AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Quick Answer:

ACH transfers are best for regular, lower-cost payments like payroll and vendor bills. Wire transfers are best for large, urgent, or international payments. ACH is cheaper and reversible. Wire is faster and final. Choose based on the size, timing, and destination of your payment.

Key Takeaways:

- ACH vs wire transfer for business depends on payment speed, cost, amount, and destination. ACH transfer works best for recurring domestic payments, while wire transfer is better for urgent or international transactions.

- ACH payments are low-cost and usually settle in 1 to 3 business days. Same-day ACH is also available for faster payroll, vendor payments, and subscription billing.

- Wire transfers move money directly between banks and usually arrive the same day in the US. International wire transfer payments can take 1 to 5 business days through the SWIFT network.

- ACH transfer fees are usually a few cents per transaction, while wire transfer fees can range from $15 to $50. International wire transfers may also include hidden foreign exchange markups.

- Businesses use ACH for payroll, recurring vendor payments, and customer billing. Wire transfer is commonly used for real estate deals, international suppliers, and high-value payments.

- RTP and FedNow are newer real-time payment systems offering instant transfers at lower costs.

When it comes to ACH vs wire transfer, most businesses pick one based on habit or what their bank suggests. That is fine, until a payroll gets delayed, a real estate closing falls through, or you realise you paid $40 for a transfer that cost 50 cents the other way.

Both payment methods move money between bank accounts. But they work differently, cost differently, and serve different situations. Using the wrong one at the wrong time has real consequences.

If you are also building a payment feature into your app or platform, then this guide is for you. It breaks down exactly how each payment type works, what it costs, how long it takes, and when to use it. It can help you get the payment infrastructure right from the start.

So, let’s begin!

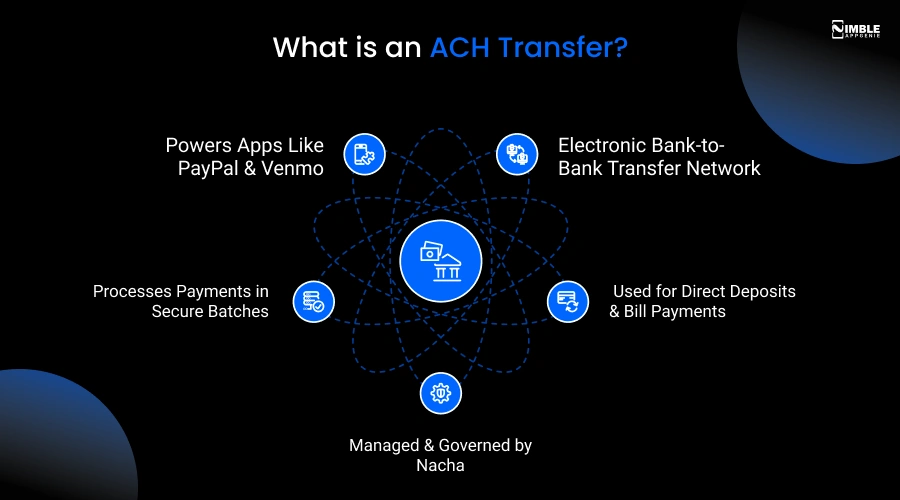

What Is an ACH Transfer?

ACH stands for Automated Clearing House. It is a network that moves money electronically between US bank accounts.

You have almost certainly used ACH, even if you did not know it by that name. Direct deposit, online bill pay, automatic subscription charges, and most peer-to-peer apps like PayPal and Venmo all run on the ACH network.

Nacha runs and governs the ACH network. When you initiate an ACH payment, your bank bundles it into a batch with other transactions from the same processing window. That batch goes to the ACH network, which routes each payment to the right recipient bank.

ACH Push vs ACH Pull

There are two types of ACH transactions:

- ACH push: You send money to someone else. For example, paying a vendor.

- ACH pull: You authorize someone to pull money from your account. For example, a subscription service charges your account each month.

Both types move money the same way. The difference is just who initiates the transfer.

Standard ACH vs Same-Day ACH

Not all ACH transfers move at the same speed. There are three tiers:

- Standard ACH: It settles in 1 to 3 business days.

- Next-Day ACH: It settles the next business day.

- Same-Day ACH: It sets the same business day if submitted before the 4:45 PM ET cut-off.

