Banking Software Development

Banking Software Development Payroll Software Development

Payroll Software Development Our Work Process

Our Work Process Awards

Awards

Key Takeaways:

- A real AI due diligence platform is a data layer, a risk-scoring layer, and an audit-trail layer, working together.

- Standard KYC/AML and GRC software works fine for routine checks, but most fintechs outgrow it once their risk rules get specific or they operate across more than one country.

- The EU AI Act and similar rules treat risk-scoring AI as high-risk, so documented, auditable decision logic isn’t optional.

- The cost to develop an AI due diligence platform can range between $40,000-$250,000 and varies a lot by compliance scope.

- One use case, then the risk engine, then integrations, then compliance hardening. This costs less and carries less regulatory risk than a single big launch.

- The strongest setups use AI for volume and pattern-spotting, with a person making the final call on anything flagged or low-confidence.

- Nimble AppGenie builds compliance-first AI due diligence and risk-assessment platforms for fintechs, banks, and insurers, from the first architecture decision through launch and support.:

How do you develop an AI due diligence platform? You connect your data sources, train AI models to score risk, add a layer that explains every decision, and build a compliance workflow around the output. Most teams start with one use case like KYC or AML, then expand from there.

If you are a fintech founder, CTO, or COO, you already know why this matters. Your compliance team is drowning in alerts that turn out to be nothing; industry data puts AML false-positive rates between 90% and 95%.

Your compliance team is drowning in alerts that turn out to be nothing, for a full breakdown of how to scope and cost an AML transaction monitoring system that actually brings that rate down, see our dedicated guide.

Also, manual due diligence was never built to handle that kind of volume. It cannot scale; it leaves gaps that regulators now expect you to close, and it produces decisions no one can explain or audit.

That is exactly the problem an AI due diligence platform is built to solve. It replaces the manual layer with a system that pulls in financial, legal, and compliance data, scores risk automatically, and logs how it reached every decision, so your team stops chasing noise and starts acting on real signals.

This guide covers how to develop an AI due diligence platform, key features, the real challenges and their solutions, what it costs, and what regulations you need to build around from day one.

What is an AI Due Diligence Platform?

AI due diligence platform is software that uses ML to pull in financial, legal, and compliance data, score risk automatically, and record how it reached each decision. It replaces manual checklists and spreadsheet reviews with a system that works faster and leaves documentation that regulators can check.

It is different from three things people often mix it up with:

- A traditional due diligence checklist is just a list that a person works through by hand.

- Generic GRC software tracks policies and tasks but does not score risk on its own.

- A single KYC or AML tool checks one thing, identity or a sanctions list, but does not tie that check to a wider risk picture.

An AI due diligence tool for investor risk scoring does all three tasks at once, pulls the data in, scores the risk, and documents the decision.

Why Do Fintech Companies Need to Develop an AI Due Diligence Platform Now?

Fintech companies need an AI due diligence platform to evaluate AI systems for risk, compliance, security, fairness, and reliability before they are deployed. The regulators now expect AI-driven decisions to be explainable. A score without a documented reason is not acceptable anymore.

- Regulators are paying closer attention to AI-driven decisions, from the EU AI Act to FCA guidance.

- AML and KYC alert volumes are increasing faster than compliance teams can scale.

- Investors now expect a documented, automated risk-assessment process, not a spreadsheet, during fundraising due diligence.

- Off-the-shelf KYC/AML tools work fine for standard checks, but they hit a ceiling once your risk rules get specific.

If you are thinking about the compliance stack, our guide on fintech regulations and digital payments compliance covers the regulatory landscape across the US, UK, UAE, and the EU.

Build vs. Buy: When Should You Actually Build a Custom Platform?

You should buy if your checks are standard and your volume is predictable. However, you can build if your risk logic is specific, you operate across more than one jurisdiction, or the platform itself needs to give you a long-term advantage with regulators or investors.

