Banking Software Development

Banking Software Development Our Work Process

Our Work Process Awards

Awards

Key Takeaways:

- Payday loan software development helps lenders manage the complete loan process, from borrower applications and identity checks to loan approvals, payments, repayments, and compliance in one platform.

- The demand for payday loan software is growing as more borrowers prefer fast online lending services with quick approvals and mobile access.

- Key features include automated underwriting, instant loan decisions, ACH fund transfers, repayment tracking, fraud checks, compliance management, and reporting dashboards.

- To build payday loan software, businesses need to define lending rules, obtain licenses, design a secure system, integrate payment and verification APIs, and perform thorough testing before launch.

- Compliance is a major part of payday loan software, requiring lenders to follow CFPB rules, NACHA regulations, state lending laws, and data security requirements.

- The cost to develop payday loan software typically ranges from $25,000 to $200,000, depending on features, compliance needs, integrations, and overall project complexity.

Most payday lending platforms fail not because of a bad business model but because of poor architectural decisions made early on.

When businesses build payday loan software without focusing on speed, scalability, and compliance, they often face operational challenges from the start. A decisioning engine that takes 8 seconds to respond loses borrowers to a competitor that approves in 2 seconds.

A well-designed payday lending platform solves these challenges by automating borrower verification, decisioning, fund disbursement, and compliance workflows.

If you are a CTO, COO, or fintech founder and want to build payday loan software, this guide gives you the exact technical blueprint, instant decisioning, ACH disbursement, and compliance built in from day one.

So, let’s begin!

What is Payday Loan Software?

Payday loan software is a digital platform that handles the end-to-end lifecycle of short-term loans. It manages borrower onboarding, KYC, automated underwriting, fund disbursement via ACH, repayment scheduling, collections, and compliance reporting.

Payday loans are small, short-term loans that borrowers repay on their next payday. It is distinct from generic loan management systems because it is built for high volume, sub-30-second decisioning, and strict state-by-state compliance rules.

Modern payday loan software includes:

- A borrower-facing application portal

- Identity and income verification

- An automated decisioning engine

- Fund disbursement via ACH or debit push

- Repayment collection via ACH debit

- A compliance engine

- A loan management system for the lender’s back office

- Reporting and audit trails

Without these elements working together, approvals are slow, compliance breaks down, and defaults go untracked.

Market Statistics: Why Build Payday Loan Software Now?

The payday loans market is growing very fast. It was worth $166.09 billion in 2023 and is forecasted to hit $224.4 billion by 2032. Online lending platforms now account for 45.2% of all payday loan transactions, driven by demand for speed and mobile access.

Approximately 12 million Americans use payday loans each year, making payday lending a significant segment of the short-term credit market.

North America remains one of the largest markets for payday and short-term lending services due to the high adoption of online lending platforms and alternative credit products.

Fintech-powered payday lenders are taking market share from storefronts. The shift is happening because digital platforms approve faster, operate more cheaply, and scale further.

If your lending business still depends on manual processes, you are losing to competitors with better technology.

Essential Features of Payday Loan Software Development

The important features of mortgage software development are a borrower application portal, KYC/AML identity verification, automated underwriting, an instant decisioning engine, ACH fund disbursement, repayment scheduling, a collections module, and admin reporting dashboards.

You should integrate these in phase one. Everything else is optimisation. Let’s have a look at the payday loan software features list you can take into consideration.

| Core Feature | Description |

| Mobile-First Application Form | It allows borrowers to apply for loans using a simple mobile-friendly form with details such as name, income, employment, and bank account information. |

| Document Upload | It enables users to upload identity documents, proof of income, and other required verification files securely. |

| Real-Time Loan Status Updates | It provides instant updates on application progress, approval status, disbursement, and repayments. |

| Account Dashboard | It gives borrowers access to loan details, repayment schedules, transaction history, and account information. |

| Multiple Repayment Options | It supports repayment methods such as ACH transfers, debit cards, and other digital payment channels. |

| Loan Origination Dashboard | Centralized dashboard for managing applications, approvals, loan disbursements, and borrower records. |

| KYC/AML Verification Logs | It maintains records of identity verification and anti-money laundering checks for compliance purposes. |

| Decisioning Rule Configuration Panel | It allows lenders to create and modify automated underwriting and loan approval rules. |

| ACH Batch Management | It manages ACH payment processing, loan disbursements, collections, and settlement batches. |

| Collections Queue with Retry Logic | It automates repayment collection attempts and manages failed payment retries. |

