AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways

- Embedded finance adds payments, lending, or banking features directly into your app, no banking license required.

- Most platforms integrate with a Banking-as-a-Service (BaaS) provider instead of pursuing their own license.

- A single embedded payments feature typically costs $30,000–$80,000 and takes 3–5 months to launch.

- Compliance (KYC/AML, sponsor bank due diligence) has to be designed in from day one, not added after launch.

- Common revenue models: transaction fees, interchange, interest spread, and platform/subscription fees.

- Nimble AppGenie builds embedded finance platforms with compliance designed in from the start, from a single payments feature to a full multi-product platform.

Customers are asking for financing options at checkout. Competitors are embedding payments, lending, and business accounts directly into their products. Meanwhile, leadership teams are asking whether embedded finance is a growth opportunity worth pursuing or a costly compliance headache waiting to happen.

The challenge is rarely the idea itself. Embedded finance platform development involves deciding whether to build or partner, estimating the budget and timeline, and understanding whether regulations, infrastructure, and banking partnerships are actually required.

If you are a founder, CTO, or product lead trying to figure out whether building an embedded finance platform is worth it for your product, and what it actually takes, keep reading. This guide includes a practical, no-fluff breakdown and covers the real decisions you will need to make.

Who This Guide is For?

This is not a beginner explainer. If you are still asking “what is embedded finance,” start with our complete guide to embedded finance first.

This guide is for people already past the question – SaaS founders, eCommerce platform owners, fintech product leads, and marketplace operators – who are trying to answer a different set of questions: do we build this ourselves or partner with a provider; what will it cost, how long until launch, what compliance work is on us, and how do we actually make money from it. We will go through each one.

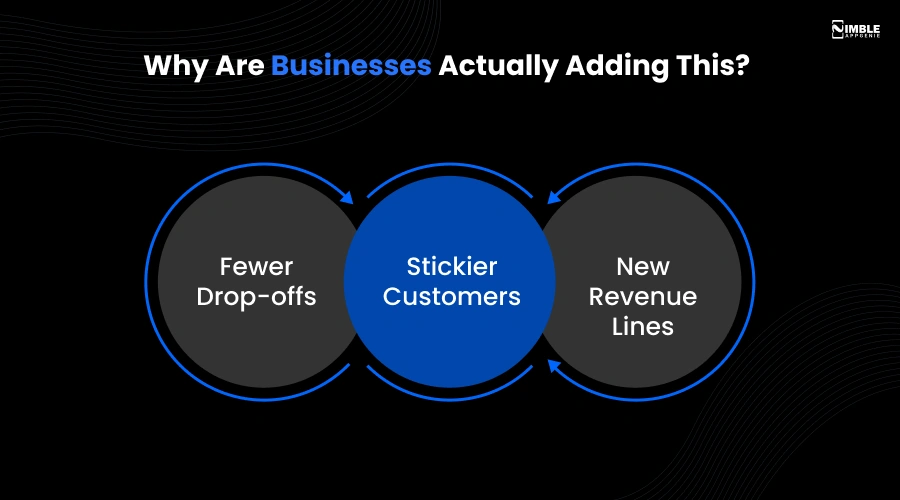

Why Are Businesses Actually Adding This?

Most customers don’t come requiring “embedded finance”. They want to get something done – pay a vendor, insure a shipment, get a small loan for equipment without leaving the app that they are already using. Embedded finance is how you make that possible, rather than directing them elsewhere to do it.

For your business, that unveils three concrete outcomes:

- Fewer Drop-offs: Every redirect to a third-party payment or lending site costs you conversions.

- Stickier Customers: Once someone’s money has moved through your platform, switching becomes challenging.

- New Revenue Lines: Interest spread, transaction fees, and interchange on volume you are already processing.

If you are a marketplace, the most common starting point is embedded payments or seller payouts. If you are a SaaS platform for small businesses or freelancers, embedded banking or lending tends to make more sense. Start with the product closer to a transaction you are already handling.

| Bain & Company projects US embedded finance transaction value will reach $7 trillion in 2026, accounting for 10% of all US financial transactions. |

Do I Need a Banking License to Build an Embedded Finance Platform?

No, not in most cases. You partner with a BaaS provider that’s connected to a licensed bank behind the scenes. The BaaS provider manages the banking infrastructure and regulatory relationship; you handle the product and customer experience.

Here’s how the three pieces fit together:

- Your Platform: It owns the user relationship and product experience.

- A BaaS/API Provider: It exposes financial functionality (cards, accounts, lending, and payments) through APIs.

- A Licensed Bank Behind the BaaS Provider: It holds the license and regulatory responsibility.

Getting your own banking license only makes sense once you are processing enough volume that the cost and time of licensing pay for itself, usually a phase-two decision for platforms already scaled through the BaaS route, not a starting point.

