AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

TL;DR

- Debt collection software development automates outreach, payment tracking, and compliance across the whole recovery lifecycle, from first notice to final payoff.

- AI features like predictive recovery scoring, smart segmentation, and automated negotiation can lift recovery rates while cutting manual collector workload.

- Regulation F, the FDCPA, TCPA, and FCRA all apply, and the CFPB has been clear: using AI does not excuse non-compliance.

- Development cost typically runs from around $30,000 for an MVP to $250,000+ for an enterprise-grade, multi-state compliant platform.

- Nimble AppGenie builds compliance-first, AI-powered debt collection software for lenders, collection agencies, and fintechs, from MVP to full-scale deployment.

- Whether you should build or buy depends on your portfolio size, compliance complexity, and how much your collection strategy needs to stand apart from off-the-shelf tools.

Debt collection software development is silently becoming one of the highest-ROI builds in fintech right now. If you are a collections agency, lender, or fintech founder deciding whether to build your own platform in 2026, this guide walks through the AI features worth building, what it actually costs, and the compliance rules you can’t afford to get wrong before writing even a single line of code.

Debt recovery has always been a volume business, but the rules around it have gotten sharper. The CFPB recorded over 207,800 debt collection complaints in its 2025 annual report, and FDCPA-relevant court filings are up roughly 36% annually. At the same time, various states are stepping up their enforcement as federal oversight changes.

For any business running collections at scale, doing it on spreadsheets and manual call lists is no longer just inefficient; it’s a real legal exposure. That is the business case for building purpose-built debt collection software, and it is why more lending platforms are treating it as core infrastructure rather than a nice-to-have.

What Is Debt Collection Software?

Debt collection software is a system that manages the entire process of recovering unpaid balances: tracking what is owed, automating outreach across texts, calls, and email, logging every interaction for compliance purposes, and offering borrowers a way to negotiate or pay on their own terms.

It sits downstream of loan origination and servicing in the loan lifecycle. For a closer look at the servicing stage specifically, see our loan servicing software guide. Modern debt collection solutions go further than reminder systems.

The better ones use AI to decide who to contact, when, through which channel, and with what message, while keeping every action inside legal bounds automatically. Whether you are a first-party lender or a third-party debt collection agency software provider, the core requirements are the same: an efficient debt collection software solution needs to balance recovery performance against strict regulatory guardrails.

Why Are Lenders Investing in AI Debt Collection Software in 2026?

Three things are converging at once, showcasing it’s the best time for debt collection automated software development:

- First, recovery margins are getting squeezed as delinquency volumes grow in a tighter economy.

- Second, compliance has become challenging to manage manually, with federal rules layered under an increasingly active patchwork of state laws.

- Third, AI has matured enough to improve recovery outcomes, not only to automate emails.

| The shift toward digital debt collection is also a market-scale story, not just a compliance one: analysts expect the debt collection software market to grow from roughly $3.34 billion in 2024 to $15.9 billion by 2034. |

Businesses that get this right are recovering more, spending less on headcount, and staying defensible if a regulator comes asking for documentation.

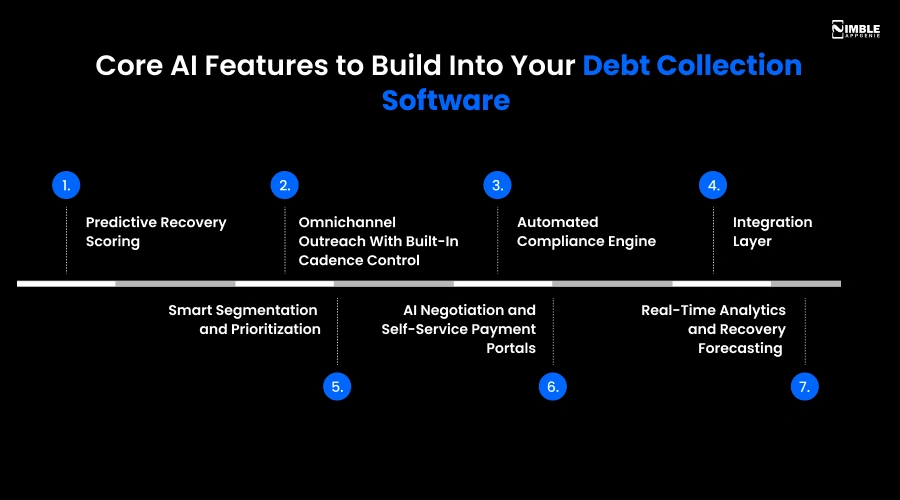

Core AI Features to Build Into Your Debt Collection Software

Let’s go through essential debt collection software features to consider while you build software for your collection business.