| Compliance Audit Trail | It tracks all system activities, user actions, and compliance-related events for regulatory reviews. |

| Portfolio Analytics & Performance Reports | It provides insights into loan performance, repayment trends, default rates, and portfolio health. |

| State-Specific Fee and Rate Management | It automatically applies lending rules, interest limits, and fee caps based on state regulations. |

| Automated CFPB Adverse Action Notices | It generates and sends required notices when loan applications are declined. |

| NACHA Authorization Management | It handles ACH authorization records and compliance with NACHA payment regulations. |

| Credit Bureau Integrations | It connects with Experian, Equifax, and TransUnion for credit checks and borrower assessments. |

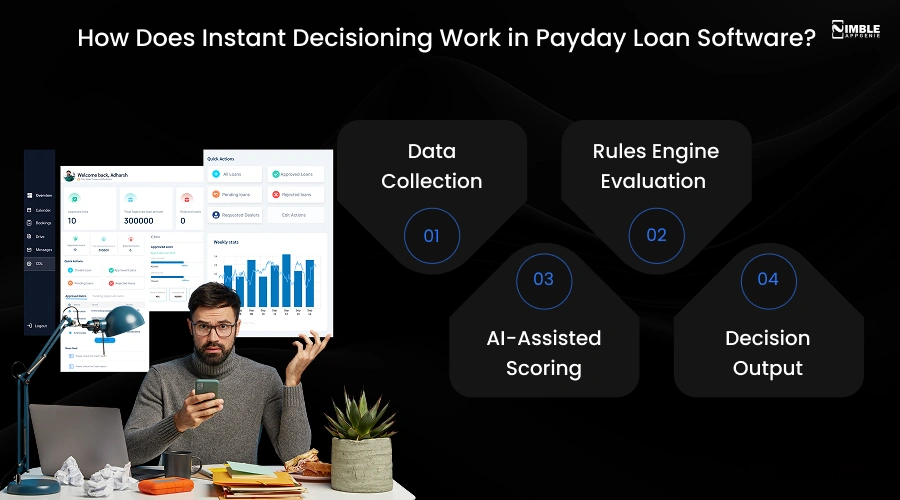

How Does Instant Decisioning Work in Payday Loan Software?

Instant decisioning in payday loan software works by connecting to real-time data sources and running the borrower’s data through a rules-based or AI-powered scoring engine.

A decision is returned in under 30 seconds, with no human review. Let’s take a look at the workflow:

1. Data Collection

The moment a borrower submits an application, the system fires parallel API calls to:

- Bank account verifier confirms account status and income patterns

- Identity verification confirms the person is real and not on fraud lists

- Credit bureau optional for thin-file borrowers pulls tradeline data

- Employment verifier checks payroll data in real time

2. Rules Engine Evaluation

The decisioning engine evaluates the borrower against a configurable credit box. Rules typically include:

- Minimum monthly income threshold

- Maximum debt-to-income ratio

- Active bank account with positive recent balance

- No active payday loans outstanding

- Income volatility score below set threshold

- ID match confirmed

Each rule returns pass or fail. The engine aggregates the results and produces a decision.

3. AI-Assisted Scoring

Some lenders layer in a machine learning model trained on historical repayment data. This helps approve thin-file borrowers who would fail a traditional FICO screen but have strong repayment patterns.

The ML score is an input to the rules engine, not a replacement for it.

4. Decision Output

The system returns one of three outcomes within 30 seconds:

- Approved: Loan amount and terms confirmed, disbursement triggered

- Declined: Adverse action notice generated automatically (CFPB required)

- Counteroffer: Smaller loan amount offered based on risk assessment

For returning borrowers, straight-through processing skips the re-verification steps and approves in under 10 seconds.

