AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- Digital microfinance uses AI-driven credit scoring and mobile data to lend to Africans with no formal credit history – no branch visit, no collateral.

- Mobile money adoption in Sub-Saharan Africa jumped 13.21 % CAGR through 2031, outpacing the global microfinance market average.

- Mobile money adoption in Sub-Saharan Africa jumped from 27% to 40% of adults (2021-2024), but only about 7% have actually borrowed through a mobile account – credit is the underused layer on top of payments infrastructure that already works.

- Tala, M-Shwari, FairMoney, and Branch prove the model works, but multi-borrowing, country-by-country licensing, and pricing transparency are the real risks to design around.

- Nimble AppGenie builds digital microfinance platforms – mobile disbursement, credit scoring engines, and fraud controls for startups, NBFCs, and banks entering the African market.

Africa’s unbanked population is no longer “unbanked” in the way it used to be. It’s “under-credited”.

Millions of people across Sub-Saharan Africa now have a mobile money account, a transaction history, and a smartphone, but no formal credit score. Digital microfinance exists to close the exact gap, and it’s expanding faster than almost any other fintech category on the continent.

This guide covers what digital microfinance is, how big the Africa-specific opportunity is, who is already winning, and the regulatory realities any new entrant demands to plan around.

What is Digital Microfinance?

Digital microfinance is the delivery of small, short-term loans (and relevant services like micro-savings and micro-insurance) completely through mobile apps, agent networks, or USSD, without collateral, paperwork, or a branch visit.

It’s created on three things traditional microfinance institutions (MFIs) never had at scale:

- Instant Disbursement: Loans land in a mobile wallet in minutes, usually through the same mobile payment infrastructure used for everyday transactions.

- Alternative Credit Scoring: Using mobile money transaction history.

- Automated Underwriting: Machine learning models that approve or decline an application without a human loan officer.

It’s a close cousin to the USSD-based mobile money systems we have covered in our USSD payment solution guide for Africa. But where USSD wallets move money, digital microfinance platforms decide who gets to borrow it, how much, and on what terms.

Let’s check the numbers explaining why fintech investors and bank CTOs keep circling back to this space.

| Metric | Figure |

| Global microfinance market size, 2026 | $285.03 billion |

| Projected global market size, 2031 | $480.73 billion |

| Global CAGR (2026–2031) | 11.02% |

| Middle East & Africa CAGR (through 2031) | 13.21% (above global average) |

| Licensed digital credit providers in Kenya (April 2026) | 227 Providers |

| Digital loans issued in Kenya (as of Feb 2026) | 7.5 million loans worth KSh 133.5 billion |

| Licensed digital lending platforms in Nigeria | 457+ Apps |

Most reports skip that mobile money adoption has surged, but credit adoption is still catching up.

Mobile money account ownership in Sub-Saharan Africa jumped from 27% of adults in 2021 to 40% in 2024, according to the World Bank’s Global Findex Database, yet only about 7% of adults actually borrowed through a mobile account in 2024, accounting for nearly 60% of all formal borrowing in the region. Savings and payments went mainstream first.

Credit is the new wave, not the current one; that’s why this is still an open market rather than a saturated one.

Two takeaways for anyone evaluating this space:

- Africa is growing faster than the global average: This isn’t a mature, saturated category; it’s still in expansion mode.

- Regulation is catching up fast: Kenya’s jump to 227 licensed providers, with stricter rules in draft, signals that compliance-by-design is no longer optional; check our breakdown of fintech and digital regulations for what this means for new entrants.

What People Are Actually Asking About Digital Microfinance Apps in Africa?

Seeing improved market figures, the would-be founders and users seek answers to the questions.

Let’s clear it all up.

1. Which Loan App is the Best in Kenya / Nigeria?

This is one of the most frequently asked questions on Quora and forums, and the genuine answer is “it depends on licensing and transparency, not just brand.” Branch and Tala lead in Kenya; FairMoney, Carbon, and PalmCredit lead in Nigeria, but users repeatedly flag that licensed, CBN- or CBK-regulated apps are safer bets than unlicensed ones.

2. How Do I Know if a Loan App is Legitimate or a Scam?

A recurring concern across user forums: “fake loan apps” that advertise low rates (e.g., 2%) but charge effective rates well above 10%, use aggressive contact-list harassment for collections, or operate without a banking license. This is a real trust gap in the market and a real product differentiation opportunity for compliant platforms. Google Play’s own policy now needs loan apps to disclose full APR and avoid contact-list access for collections.

3. How Much Does it Cost to Build a Loan App Like Tala or Branch?

You can find these questions asked repeatedly in founder and developer forums. Quoted answers online vary widely (from a few thousand dollars to six figures) because most don’t account for the credit-scoring engine, which is the real cost driver, not the app shell. See our detailed cost breakdown for the real number.

4. Are There Peer-To-Peer Lending Platforms Operating in Africa?

Yes, though most “digital microfinance” activity in Africa is app-to-consumer lending (Tala, Branch, and FairMoney) rather than true peer-to-peer. A small number of blockchain-based P2P platforms (e.g., Bitbond) operate across African markets including Kenya, but adoption is far smaller than app-based microlending.

5. Why Do People Get Rejected or Denied by These Loan Apps Despite Having a Mobile Money History?

A common frustration in user discussions: recent SIM swaps, irregular transaction patterns, or thin transaction history can all trigger automatic declines from scoring algorithms – this is a real UX and fairness challenge digital lenders are still working through, not a solved problem.

