AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

TL;DR

- AI chatbots in fintech customer service now handle over 85% of routine interactions, saving the industry $11.5 billion annually.

- Modern fintech chatbots go far beyond answering FAQs – they run KYC, detect fraud in real time, process loans, and act as compliance auditors.

- The average fintech company sees a full ROI within 6–9 months of deploying an AI chatbot, with neobanks and payments companies averaging 320% ROI.

- Klarna’s AI handling 2.3 million conversations in one month, equal to 700 agents, is the clearest real-world proof of what scale looks like.

- Agentic AI is the next frontier -it does not just respond, it acts, decides, and completes multi-step financial workflows end-to-end.

- Compliance is not optional: GDPR, PSD3, DORA, KYC, and AML requirements must be built in from day one -not retrofitted.

- Nimble AppGenie, an experienced AI chatbot development company, builds compliance-ready, AI-powered fintech chatbots, from MVP through to enterprise-scale deployment, globally.

AI chatbots in fintech customer service now manage over 85% of routine customer interactions, and they are saving $11.5 billion for financial institutions every year. That’s not a projection; that’s where the fintech industry stands in 2026.

Yet most fintech companies are still running customer service the costly way – large support teams, inconsistent answers, long queues, and no audit trail. The three factors making this unsustainable are merging fast:

- Evolving customer expectations: People now anticipate 24/7, instant support – on any channel, in any language.

- Cost pressure: Hiring and retaining support agents costs 3-5x more than AI-powered automation at scale.

- Regulatory complexity: GDPR, DORA, PSD3, KYC, and AML requirements demand documentation and audit trails that human teams struggle to maintain consistently.

This guide is created for fintech founders, product leaders, and CTOs who want the full picture, not a surface-level overview. By the time you finish reading, you will know:

- What AI chatbots in fintech actually are and how they have evolved from basic IVR to agentic AI.

- The 10 highest-impact use cases, including ones your competitors have missed entirely.

- Exactly how to calculate the AI chatbot ROI for financial services for your specific business.

- A compliance checklist covering GDPR, PSD3, DORA, KYC, and AML.

- A 12-week implementation roadmap you can hand to your development team today.

What Are AI Chatbots in Fintech?

An AI fintech chatbot is software that replaces your front-line support team for routine financial queries, handling everything from account questions and KYC to fraud alerts and loan pre-qualification at a fraction of the cost, with a full compliance audit trail baked in.

But the version you are thinking of is perhaps already outdated. The technology has shifted through four different generations in less than a decade.

The Four Generations of Fintech Chatbots

| Generation | Technology | What It Could Do | Key Limitation |

| 2018 -Basic IVR / Rule-Based | Decision trees, keyword matching | Answer pre-set FAQs, route calls | Broke on any unexpected input |

| 2021 -NLP-Powered Bots | Natural Language Processing (NLP) | Understand intent, handle varied phrasing | No memory, no context retention |

| 2024 -LLM-Powered Bots | Large Language Models (GPT-4 class) | Contextual multi-turn conversation, personalisation | Still reactive -only responds when asked |

| 2026 -Agentic AI | LLM + multi-agent orchestration + APIs | Acts, decides, executes end-to-end workflows | Requires robust compliance architecture |

The technology behind these systems has evolved rapidly – for a full breakdown of how AI is being applied across the financial industry today, read our guide on AI in fintech.

What Is Agentic AI And Why Does It Matter for Fintech?

Agentic AI is an AI system that can independently plan, make decisions, and complete multi-step tasks instead of only responding to questions.

In fintech, it matters because it can automate complex workflows such as KYC verification, fraud detection, loan processing, compliance checks, and customer onboarding, helping companies reduce costs, improve efficiency, and scale operations faster. Agentic AI is the crucial shift in this space right now.

How does agentic AI differ from regular chatbots in financial services?

A standard chatbot waits for a question and responds. That’s it.

An agentic AI system receives a goal, such as “complete KYC verification for a new user,” and then plans and executes the required steps.

This can include collecting documents, verifying identity, cross-checking sanctions lists, running fraud checks, and generating compliance records. In fintech, these systems typically operate with built-in guardrails and may escalate edge cases to human review for regulatory compliance.

- McKinsey projects that agentic AI could reduce operational workloads in financial services by 30-50%.

- 53%+ of financial institutions are already running AI agents in production (Google Cloud, 2025).

- The global agentic AI market spend is projected at $50 billion (KPMG).

Agentic AI is already running in production at financial institutions worldwide. Our in-depth guide on agentic AI in financial services covers exactly what that means for fintech companies building now.

