursement upon loan completion. It meets FCA client money rules and equivalent US requirements.

Automated collections sequences, soft collections integration, and default escalation workflows. It supports third-party debt collection agency handoff with compliant data transfer.

Real-time portfolio risk view - NPL rates, delinquency by risk grade, vintage analysis, and exposure concentration. Gives ops and risk teams early warning on deteriorating cohorts.

Automated generation of regulatory reports for FCA (UK), SEC/CFPB (US), and other jurisdictions. It reduces compliance overhead and removes manual reporting risk.

Types of P2P Lending Solutions We Develop

Whether you are targeting retail browsers, real estate investors, SMEs, or emerging markets, we create lending infrastructure that fits the model.

Real Estate / Mortgage P2P Platform

Mortgage P2P lending platforms we create come with security documentation workflows, FCA Article 36H compliance for UK platforms, and property valuation integrations. Also suitable for US real estate crowdfunding under Reg CF and Reg D structures.

Student Loan P2P Platform

We build education financing platforms with income-linked repayment structures, income-share agreement (ISA) support, and university verification workflows. It's designed for alternative student lending programs that sit outside federal loan structures but need the same compliance rigour.

Invoice Financing Platform

By offering P2P lending software development services, we build platforms that allow businesses to raise funds against outstanding invoices. We develop invoice discounting and factoring marketplaces with debtor risk assessment, receivables verification, and automated repayment on invoice settlement.

Microfinance P2P Platform

Platforms serving underbanked and unbanked populations where alternative credit data - utility payments, mobile usage, and peer references - replace traditional bureau data. We build microfinance P2P platforms with offline-capable mobile-first UX, flexible loan structures, and local payment rail integrations for micro-loan products.

Crypto-Collateralized P2P Lending

Platforms where borrowers pledge crypto assets as collateral against stablecoin or fiat loans. We build crypto-collateralized P2P lending with automated margin call, real-time collateral monitoring, and liquidation logic, smart contract-based loan agreements, and multi-chain wallet integrations. For a detailed walkthrough of how P2P lending platforms work technically, see our guide on how to create a P2P lending app.

Our P2P Lending Platform Development Process

We conduct seven structured steps from business model design to post-launch support built to reduce compliance surprises, timeline risk, and expensive rebuilds after launch.

01

Discovery & Business Model Design

We start with mapping your loan product, target borrower profile, revenue model, and investor acquisition strategy. Here we resolve uncertainties before they become architectural issues - covering loan types, fee models, interest rate structure, and whether the platform is a marketplace, centralized, or hybrid.

02

Regulatory & Compliance Scoping

P2P lending is a regulated activity in each major jurisdiction. Our team scopes your licensing requirements (FCA Article 36H in the UK; SEC registration, state lending licenses, and CFPB obligations in the US), consumer protection requirements, and AML obligations. This shapes your development scope.

03

Credit Scoring & Risk Architecture

We design your underwriting model before starting platform code. This includes scoring variables, credit data scores, loan pricing logic, risk grading buckets, and default management workflows. Getting this right in the design phase avoids expensive model changes post-launch.

04

Agile Platform Development

Development runs in two-week sprints with regular client reviews. We create borrower UX, matching engine, lender portals, payment processing, KYC/AML integrations, and admin infrastructure in parallel tracks to compress the timeline without sacrificing quality.

05

Security Audit & Compliance Testing

Before soft launch, every P2P lending platform goes through penetration testing, data protection review (GDPR/CCPA), OWASP vulnerability assessment, and compliance workflow validation. KYC/AML flows, client money segregation, and escrow handling are all tested against regulatory standards.

06

Regulatory Review & Soft Launch

We support your SEC or FCA submission with technical documentation, compliance evidence packs, and data flow diagrams. Soft launch with a regulated cohort validates repayment processing, loan origination, and lender experience in a live environment before complete commercial launch.

07

Full Launch & Ongoing Support

Our full launch support includes infrastructure scaling, performance monitoring, and a dedicated support SLA. We offer ongoing development for credit model iteration as live portfolio data matures, feature roadmap delivery, platform optimization based on real user behavior, and regulatory change management.

Technology Stack We Use

We choose production-grade fintech infrastructure for scalability, security, and compliance. We ensure every component is proven in live lending environments.

