AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways

- Payment modernization in banking is the system where banks transform their financial services into agile and cloud-native architectures.

- These systems offer modernization by converting batch to real-time processing and then automating the compliance networks.

- Banks can implement payment modernization by evaluating the existing system, establishing business objectives, integrating payment networks, testing the app, and then monitoring its performance after launch.

- The overall cost to implement payment process modernization can vary from $10,000 to $80,000 depending on the type of bank app.

- Partnering with the leading app developers, such as Nimble AppGenie, can help you to scale up from traditional and legacy banking systems.

Your customers depend on the third-party apps for making payments. Why can’t you upgrade your banking app to engage and retain your customers?

Well, payment modernization in banking has made it possible through integrating modern technologies and transforming the complete financial systems to a cloud-native architecture.

Overall payment processor market size is expected to grow from USD 63.87 billion in 2025 to USD 122.08 billion by 2031.

If you want to know more about what is payment modernization in banking, this is the right place.

In this guide, you will find details on the concept, why banks should opt for a payment modernization system, challenges, steps to implement, and much more.

Without further ado, let’s get started.

What is Payment Modernization?

Payment modernization is the strategic upgrade of an outdated financial system into an agile, cloud-native architecture. This term describes the complete journey and business strategy.

It is built to highlight replacing manual paper-heavy workflows with APIs, digital wallets, and AI-driven fraud detection. This enables real-time, 24/7 transactions and allows institutions to handle digital wallets and open banking APIs.

The core pillars of payment modernization are:

- Real-time Capabilities

- Data Enrichment

- Agile Orchestration

- Proactive Security

But the question remains, “What is payment modernization in banking?”

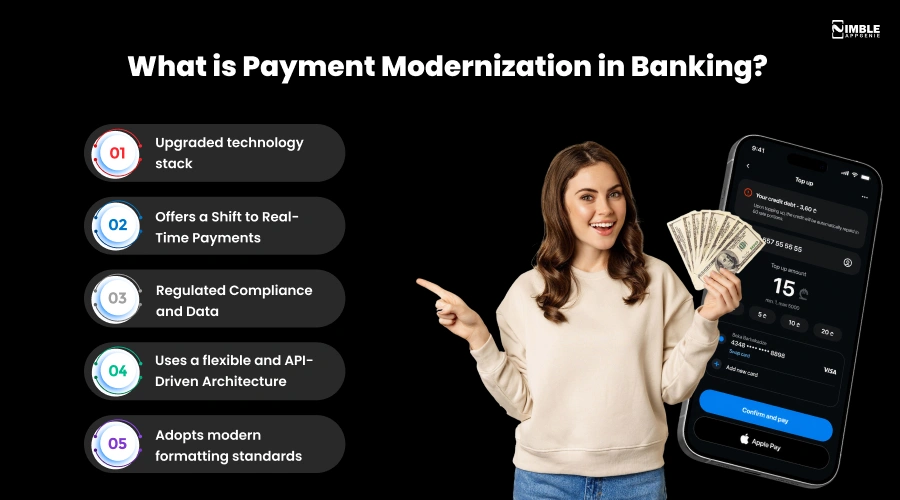

What is Payment Modernization in Banking?

Payment modernization in banking is the process of updating the traditional banking system with the latest technologies, such as real-time payments, software as a service (SaaS), blockchain, AI, and machine learning (ML), and all other latest technologies.

To keep pace with the market revolution, the banks in 2026 need to move on from their batch-based core banking systems.

Many fintech firms and entrepreneurs creating a banking app are looking for payment process modernization in banking. Here, the core banking transformation is increasingly a board-level issue rather than an IT-led initiative.

Here’s how payment modernization serves:

- Upgraded technology stack

- Offers a Shift to Real-Time Payments

- Regulated Compliance and Data

- Uses a flexible and API-Driven Architecture

- Adopts modern formatting standards

But how is payment modernization in banking replacing the traditional banking system?

Let’s get started with the same.