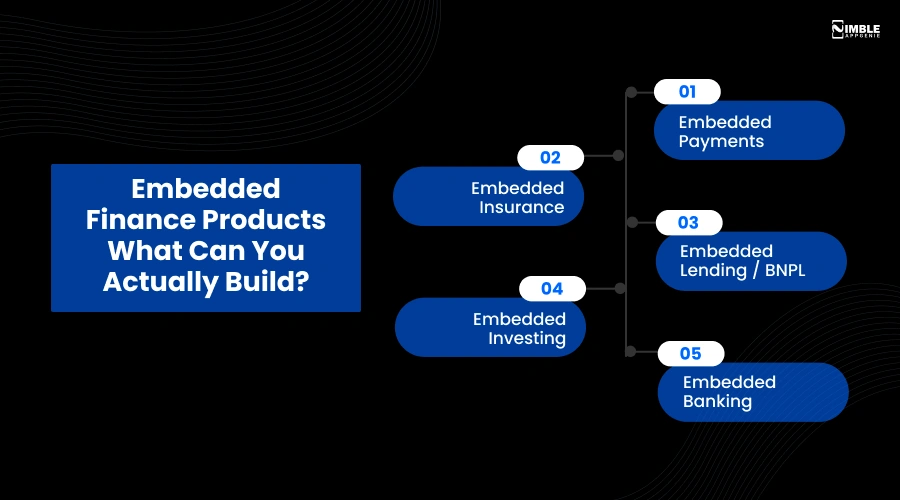

Embedded Finance Products – What Can You Actually Build?

Most businesses start with one product, prove it works, then expand:

- Embedded Payments: Wallets, in-app payments, seller payouts, and split payments.

- Embedded Insurance: Coverage offered at checkout (travel, shipping, and device protection).

- Embedded Lending / BNPL: Point-of-sale financing, installment plans, and working capital for sellers – see our BNPL app development services.

- Embedded Investing: Round-up investing, idle balance yield, and treasury tools for B2B platforms.

- Embedded Banking: Branded accounts and card issuance through a partner bank, identical infrastructure to our eWallet app development work.

Trying to launch all five at once is one of the most common reasons embedded finance projects stall. Pick one, ship it, then layer in the next.

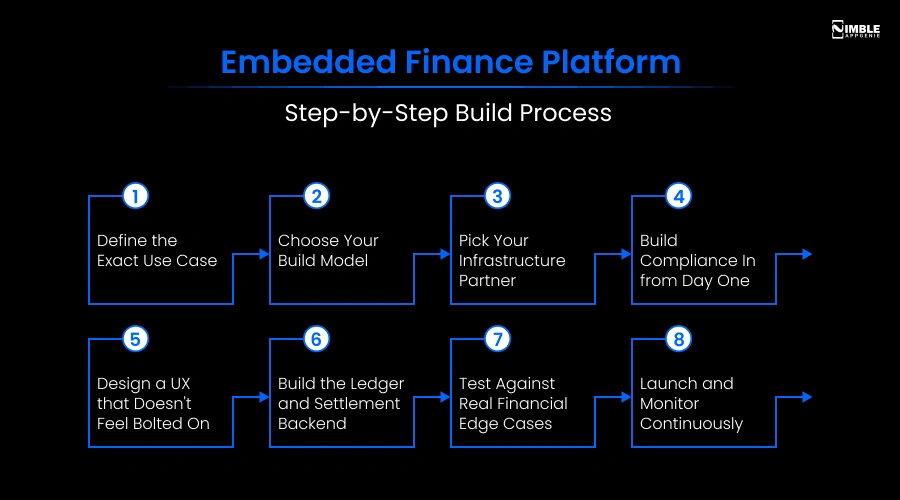

Embedded Finance Platform – Step-By-Step Build Process

1. Define the Exact Use Case

“Embedded payout for our marketplace sellers” is a spec you can build. “Embedded finance for our platform” is not.

2. Choose Your Build Model

API integration with a BaaS provider, a fully custom build, or a white-label platform. This single decision drives your complete cost and timeline.

3. Pick Your Infrastructure Partner

Depends on the product, your target country, and how much compliance work you want to own versus outsource. Ask tough questions about sandbox access, API docs, and what they actually handle for you.

4. Build Compliance in From Day One

KYC, AML, and identity checks should be included in your first wireframe, not an add-on feature before launch. Retrofitting compliance is the most costly mistake we see.

5. Design a UX That Doesn’t Feel Bolted On

The financial feature should feel like part of your product, not a handoff to someone else’s checkout page.

6. Build the Ledger and Settlement Backend

Invisible to users, non-negotiable- get right. Errors here become compliance issues fast, not only bugs.