1. Predictive Recovery Scoring

Instead of treating each past-due account the same way, an AI model scores every account by likelihood to pay, recommended channels, and ideal contact time. This is the same predictive modeling approach we cover in the guide to predictive analytics in finance, applied particularly to recovery.

2. Omnichannel Outreach With Built-In Cadence Control

Calls, emails, texts, and letters, coordinated from one system, with tough limits baked in so no account gets contacted more than Regulation F allows. This is where automation earns its keep; a rule engine that will not let a call go out if the account has already hit its weekly limit.

3. Automated Compliance Engine

This is the feature that actually safeguards the business: automatic validation notice generation within the five-day window, consent logging for TCPA, opt-out handling per channel, and a full audit trail timestamped down to the individual message.

4. Integration Layer

Debt collection software for banks rarely stands alone. It needs to talk to your core banking or loan servicing system, payment gateway for real-time settlement, and credit bureau for FCRA-related reporting. If you are also building or connecting fraud checks into this stack, our guide on AI fraud detection in fintech is a useful companion read.

5. Smart Segmentation and Prioritization

Not every delinquent account needs the same urgency. Segmentation groups accounts by risk, behavior pattern, and balance size. So your team (or your AI agent) spends effort where it actually moves the needle.

This is also where your debt collection strategies get sharper: early-stage accounts might only need a friendly reminder, while chronic late-payers need a firmer, structured approach.

6. AI Negotiation and Self-Service Payment Portals

Conversational AI can handle routine negotiation, offer payment plans within pre-approved parameters, and let borrowers self-serve without ever talking to a human. We go deeper on this pattern in our piece on AI chatbots in fintech.

7. Real-Time Analytics and Recovery Forecasting

A dashboard that shows recovery rate by channel performance, segment, and forecasted cash flow, so leadership can see what is working without waiting on a monthly report.

What Compliance Rules Apply to Debt Collection Software?

Most debt collection platform development teams underestimate this part, which determines whether your software is an asset or a liability.

1] The FDCPA and Regulation F

The Fair Debt Collection Practices Act (FDCPA) is the federal foundation, and Regulation F, in effect since November 2021, is the CFPB’s rule that translates it into concrete operational limits. The two rules your software must enforce absolutely:

- The 7-in-7 Rule: More than seven calls about the same debt within seven days is presumed harassment, whether or not it was intentional.

- The File-day Validation Notice: Collectors should send a written or electronic notice within five days of first contact, stating the amount owed, the creditor’s name, and the consumer’s right to dispute the debt.

Regulation F also formally permits email, social media messaging, and text, but every digital message needs a clear opt-out mechanism, and voicemails can’t disclose debt details to anyone but the borrower.

2] FCRA: Data Accuracy and Disputes

The Fair Credit Reporting Act governs how you manage disputes when a borrower challenges the accuracy of a reported debt. Inaccurate balances or slow dispute handling create direct regulatory exposure, so your software needs a clean, timestamped dispute workflow.

3] TCPA: Consent for Automated Communication

The Telephone Consumer Protection Act needs prior express written consent before sending automated texts or making autodialed calls.

Consent has to be captured separately from other terms and should be easy to revoke. TCPA violations tend to create the largest financial exposure of any collections-relevant rule, since penalties stack per call or message.

4] UDAAP and the 2026 Enforcement Shift

Beyond the checklist rules, the CFPB also evaluates conduct under UDAAP (unfair, deceptive, or abusive acts and practices) – a framework based on individual steps. A workflow can technically follow Regulations F and still create UDAAP exposure if the cumulative experience feels deceptive.