The table below showcases the comparison between building a custom AI risk management platform or buying an off-the-shelf tool.

| Buy an off-the-shelf tool when | Build a custom platform when |

| Your checks follow standard rules (basic KYC/AML) | Your risk logic is specific to your business |

| You operate in a single jurisdiction | You operate across multiple jurisdictions |

| Your volume is low or steady | Your volume is growing fast or unpredictable |

| You need something running this quarter | You want the platform itself to be a long-term advantage |

Core Features of AI Due Diligence Platform Development

The core features of an AI due diligence platform are data ingestion & aggregation, risk-scoring ML models, KYC/KYB & AML screening, document intelligence, explainability (XAI) layer, compliance & audit-trail engine, and so on. Every feature below serves a distinct task.

If you miss any fintech features, then it creates a gap that regulators or auditors will find.

| Feature | What It Does | Why It Matters |

| Data ingestion & aggregation | It pulls data from internal systems, public records, and third-party sources into one place. | Without clean, complete data, every other layer is guessing. |

| Risk-scoring ML models | It scores each entity or transaction against your risk criteria. | This is the core engine that replaces manual scoring. |

| KYC/KYB & AML screening | It checks identity, ownership, and sanctions or watchlist status. | Required by regulators in nearly every jurisdiction. |

| Document intelligence (OCR + NLP) | It reads and pulls data from contracts, filings, and ID documents. | It cuts manual document review time by a wide margin. |

| Explainability (XAI) layer | It shows why a model gave a specific score. | Regulators expect this; without it, you cannot defend a decision. |

| Compliance & audit-trail engine | Logs every decision, input, and override with a timestamp | This is what you hand a regulator or auditor |

| Case management/workflow | It routes flagged cases to the right reviewer | Keeps human review organized instead of stuck in email threads |

| Reporting & dashboards | It summarizes risk trends and compliance status for leadership | Turns raw scoring data into something a COO can act on |

If you are building a broader AI stack, read the guide on AI in fintech that covers how AI layers work across the full product.

What Advanced Features Make an AI Due Diligence Platform Stronger?

The features that make an AI due diligence platform stronger are real-time monitoring, agentic AI investigation workflows, multi-jurisdictional, bias, and fairness monitoring, core banking integrations, and predictive analysis.

When you develop an AI due diligence platform, it is vital to add these features to it.

| Advanced Feature | Description |

| Real-time continuous monitoring | Flags a risk change as it happens, not at the next scheduled review |

| Agentic AI investigation workflows | Drafts a first version of a suspicious-activity report for a human to review and file |

| Multi-jurisdiction regulatory mapping | Applies the right rule set automatically based on where the entity operates |

| Bias & fairness monitoring | Flags whether the model scores certain groups unfairly, before a regulator does |

| Core-banking / CRM / VDR integrations | Connects to systems already in use instead of running as a separate silo |

| Predictive risk analytics | Flags entities likely to become high-risk before they cross the threshold |

If your AI compliance platform for fintech also needs to automate investigation workflows, read the blog on agentic AI in financial services that explains how AI agents handle KYC, AML, and EDD flows end to end.

How to Develop an AI Due Diligence Platform for Risk Assessment and Compliance?

To develop an AI due diligence platform for risk assessment and compliance, you have to follow a proper roadmap.

Each stage below has a defined scope, a concrete output, and a clear reason for the sequence. Let’s take a look at the development process.

1. Define Scope and Regulatory Footprint

Firstly, start by deciding which checks you are automating first, like KYC, AML, fraud screening, or ESG risk. Choose the jurisdictions you need to comply with from day one, since adding a new country’s rules later means rebuilding parts of your compliance logic.

It is advisable to start with the single use case that causes the most manual work today. Whether that is onboarding delays or an alert backlog, since that’s where a focused MVP proves value fastest.

2. Design Your Architecture

A microservices fintech architecture is the standard choice. It allows you to update the AI scoring layer later without touching the rest of the system.

This matters more than it sounds. When regulations change, or you need a better model, you update that one service instead of touching the whole system.

A monolithic build ships faster at first, but it gets expensive to change later, and compliance requirements change often enough that this cost shows up within the first year.