The State of AI Chatbots in Fintech in 2026

Why fintech companies can’t wait any longer. Three data points below will reframe this from ‘nice to have’ to ‘operationally important’:

- 43% of US banking customers now prefer chatbots over visiting a branch.

- 63% of consumers expect round-the-clock support, which human teams cannot deliver at scale.

- 80% of customer interactions in fintech will be AI-driven by the end of 2026 (Gartner).

The fintech companies that deployed AI chatbots two years ago are now working at a structural cost advantage. Their support cost per interaction is 60-80% lower. Their CSAT scores are higher, compliance audit trails are transparent, and the gap between AI-adopters and laggards is expanding every quarter.

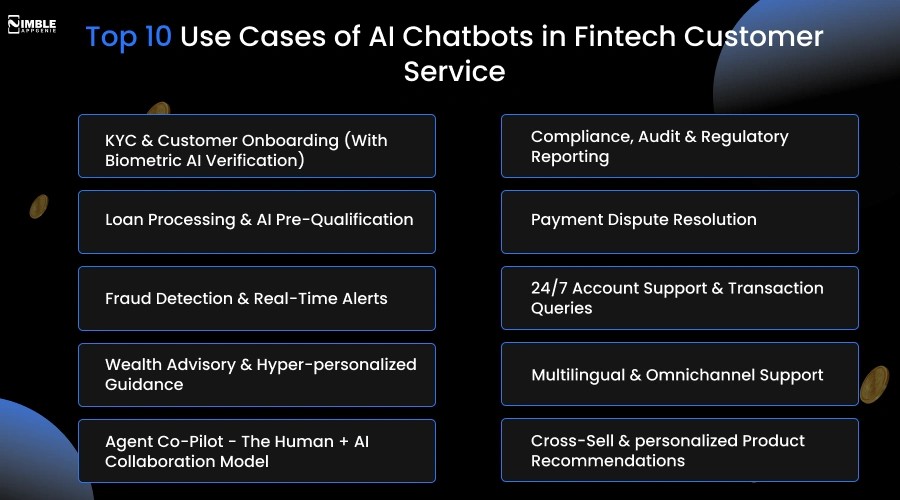

Top 10 Use Cases of AI Chatbots in Fintech Customer Service

Let’s get deeper and learn fintech chatbot use cases that companies should know.

1. KYC & Customer Onboarding (With Biometric AI Verification)

Friction makes traditional KYC drop 40-60% of applicants. AI-powered onboarding chatbots guide users sequentially through document upload, facial recognition matching, liveness detection, and sanctions screening in a single mobile session.

Can AI chatbots process KYC and onboarding automatically?

Yes. Modern fintech chatbots can automate large parts of the KYC and onboarding process by integrating e-KYC with biometric AI verification.

Instead of simply collecting documents, the chatbot can verify liveness (determining whether the user is a real person rather than a photo or spoof attempt), match facial features against the submitted ID, and cross-check information against PEP (Politically Exposed Persons) and sanctions databases in real time.

This reduces onboarding friction, accelerates verification, and creates a stronger compliance process with an automated audit trail.

KYC is one of the most complex compliance requirements in fintech. Our dedicated guide on KYC in fintech apps covers how it works, what types exist, and how AI is automating it end-to-end.

| Advanced AI tools in KYC/AML have increased from 42% to 82%, with Singaporean firms leading (92%), followed by the US (79%) and the UK (77%). |

2. Loan Processing & AI Pre-Qualification

Manual loan processing demands an average of 3 working days. An AI chatbot pre-qualifies applicants within 2 minutes by pulling credit bureau data and assessing alternative data signals (cash flow patterns, transaction behavior), and showcasing a preliminary offer, all within the same conversation.

Process:

- Customer initiates loan request,

- Chatbot collects 6 data points,

- API call to credit scoring engine,

- AI assesses eligibility,

- Preliminary offer presented, and

- Hand off to a human underwriter only if an edge case is detected.

| Natural Language Processing (NLP) technologies extract and validate information from submitted documents, reducing processing time by up to 80% and error rate by 90%. |

For fintech companies building lending products, our loan lending app development page covers AI-powered credit scoring, automated KYC, and smart loan lifecycle management.

3. Fraud Detection & Real-Time Alerts

AI chatbots integrated with ML fraud detection engines monitor each transaction as it happens. On an anomaly detection, an unusual location, a transaction pattern outside the user’s norm, or a device fingerprint mismatch, the chatbot instantly contacts the customer for verification.

Here is what that alert flow looks like in practice:

- ML model flags a $2,300 transaction in a new geography as high-risk (confidence: 94%).

