AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- A cross-border payment app allows users and businesses to send, receive, and hold different currencies across diversified platforms.

- The working process of a cross-border payment app begins with initiation, currency conversion, immediate processing, compliance checks, settlements, and confirmation.

- The cross-border payment app development begins with a market study, selecting the features, designing the app, selecting the right tech stack, testing, and then launching the app in the competitive market.

- The cost to develop a cross-border payment app varies from $15000 to $80,000+. Here, this cost can vary depending on factors such as the complexity of features, tech stack, design, and hiring app developers.

- The pain points include a lack of security, a wrong payment corridor, and high cost parameters.

- Connect with Nimble AppGenie and build your cross-border payment app successfully.

Picture this: An engineer works for his client in Dubai and gets paid after 5 days due to cross-border transactions; now multiply this amount by millions, and that’s the gap for your business to capture.

Now, you might be imagining how cross-border apps have become one of the most in-demand, as they are building fintech right now.

However, the cross-border payment app development is not simple; here you need to add a “send money abroad” button to an existing app. Here, you require a real-time currency conversion, fraud detection, as well as banking partnerships that most of the entrants struggle to secure.

In this guide to a cross-border payment app, we cover it all from the concept, working process, requirements of the app, methods, and a complete step-by-step development process of a cross-border payment app.

Hence, without any further ado, let’s get started.

What is a Cross-Border Payment App?

A cross-border payment app allows users and businesses to send, receive, and hold multiple currencies across different countries. These apps bypass traditional, slow bank wire systems by offering instant currency exchange and a seamless local payment method.

Depending on the nationality and region, the cross-border payments functionality changes. This cross-border payment industry now utilizes many payment modes such as credit cards, cross-border gateways, wire transfers, e-wallet, distributed ledger technology, APIs, etc., every day to facilitate international payments.

Different determinants of cross-border payment apps are:

- Digital Payments Regulatory and Compliance Frameworks

- User-Facing Interface

- Compliance Modules and Settlement Mechanisms

- Backend Processing

- Beneficiary Payout and Confirmation

But how does the cross-border payment work?

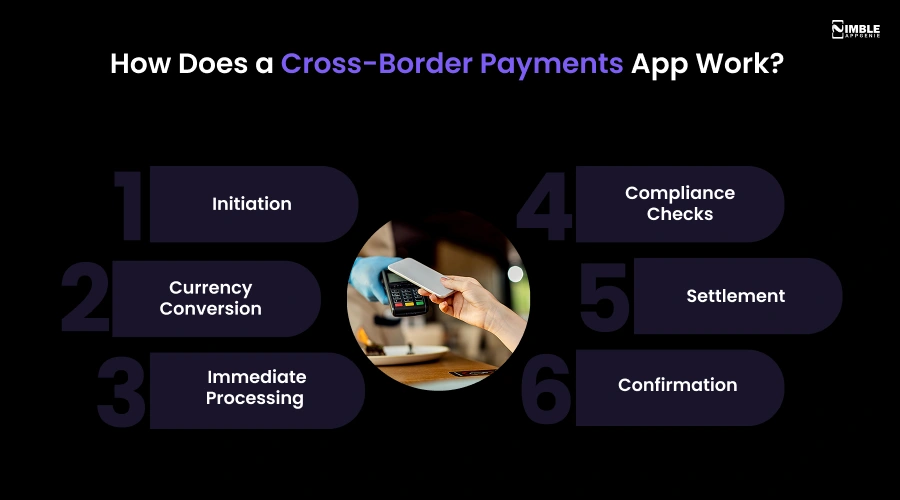

How Does a Cross-Border Payments App Work?

In the fintech market, the apps are unlimited, but the working process of the apps differs based on their targeted market and audience.

The cross-border payment app goes through a complete step-by-step working process:

Step 1: Initiation

Under this step, the sender creates a payment instruction with their bank or even a payment provider. Here, the user enters all the details of recipient’s details, such as bank account number, UP ID, and phone number.

