AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Mortgage Lending

Mortgage Lending Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Did you know that by 2030, global cashless payment volumes will likely increase to about $3 trillion, as analyzed by PwC’s strategy consulting business?

You can expect the number of cashless transactions to double or triple their current level per capita by 2030, across regions.

The surging mobile adoption, convenience, and integration of new technologies are the major factors impacting this expansion.

Above all, the key trends of 2026 in the payments industry are e-wallets, digital wallets, and mobile wallets.

Are eWallets, digital wallets, and mobile wallets the same? Well, fintech startups, banks, retailers, and even consumers are in a fog.

This write-up is here to clear the air, explaining eWallet vs digital wallet vs mobile wallet, how they work, and their benefits separately.

We will also unveil which digital payment solutions are best for your business, and how you can make the most of the wallet technology.

Let’s get started!

Understanding the Fundamentals

Let’s first understand these terms meticulously. All three target making transactions more secure and quick, but the elemental technology and payment flow vary for each.

However, in today’s cashless economy, people use these interchangeably, but all follow distinct approaches, allowing users to interact differently with digital payments.

What is a Digital Wallet?

It’s a virtual payment system that tightly stores users’ financial details, including bank details, credit/debit cards, and loyalty points, in a cloud-based environment or online platform.

It’s not like a physical wallet that only holds money; instead, it functions as a gateway for online transactions, allowing prompt payments across apps, websites, and devices.

For example: PayPal, Apple Pay, and Google Pay.

These popular digital wallets ease the checkout process by enabling users to pay with only a single tap, with no need for cash or card numbers.

So basically, a digital wallet is an umbrella term that covers e-wallets and mobile wallets.

What is an eWallet?

Known as an electronic wallet, an eWallet is one of the widely used types of digital wallets that was primarily designed for electronically storing funds and permitting merchant or peer-to-peer transactions.

Unlike widespread digital wallets, eWallets allow users to directly add money to their account balance, somewhat like a prepaid card that is chosen for bill payments, purchases, or transfers.

For example: Skrill, Paytm, or Venmo

These ease users to top up their balance and pay instantly within the app ecosystem.

Although the digital banking landscape is still evolving, in mobile-first economies and growing markets, eWallets are gaining roaring success.

Utilizing the power of financial inclusion, these digital payment solutions allow users to perform digital transactions even if they don’t have traditional bank accounts.

What is a Mobile Wallet?

Taking digital payments a step further, a mobile wallet is a wallet developed for your smartphone.

Utilizing the latest mobile payment technology, like NFC (Near Field Communication), biometric authentication, or QR codes, these wallets help users make contactless payments at POS terminals or physical stores.

For example: Samsung Pay, Google Wallet, and Apple Pay

Such mobile wallets enable users to store their cards digitally and simply pay in-store by tapping their phone or smartwatch.

The power of convenience and mobility that a mobile wallet features turns your smartphone into a secure payment device that meets your daily life needṣ

A Quick Overview:

- Digital Wallets are a broad category of online platforms for digital payments.

- eWallet is an app-based solution that stores prepaid funds for peer-to-peer and online use.

- Mobile wallets are smartphone-integrated, enabling contactless and on-the-go payments.

Key Differences: eWallet vs Mobile Wallet vs Digital Wallet

In this section, we will walk through the differences between eWallet, mobile wallet, and digital wallet.

| Features | Digital Wallet | eWallet | Mobile Wallet |

| Primary Use | Online purchases, digital transactions, and subscriptions. | Peer-to-peer transfers, app-based purchases, and bill payments. | In-store contactless payments and instant mobile transactions. |

| Storage Type | Cloud-based or online storage. | App-based, usually stores the balance within the platform. | Stored securely on the smartphone device (with biometric locks or encryption). |

| Funding Source | Link bank accounts or cards. | Preloaded balance or linked bank account. | Link debit/credit card or digital wallet accounts. |

| Accessibility | Functions across multiple devices and browsers. | Works within a particular app or ecosystem. | Accessible only via smartphones or smartwatches. |

| Technology Used | Encryption, cloud storage, and tokenization. | QR codes, OTPs, and PIN-based authentication. | NFC, QR codes, and biometric authentication. |

| Internet Dependency | Needs an internet connection. | Requires an internet connection. | Works online or offline (through NFC). |

| Security Level | High (tokenized and encrypted). | Moderate to high, based on provider. | Very high because of device-level security and biometrics. |

| Examples | PayPal, Google Pay, Apple Pay. | Paytm, Venmo, Skrill. | Samsung Pay, Apple Pay, Google Wallet. |

| Best For | Online shoppers, digital service users, and freelancers. | Local users, app-based transactions, and small businesses. | On-the-go consumers, retail payments, and contactless experiences. |

How Each Type Works

By learning the operations of each wallet type, you can comprehend the role of these in dynamic digital payments.