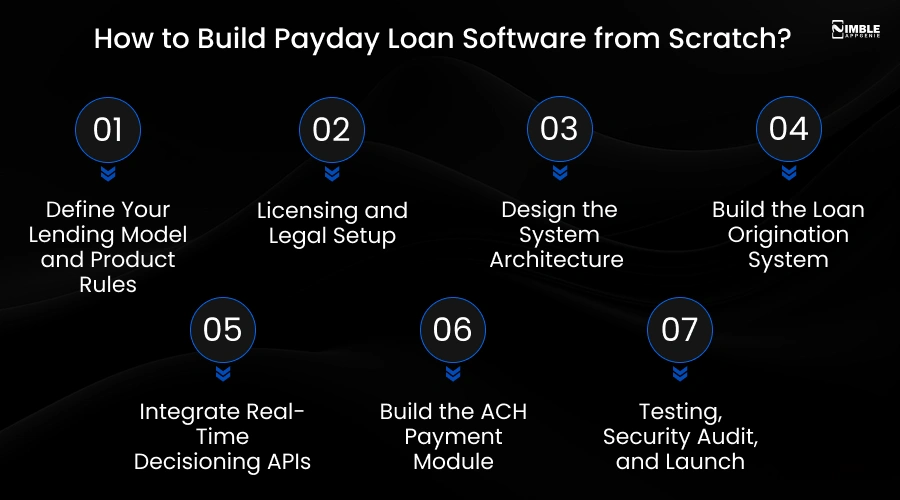

How to Build Payday Loan Software from Scratch?

To create payday loan software, you have to define the lending model, licensing and legal setup, design system architecture, build a loan-originating system, integrate an API, build an ACH payment module, test, and launch.

Let’s understand the payday loan software development process in detail.

1. Define Your Lending Model and Product Rules

Every technical decision downstream depends on what kind of lending product you are building. Start by answering:

- What states will you lend in?

- What are your loan amounts, rates, and fees?

- Will you lend to thin-file borrowers?

- Online-only or hybrid storefront + online?

- Will you use your own capital or a bank partner?

If you do not have a lending license, you may be able to operate as a technology provider for a licensed bank, a bank-as-a-service arrangement.

This significantly changes your regulatory footprint and can allow you to focus on technology, payments, and AI in lending rather than managing lending licenses directly.

Online only or storefront hybrid? Online-only is simpler to build, but some states require or incentivise storefront presence. Getting these decisions right in the planning stage prevents costly reworks during development.

2. Licensing and Legal Setup

You cannot legally originate loans without state lending licenses. Each US state has its own licensing regime, managed by the state’s financial regulator.

You can start the licensing process in parallel with development; do not wait for the software to be built before applying for licenses. You will also need to establish your ODFI relationship for ACH origination before launch.

If you are not a licensed bank, you need a bank agreement to originate ACH entries on your behalf. Building the legal entity, engaging fintech-specialist legal counsel, and filing license applications should all happen in the first month of the project.

3. Design the System Architecture

You can design a microservices architecture with clear service boundaries before writing any code. This design phase should produce an architecture diagram showing every service, every API connection, every data store, and every third-party integration.

Define the data model for a loan entity, every field, every state it can occupy, and every allowed state transition. Also, define the API contracts between services, what data flows in, what flows out, and what the error states are.

The most common architectural mistake in payday loan software is building the payment module too tightly coupled to the origination system, which makes it nearly impossible to swap payment providers or add new ACH capabilities without a full rebuild.

4. Build the Loan Origination System

The LOS is the first component to build because it establishes the core data model that every other service depends on. The borrower portal should be built in parallel with the LOS API.

You should create the application form first; keep it minimal. A 5-field form outperforms a 15-field form in completion rate. The bank linking flow must be smooth; any friction here causes borrowers to abandon before decisioning even starts.

The LOS API should handle creating a loan application record with a unique ID, storing KYC inputs, triggering the decision flow, and updating the loan record with the decision outcome.

The back-office dashboard can be a simpler internal tool, but it must expose the same underlying API as the borrower portal for data consistency.

5. Integrate Real-Time Decisioning APIs

You are connecting four or more external APIs that each need to run within a tight latency budget, ideally under 10 seconds combined. Each API integration needs authentication, request formatting, response parsing, error handling, and a fallback logic path.

You can store every API request and response in your audit log with a timestamp. This record is what regulators ask for when they want to see the basis for a credit decision.

The dedicated development team must develop the decisioning rules engine as a separate service with a clean API; the rules should be stored in a database and fetched at runtime.

6. Build the ACH Payment Module

The ACH module is the most legally sensitive technical component. Start by establishing your ODFI relationship and getting sandbox credentials for ACH testing. Build the ACH credit flow first, then the debit flow.

The ACH credit file generation must produce a valid Nacha-format file with correct field lengths, padding, and record counts. Run your generated files through a Nacha file validator before submitting to your ODFI.

Now, build the CFPB-required notice templates and hook them into the event trigger that fires when the two-strike block activates. Test every return code scenario in the ODFI sandbox before going live.

Read more about: How to Build ACH Payment Software?