Who is Already Winning: Digital Microfinance Players in Africa

| Platform | Market | Model |

| M-Shwari | Kenya | Bank-telco partnership (NCBA + Safaricom) built on M-Pesa; largest share of Kenya’s digital credit market |

| Tala | Kenya, and expanded to the Philippines, Mexico, and India | Standalone app using smartphone and mobile money data for AI-driven scoring |

| Branch | Kenya, Nigeria, Tanzania | Algorithm-driven credit scoring using device and social data |

| FairMoney | Nigeria | Started as an instant-loan app, now holds a microfinance bank license from the Central Bank of Nigeria |

| JUMO | Multiple Sub-Saharan markets | AI-driven lending infrastructure powering bank partnerships, including a 2024 financing deal with Standard Bank in Uganda |

| Carbon (formerly Paylater) | Nigeria | Evolved from a loan app into a full digital bank with savings and bill pay |

The pattern across all of them: none stayed a single-product loan app for long. FairMoney and Carbon became licensed banks. Tala added savings tools. JUMO became infrastructure for other banks. The lending product is the entry point – not the end state.

That’s the same trajectory we have witnessed play out in eWallet app development across the region, where a single-feature app hardly survives past year two.

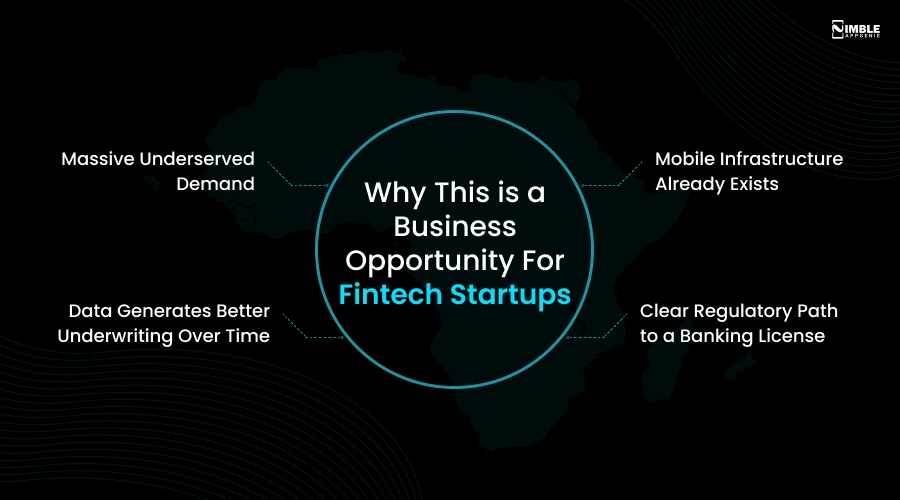

Why This is a Business Opportunity For Fintech Startups?

► Massive Underserved Demand

Over 2 billion people stay unbanked globally, and Sub-Saharan Africa carries a disproportionate share. Each represents a potential first-time borrower with no existing relationship with a bank or lender.

► Data Generates Better Underwriting Over Time

Every repaid loan improves the credit model. This creates a compounding advantage for early-launching platforms and ones that scale their data set more rapidly than competitors.

► Mobile Infrastructure Already Exists

You are not building on bare ground. USSD networks, mobile money rails, and smartphone penetration are already in place – the same infrastructure covered in our mobile payment technology breakdown. A lending app plugs into rails that already carry money.

► Clear Regulatory Path to a Banking License

Several players (M-Shwari, FairMoney) used a lending app as the on-ramp to a full microfinance bank license. A digital microfinance app can be step one of a much larger institution.

Already Decided to Build? Here’s Where to Go Deeper

Once you have validated the Africa opportunity, the build process itself is not unique to this region. Our P2P lending app build guide walks through the comprehensive development process step by step; our loan lending app cost breakdown covers pricing tiers in detail.

For a closer African market reference point specifically, see our FairMoney development cost guide.

Risks And Regulatory Realities to Design Around

Digital microfinance is not risk-free, and ignoring this in product design is how apps get pulled from app stores.

♦ Predatory Pricing Perception

Flat fees that look small can annualize into triple-digit APR (Annual Percentage Rates). Transparent, upfront total-cost disclosure is not only good practice – regulators are starting to require it.

♦ Multi-Borrowing

Many users borrow from one app to repay another. Build cross-platform default checks into your risk model from day one.

♦ Licensing Fragmentation

A model compliant in Kenya may not be compliant in Uganda or Nigeria. Multi-country expansion demands a country-by-country compliance review, not a copy-paste rollout.

♦ Data Privacy

Apps that demand full contact, phone, and SMS access without clear consent are facing increasing user pushback and regulatory action. Build minimal, consent-based data collection.

♦ Fraud

Synthetic identities and account takeover are rising issues in mobile lending. Pair this build with a dedicated fraud detection system and make sure your tech stack is built for the security and compliance load this category needs.

Why Choose Nimble AppGenie For Digital Microfinance App Development?

Nimble AppGenie has spent over seven years building fintech products for markets exactly like these – high mobile penetration, low traditional banking access, and a need for products that work on real-world connectivity, not best-case scenarios.

We have delivered 350+ projects for 250+ clients globally, including fintech platforms like SatPay and DafriBank, built specifically for the African market and operating conditions.

Our lending and credit infrastructure work covers:

- Alternative credit scoring engine design and integration.

- Mobile money and USSD disbursement integration.

- Multi-country regulatory and compliance structuring.

- Fraud detection and risk monitoring dashboards.

- End-to-end P2P and digital lending platform development.

Conclusion

Digital microfinance in Africa is not a speculative trend; it’s already a multi-million-dollar, multi-country industry with clear regulatory frameworks forming around it. The opportunity is real, but so is the operational complexity: fraud prevention, credit scoring, and compliance can’t be afterthoughts.

Validate the market, understand the regulatory landscape of your target country, and build toward a real financial institution, not just an app.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.