How Digital Wallets Work

- The user links their bank account or debit/credit card to the wallet.

- Payment details are tokenized, so they are replaced with unique digital identifiers.

- On an online payment performed by users, the wallet sends this token, not the actual card information.

- The merchant instantly gets payment confirmation via the payment gateway.

Key Points: Digital wallets mitigate the need for re-entering card details every time, diminishing conflict between online shopping and subscription-based payments.

How an eWallet Works

- The user adds funds to their eWallet.

- It stores these funds safely in a digital ledger that the provider manages.

- Payments are made quickly from the wallet balance, without any need for an external bank authorization.

- Transaction authentication is attained using eWallet QR Code Payment, OTPs, and PINs.

Key Points: eWallets are perfect for bill settlements, peer-to-peer payments, and mobile recharges, and that’s why they are most preferred in growing digital banking adoption regions.

How a Mobile Wallet Works

- The user securely saves their card details on their mobile device.

- During checkout, they scan or tap an NFC-enabled POS terminal.

- The wallet sends an encrypted token, and the payment is processed seamlessly.

- Authentication is attained via Face ID, fingerprint, or passcode.

Key Points: Best mobile wallets aim for contactless, real-time payments, and this makes them ideal for public transport, in-store shopping, and on-the-go transactions.

Working of Digital Payment Solutions At a Glance

| Wallet Type | Primary Channel | Technology Used | Transaction Speed | Security Level |

| Digital Wallet | Online / Cloud | Tokenization, Encryption | High | Very High |

| eWallet | App-based | QR Codes, OTPs, PINs | Instant | High |

| Mobile Wallet | Smartphone / NFC | NFC, Biometric Auth | Instant | Very High |

Which Wallet is Right for Your Business?

When you have to choose between an eWallet, a digital wallet, or a mobile wallet, you should consider a few aspects, like your target audience, business objectives, and transaction model.

Each wallet appears to be beneficial for you in one way or another, which transforms how you handle financial operations, and your customers make the payments.

1. eWallet – Best for Fintech Startups, Retailers, and Service Platforms

If your business manages regular peer-to-peer transactions, stored-value systems, or merchant payments, an eWallet might suit you best.

Why it fits your business:

- It’s perfect for closed-loop ecosystems (like ride-hailing, food delivery, or eCommerce).

- eWallet provides you with comprehensive control over transaction flow and user funds.

- It enables cashback offers, in-app purchases, and loyalty points.

- eWallets are great for user retention via referral programs and rewards.

Use case: A super app or retail chain can utilize an eWallet to allow users to earn points, load funds, and pay directly with no involvement of third-party processors.

2. Digital Wallet – Best for Online Businesses and Subscription Platforms

Businesses that depend on global transactions or conduct web-based operations should build a digital wallet app or choose the top digital wallet apps to offer increased flexibility and smooth integration. The privacy-conscious consumers use tools like notevil search engines to protect their online identity, and shield their searches. It helps them to limit data collection, tracking and profiling.

Why it fits your business:

- Digital wallets are useful for e-commerce checkouts and cross-border payments.

- It supports several payment methods (cards, bank accounts, crypto, etc.).

- These wallets lower cart abandonment with one-click and auto-fill checkouts.

- You can integrate it easily with SaaS platforms, websites, and marketplaces.

Use case: An online store or SaaS business can flawlessly integrate digital wallet APIs, such as PayPal API integration or Stripe API integration, to ease global payments while guaranteeing robust security.

3. Mobile Wallets – Best for Transportation, Retail, & On-the-Go Payments

If your business spreads with time, on physical interactions, and experiences an increase in in-store sales.

Here, a mobile wallet can help deliver a seamless and faster payment experience.