Frontend

React.js

Next.js

React Native

TypeScript

Tailwind CSS

Backend / API

Node.js

Python

Django / FastAPI

GraphQL

REST APIs

Microservices Architecture

AI / ML

TensorFlow

PyTorch

fraud detection

auto-invest logic

Database

PostgreSQL

MongoDB

Redis

Elasticsearch

Payments

Stripe

Modulr

Railsbank (UK)

Dwolla

Plaid ACH (US)

SWIFT/SEPA

KYC / AML

Jumio

Onfido

Sumsub

ComplyAdvantage

Open Banking

TrueLayer (UK)

Plaid (US)

Yapily

Blockchain (Optional)

Ethereum

Solidity smart contracts

Cloud & DevOps

AWS

Google Cloud

Azure

Docker

Kubernetes

Security

AES-256 encryption

OAuth 2.0

ISO 27001

SOC 2 readiness

Built for P2P Lending Compliance from Day One

We prioritize compliance as much as platform functionality. Every architecture decision, from data flows to client money handling, is designed around regulatory obligations. For market-specific requirements, see our P2P lending regulations by country guide.

Lending Licences

FCA Authorisation: Required for all P2P lending platforms operating in the UK

State Lending Licences: US requirements vary by state and lending model

Why Choose Nimble AppGenie for P2P Lending Platform Development?

We are recognized as the top lending software development company in the US with 8+ years of fintech development across payments, lending, and digital banking.

1

Fintech-First Expertise

P2P lending platform development is not a standard software project. It includes financial regulation, fund management, credit risk engineering, and lender-borrower trust mechanisms - all in one product. Our P2P lending platform development company has built fintech products, including lending platforms, digital wallets, neobanks, and ACH payment systems, giving us the cross-domain depth that this type of build actually demands.

For a broader overview of fintech payment regulations across jurisdictions, see our fintech and digital payments regulations guide.

2

AI Credit Scoring Built-In

Most development agencies build the platform and treat credit scoring as a third-party bolt-on. We design the AI credit scoring architecture in Step 3 of our process before platform development starts. This means your underwriting model, loan pricing logic, and risk grades are native to the platform, not an afterthought.

3

Multi-Jurisdiction Compliance

We have delivered compliant fintech platforms for clients in the US and UK. In discovery, our process includes regulatory scoping, and we produce technical documentation showcasing data flow diagrams, security architecture summaries, and compliance evidence packs that directly support your FCA or SEC submissions. We have navigated both jurisdictions.

4

End-to-End Marketplace Build

We don't hand off lender dashboards to one agency, borrower UX to another, and admin infrastructure to a third. Nimble AppGenie delivers the complete platform - lender portal, borrower journey, matching engine, escrow, payments, KYC/AML, reporting, collections, and admin under one team, one accountability, one architecture.

5

Secondary Market Capability

A P2P lending platform with secondary market functionality is a differentiator that most platforms don't offer at launch and struggle to retrofit later because it impacts the loan agreement structure, regulatory position, and fund flow design. We design secondary market capability into the platform architecture from the start.

6

Post-Launch Credit Model Iteration

A credit model created before you have live loan data is a first draft. Post launch, after 6-12 months, as your portfolio matures, you need to adjust risk grades, tune scoring variables, and tighten or loosen underwriting criteria based on actual default patterns. We offer post-launch credit model iteration as part of our ongoing support service.

7

NDA & IP Protection

Every project starts with a signed NDA before any discovery discussion. All code, credit model design, and platform architecture produced by our team for your project is your IP transferred in full on project completion. No reuse of proprietary components, no shared codebases across clients.

P2P Lending Platforms We Have Built

Check our samples of lending platform projects across SME, consumer, and embedded finance verticals.

Consumer P2P Lending Marketplace (US)

Market / Vertical: US consumer lending - personal loans $5,000–$35,000

Challenge:

A fintech startup had a validated loan product and a retail investor network but lacked the technical platform to connect them. They needed FCA-equivalent US compliance, automated underwriting, and a lender portal that institutional investors would trust.

Solution:

Nimble AppGenie delivered a full marketplace platform, AI credit scoring with a 14-variable model, automated KYC/AML, borrower application and lender investment portal, escrow and fund management, and an admin risk dashboard with vintage loan analysis.

Platform live in 11 months, 1,200+ loan applications processed in first 90 days, default rate held within underwriting projections at 3.1%, and Lender retention above 78% at six months post-launch.

SME Invoice Financing Platform (UK)

Market / Vertical: UK SME lending - invoice discounting platform for B2B businesses with 30–90 day payment terms

Challenge:

An existing invoice factoring firm wanted to convert its manual process into a fully digital marketplace, allowing SME borrowers to list invoices and institutional investors to fund them in real time with FCA Article 36H compliance.