- Chatbot sends a push notification and in-app message within 0.3 seconds.

- Customer taps ‘This wasn’t me’ – chatbot instantly freezes the card and opens a dispute case.

- Full audit trail logged automatically for compliance review.

AI is also transforming the payments layer underneath customer service. See how in our guide on AI in digital payments.

| Klarna’s AI reduced repeat inquiries by 25% and resolved issues in under 2 minutes vs. 11 minutes previously |

4. Wealth Advisory & Hyper-personalized Guidance

In 2026, wealth advisory chatbots offer hyper-personalized guidance, adjusting SIP amounts based on cash flows, rebalancing portfolio suggestions based on risk profile shifts, and flagging tax optimization opportunities.

The difference between an AI chatbot for wealth management customer service and basic robo-advisors: These chatbots leverage real-time transactions, not only user-submitted preferences. They witness your actual spending and income patterns and make recommendations fixed in your financial reality, not a form you filled in once.

Wealth advisory chatbots are closely related to robo-advisor technology. Our guide on robo advisor platform development explains exactly how these systems work and what it takes to build one.

| McKinsey data shows personalized financial experiences can boost customer satisfaction by 15-20% and revenue by 5-8%. Hyper-personalized AI chatbots see 2.3x higher engagement than generic robo-advisors. |

5. Agent Co-Pilot – The Human + AI Collaboration Model

The best fintech chatbot deployments are not about replacing human agents. They are about making human agents dramatically more effective. The Agent Co-Pilot model puts AI alongside the human, but does not replace them.

What this looks like in real practice: When a complex call comes in, the AI co-pilot listens in real-time, transcribes the conversation, comes up with the customer’s complete history and related policy information, tags the emotional sentiment of the call (distress, confusion, and frustration), and drafts a resolution summary – all before the human agent has to type a single word.

The result: Average Handle Time (AHT) drops by 35-45%. Agent satisfaction improves, and each interaction is automatically documented for quality review and compliance.

6. Compliance, Audit & Regulatory Reporting

It’s one of the most valuable for fintech companies.

An AI chatbot can be configured to automatically generate audit trails for each customer interaction, produce PSD3-compliant transaction summaries, flag interactions that need human review under GDPR Article 22 (automated decision-making), and generate DORA-ready incident logs when service disruptions occur.

The practical impact: A compliance team that used to take a week to compile for a regulatory audit can now generate in minutes, as the chatbot has been logging everything in a structured, query-ready format from day one.

| Key regulations your chatbot compliance architecture must cover: GDPR (data privacy, consent, right to explanation), PSD3 (payment service transparency), DORA (digital operational resilience, incident reporting), KYC/AML (identity verification, suspicious activity reporting). |

7. Payment Dispute Resolution

AI chatbots manage the whole dispute flow, collecting evidence, cross-referencing merchant data, checking the transaction timeline, filing the claim with the related payment network, and sending real-time status updates to the customer throughout, despite running a 7-10 day dispute process through a call center.

8. 24/7 Account Support & Transaction Queries

The basic use case, but still worth stating transparently. AI chatbots manage balance inquiries, payment confirmations, transaction history, card management, and statement requests around the clock.

Now, 43% of banking customers prefer this over visiting a branch. The chatbot never has a bad day, never sleeps, and manages thousands of conversations simultaneously.

9. Multilingual & Omnichannel Support

Modern fintech chatbots support 50+ languages and work across mobile apps, web, voice, SMS, and WhatsApp, maintaining the whole conversation context across channels.

A user who begins a query on WhatsApp can continue it in the app without repeating themselves. For fintech companies operating across India, Southeast Asia, the Middle East, and Europe, this is not a feature; it’s a market access need.

10. Cross-Sell & personalized Product Recommendations

AI in fintech customer support analyzes user behavior and transaction patterns to identify the right moment for a product recommendation – a credit card offer when a user is constantly overspending their debt account, an insurance product after a big purchase, and a savings product when salary patterns reveal a constant monthly surplus, no spray-and-pray, only context-aware.

Retaining users once you have acquired them is where fintech revenue compounds. Our guide on fintech app features covers the 39 features that drive engagement and retention in high-performing financial apps.