How is Payment Modernization Replacing the Traditional Banking System?

The payment process modernization in banking replaces the slow, manual batch-processing systems with real-time, 24/7 processing capabilities, leading to the authorization and settlement of transactions in seconds.

Here is the payment modernization process for traditional banking systems:

1. From Batch to Real-Time Processing

With the payment modernization systems in banking, there is no need to wait for hours or days to clear payments. Through modern systems, you can authorise and settle transactions in seconds.

The modernized networks do facilitate a continuous availability, authorizing and clearing payments in a matter of seconds.

2. Offers Advanced Security and Tokenization

The payment modernization systems do offer an advanced security landscape by employing multilayered protocols such as end-to-end encryption, AI-driven fraud detection, and tokenization to remove cyber threats.

It replaces the outdated legacy infrastructure with real-time, API-driven, and cloud-native frameworks.

3. Automated Compliance & Fraud Management

The automated compliance and fraud management replaces the traditional, manual banking systems by shifting the operations from reactive and human-led reviews to continuous and AI-driven governance.

Instead of relying on rigid, predefined rules and slow paperwork, the banks use intelligent systems to bridge machine speed with human intelligence.

4. Offers Built-In Audit Trails

These modernization systems do offer built-in audit trails through passively capturing the chronological, tamper-resistant data for every transaction.

It replaces manual, fragmented after-the-fact logs with automated, continuous traceability from the initiation to the payment process settlement.

5. AI & Continuous Monitoring

Payment modernization uses artificial intelligence to automate and secure financial ecosystems. This automation analyses live transaction data streams for instantly automating compliance and even removing the need for manual and reactive reviews.

With the help of machine learning, the payment process modernization identifies suspicious patterns and prevents fraudulent activity in real time.

Legacy Vs Payment Modernization Process

The traditional legacy banking system refers to an older, on-premises software platform that is used by banks for managing all banking operations.

However, the payment modernization process offers real-time processing through relying on parallel transaction execution, instant API-driven authorization, as well as round-the-clock uptime.

Here is the list of differences between the legacy and payment modernization processes:

| Aspect | Legacy Payment System | Payment Modernization System |

| Processing Speed | Batch-based, slower settlement | Real-time or near-real-time processing |

| Availability | Limited operating hours | 24/7/365 availability |

| Payment Types | Primarily traditional payment methods | Supports instant payments, digital wallets, APIs, and cross-border payments |

| Integration | Siloed, difficult to integrate | API-driven, cloud-ready, and easily integrated |

| Scalability | Limited scalability | Highly scalable and flexible |

| Security | Basic fraud detection and compliance | Advanced security, fraud detection, and regulatory compliance |

| Customer Experience | Slower transactions with limited visibility | Faster payments, real-time tracking, and improved user experience |

| Cost | Higher maintenance due to legacy infrastructure | Lower long-term operational costs through automation and modernization |

Based on the list of differences, you can identify that payment process modernization is a suitable and best way for banks to opt for the latest technology.

Well, if you are still confused, let’s consider the benefits of payment process modernization for banks in the next section.

Why Can’t Banks Ignore the Payment Modernization Process?

Banks cannot ignore the payment modernization process because they risk losing critical customer relationships and face severe operational inefficiencies.

Here is the list of benefits to consider:

1] Shifting Customer Expectations

Customer expectations have shifted from slow, and manual procedures to an expectations that transactions should be invisible with omnichannel availability, and should be invisible. Hence, banks are required to opt for a payment modernization process.

2] Faster Payment Processing

The need for faster payment processing is forcing the banks to adopt a payment modernization process because the older systems take 24 hours to reconcile and settle. The traditional systems are not built to handle speed; a switch is required.

3] Advanced Fraud Prevention

With the shifts towards instant real-time networks, banks no longer have the luxury of the multi-day holds for investigating anomalies and recovering funds. These banks are forced to completely re-platform their legacy infrastructure into modern agile systems.