3. Choose Your Tech Stack

Tech stack decisions made here are expensive to reverse, so base them on your dedicated development team’s existing skills and the compliance requirements of your target markets.

Most teams pair a React frontend with a Python or Node.js backend, an LLM provider for document intelligence, a vector database for search and matching, and a relational database for records and audit logs.

Cloud infrastructure choice should be driven by your data residency requirements, not just cost. You should lock in identity verification APIs, sanctions data feeds, and audit logging controls as part of the tech stack.

4. Build the Data Pipeline

Connect internal databases, public records sources, and third-party APIs into a single clean data feed your models can read. This stage takes longer than most teams expect because source data is rarely in a consistent format.

Build validation gates that flag missing or malformed records before they reach the model. Data quality at this stage directly determines model quality downstream. If your source data is incomplete or inconsistently structured, your risk scores will reflect that.

5. Train Your Risk-Scoring Models

Start with one narrow use case and a clean, labeled dataset, rather than modeling every risk type in the first release. A narrow scope allows you to validate the model’s accuracy against known outcomes before you trust it with real cases.

Most teams underestimate how much labeled data they need and end up retraining earlier than planned. If you do not have enough historical data to train confidently, start with a simpler, rules-based model and layer ML once you have more to learn from.

6. Build Explainability and Audit Logging

Build both of these from day one, not after the model is deployed. The XAI layer should produce a human-readable explanation for every risk score. The audit log should capture every input, every score, every human override, and every system action with a timestamp and a user ID.

These are not PCI compliance decorations. They are the foundation of your regulatory defence. Under the EU AI Act and FCA guidance, you need to reproduce and explain any decision the system has ever made. If you cannot do that at launch, regulators will expect it before you can scale.

7. Design Role-Based Interfaces

Analysts, auditors, compliance officers, and system admins all need different views of the same underlying data. Analysts need a case queue with contextual data and AI explanations. Auditors need an immutable log view.

Admins need configuration controls for scoring thresholds and workflow routing. Creating a single interface that tries to serve all four groups usually serves none of them well.

This is also where your fintech’s broader approach to fintech security matters: RBAC, session management, and access logging belong here.

8. Test Before You Trust

Run three types of testing before any model touches a real case. Accuracy benchmarking confirms the model performs at the level you designed for. Adversarial testing checks whether the model can be gamed by edge-case inputs.

Bias testing checks whether the model scores certain demographic or geographic segments unfairly. All three should run against data that was not used in training.

Document every test and its results, because regulators will eventually ask to see this evidence, not just hear that testing happened. Teams that skip this step tend to find their bias problems after a regulator does.

9. Deploy With Human-in-the-Loop Oversight

Do not deploy fully autonomous decisions on high-stakes cases. Design a tiered system: low-risk decisions pass automatically, medium-risk decisions trigger a reviewer notification, and high-risk or low-confidence decisions require human sign-off before action is taken.

You can build the case management interface so reviewers can see the AI’s reasoning alongside the decision. This makes review faster, and the override log more useful.

10. Monitor, Maintain, and Retrain

Lastly, set a quarterly retraining schedule from the start, not as a future task. Build model drift detection into your monitoring stack so performance degradation triggers an alert before it affects real decisions.

Track false-positive and false-negative rates over time and use them to drive retraining priorities. Model maintenance is not an optional line in your post-launch budget; it is a regulatory obligation.

What Tech Stack Is Required for AI Due Diligence Platform Development?

What is the best tech stack to build an AI due diligence platform?

The best fintech tech stack for AI due diligence platform development includes a frontend, backend, AI/LLM layer, database, cloud infrastructure, and identity compliance tooling. These technologies help you build an AI risk assessment platform for fintech startups. Take a look:

| Layer | What to Use |

| Frontend | React, or a similar framework, built around separate analyst, auditor, and admin views |

| Backend | Node.js or Python, depending on your team’s existing stack |

| AI / LLM layer | An LLM provider plus a vector database for document search and matching |

| Database | A relational database, such as PostgreSQL, for structured records and audit logs |

| Cloud infrastructure | AWS, Azure, or GCP, chosen based on your existing setup and data residency needs |

| Identity & compliance tooling | Identity verification APIs, sanctions and watchlist data feeds, and access controls for audit logging |

Regulatory & Compliance Mapping You Need to Build Around

The main regulatory and compliance to think about are the EU AI Act, ISO, BSA, FCA, and GDPR compliance. You should plan for compliance requirements from the beginning.