Solution:

Built invoice verification workflows with Companies House API integration, debtor risk scoring, automated FCA-compliant investor disclosures, CASS 7 segregated escrow, and an admin dashboard with real-time portfolio risk view.

Invoice processing time reduced from 5 days to under 4 hours, £2.1M funded in the first quarter post-launch, and FCA application submitted with a full technical documentation pack produced by our team.

White Label P2P Lending Platform (Neobank, US)

Market / Vertical: US neobank expanding from deposit and payments into marketplace lending for its existing user base

Challenge:

The neobank had 85,000 active users but no lending product. They wanted a fully-integrated P2P lending module within their existing app, not a standalone platform with the same-brand UX and shared KYC data.

Solution:

Embedded lending module delivered via API-first architecture, connecting to the neobank's existing user authentication, KYC store, and payment rails. Credit model built using the platform's existing transaction data as primary scoring input, improving approval rates vs. bureau-only models.

Launched in 8 months. 3,200 loan applications within 60 days, 22% higher approval rate vs. bureau-only underwriting, and loan origination contributed $1.4M to revenue in the first six months.

Frequently Asked Questions

Here are the common frequently asked questions that will help you to solve your common questions related to connecting with us and building a crypto wallet app:

A P2P lending platform is a digital marketplace that connects borrowers directly with individual or institutional investors. It manages loan applications, credit assessment, investor matching, fund disbursement, repayments, and collections through a single platform.

P2P lending platform development typically costs $40,000–$80,000 for an MVP, $120,000–$350,000+ for a full-featured platform, and $350,000–$600,000+ for enterprise-grade solutions. Cost depends on compliance requirements, integrations, loan products, and platform complexity.

An MVP usually takes 4–6 months, while a full-featured P2P lending platform can take 9–14 months. Timelines vary based on features, compliance scope, and third-party integrations.

AI credit scoring uses traditional credit data alongside alternative data sources such as banking transactions and income verification. It helps assess borrower risk, improve approval rates, and support better lending decisions.

Yes. Our white label P2P lending platforms include configurable loan products, compliance workflows, borrower and lender portals, and custom branding, helping businesses launch faster without building from scratch.

Core features include borrower KYC, AI credit scoring, loan origination, investor portal, auto-invest engine, escrow management, repayment tracking, and an admin risk dashboard. The exact scope depends on your loan product and target jurisdiction.

Typically, React or Next.js on the frontend, Node.js or Python on the backend, PostgreSQL for the database, and Python ML frameworks for credit scoring. KYC uses APIs like Jumio or Onfido, payments via Stripe or Dwolla, and infrastructure on AWS or Google Cloud.

Success Stories Client Testimonials

Nimble AppGenie is committed to delivering results that satisfy our client’s needs and their business objectives. Here are testimonials from our clients about their experiences of working with us.

Exceptional service tailored to our unique business needs. The team’s expertise brought my idea to life, making to process seamless. Their dedication to quality is commendable. Highly recommended for their professionalism and results.

Uri. S

(Managing Director of Xparking, USA)

“Nimble AppGenie delivered a standout website that has attracted significant traffic. Their collaborative and organized approach made the development process smooth. Their expertise shines in the end product, making them the go-to web development company in London.

Francis Ejiegbu

(CEO of StepbyStepFitness, UK)

We hired Nimble AppGenie for web development services related to our edtech platform, Glu Learning. They integrated well with our team to solve all the problems and deliver remarkable solutions. Their team have great command of both client side and server side technology. We highly appreciate and recommend their services.

Ryan Williams

(CEO of GLU Learning, United Arab Emirates)

"Our journey with Nimble AppGenie is defined by their consistent availability, reliability, and efficiency. As we look towards expansion, I'm confident our partnership will grow even stronger. And we are eagerly anticipating the next chapter with them.

Dr. Christian Herbert Ayiku

(CEO of DafriBank, South Africa)

For the last year, we have been working closely with the Nimble team to develop our app. Nimble has provided consistent customer care, good communication, solutions to issues, and an end product that we're all really happy with.

Daisy Girifalco

(Founder and President of skiMate)

BLOGS Our Latest Blogs

Read the latest blogs for the top industrial insights of development processes, tech guides, and the latest trends to stay updated & learn more.

Financial AI Assistant Solution

Financial AI Assistant Solution Insurance AI Agent Solution

Insurance AI Agent Solution Insurance Automation Software Solution

Insurance Automation Software Solution Banking Software Development

Banking Software Development Payroll Software Development

Payroll Software Development Hire Developers

Hire Developers Our Work Process

Our Work Process Awards

Awards