4] Enhanced Security

In the current era, banks are focusing on boosting security parameters by implementing a multi-layered defense system. Here, the banks do integrate a multi-factor authentication (MFA), with advanced biometric and real-time fraud detection.

5] Regulatory Compliance

Banks in the present era do offer regulatory compliance through embedding strict operational frameworks as well as advanced RagTech. These practices do offer customer data protection and avoid steep penalties.

6] Offers Greater Scalability and Innovation

Scalability is forcing the banks to modernize because the legacy batch-processing architectures cannot handle the 24/7, real-time transaction volumes of modern digital commerce.

Fintech firms often ask, “How can I implement payment process modernization in my banking app?”

Let’s get the details in the following section.

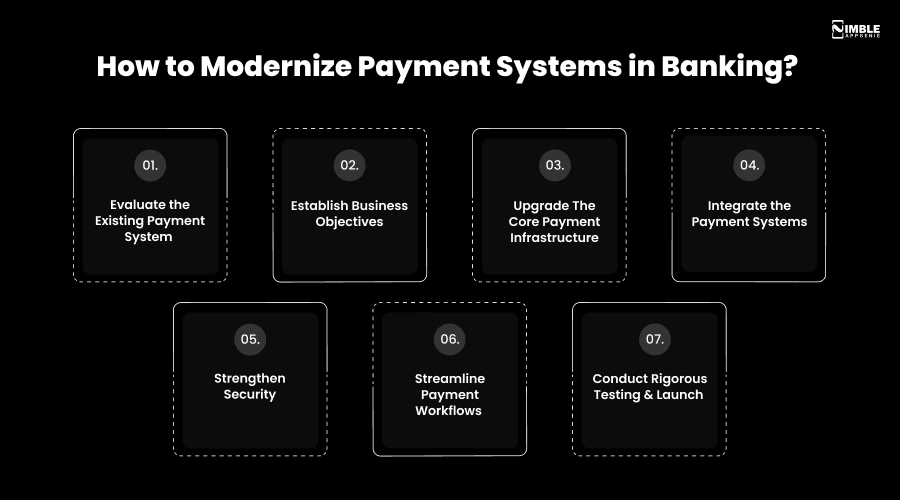

How to Modernize Payment Systems in Banking?

Modernizing a banking system refers to transitioning from legacy, batch-based infrastructure to an agile and real-time architecture.

Here are the ways to modernize the complete payment systems in banking:

Step 1: Evaluate the Existing Payment System

This is the first step where you need to identify the existing payment processes and systems and explore the need to modernize the payment system. In this step, you should analyze the key metrics such as transaction success rates, checkout conversion, and system reliability.

Step 2: Establish Business Objectives

Modernizing the payment systems does require aligning the technical upgrades with the institution’s core strategic goals. You should have an aim and a purpose that clarify the need to modernize payment systems in banking.

Step 3: Upgrade The Core Payment Infrastructure

This is the third step, where you are required to upgrade the core payment infrastructure without risking the operational stability of your banking app. Opt for a mobile app tech stack where you require a balance of security and the latest technologies for your banking app.

Step 4: Integrate the Payment Systems

Under this step, you should use APIs for building the modular “payment hubs” and even digital wrappers around legacy ledgers. This allows the adoption of real-time processing and even AI-driven security.

Step 5: Strengthen Security

Now, you should strengthen the security parameters, as when you integrate the payment process modernization, one of the most challenging aspects will be implementing robust security parameters for your banking app.

Step 6: Streamline Payment Workflows

For successfully streamlining the payment workflows, this is the step where you must remove the bottlenecks via automation, establish a standardized payment workflow, and implement an API-driven architecture.

Step 7: Conduct Rigorous Testing & Launch

This is the last step, where you need to consider rigorous testing during system modernization. Here, a skilled mobile app development company performs testing for security, operational workflow, and even functionality.

Well, with these payment process modernization steps, you can integrate payment process modernization in banks.

Here, fintech and bank startups often ask, “How much does it cost to me for adopting payment process modernization?”