Step 2: Currency Conversion

Here, the sender’s local currency is further converted to the recipient’s currency based on the foreign exchange rates. In this step, the currency is converted only when both currencies are different.

Step 3: Immediate Processing

Banks and fintechs process payments across different networks and systems. It is a real-time backend workflow. This step securely captures the payment details, executes instant compliance screenings, and conditionally settles funds across borders.

Step 4: Compliance Checks

Compliance is mandatory and non-negotiable for the cross-border apps; here, these apps check the compliance for both sides.

Step 5: Settlement

Under this step, you process the complete settlement, where the funds are routed and delivered to the recipient.

Step 6: Confirmation

Both parties get the notification of confirmation related to the payment received and debited. This confirmation is sent via message, mail, and other electronic means.

Here, the fintech startups often ask, “Why should merchants use cross-border payments?”

Why Should Merchants Use Cross-Border Payments?

Merchants use cross-border payments to instantly expand their global customer base, unlock new international revenue streams, as well as diversifies business risks across diverse economic landscapes.

Here are some of the reasons to consider creating a cross-border payment:

1. Expand Customer Reach

Efficient cross-border payments drive global expansion by removing the financial friction of international trade.

Through integrating localized, secure, and multi-currency options, the merchants remove the buying function, increase conversion rates, and then tap into global revenue streams.

2. Optimizes Currency Conversion

The cross-border payment platforms do optimizes the currency conversion using AI-driven routing, multi-currency accounts, and direct local clearing networks.

Cross-border payments minimize markup fees and eliminate hidden charges. Sometimes these digital rails bypass traditional intermediary wire networks by utilizing the local clearing channels and blockchain for settling transactions.

3. Offers Advanced Risk Management

The cross-border payments minimize international trade risks by using the automated, AI-driven, and data-rich infrastructure.

Instead of relying on slow, opaque networks, modern systems mitigate threats via several advanced mechanisms.

4. Diversified Business Risk

Cross-border payment infrastructure directly enables businesses to geographically diversify their operations.

By facilitating seamless international transactions, companies can hedge against local market downturns via global expansion and multicurrency liquidity management.

5. Growing Market Size

The global cross-border payment market size was valued at USD 187.7 billion in 2025 and is projected to grow from USD 193.5 billion in 2026 to USD 312.1 billion by 2033, at a CAGR of 7.1% from 2026 to 2033.

This growing market size indicates that the opportunity for cross-border payments apps is increasing rapidly.

Now, let’s get ahead with the different types of cross-border payments in the following section.

What are the Different Cross-Border Payment Methods?

Different types of cross-border payments include wire transfer, credit card transactions, electronic funds transfer (EFTs), international money orders, online payment platforms, and cryptocurrencies.

Here are the different types of methods to consider:

1. Credit Card Transactions

Credit cards are widely accepted and used around the world; here, businesses can accept payment from customers in different currencies.

This is one of the most significant methods of cross-border payments, where the credit card transactions may be subject to currency conversion fees.

2. Electronic Fund Transfers (EFTs)

The electronic fund transfers are commonly referred to as electronic bank transfers, e-cheques, or electronic payments.

Such transfers do allow individuals and businesses to quickly send and receive money electronically. This is a method in which faster and more convenient transfers are performed across borders.

3. Online Payment Platforms

To create a cross-border payment app, you need to know about the online payment platforms that act as a bridge between a buyer, seller, and the financial institution.

Through connecting with different global networks, these platforms act as an efficient method for cross-border payments, which allows users to send and receive funds efficiently.

Also Read: Payment Gateway Integration Guide

4. International Money Orders

The international money order is a secure paper-based document, which is similar to a check that is prepaid by the sender and even issued by a bank and postal services for transferring a specific amount to an overseas recipient.

It is a secure, paper-based document that is prepaid by the sender and issued by a bank for transferring money.

5. Cryptocurrencies

Cryptocurrencies do enable cross-border payments by replacing traditional banking networks with direct and blockchain transfers.

This type of method of cross-border payment app bypasses the traditional banking system, such as SWIFT, by utilizing decentralized networks between the parties in different countries.