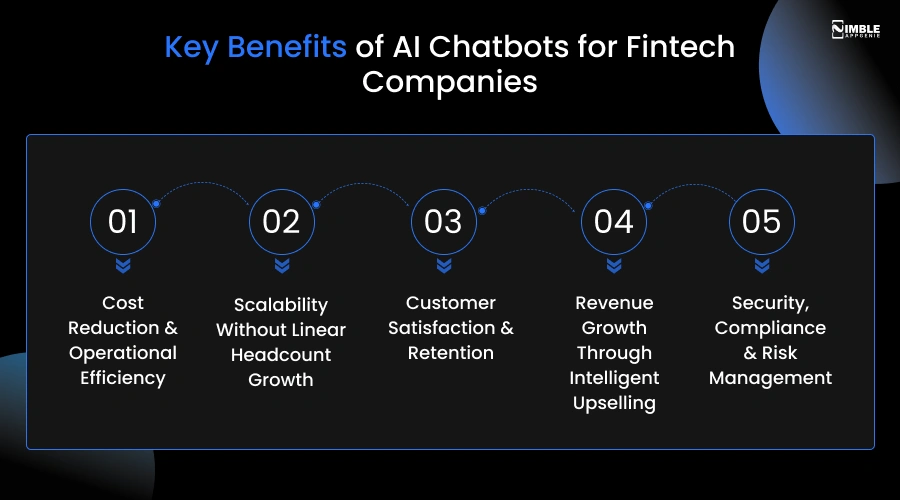

Key Benefits of AI Chatbots for Fintech Companies

AI chatbots for fintech companies help in many ways. Below are the key benefits with real-world examples.

1. Cost Reduction & Operational Efficiency

Most fintech companies reach an edge where customer support volume expands the team handling it. The obvious answer is hiring more agents. But it’s the most costly one. Salaries, attrition, management layers, and training costs stack up fast, and the issue never completely goes away as volume keeps growing.

AI chatbots break the cycle. How do AI chatbots reduce customer service costs in fintech? They manage the high-volume, repetitive queries that take the majority of agent time – transaction status, account questions, payment confirmations, and KYC guidance without any incremental cost per conversation. The more queries they manage, the lower your cost per interaction gets.

Gartner predicts conversational AI will reduce contact center agent labor costs by $80 billion globally in 2026. The figure showcases what happens when thousands of organizations shift routine interaction volume away from human agents simultaneously.

Real example: Klarna attributed $40 million in profit improvements to its AI assistants in the first year, not by cutting service quality, but by managing two-thirds of all customer service conversations through AI while freeing human agents to focus on high-value, complex cases.

2. Scalability Without Linear Headcount Growth

A traditional customer support team scales linearly. As users double, you roughly need double the agents. For a fintech growing from 100,000 to one million users, that math becomes a serious financial and operational constraint – especially during fundraising rounds when burn rate is closely scrutinised.

AI chatbots don’t scale that way. One deployment manages ten conversations or ten thousand simultaneously, at the same infrastructure cost. Your support capacity grows with your user base without a proportional expansion in payroll, headcount, or management overhead.

Real example: Bank of America’s AI assistant Erica handled 676 million client interactions in 2024 alone across transaction questions, balance inquiries, savings nudges, and dispute flagging. That volume would be operationally challenging to absorb through human agents alone and excessively expensive to attempt.

3. Customer Satisfaction & Retention

Long customer wait times can lead to increased churn in fintech products. A fraud alert they can’t reach anyone about, a KYC document request with no follow-up, and a payment query stuck in a queue; all these are not dramatic failures; they are the everyday frictions that make customers choose competitors.

Fenergo’s 2025 survey of 600 senior financial executives discovered that 70% of financial institutions lost clients in the past year due to slow, inefficient processes – the highest rate ever recorded. Customers didn’t leave because of product issues. They left because getting help was too tough.

Now, you would ask, “How can we reduce customer wait times in our banking app?”

AI chatbots reduce that friction at the source. They respond immediately, retain context throughout the conversation, and resolve the most common queries without any wait time – at any hour, on any day.

Real Example: Klarna’s AI assistant cut average resolution time from 11 minutes to under 2 minutes. Customer repeat contact rates reduced by 25% – meaning issues were being resolved the first time correctly, not only closed and reopened.

4. Revenue Growth Through Intelligent Upselling

Typically, support interactions are treated as a cost to minimize. AI chatbots reframe them as a revenue opportunity because each conversation is a moment when the chatbot already has the customer’s attention and their complete financial context in view.

A customer asking about their balance who constantly runs low in the final week of the month is a candidate for a credit product or an overdraft facility.

A customer who has only received a large salary payment is a candidate for an investment or savings product. And a customer disputing a transaction on a particular merchant category might benefit from a cashback card for that spending type.

The difference between a well-timed AI recommendation and a generic product push is context. McKinsey’s research confirms that personalized financial experiences boost customer satisfaction and revenue by 5–15%, and AI is the only mechanism that delivers that personalization at scale, in real time, without a human making each judgment call.