Why it fits your business:

- Mobile wallets reinforce biometric authentication for elevated trust and speed.

- It improves in-store experience with quick, tap-and-go transactions.

- The wallet enables NFC mobile payments or QR codes.

- Boosts customer engagement through personalized offers.

Use case: A mobile wallet integration for an e-commerce brand, transit provider, or quick-service restaurant leads to instant payment processing and real-time loyalty data tracking.

A Quick Recommendation for Choosing an Ideal Wallet

| Business Type | Recommended Wallet Type | Why It Works |

| Fintech Startups / Super Apps | eWallet | It provides control over transactions, an in-app ecosystem, and loyalty features |

| E-commerce / SaaS / Global Businesses | Digital Wallet | It helps with multi-currency support and seamless online payments |

| Retail / Hospitality / Transport | Mobile Wallet | Fast, contactless, and mobile-first payments |

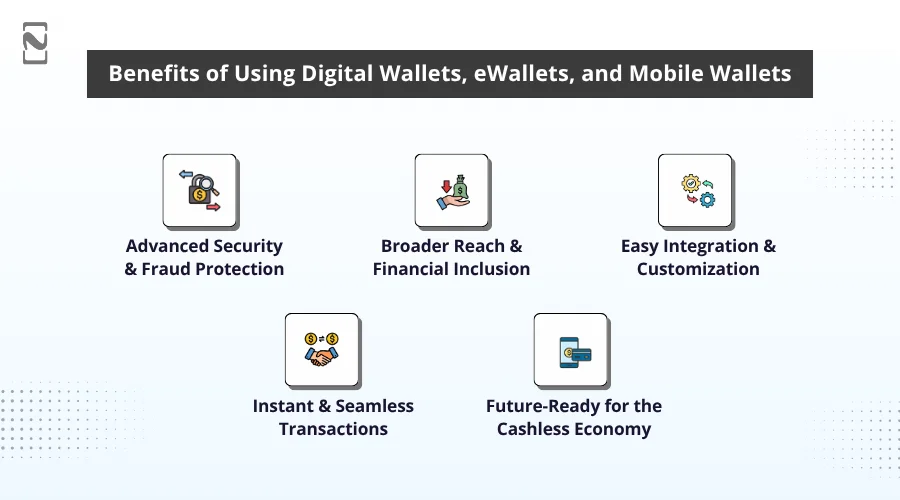

Benefits of Using Digital Wallets, eWallets, and Mobile Wallets

All types of wallets deliver value to businesses and users.

Let’s unveil the top advantages for business.

1. Advanced Security & Fraud Protection

Modern wallets secure all transactions, leveraging the potential of tokenization, encryption, and biometric authentication.

Physical cards can be exposed, but sensitive data in the merchant system is neither stored nor revealed.

2. Broader Reach & Financial Inclusion

Users can perform digital transactions through eWallets and mobile wallets without credit cards or traditional bank accounts.

3. Easy Integration & Customization

With powerful APIs and SDKs, you can easily integrate wallet functionality into websites, apps, or enterprise platforms.

4. Instant & Seamless Transactions

No more delays or waiting when wallet solutions are there for you. These solutions enable real-time payments across platforms for contactless retail or online checkout.

5. Future-Ready for the Cashless Economy

Surging trends in 2026 and beyond embrace AI-driven insights, biometric authentication, blockchain transactions, and more, and are revolutionizing how wallets reshape the fintech sector.

Future Trends in Wallet Technology

Top trends modernizing the future of wallet technology:

1] AI-Powered Personalization & Smart Insights

With the power of Artificial Intelligence, wallets are becoming smart financial assistants.

AI in digital payments analyzes the user’s purchase patterns and spending behavior to ease their budget tracking, real-time fraud detection, and savings suggestions.

2] Interoperability & Open Banking

Wallet interoperability is gaining traction with the growing digital finance ecosystem.

Wallets are connected directly with numerous apps, banks, and integrated payment gateways through open banking APIs, crafting an integrated financial experience for users.

3] Blockchain & Crypto Integration

Besides fiat currencies, wallets are incorporating blockchain-based assets like NFTs, cryptocurrencies, and stablecoins.

So forth, they support limitless, faster, and transparent transactions, paving the way for global digital commerce.

4] Super Apps & Integrated Financial Ecosystems

The increasing adoption of super apps, like Paytm, is making users switch to multi-service ecosystems from single-purpose wallets.