Bonus Read: Guide to Crypto Platform Development

6. Wire Transfer

Wire transfer is an electronic transfer of funds between two different banks and financial institutions.

It is a cross-border method of moving funds between different countries that relies on a secure global messaging network and instructs banks to credit and debit accounts.

Here, the fintech startups often ask, “What is the best cross-border payment app for my business?”

Well, the selection process of the cross-border app payment depends on the target market preferences, translation success rates, regional compliance requirements, and seamless settlement.

But what is the right step-by-step process for a cross-border payment app?

Let’s check the complete process in the following section.

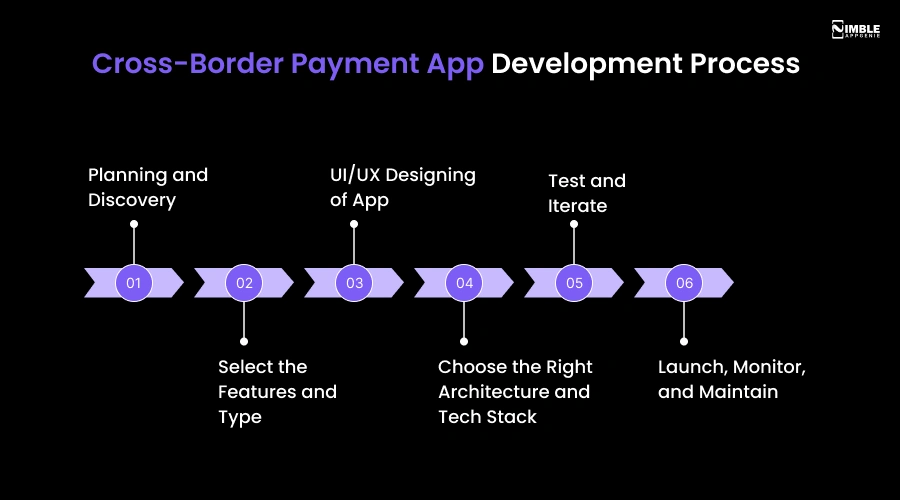

Cross-Border Payment App Development Process

The cross-border payment app development process begins with the market study, evaluating the core features to include in the app, designing the app, selecting the right tech stack, and then testing it.

The complete process of a cross-border payment app development is:

Step 1: Planning and Discovery

Do you need a cross-border app? If yes, then why?

Well, if you stick to your why, the process from selecting the app idea to launching it will have a purpose. Here, you should know what is included in the planning process and discovery process for beginning with your complete cross-border payment app development:

- State the complete objectives for your app.

- Select the right framework for your app and a type of approach.

- Discover the competitor’s landscape for your app

- Plan for hardware and performance.

Step 2: Select the Features and Type

Features act as the lifeblood of cross-border apps; here, the features can comprise multi-currency support, international shipping, and custom automations, as well as regulatory compliance. Additionally, select the right type and method that fulfill your app’s goal. Here’s what you need to do:

- Select the type that complies with your business goals.

- Multi-currency Wallets

- Live-exchange rates

- AI in fintech

- Automated KYC/AML verification

Step 3: UI/UX Designing of App

Under this step, you need to opt for a cross-border payment app design that should be user-friendly and engaging.

- Ensure that the button placements and navigation adhere to human guidelines

- Select the framework including react native, Flutter, and Kotlin.

- Integrate the core APIs during this fintech app design

- Design as per trust-centric user journeys

Step 4: Choose the Right Architecture and Tech Stack

What is the right tech stack for your cross-border app payment development?