Worth noting heading into the rest of 2026: the CFPB has scaled back its supervisory activity, and state attorneys general have stepped in to fill the gap, specifically in states like New York, California, and Florida. California’s Rosenthal Act, for instance, now extends FDCPA-style protections to some commercial debts as well, not only consumer debts.

That is a meaningful distinction if your business touches commercial debt collection alongside consumer accounts, since B2B debt has historically sat outside FDCPA entirely and is only now picking up state-level protections in places like California.

If you operate across various states, your compliance engine must handle this patchwork, not just the federal baseline.

What This Means for AI Specifically

The CFPB has been direct on this point: using AI doesn’t excuse non-compliance. If your AI agent sends a message that violates Regulation F, the fact that an algorithm decided to send it is not a defense.

Best practice is to have your AI clearly identify itself as a virtual agent rather than simulate a human collector, since ambiguity here adds legal risk with no major practical benefit. For a closer look at how compliance and AI decisioning intersect more broadly, see our guide on building AI due diligence platforms.

| Statutory damages under the FDCPA can reach $1,000 per violation, and class actions can climb to $500,000 or 1% of the collector’s net worth, plus legal fees. Compliance is not a paperwork exercise here; it is a direct cost-avoidance feature. |

How Much Does It Cost to Build Debt Collection Software?

The cost to develop a debt collection system depends heavily on how many channels, compliance jurisdictions, and integrations you need to support. Here is a realistic breakdown:

| Tier | Estimated Cost | What’s Included |

| MVP | $30,000 – $70,000 | Core account tracking, basic dashboard, single-channel outreach, manual compliance checklists |

| Mid-Tier | $70,000 – $150,000 | Omnichannel automation, AI-based scoring, self-service payment portal, 2–3 system integrations |

| Enterprise | $150,000 – $300,000+ | AI negotiation agents, predictive forecasting, multi-state compliance engine, full API ecosystem, white-label options |

The biggest cost drivers are the number of communication channels you automate, how many states or jurisdictions your compliance engine needs to cover, the sophistication of your AI models, and how many external systems (credit bureaus, core banking, payment processors) you need to connect.

If you are also evaluating a broader AI build, an automated debt collection software, our AI integration services page includes a real example: a mid-market lending platform that cut loan decision time from 5 days to under 4 hours after integrating AI into its workflows.

The same infrastructure principles apply directly to a debt collection software platform, whether you are building it as a standalone tool or as one module inside a broader debt collection management software suite.

Build vs. Buy: Which Makes Sense for You?

An off-the-shelf debt collection app can work fine if your portfolio is small, single-state, and your debt collection process doesn’t need to be differentiated. But if you are operating across multiple states, need collection logic that reflects your specific risk appetite, or want your recovery data feeding back into your own underwriting models, custom debt collection software development usually pays for itself within a year or two through better recovery rates and lower compliance risk.

This is the same calculus we walk through in our loan app development guide – the deciding factor is almost always how much your operational process differs from the generic templates a vendor is selling you.

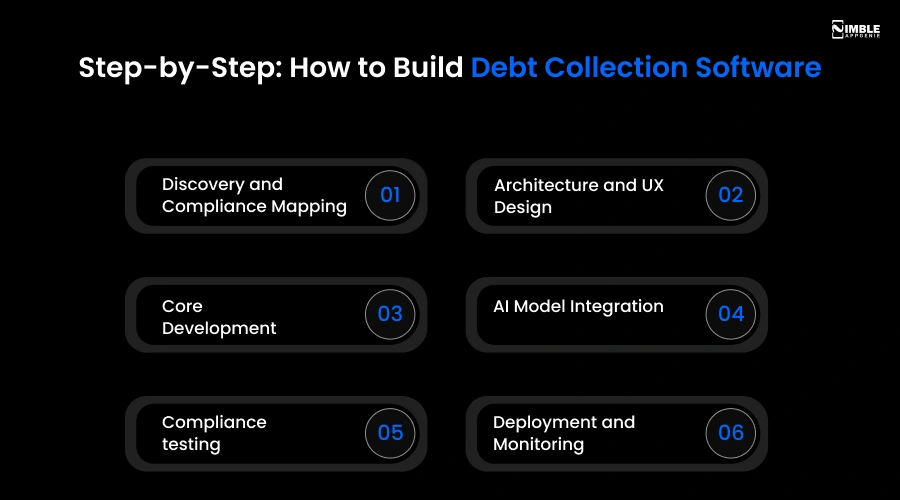

Step-by-Step: How to Build Debt Collection Software

Below are the steps to follow for debt collection software development:

Step 1: Discovery and Compliance Mapping

Map every state you operate in and the specific rules that apply before any design work starts.