Real Example: Klarna’s AI manages personalized cross-sell flows as part of its standard conversation design, contributing to the $40 million profit improvement attributed to its AI deployment in year one. The revenue came not only from cost reduction but from context-aware customer engagement.

5. Security, Compliance & Risk Management

Compliance in fintech touches each customer interaction. Every transaction query, onboarding conversation, and dispute resolution carries regulatory weight. PSD3, GDPR, AML, and KYC – the documentation requirements are consistent, and the penalties for gaps are notable.

AI chatbots address this in two ways that most fintech companies have not fully accounted for yet.

First, automatic audit trails. Every chatbot interaction is logged, structured, and timestamped from the moment it happens. When a regulator asks for documentation, it is already there, not assembled the week before a review under pressure.

Second, real-time fintech fraud detection AI. AI models embedded in chatbot workflows monitor transaction patterns constantly, flagging anomalies before they become losses.

Here, the speed benefit is significant – a rule-based system catches known patterns; an ML-powered chatbot catches behavior that has never been witnessed before.

ROI of AI Chatbots in Financial Services: Real Numbers

The Formula:

ROI (%) = [(Annual Cost Savings + Revenue Uplift) – Total Implementation Cost] ÷ Total Implementation Cost × 100

Payback Period (months) = Total Implementation Cost ÷ (Monthly Cost Savings + Monthly Revenue Uplift)

Most financial institutions ask two common questions:

“How do I calculate the cost savings from a banking chatbot?” and “Our fintech support team is overwhelmed – can AI chatbots realistically reduce the workload?”

Let’s understand it through an example below.

Worked Example – Mid-Size Fintech with 50,000 Monthly Support Tickets

| Variable | Value | Notes |

| Monthly support tickets | 50,000 | Baseline volume |

| Chatbot deflection rate | 65% | Industry average for well-trained fintech bots |

| Tickets deflected per month | 32,500 | 50,000 × 65% |

| Average cost per human ticket | $8.50 | Typical for mid-market fintech support |

| Monthly cost savings | $276,250 | 32,500 × $8.50 |

| Annual cost savings | $3,315,000 | $276,250 × 12 |

| Revenue uplift (cross-sell, reduced churn) | $480,000/yr | Conservative 15% of cost savings |

| Total annual benefit | $3,795,000 | Cost savings + revenue uplift |

| Implementation cost (one-time) | $55,000 | Mid-range custom build |

| Annual licensing & maintenance | $72,000 | $6,000/mo licensing + maintenance |

| Year 1 total cost | $127,000 | Implementation + first year running costs |

| Year 1 ROI | 2889% | [(3,795,000 – 127,000) ÷ 127,000] × 100 |

| Payback period | < 1 month | Savings begin immediately as tickets are successfully deflected. |

ROI Benchmarks by Fintech Segment

| Fintech Segment | Average ROI | Primary Driver | Avg Payback Period |

| Payments & Neobanks | 320% | High ticket volume + simple query types | 5–7 months |

| Retail Banking | 280% | Account servicing automation + fraud alerts | 6–8 months |

| Insurance (Insurtech) | 240% | Claims triage + policy query automation | 7–10 months |

| Wealth Management | 190% | Complex queries need more human oversight | 8–12 months |

| Lending Platforms | 260% | Loan pre-qual + application support automation | 6–9 months |

Cost Breakdown – What You Are Actually Paying For

| Cost Component | Range | Notes |

| Licensing (SaaS platform) | $1,500 – $8,000 / month | Varies by volume, features, and compliance tier |

| Custom implementation (one-time) | $15,000 – $80,000 | Depends on integrations, use cases, and compliance build |

| Annual maintenance | 10–15% of the implementation cost | Model retraining, conversation flow updates, and monitoring |

| Compliance architecture (one-time) | $8,000 – $25,000 | Often underestimated -budget for this separately |

| Training data preparation | $5,000 – $20,000 | Financial intent training, NLP tuning, QA |

Want to see a real fintech product we built? Our Pay By Check case study walks through how we delivered a multi-currency eWallet that works across iOS, Android, and web – compliantly and at scale.

| The most common budgeting mistake: Teams plan for licensing and implementation, but forget training data and compliance architecture. These two items alone can add $13,000–$45,000 to your build cost if not scoped upfront. Include them in your first estimate. |

Understanding the full cost picture matters before you commit to a build. Our AI app development cost guide breaks down every cost component from MVP through enterprise scale.

AI Chatbot 12-Week Implementation Roadmap for Fintech

Fintech companies usually ask:

- How to implement AI chatbot in financial services step by step?