Well, it depends on your app and the type of features that you have selected. For AI integration, you can connect with an expert AI app development company. Here is the table defining the tech stack to include in the cross-border app development platform:

| Layer | Technologies |

| Frontend (Mobile) | Flutter, React Native, Swift, Kotlin |

| Frontend (Web) | React.js, Angular, Next.js |

| Backend | Node.js, Java (Spring Boot), Python, .NET |

| Database | PostgreSQL, MySQL, MongoDB |

| Cloud | AWS, Azure, GCP |

| Architecture | Microservices + event-driven |

| FX Engine | Reuters/XE rate feeds, custom FX markup logic |

| Payment Rails | SWIFT, mobile money (M-Pesa), local ACH, stablecoins (USDC/USDT) |

| KYC/AML | Onfido, Jumio, ComplyAdvantage |

| Payment Gateway/API | Stripe, Wise Platform API, Airwallex |

| Security | Encryption, tokenization, OAuth 2.0, MFA/biometrics |

| Notifications | Firebase Cloud Messaging, Twilio |

| Fraud Detection | AI/ML-based risk scoring, rule-based monitoring |

Step 5: Test and Iterate

Testing is not the step to be done after the process; it goes on as the app development process executes. At every step of developing a cross-border payment app, you need to have a complete testing landscape. Whether it’s about fintech app testing or a cross-border payment app, here’s what you need to test:

- Test for security, functionality, conversion, and settlement accuracy

- Verify for compliance and KYC

- Evaluate the different errors and idempotency.

- Check for the end-to-end payment flow in the app.

Step 6: Launch, Monitor, and Maintain

At this step of your cross-border payment app development, you need to establish banking partnerships, secure the necessary licenses, and continuously monitor for latency and regulatory shifts. Here’s what you need to look for:

- Obtain the necessary payment and money transfer licenses

- Launch your app on the specific platforms.

- Monitor your app’s performance continuously.

- Offer long-term maintenance and support.

Here, the fintech startups and enterprises often ask, “What is the right cross-border payment app development process for my app?”

Well, for the right cross-border payment app development process, you need to identify your core app requirements, features, and the right framework for your cross-border payment app.

Another crucial determinant to identify is cost; hence, let’s drive it out in the following section

What’s the Cost of Cross-Border Payment App Development?

The overall cross-border payment app development cost can range from $15,000 to $100,000+, and this range varies due to different factors such as selection of technologies, right features, API integration, and platform choice.

In the given cost breakdown of cross-border payment app development, you will find the complete cost and its different factors impacting this cost:

| App Complexity | Features Included | Cost Range |

| Basic MVP | Single corridor, basic KYC, wallet, manual FX rates | $15,000 – $30,000 |

| Mid-Range App | Multi-currency wallet, real-time FX, automated KYC/AML, multiple payout rails | $30,000 – $50,000 |

| Advanced App | Multi-corridor support, fraud detection, compliance automation, admin dashboard, API integrations | $50,000 – $100,000 |

| Enterprise-Grade Platform | Custom liquidity management, advanced security, scalable microservices architecture, multi-market compliance | $100,000+ |

Now, with the help of the table stated above, let’s evaluate the right pain points, defining how the cross-border payments app development process has become an issue or is a challenge for companies like you.

Also Read: Fintech App Development Cost

What are the Common Pain Points of a cross-border payment app?

With the growing use of machine learning and the updated use of technology, here is a list of certain pain points often asked about.

We do have listed how we have resolved them all:

What are the key security measures I need to take for building my cross-border payment app?

Building the secure cross-border payment app requires a multi-layered security strategy that addresses data protection, strict user authentication, and leads to global regulatory compliance.

Lack of security in fintech apps is not a minor issue; it can even lead to losing your customers. Hence, it should be addressed with robust security measures.

How do I choose the right payment corridor to launch first?

Selecting the right payment corridor to launch first comprises balancing transfer volume, regulatory complexity, and fixing costs. Here, you should prioritize the route where you hold a competitive advantage, such as a large existing user base and a strong direct payout partnership.

Wrong payment corridor to launch can result in catering to the wrong audience. You should be well aware that a misleading payment infrastructure creates a ripple effect on the users.

Do we need a separate money transmitter license for every state or country where we operate?

Yes, you generally need a separate license for every country, or here you can use an EU/EEA passporting system to cover 27 countries or partner with another global banking-as-a-service provider.

Inappropriate licensing can result in voiding the contract agreement of your fintech business, which can even restrict you from a certain region or country. Get a license for your cross-border payment app to launch your business.