If you add them later, it can increase costs, create delays, and require extra development work. The table below shows the vital fintech compliance requirements for AI due diligence.

| Regulation / Framework | What It Requires | What It Means for Your Platform |

| EU AI Act | Classifies AI used for risk-scoring as high-risk | Documented decision logic, human oversight, and a risk assessment before deployment |

| GDPR | Lawful basis for processing personal data + right to explanation for automated decisions | Your XAI layer must satisfy data-subject rights, not just regulators |

| NIST AI RMF / ISO 42001 | Voluntary frameworks for AI risk governance | Following these demonstrates good-faith compliance where the law is still unclear |

| US: BSA/AML, FCRA | Ongoing monitoring, SAR reporting, fair use of data in risk decisions | Audit trail and bias checks must map directly to these requirements |

| UK: FCA | Explain and govern any AI used in regulated decisions | Similar explainability bar to the EU AI Act, enforced through FCA supervision |

How Much Does It Cost to Develop an AI Due Diligence Platform?

The cost to develop an AI due diligence platform ranges between $40,000-$250,000, depending on the platform’s complexity, compliance requirements, AI features, integrations, and customization needs.

A basic platform with limited features costs less, while an enterprise solution with advanced compliance and monitoring features requires a larger investment. You can reduce the costs by choosing fintech development outsourcing instead of building an in-house team.

Here is the table of the cost to build an AI due diligence platform showing the breakdown based on complexity.

| Tier | Cost Estimation | What’s Included |

| MVP version | $40,000-$80,000 | One use case, a core risk-scoring model, and basic audit logging |

| Mid-tier platform | $80,000-$180,000 | Various use cases, multiple integrations, and stronger explainability tooling |

| Enterprise platform | $180,000-$250,000 | Multi-jurisdiction compliance, a full integration suite, and dedicated monitoring and retraining. |

These figures are only rough estimates.

Compliance requirements have a bigger impact on development costs than the AI technology itself. A simple model with complex multi-jurisdiction compliance work usually costs more than a complex model with light compliance requirements.

Investing in the right AI due diligence platform from the start is often more cost-effective than the cost of retrofitting compliance after a regulatory review or audit.

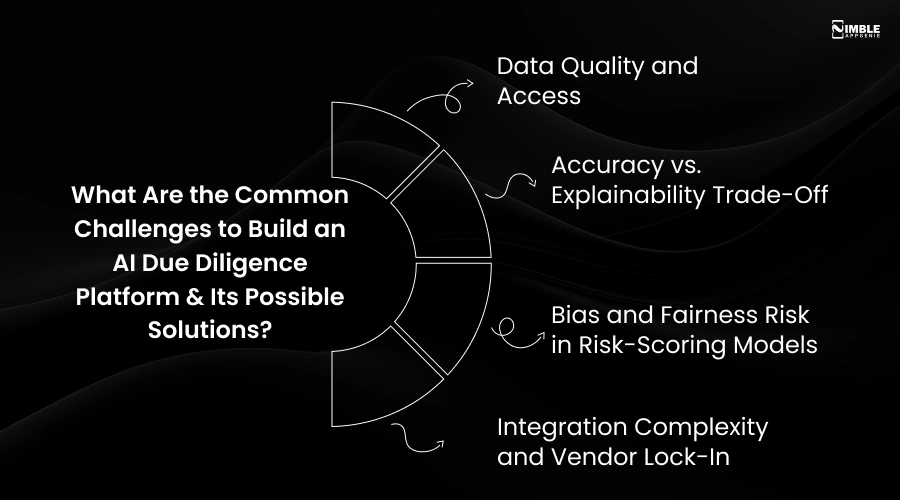

What Are the Common Challenges to Build an AI Due Diligence Platform & Its Possible Solutions?