- How long does it take to implement an AI chatbot for a fintech company?

Below is the exact process Nimble AppGenie follows when building a fintech chatbot, from discovery through to live deployment. Explore the AI chatbot implementation roadmap in financial services.

Phase 1: Discovery & Planning (Weeks 1–3)

| Activity | Detail | Output |

| Support ticket audit | Analyse 3–6 months of tickets; identify the top 20 query types by volume | Query frequency matrix |

| Use case prioritisation | Map queries to chatbot capability; rank by ROI impact and build complexity | Prioritised use case list |

| Vendor/architecture decision | Evaluate: custom build vs. platform, LLM selection, NLP engine | Tech stack decision doc |

| Integration mapping | Document all APIs: core banking, CRM, credit bureau, fraud engine, KYC provider | Integration architecture diagram |

| Compliance scoping | Identify applicable regulations; brief legal/compliance team; scope audit trail requirements. | Compliance requirements doc |

| Deliverable: Use Case Matrix + Vendor Shortlist + Compliance Scope Document |

Phase 2: Build & Integrate (Weeks 4–7)

| Activity | Detail | Output |

| API integration | Connect to core banking, CRM, fraud detection, KYC, and credit scoring systems | Live API connections + test results |

| Intent training | Train NLP on fintech-specific language, financial jargon, and local dialects | Trained intent model (>90% accuracy target) |

| Compliance build | GDPR consent flows, audit logging, PSD3 disclosures, DORA incident triggers, AML flags | Compliance-approved architecture |

| Agent handoff design | Define escalation triggers; build seamless human handoff with full context pass-through | Escalation workflow + agent UI |

| QA & security testing | Penetration testing, adversarial conversation testing, edge case QA, load testing | QA sign-off report |

| Deliverable: Compliance-Approved Chatbot + Full Integration Documentation + QA Report |

Phase 3: Launch & Optimise (Weeks 8–12)

| Activity | Detail | Output |

| Soft launch (10% traffic) | Deploy to a controlled user segment; monitor for errors, edge cases, compliance gaps | Initial performance baseline |

| KPI monitoring setup | Track: deflection rate, CSAT, AHT, first-contact resolution, escalation rate | KPI dashboard (live) |

| A/B conversation testing | Test alternative phrasings, flows, and escalation triggers for optimization | Winning conversation flows |

| Full rollout | Scale to 100% of traffic; brief the support team on the co-pilot model | Full live deployment |

| Ongoing optimization cadence | Monthly model retraining, quarterly compliance review, bi-annual audit | Review calendar + owner assignments |

| Deliverable: Live Deployment + KPI Dashboard + Monthly optimization Cadence |

The KPIs That Actually Matter

The fintech companies usually ask, “What metrics should I track for my fintech chatbot performance?” or “How to measure chatbot performance in banking?” The table below will answer these questions.

| KPI | What to Measure | Target Benchmark |

| Deflection Rate | % of tickets fully resolved without a human agent | 60–75% within 90 days |

| CSAT Score | Post-interaction satisfaction rating | >4.2 / 5.0 |

| First-Contact Resolution (FCR) | % resolved in one interaction, no follow-up needed | >70% |

| Average Handle Time (AHT) | Time from first message to resolution | < 3 minutes for routine queries |

| Escalation Rate | % of chatbot conversations escalated to a human | < 25% |

| Compliance Audit Pass Rate | % of AI decisions flagged correctly for human review | 100% -non-negotiable |

Choosing the Right AI Chatbot Development Company: Selection Criteria

Picking the wrong partner is one of the most costly mistakes a fintech company can make. A platform that works for a retail eCommerce business will not manage KYC flows, PSD3 compliance requirements, and fraud escalation logic.

The selection criteria for fintech AI chatbots are basically different from general customer service tools.