Same-day ACH has a per-transaction limit of $1 million. It costs a bit more but is mostly cheaper than a wire transfer.

| Example: You run a 50-person company and process payroll every two weeks. You use ACH to direct-deposit salaries. Submitting payroll on Wednesday afternoon means your employees see the money in their accounts by Friday morning. The total cost is a few cents per transaction. |

What is a Wire Transfer?

A wire transfer moves money directly from one bank to another. Unlike ACH, it does not batch with other transactions. It goes out individually and almost in real time.

For domestic US transfers, banks use the Fedwire network. For international money transfers, banks use the SWIFT network, which connects financial institutions globally.

Domestic vs International Wire

Domestic wires are easy. Your bank debits your account, sends the funds to the recipient bank, and the money arrives the same day, as long as you submit before your bank’s cut-off time. Cut-off times simply fall between 3 PM and 5 PM ET.

International wires are more complex. Your money may travel through one or more intermediary banks before reaching its destination. Each intermediary can deduct its own fee. Transmit time is usually 1 to 5 business days, depending on the destination country.

| For example, you import raw materials from a manufacturer in Germany. They require full payment before shipping. You send a SWIFT wire transfer on Monday morning. The funds arrive in Germany by Wednesday, and your order ships on Thursday. A US-only ACH could not have handled this at all. |

ACH vs Wire Transfer: A Quick Comparison

ACH and wire transfers are two common ways to send money electronically, but they work differently. Wire transfers are usually faster and send money directly between banks. ACH transfers go through a processing network and may take a few business days.

Here is the comparison table of ACH vs Wire Transfer. Take a look at how the two electronic payment types compare across the factors that matter most to businesses.

| Feature | ACH Transfer | Wire Transfer |

| Settlement time | 1–3 business days (standard); same day available | Same day (domestic); 1–5 days (international) |

| Outgoing fee | $0.20–$1.50 per transaction | $15–$50 per transfer |

| Incoming fee | Free or minimal | $10–$20 at most banks |

| Reversible? | Yes — within a limited window | No — rarely |

| Transaction limit | $1M per transaction (same-day ACH) | No federal cap |

| International? | US only (limited IAT exceptions) | Yes — worldwide via SWIFT |

| Processing style | Batch | Individual |

| Best for | Payroll, recurring bills, vendor payments | Large, urgent, or international payments |

| Risk level | Lower (reversible) | Higher (irreversible) |

ACH Payment vs Wire Transfer: Full Feature-by-Feature Comparison

Now that you have deeply understood every payment method, let’s put ACH transfer vs Wire Transfer side by side across the factors that matter most for businesses. Take a look at the wire transfer vs ACH comparison in detail.

1. Speed Comparison

Speed is often the deciding factor when choosing between an ACH payment vs wire transfer. Here is what actually happens on each timeline.

Standard ACH takes 1 to 3 business days. Same-day ACH requires submission before 4:45 PM ET. It does not run on weekends or federal holidays. Domestic wires settle within hours if sent before your bank’s cut-off. International wires take 2 to 5 business days.

# Real World Gap

For most routine payments, the speed gap does not matter. An ACH submitted on Wednesday afternoon usually arrives by Friday. But if you need funds there by tomorrow morning and it is already Thursday afternoon, a wire transfer is your only reliable option.

| Factor | ACH Transfer | Wire Transfer |

| Standard processing time | 1-3 business days | Domestic: same day or within hours |

| Faster option | Same-day ACH available | Usually already fast |

| International timing | Limited support | 2-5 business days |

| Weekend/Holiday processing | Not processed on weekends or federal holidays | Depends on banks, but usually business days only |

| Cut-off Time | Same-day ACH cut-off: 4:45 PM ET | Bank-specific cut-off times |

| Best use cases | Routine payments like payroll and vendor payments | Urgent or high-value payments |

2. Cost Comparison: What Your Business Actually Pays

This is the difference between ACH and wire transfer from each other. The cost gap is significant if you run high volumes of transactions.

-

ACH Transfer Costs

ACH is cheap. Many business accounts include a set number of free ACH transfers monthly. Incoming ACH is almost always free.