7. Testing, Security Audit, and Launch

Do not cut corners on app testing. A compliance bug that gets past QA can trigger a regulatory action that costs more to resolve than the entire development budget.

You should run unit tests on every decisioning rule, specifically testing the boundary conditions.

Many platforms discover that their ACH batch processing is a bottleneck only under load, not in isolated integration testing. Commission a penetration test before launch. Most state licenses require evidence of a security audit.

Now launch with a soft rollout, start with a single state and limited application volume, monitor ACH return rates closely, and expand to additional states once you have confirmed the compliance layer is working correctly.

Tech Stack For Payday Loan Software Development

Choosing the right technology stack is important for building secure and scalable payday loan software. The technologies you select will affect everything from application performance and payment processing to data security and future growth.

So, it is best to check out the loan lending app tech stack table.

| Layer | Technology Choice |

| Frontend (Web) | React.js, Next.js |

| Mobile App | React Native, Flutter |

| Backend API | Node.js (Express), Python (FastAPI) |

| Database | PostgreSQL (primary), Redis (cache/queues) |

| Bank Verification | Plaid, MX, Finicity |

| ACH Processing | Dwolla, Nacha-certified ODFI, Stripe Treasury |

| KYC / Identity | Alloy, Trulioo, Onfido, Persona |

| Employment / Income | Argyle, Pinwheel, The Work Number |

| Credit Bureau | Experian, Equifax (via API) |

| Fraud Detection | Socure, Sardine, NICE Actimize |

| Cloud Infrastructure | AWS, Azure, or GCP (multi-AZ for uptime) |

| DevOps / Scaling | Kubernetes, Docker, CI/CD via GitHub Actions |

| Security | TLS 1.3, AES-256 encryption, OAuth 2.0 + JWT |

Kubernetes is particularly valuable here. Payday lending sees traffic spikes around paydays. It is typically the 1st and 15th of each month. Auto-scaling handles these surges without you manually provisioning servers.

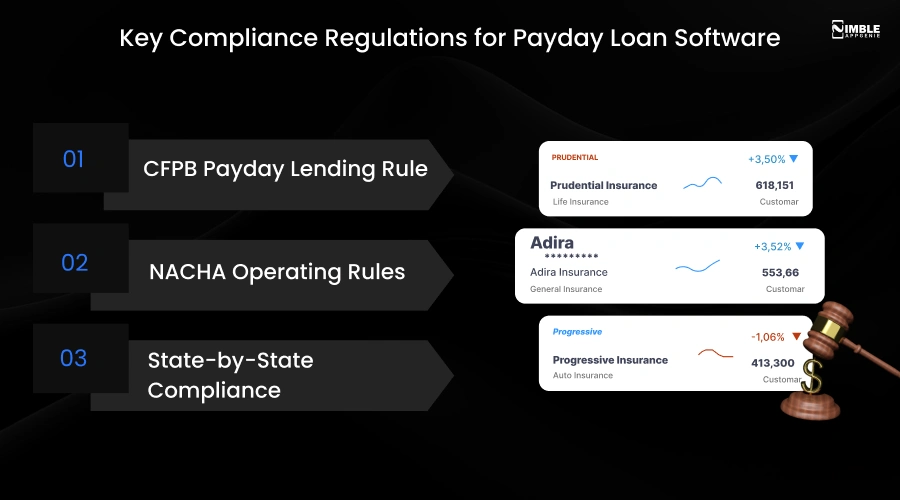

Key Compliance Regulations for Payday Loan Software

Payday loan software must comply with three layers of regulation: federal CFPB rules, NACHA operating rules for ACH transactions, and state-specific lending laws.

It covers interest rate caps, loan rollovers, and fee structures. Compliance is not a feature you add later. Build it into the architecture from day one. Take a look at the major security and compliance for digital lending software.

1. CFPB Payday Lending Rule

The CFPB rule took effect on March 30, 2025, following a Supreme Court ruling that upheld the CFPB’s constitutional funding. The current rule governs payment provisions, not ability-to-pay requirements, which were rescinded in an earlier revision.