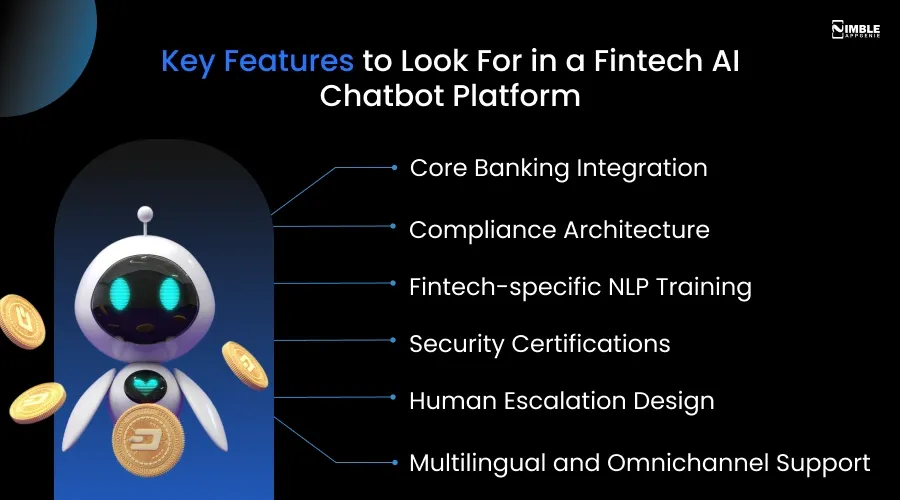

Key Features to Look For in a Fintech AI Chatbot Platform

You might be wondering, “What features should a fintech AI chatbot have?” Before shortlisting any agency, you should verify these non-negotiables:

1. Core Banking Integration

Can your AI chatbot connect to your current core banking system, KYC provider, fraud detection engine, and CRM via API?

2. Compliance Architecture

Does the platform support GDPR consent logging, data residency controls, and full audit trails? If the company can’t answer this in detail, walk away.

3. Fintech-specific NLP Training

General chatbot platforms are trained on generic language. Financial queries – KYC document requirements, loan eligibility, and transaction dispute flows need domain-specific intent models.

4. Security Certifications

PCI DSS compliance, ISO 27001, and SOC 2 Type II. These are mandatory for any platform managing financial data.

5. Human Escalation Design

How does it hand off to a human agent? A clunky handoff destroys the experience. Does it pass full conversation context, sentiment tags, and customer history?

6. Multilingual and Omnichannel Support

Web, WhatsApp, mobile app, and voice. If your users are across markets, then single-channel is not sufficient.

Nimble AppGenie helps fintech firms needing complete control in building a custom AI chatbot to their exact regulatory needs to integrate with any systems through the required API.

Build Custom vs. Buy a Platform -Which Is Right for You?

Most fintech companies make a common mistake where they choose the cheapest option upfront and discover 18 months later that it can’t handle their compliance requirements or expand with their user base.

Is it better to build or buy an AI chatbot for my bank? The table below will make it clear for you.

| Factor | Off-the-Shelf Platform | Custom Build |

| Time to deploy | 2–4 weeks | 8–12 weeks |

| Upfront cost | Low ($1.5K–$5K/mo) | Medium-High ($25K–$80K one-time) |

| Compliance customisation | Limited -generic templates | Full -built to your regulatory requirements |

| Integration flexibility | Limited to platform connectors | Any API, any system, any data source |

| Training on your data | Partial -general financial NLP | Fully trained on your actual ticket data |

| Scalability | Platform limits apply | Scales with your architecture |

| Long-term cost | High -ongoing licence fees at scale | Lower -maintenance only after build |

| Best for | MVP / proof of concept | Production-grade, compliant, scalable deployment |

| Our recommendation for most fintech startups: If you are testing whether a chatbot adds value, buy a platform and learn fast. If you are building for compliance, scale, and a specific user journey – build custom. Most fintech companies that start with a platform end up rebuilding within 18 months anyway, at increased total cost. |

Our fintech app development services page covers the full scope of what we build, from neobanks and lending platforms to AI-powered wallets and compliance tools.

Regulatory Compliance & Security in Fintech AI Chatbots (2026)

It’s not only like inviting a legal risk when a fintech chatbot doesn’t meet regulatory requirements, but it’s also a reputational one.

Below is the compliance checklist that each fintech AI chatbot deployment should address, and you will also know how to train an AI chatbot on financial regulations like GDPR and PSD3.

AI Chatbot Compliance Regulations Fintech 2026

| Regulation | Requirement for Chatbot | How to Meet It |

| GDPR | Lawful basis for processing, right to explanation for automated decisions, data minimisation | Consent logging, Article 22 flags, human escalation trigger for high-stakes decisions |

| PSD3 | Transparent transaction communication, strong customer authentication | Chatbot must explain transaction status clearly; integrate with SCA flows |

| DORA | Digital operational resilience, incident reporting within 4 hours | Chatbot downtime triggers automated DORA-compliant incident logs |

| KYC / AML | Identity verification, sanctions screening, suspicious activity reporting | Biometric e-KYC integration, real-time PEP/sanctions API, SAR filing workflow |

| PCI DSS | Secure handling of payment card data | No card data stored in chatbot logs; tokenisation required for card queries |

| RBI Guidelines (India) | Data localisation, customer grievance redressal timeline | All data stored in India; 30-day resolution SLA tracking built in |

| Transparent data use disclosures are not only a legal requirement, but they are also a competitive advantage. Build chatbot’s consent and transparency flows before you create anything else. |