Should we build our own payment rails from scratch? What’s the real cost difference long-term?

No, you should not build your own payment rails from scratch unless you process over $100 million annually or payments are your core product, where building custom payment rails is a massive misallocation of resources. If you build it later, the difference can be huge, but building your own payment rails from scratch it will comprises of a wide resources.

The struggle with high transaction costs can end with building your own payment rails; however, building it from scratch will take a lot more resources.

What tech stack should I choose for building a scalable cross-border payment app?

The right tech stack to include for creating a scalable cross-border payment app is a polyglot, API-first architecture that balances real-time foreign exchange with the heavy transaction volume.

For the scalable cross-border payment app, you can make use of cloud-native microservice architecture.

Well, here, most of the startups and fintech enterprises often ask, “What can be the right monetization strategies for my cross-border app?”

The money-making strategies for a cross-border payment app can vary from a subscription model, a usage-based model, and a hybrid model.

In the following section, you can learn them all.

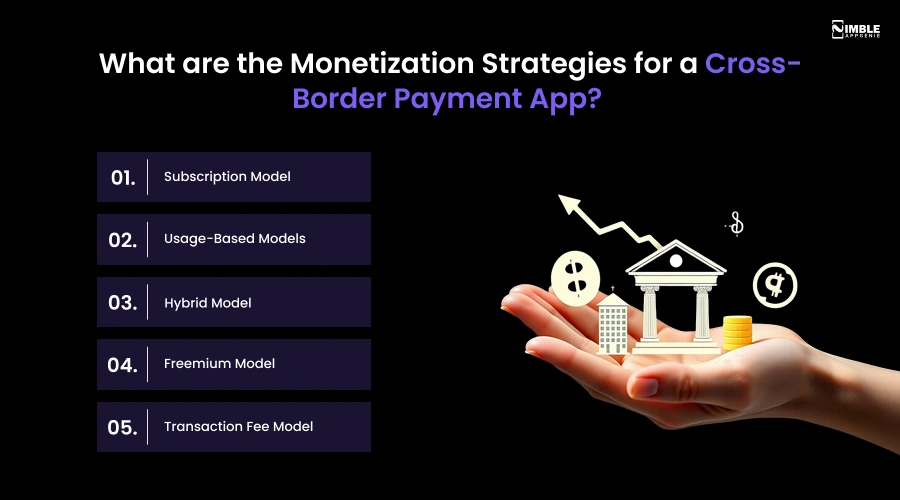

What are the Monetization Strategies for a Cross-Border Payment App?

The key monetization strategies for a cross-border payment app are a subscription model, which combines a fixed recurring fee for API access, a usage-based model, a freemium model, and a transaction fee model.

Let’s discuss all these fintech monetization models below:

1] Subscription Model

The subscription model is a cross-border payment model that helps users and businesses to pay a recurring monthly and annual fee for accessing international transfers and premium financial tools.

Here you will charge the users a recurring fee to access premium features, usually bundled with reduced transfer costs.

2] Usage-Based Models

A usage-based model in a cross-border payment app works by offering a certain number of free requests to the users per month, and then charging the users for further requests.

Here you can consider an example of Google Maps, which offers 28000 requests for free, and the platform charges a suitable amount. This model charges based on the resources used and the API calls that are made.

3] Hybrid Model

Under the hybrid model, you offer a combination of monetization strategies to your customers. Here, you can allow users a subscription policy along with the limited API calls.

When you create a cross-border payment app, you can include the two models as a subscription plan model and a usage-based model.

4] Freemium Model

The freemium model for the cross-border payment app does offer a basic version for free. It lowers the entry barriers to build mass adoption, then uses “upgrade triggers” like usage caps or locked capabilities.

For instance, you can offer the users some free transactions, and then opt for usage caps or locked capabilities.

5] Transaction Fee Model

A cross-border transaction fee model is simple; it charges the customers per transaction through the API. This is a standard model in the fintech APIs.