Step 2: Architecture and UX Design

Design the collector-facing dashboard, account management core, and borrower-facing self-service portal.

Step 3: Core Development

Build a communication engine, account tracking, and payment processing engine.

Step 4: AI Model Integration

Add segmentation, predictive scoring, and (if applicable) conversational negotiation agents.

Step 5: Compliance testing

Run every workflow against FDCPA, TCPA, Regulation F, and your target states’ rules before launch, not after.

Step 6: Deployment and Monitoring

Launch with full audit logging active from day one, and monitor recovery rate and compliant volume closely in the first few months.

Common Mistakes to Avoid

- While you build debt collection software for small businesses, you should avoid the below common mistakes:

- Treating compliance as a feature to add later instead of the foundation the whole system is built on.

- Building single-state logic when your portfolio already spans multiple jurisdictions.

- Skipping real dispute-handling workflows, which creates direct FCRA exposure.

- Underestimating integration cost with legacy core banking or servicing systems.

How Nimble AppGenie Helps You Build Debt Collection Software?

Nimble AppGenie builds AI-powered fintech platforms for collection agencies, lenders, and fintech startups, with compliance mapped in from day one rather than bolted on after launch.

Our team already works across the full lending lifecycle, from lending software development to agentic AI deployments that automate underwriting and recovery workflows.

We design debt collection platforms with automated Regulation F and TCPA guardrails, AI-driven recovery scoring, and full audit trails built into the architecture, not added as an afterthought.

Talk to a Fintech Specialist

Conclusion

Debt collection software for small businesses and enterprises is no longer an efficiency play. In 2026, with enforcement shifting toward the states and AI adoption accelerating across the industry. The businesses that win are the ones treating compliance as core architecture, not an afterthought.

Get the AI feature right, budget realistically, and build compliance from day one, and software debt collection becomes one of the highest-return investments a lending business can make this year.

If you are ready to scope out a build, Nimble AppGenie can walk you through the AI features, realistic costs, and compliance requirements for your specific portfolio. Get in touch for a free discovery call, or explore our loan management software guide if you are building out the rest of your lending stack.

FAQs

Debt collection software manages the recovery process for unpaid debts, automating borrower outreach, payment tracking, dispute handling, and compliance documentation. It typically scores accounts by risk, sends automated but rule-bound communications, and gives borrowers a self-service way to pay or set up a plan.

Costs generally range from $30,000 for a basic MVP to $300,000 or more for an enterprise-grade platform with full AI negotiation, multi-state compliance, and deep system integrations. The exact number depends on the number of channels, jurisdictions, and integrations you need.

Yes, using AI in debt collection is legal, but the FDCPA and Regulation F still apply in full. The CFPB has stated clearly that using AI does not excuse non-compliance, so your AI-driven workflows need the same guardrails as a human collector would, including call frequency limits, validation notices, and consent tracking.

The 7-in-7 rule, part of Regulation F, presumes harassment if a collector calls a consumer about a specific debt more than seven times within seven consecutive days, or calls again within seven days of a phone conversation about that same debt.

AI debt collection software handles sensitive financial and personal data, so security has to cover encryption at rest and in transit, strict access controls, regular patching, and compliance with data privacy regulations like GDPR or state-level privacy laws. Any AI vendor or in-house build should also log every model decision for audit purposes, since regulators expect a clear trail of why an action was taken.

For a custom build, an MVP typically takes 3 to 4 months, a mid-tier platform with AI scoring and automation takes 5 to 8 months, and a full enterprise platform takes 9 to 12 months or more. Implementation time also depends heavily on data migration complexity and how many existing systems it needs to connect to.

Buying an off-the-shelf platform can work for smaller, single-state operations. Building custom software makes more sense if you operate across multiple states, need collection logic tailored to your own risk model, or want recovery data feeding directly back into your underwriting systems.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.