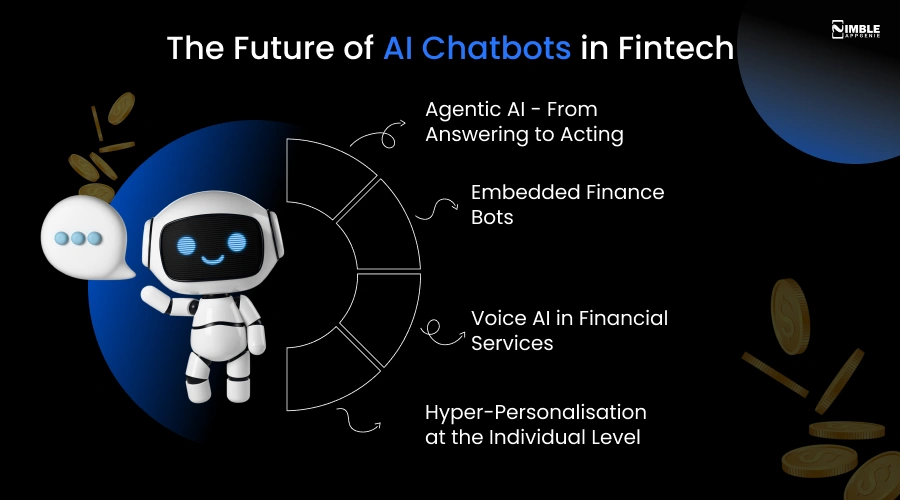

2026 Trends: The Future of AI Chatbots in Fintech

You may be wondering: “What are the latest AI chatbot trends in fintech 2026?” or “How is AI transforming fintech in 2026?” The fintech chatbot in 2026 looks basically different from 2023. The four shifts below define what comes next.

1. Agentic AI – From Answering to Acting

The most notable shift is from reactive to agentic AI fintech. The best chatbots today answer questions and complete simple transactions.

Agentic AI systems receive an objective and execute each step needed to attain it, running KYC end to end, resolving a dispute from evidence collection to claim filing, and processing a loan application from submission to preliminary decision without a human approaching every step.

2. Embedded Finance Bots

The next generation of fintech chatbots will not be integrated in a fintech app; they will be embedded inside the platforms and products customers already use daily.

For example: a lending bot embedded in an e-commerce checkout, a chatbot embedded in an accounting tool that proactively flags cash flow issues, and an insurance bot embedded in a travel booking platform. The chatbot reaches the customers where they already are, rather than waiting for them to open a separate app.

3. Voice AI in Financial Services

Voice-first interactions are preferred more than text-based chatbots, particularly for accessibility use cases, older demographics, and markets where voice is the ruling mobile interface.

Voice AI in fintech means a customer can authorize a payment, check their balance, or report a suspicious transaction completely through voice interactions with the same security, context awareness, and compliance logging as a text conversation.

Voice is the next frontier in fintech customer interaction. Our breakdown of voice payments in fintech covers where the technology stands today and what to build for.

4. Hyper-Personalisation at the Individual Level

Early personalization in fintech meant dividing users into broad categories. The 2026 version works at the individual level – behavioral signals, real-time transactions, predictive modeling, and life event detection combined to deliver an intervention or a recommendation that is specific to one customer’s financial reality at that particular moment.

Retaining users once you have acquired them is where fintech growth compounds. Our guide on user retention in fintech apps covers the strategies that work in practice.

Conclusion

AI chatbots in fintech customer service are not an innovation anymore; they have moved to infrastructure. Now, the question is no longer whether to deploy one; it’s whether the chatbot you build will be integrated enough, compliant enough, and intelligent enough to actually make your business succeed.

The difference between a chatbot that generates ROI and one that becomes a liability is completely in how it is architected. It should be compliance-first, trained on real financial language, integrated deeply with your core systems, and built with a human escalation model that supports your agents rather than frustrating your customers.

That is exactly how Nimble AppGenie approaches every fintech chatbot engagement, from use case scoping and compliance architecture through to live deployment and ongoing optimization. We have built AI-powered financial products for startups and enterprises across AI customer service, banking, lending, payments, and insurance globally.

If you are ready to explore what is possible for your product, the first step is a conversation with our AI app development company.

The first step is a 30-minute conversation with no obligation. Schedule a free AI audit, and we will tell you exactly what to build, what it will cost, and how long it will take.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.