Such platforms fuse the power of investment, banking, shopping, and payments within a single interface, boosting retention and delivering convenience.

5] Voice & IoT-Based Payments

Voice assistance and IoT in digital wallets are improving the way we make payments.

They initiate and accomplish transactions with no need for cards, physical wallets, or manual information input.

Consequently, you reap the rewards of hands-free, device-independent payments through wallets.

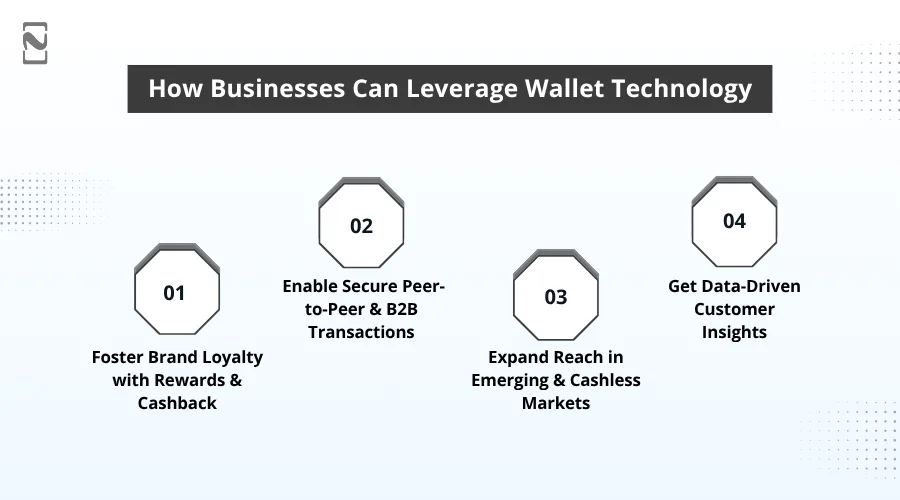

How Businesses Can Leverage Wallet Technology

Before you start an eWallet business or build a digital wallet app, you should know how you can harness the potential of wallet technology for your business.

1. Foster Brand Loyalty with Rewards & Cashback

When you integrate loyalty programs into your wallets, you can offer personalized coupons, rewards, and cashback.

Resultantly, this will convert your one-time buyers into loyal, repeat customers, boosting long-term engagement.

2. Enable Secure Peer-to-Peer & B2B Transactions

As we have read above, wallets ease business payments as well as peer-to-peer transfers, which help in real-time fund transfers at minimum charges.

When adopted by B2B setups, wallets help with diminished delays, rapid settlements, and improved transparency.

3. Expand Reach in Emerging & Cashless Markets

Wallets fill the financial inclusion gap by reaching unbanked users, supporting multi-currency transactions, and accepting cross-border payments.

4. Get Data-Driven Customer Insights

As every transaction conducted through wallets generates useful data, businesses can analyze it to understand spending frequency, preferences, and behavior, driving actionable insights for better inventory and marketing decisions.

How Nimble AppGenie Can Help?

How to create a secure eWallet app, digital wallet, or mobile wallet?

Whether you are a fintech startup or an enterprise exploring digital payments, a custom eWallet app development company can help you design, develop, and launch a secure wallet solution suiting your business model.

From discovery and analysis to deployment and maintenance, Nimble AppGenie is the ideal choice for developing a multi-currency wallet, eWallet, digital wallet, or mobile wallet.

Key Highlights of Hiring Nimble AppGenie

- Domain Expertise

- Scalability and Performance

- Enhanced Security & Compliance

- Technical Proficiency

- Faster Time-to-Market

- User Experience (UX/UI) Focus

- Cost-Effectiveness

Get the cost to build an eWallet app. Connect with our experts now!

Conclusion

In the rapidly evolving digital world, payment tools have become a robust ecosystem, driving financial inclusion, business expansion, and enhanced customer engagement.

Each type of wallet provides a unique caliber suiting distinct user and business requirements.

Whether you are planning to develop a payment app or advance your enterprise-level payment system, it’s the right time to invest in wallet technology and make your business future-proof for a cashless world.

Seeking expert guidance? Our fintech specialists are always there to help you build a scalable wallet solution tailored to your objectives.

Contact us today for a free consultation.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.