7. Test Against Real Financial Edge Cases

Partial refunds, failed payments, compliance flags, and fraud triggers all need dedicated test coverage.

8. Launch And Monitor Continuously

Embedded finance products demand ongoing monitoring for fraud, reconciliation, and compliance reporting. This is not ship-and-forget.

Core Features You Will Need For Embedded Finance Platform Development

| Feature | Why it matters |

| Instant digital onboarding & KYC | Every extra second in onboarding costs you signups |

| Real-time transaction processing | Users expect instant confirmation, not batch settlement |

| Ledger & reconciliation engine | Required for accuracy and audit readiness |

| Fraud detection & risk scoring | Financial features are a fraud target from day one |

| Compliance reporting dashboard | Needed for your BaaS partner and regulator reporting |

| Multi-product architecture | Lets you add lending or insurance later without a rebuild |

How Much Does It Cost to Build an Embedded Finance Platform?

Cost depends heavily on your build model and how many products you are launching.

Use these as planning ranges:

| Embedded Finance Solution | Estimated Cost | Description |

| MVP | $30K–$80K | Build a single embedded payments feature using Banking-as-a-Service (BaaS) integration for faster market entry and validation. |

| Lending / BNPL | $50K–$150K | Develop embedded lending or Buy Now, Pay Later (BNPL) features with credit assessment and repayment management. |

| Full Platform | $150K–$400K+ | Create a comprehensive multi-product embedded finance platform with multiple financial products, APIs, and scalable infrastructure. |

Cost drivers, ranked by impact: build model (BaaS vs. custom vs. white-label), the compliance scope across regions, number of products launched with, and the depth of fraud/risk infrastructure your BaaS partner needs. For a wider view of infrastructure pricing, see our breakdown of top fintech APIs for startups.

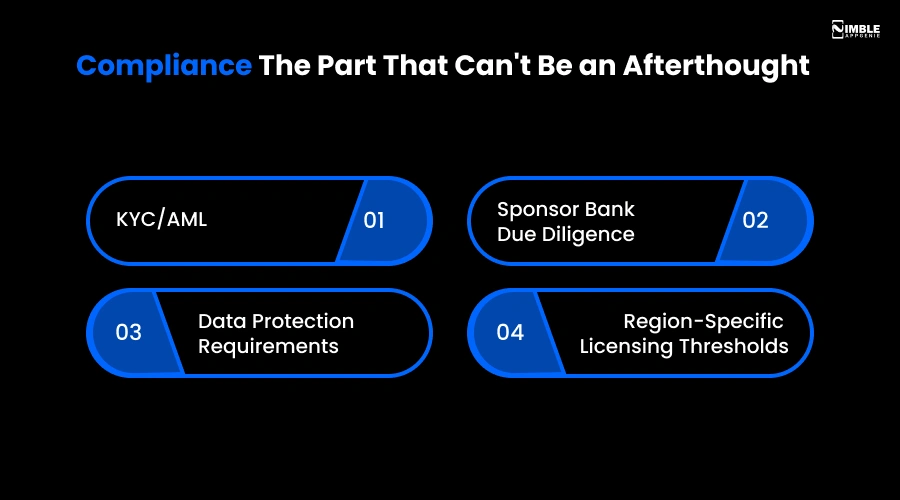

Compliance: The Part That Can’t Be an Afterthought

You don’t need a banking license, but you are not exempt from financial regulation either.

Plan For:

- KYC/AML: On every user transaction through your financial features.

- Sponsor Bank Due Diligence: Your BaaS partner’s bank runs its own risk assessment on your business, which can impact your launch timeline.

- Data Protection Requirements: Specific to financial data (GDPR and regional equivalents).

- Region-Specific Licensing Thresholds: Some activity demands no license; other activity crosses into money transmitter territory depending on geography and volume.

This is where the gap between a launch-ready product is widest, and where most timelines slip. Our Banking-as-a-Service explainer breaks down how BaaS, open banking, and embedded finance relate if you want the fuller regulatory picture.