The challenges to develop an AI due diligence platform are data, compliance, system integration, model accuracy, and changing regulations. Identifying these challenges early and finding the right solutions can help create a secure, reliable, and efficient platform.

Let’s check out the challenges and their possible solutions.

1. Data Quality and Access

Risk scores are only as good as the data behind them. Most fintech companies store data across multiple systems, including banking platforms, CRMs, API integration, and spreadsheets. Missing fields, inconsistent formats, and siloed databases can make it difficult to build accurate AI models.

The Solution:

You should run a data audit before any model development begins. Map every source, document what is missing, and build a data pipeline with validation gates. For identity and sanctions data, use established third-party feeds rather than building your own.

2. Accuracy vs. Explainability Trade-Off

Regulators under the EU AI Act and FCA rules increasingly require that AI-driven risk decisions come with a clear, documented reason. A black-box model that scores entities with 98% accuracy is not acceptable if you cannot explain to a regulator or data subject why a decision was made.

The Solution:

Define your explainability requirements before selecting a model. Tools like SHAP and LIME can help explain decisions without sacrificing performance. This is vital for AI fraud detection in fintech, where decision transparency is becoming a key compliance need.

3. Bias and Fairness Risk in Risk-Scoring Models

AI models trained on historical data can unintentionally learn existing biases. This can lead to unfair outcomes for certain customer groups and create both regulatory and reputational risks.

The Solution:

Test models for fairness before launch and continue monitoring them after deployment. When bias is detected, the issue is often related to the training data rather than the model itself. This is particularly important for KYC in fintech apps, where fair and consistent customer verification is essential.

4. Integration Complexity and Vendor Lock-In

Most fintech platforms already have a core banking system, a CRM, and at least one KYC/AML API. Getting a new AI platform to talk to all of these is harder than it looks.

The Solution:

Design your integrations around open fintech APIs and standard data formats from day one. Before committing to any vendor, verify that you can export your data and migrate away. Build an API abstraction layer so your application talks to a standard interface, not directly to a vendor’s proprietary API.

How Nimble AppGenie Can Help You Build an AI Due Diligence Platform?

Nimble AppGenie is a trusted fintech software development company that builds AI due diligence and risk-assessment platforms for fintechs, banks, and insurers.

We manage KYC and AML automation, risk-scoring, compliance reporting, and case management. The work usually covers:

- KYC and AML automation built around the onboarding flow you already have

- Risk-scoring models with explainable, audit-ready logic from day one, not bolted on later

- Compliance reporting and audit trails mapped to RBI, SEC, FCA, and EU AI Act requirements

- Workflow and case management tools built for compliance teams, not adapted from a generic project tool

- End-to-end development: architecture, data pipeline, AI models, QA, deployment, and support after launch

We have done this before. For SWAP Africa, a multi-currency wallet app, we built both individual and business KYC verification from scratch, in markets with no existing card networks or agent banking APIs.

Every user passes identity checks before they can transact, and businesses go through extra verification before sending bulk payroll payments. The app launched with over 3,000 users already on the waitlist.

It was built to work on affordable Android phones and slow 3G connections, not just ideal conditions. That is the same standard we bring to AI due diligence development. The real compliance logic is tested for the conditions you actually operate in, not a demo environment.

Conclusion

If you are deciding whether to develop an AI due diligence platform or buy one, it usually comes down to two things: your risk requirements and how much control you need over compliance.

For basic checks and lower volumes, buying a ready-made solution is often the better option. If you need custom risk rules or operate in multiple countries, building your own platform gives you more flexibility and control.

Whatever option you choose, make sure the platform can explain its decisions. AI should support decision-making, not replace it. For high-risk cases, a person should always review the final decision.

Thus, if you need help evaluating, planning, or building an AI due diligence platform, an AI development company can help design a solution that fits your business and regulatory needs.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.