What your software must automate:

- Two-strike ACH block

- Advance notice before first ACH withdrawal attempt

- Notice of consumer rights when two consecutive attempts fail

- Complete audit trail of every payment attempt and its outcome

- Adverse action notices when loans are declined

2. NACHA Operating Rules

NACHA governs how ACH entries are formatted, submitted, and handled. The major rules for payday lenders are:

- WEB entry type is required for online-originated ACH debits

- Written authorisation must be obtained and retained for WEB entries

- Annual audit of WEB debit origination practices is required

- Return rates must stay below NACHA thresholds

- ODFI risk management needs apply to high-risk originators

3. State-by-State Compliance

Payday lending is regulated differently in every US state. Some have banned it outright. Others cap APRs at 36%. Your software needs a configurable compliance layer, not hardcoded rules.

| Rule Type | What to Build |

| Rate/fee cap | State-specific; e.g., California caps at 36% APR |

| Maximum loan amount | Typically $300-$1000 depending on state |

| Rollover restrictions | Many states ban or limit rollovers |

| Cooling-off periods | Some states need gaps between loans |

| Database checks | FL, OK need lenders to check state loan databases |

| License requirements | Every state has its own lender licensing regime |

Other Regulations are:

- Bank Secrecy Act (BSA): It requires an AML programme and SAR filing.

- Gramm-Leach-Bliley Act (GLBA): It requires data privacy notices.

- Fair Credit Reporting Act (FCRA): It governs credit bureau data use.

- Electronic Fund Transfer Act (EFTA) / Regulation E: It governs ACH authorisation.

How Much Does it Cost to Build Payday Loan Software?

The cost to build payday loan software can be around $25,000 to $200,000 for a custom build, depending on complexity, team location, and feature scope. An MVP with core features takes 2–4 months.

However, a full-featured platform with AI decisioning, multi-state compliance, and mobile apps takes 5–9 months. So, according to your project requirements, you must decide the budget.

Here is a table showcasing the breakdown of the cost to develop payday loan software.

| App Type | Estimated Cost | Timeline |

| MVP with core features | $25,000-$70,000 | 2-4 months |

| Midrange with multi-state | $80,000-$150,000 | 4-6 months |

| Enterprise with AI decisioning | $150,000-$200,000 | 6-9 months |

The figures above provide a general estimate, but the actual cost can vary from one project to another. Factors like development approach, project complexity, customization requirements, and the experience level of the development team can affect the final budget.

It is vital to first define your business goals and project scope early. It will help create a more accurate payday loan software development cost estimate and development timeline.

How Nimble AppGenie Can Help You Develop Payday Loan Software?

Nimble AppGenie is a trusted fintech software development company that has built lending platforms, digital banking products, and payment solutions for global clients.

Our team develops custom platforms designed around your lending model, business rules, and operational requirements.

The Value We Bring to Your Project

- Faster development through proven fintech development practices.

- Scalable architecture that supports future business growth.

- Reliable integrations with banking, payment, and verification providers.

- Long-term technical support and platform enhancements.

- A solution designed to help streamline lending operations and improve efficiency.

Nimble AppGenie can develop lending software that is development-ready, compliant, and scalable. Whether you are a startup building your first lending product or a lender modernising legacy systems, we can help. Contact us for a free discovery call and technical scoping session.

Conclusion

Building payday loan software is a technical and regulatory challenge. Get the architecture wrong, and you face compliance fines, slow decisions, and high default rates.

Get it right, and you have a platform that processes thousands of loans per day with sub-30-second approvals and near-zero manual intervention.

So, it is vital to clear all the fundamentals like automating decisioning, building ACH correctly, enforcing CFPB rules from day one, and making your compliance layer configurable when you build payday loan software.

Digital lending is taking over from storefronts. You have to consult the right development partner that delivers end-to-end payday loan software development.

From system architecture and API integrations to compliance engineering and launch support. Get in touch with us to start your project today!

FAQs

The software itself does not need a license. But your lending operation does. Each US state requires a separate lender license. You also need an ODFI relationship for ACH origination. Build compliance features into the software while you pursue licensing in parallel.

The cost of payday loan software development can be around $25,000-$200,000, depending on your project requirements. It is best to first start with an MVP app and then later build the full-featured app.

Yes, if you have your own lending capital and state licenses. But for ACH origination, you need an ODFI, which is always a bank. Many fintechs partner with a BaaS bank to get ACH access without a full bank charter.

An MVP takes 2–4 months. A full-featured platform with AI decisioning, mobile app, multi-state compliance, and ACH integration takes 9–14 months. Timeline depends heavily on team size, location, and API integration complexity.

The minimum viable integrations are: bank account verification, identity/KYC, ACH processor, and credit bureau access. Additional integrations like employment verifiers, fraud scoring, and collections tools improve performance but are not required for launch.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.