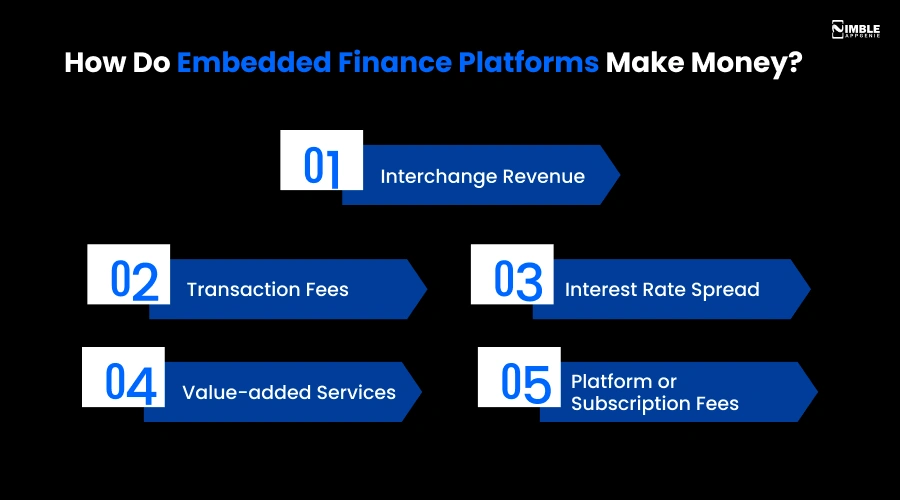

How Do Embedded Finance Platforms Make Money?

- Interchange Revenue: On card-based embedded products.

- Transaction Fees: A percentage or a flat fee per payment, loan, or transfer.

- Interest Rate Spread: On embedded lending or credit products.

- Value-added Services: Reporting, analytics, or premium features layered on top.

- Platform or Subscription Fees: Charged to merchant partners using your embedded finance layer.

Most platforms combine two or three of these rather than betting on one. For a wider view of fintech monetization, see our guide on how fintech apps make money.

Questions to Ask Before You Pick a BaaS Provider

- Which financial services do they actually offer: payments, lending, insurance, or all three?

- Is their API documentation public, current, and usable, or do you have to request it?

- Can you get sandbox access immediately, or does it require a sales call first?

- How much of onboarding, KYC, and fraud monitoring do they handle versus leave to you?

- What’s their track record with businesses in your industry and geography?

- How do they handle scaling, and can their infrastructure absorb a sudden spike in volume?

A BaaS provider that’s slow or vague on any of these is a signal worth taking seriously before you build your architecture around them.

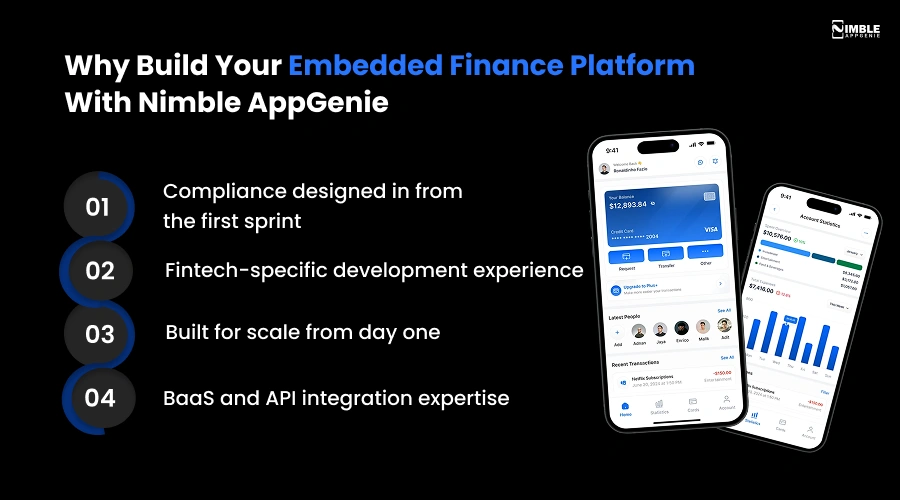

Why Build Your Embedded Finance Platform With Nimble AppGenie?

Building embedded finance right demands more than API integration. It takes a team that treats ledger accuracy, compliance, and fraud risks as part of the architecture, not an afterthought.

That’s the approach Nimble AppGenie, a fintech app development company, brings to fintech builds:

- Compliance designed in from the first sprint: KYC/AML flows, sponsor-bank requirements, and data protection are part of initial architecture, not an add-on after launch.

- Fintech-specific development experience: Including eWallet, BNPL, cross-border payments, and multi-currency wallets builds, not generic app development applied to finance.

- Built for scale from day one: Ledger and reconciliation systems designed to handle growth in transaction volume without a rebuild.

- BaaS and API integration expertise: Helping you evaluate and integrate the right infrastructure partner for your specific product and geography, instead of locking into the first vendor you talk to.

If you are evaluating whether to build in-house, hire a generalist agency, or work with a fintech-focused team, the last distinction is generally the one that determines whether your budget and timeline hold up past the MVP stage.

Conclusion

Embedded finance is not a feature to add later; it’s infrastructure you design in from the start. The businesses getting real ROI from it are not the ones chasing every product at once; they are the ones who pick a single use case close to a transaction they already handle, build compliance in from day one, and expand from there.

If you are weighing whether to build an embedded finance platform yourself, partner with a BaaS provider, or bring in a team that has done it before, the fastest way to get a real answer is to scope your specific use case against real cost and timeline figures.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.