Cost to Implement Payment Process Modernization

Implementing the payment process modernization typically costs between $10,000 and $80,000, depending on the skills of developers and the complexity of your banking app.

Here is the complete cost breakdown for implementing the payment process modernization in banks:

| Cost Component | Pilot Project (USD 10,000) | Full Modernization (USD 80,000) |

| Assessment & Planning | $1,000 | $6,000 |

| Software Licensing / Payment Platform | $2,500 | $22,000 |

| System Integration & API Development | $2,000 | $16,000 |

| Cloud Infrastructure & Data Migration | $1,000 | $10,000 |

| Cybersecurity & Compliance Upgrades | $1,200 | $9,000 |

| Testing & Quality Assurance | $800 | $6,000 |

| Employee Training & Change Management | $700 | $5,000 |

| Contingency & Post-Implementation Support | $800 | $6,000 |

| Total Estimated Cost | $10,000 | $80,000 |

Well, with this cost breakdown and within the process of payment modernization in banks, there might be a certain list of challenges you can come across.

Also Read: eWallet App Development Cost

Major Challenges and Pain Points (Bank and Fintech Startups)

Within the process of implementing the payment process modernization, banks come across certain questions and banking app development challenges.

Here is the list of some of them we generally solve:

“We can’t afford the downtime, but we cannot afford to remain the same either”

Staying with the same traditional legacy banking system will make your work and operational workflow incapable of delivering adequate services to your customers. This will result in losing your customers to competitors.

You can hire mobile app developers who know well how to implement payment process modernization without impacting the live operations of your banking app.

“High cost of legacy maintenance vs. uncertain ROI of modernizing”

Banks fear that if the legacy system maintenance is costing them 70% of the total revenue, adopting the modernization in banking systems will actually cost less or be a headache.

This has always been a resolution for the next year for almost every traditional bank; therefore, it’s important to analyse the skills of developers before you hire them.

“Integration complexity with existing core banking systems”

The payment systems are deeply wired into ledgers and liquidity engines. Here, banks worry that modernizing the payments in isolation will break something else, where a rip-and-replace approach is the only option, and that feels too risky to adopt.

Connecting with the experts and discussing with them your complete operational system is the only solution to consider here.

Why Connect with Nimble AppGenie for Payment Process Modernization?

If you are struggling with modernizing your banking app, Nimble AppGenie, a leading banking software development company, can help with a range of experts. We offer different solutions that cater to the diversified needs of banks and fintech institutions.

How we can help:

- Digital Wallets & Transfers: Nimble AppGenie is the leading eWallet app development company, which knows how to create robust e-Wallet apps that enable multi-currency usage and even real-time payment transfers.

- Offers Compliance and Security: Our app complies with the latest GDPR compliance practices by enforcing zero trust architecture. We offer privacy-preserving designs as well as AI-driven systems.

- Provides Risk & Audit management: Nimble AppGenie knows well where you can take risks and what the leading determinants are that can be helpful in performing audit management for your bank applications.

- AI-Powered Automation: The team at Nimble AppGenie provides AI development services, where we offer AI transformation for your traditional banking operations and app.

We have already done it before:

- Pay By Check: The app was built to simply payments via ACH & EFT support, which enables easy transfers and currency exchange patterns.

- MaxPay: MaxPay is a secure payment wallet that is designed for betting and fantasy apps.

- Swap Africa: This app was created for the African market to make everyday transactions simple and easy.

You can check out our latest case studies.

Conclusion

Banks cannot ignore the payment process modernization, because failing to update the limits in revenue growth, struggling with 24/7, and instant-transaction demands are growing, creating the need to switch towards payment modernization.

To implement this system, you should evaluate the need for your bank app to modernize, then follow the complete procedure from upgrading the core payment infrastructure to conducting rigorous testing. Here, the cost of implementation varies depending on the skills of developers and the complexity of the app.

The challenges related to downtime, or the risk of ROI in modernization, can be overcome by connecting with the top developers.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.