This model charges for moving money across the digital and geographical borders, and is highly variable depending on facilitating the merchant checkouts, and peer-to-peer remittances.

Well, if you are ready to go ahead with the cross-border payment app development process, then connecting with the right app developers can help.

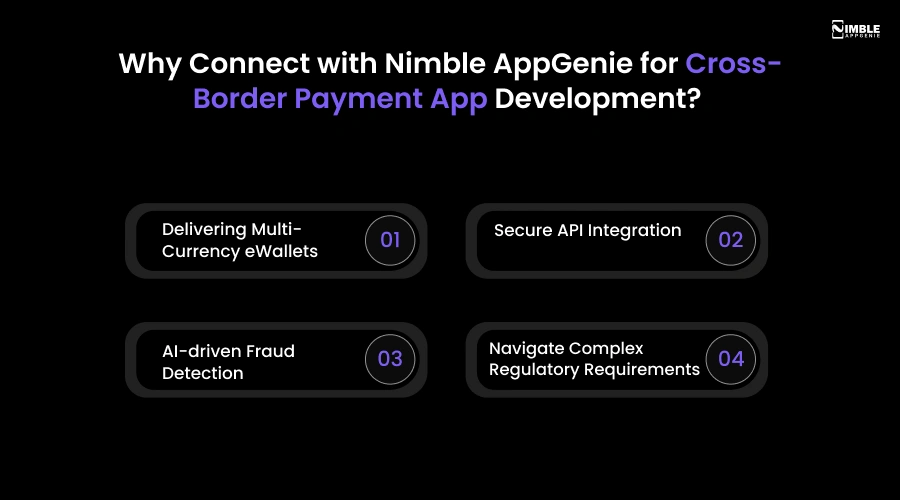

Why Connect with Nimble AppGenie for Cross-Border Payment App Development?

Nimble AppGenie is the top fintech app development company, offering cross-border app development solutions tailored to the customized needs and requirements of businesses and users.

As the leading fintech software development company, offering custom solutions for eWallets, lending, and even digital banking. Whether you are looking for cross-border payment app development or any other fintech services, connecting with us can help you in:

1. Delivering Multi-Currency eWallets

Our company offers multi-currency eWallets development services, where we offer our clients cut down on high foreign transaction fees and tedious international banking processes.

2. Secure API Integration

Nimble AppGenie offers a secure API integration through deploying an advanced, multilayered, robust security strategy featuring OAuth 2.0 authentication and rigorous input sanitation.

3. AI-driven Fraud Detection

Our company does offer an AI-driven fraud detection to users and businesses by offering them AI integration services in their core foundational app.

4. Navigate Complex Regulatory Requirements

The team knows well how to navigate the complex regulatory requirements by integrating the regulatory-grade architecture as well as automation directly into the app development process.

Conclusion

The cross-border payment app development is the process that begins with market research, selecting the right features, designing the app, integrating the right framework, selecting the tech stack, testing, and launching the app.

A cross-border payment app allows users and businesses to receive, send, and hold multiple currencies across different countries. The working process begins with initiation, currency conversion, immediate processing, compliance checks, settlements, and confirmation.

Here, the money-making strategies that are included in the cross-border payment app development are subscription model, hybrid model, usage-based models, freemium, and transaction-fee model.

FAQs

A cross-border payment app enables users to send and receive money across different countries and currencies, unlike a regular payment app that typically processes transactions within a single country or currency.

The cost to develop a cross-border payment app is $15,000 to $100,000+, depending on the diversified factors such as the complexity of the features, design of the app, selection of tech stack, and the team of developers.

It might take 3 months to 12 months to develop a cross-border payment app, depending on the complexity of its features, compliance scope, and the number of corridors supported.

The key tech stack that is best for building a scalable cross-border payment app is Flutter, react native, and cloud infrastructure such as AWS, Google Cloud, and Microsoft Azure. Other than this , there are databases and APIs as per the requirements of your app.

Essential measures include end-to-end encryption, tokenization, multi-factor authentication, and real-time AI-based fraud and sanctions monitoring.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.