-

Wire Transfer Fees by Bank

Here are the current approximate fees at major US banks for business accounts. Always confirm directly with your bank before planning.

| Bank | Out-Domestic | In-Domestic | Out – International | In – International |

| Chase business | $25–$35 | $15 | $40–$50 | $15 |

| Bank of America Business | $30 | $15 | $45 | $16 |

| Wells Fargo Business | $30 | $15 | $45 | $16 |

| Citi Business | $25 | Free | $35 | Free |

Fees shown are approximate and may vary by account type or negotiated pricing. Verify current rates with your bank.

-

The Hidden Cost: FX Markup on International Wires

Banks convert your dollars at a rate worse than the mid-market exchange rate. The markup is typically 2% to 4%. On a $50,000 payment, that is $1,000 to $2,000 in hidden costs on top of the transfer fee.

If you send international payments regularly, compare fintech apps like Wise Business or Airwallex. They usually offer rates closer to the mid-market rate.

3. Transaction Limits

For same-day ACH, Nacha sets a per-transaction limit of $1 million. Standard ACH has no Nacha cap, but your bank sets its own daily limits, which vary from $25,000 to several million dollars per day.

If you need to go above your bank’s limit, call the business line. Limit increases are common for established accounts.

There is a federal cap on wire transfers. Banks set their own limits. For very large wires, your bank may ask for additional verification. That is a fraud detection and prevention step, not a legal restriction.

| Factor | ACH Transfer | Wire Transfer |

| Same-day Limit | $1 million per transaction | No federal limit |

| Standard limit | Bank-dependent | Bank-dependent |

| Daily limits | Usually $25,000 to several million | Usually very high |

| Large transaction approval | Possible bank approval needed | Verification often required |

4. Security and Fraud Risks

Both payment types carry fraud risk, and fintech security is really important, but the risk profiles are very different.

(i) ACH Fraud and Returns

The main ACH risk is unauthorised debits. Someone gets your account and routing number and pulls funds without your permission. ACH is reversible. Businesses typically have 24 hours from when a transaction posts to dispute it.

Common ACH return codes:

- R01 – Insufficient funds

- R02 – Account closed

- R10 – Customer advises not authorized

- R29 – Corporate customer advises not authorized

- R16 – Account frozen

Note: business accounts have a 24-hour dispute window. Consumer accounts have 60 days. Check your bank’s terms.

(ii) Wire Transfer Fraud

Wire fraud is a different level of risk. Once a wire leaves your bank, it is almost impossible to recover. There is no return code system and no standard reversal window.

The FBI’s Internet Crime Complaint Center reported that Business Email Compromise scams cost US businesses over $2.9 billion in 2023. Most BEC scams end in a fraudulent wire transfer.

How to Protect Your Business?

- It requires dual authorization for all wire transfers.

- Never update vendor banking details based on email alone. Call the vendor on a known number.

- Use callback verification for any new or changed payment instructions.

- Whitelist known recipients in your banking portal.

- Train your team to recognize urgency-based pressure tactics.

- Set up real-time alerts for every outgoing wire.

| Factor | ACH Transfer | Wire Transfer |

| Fraud type | Unauthorized ACH pulls | Wire fraud and BEC scams |

| Reversible? | Yes, within the dispute window | Usually no |

| Dispute window | Business: more than 24 hours | Very limited |

| Consumer protection | Stronger | Limited |

| Main risk | Account or routing misuse | Irrecoverable transfers |

5. International Payments: ACH vs Wire Transfer

(i) Can you use ACH for international payments?

Not really. ACH is a US-only network. International ACH Transfer technically exists but is rarely supported by most SMBs. For cross-border payments, ACH is not a real option.

(ii) SWIFT Wire for international payments

International wires use SWIFT. You need the recipient’s SWIFT/BIC code and IBAN. Transit often goes through intermediary banks, each potentially deducting a fee. Expect 1 to 5 business days for funds to arrive.

| Factor | ACH Transfer | Wire Transfer |

| International Support | Very limited | Widely Supported |

| Network used | ACH/IAT | SWIFT |

| Required Details | Limited international support | SWIFT/BIC/IBAN address |

| Processing time | Rarely used internationally | 1-5 business days |

| Intermediary bank fees | Rare | Common |

When to Use ACH and Wire Transfer?

You can use ACH when:

- You pay employees through payroll, direct deposit.

- recurring vendor or supplier payments.

- collecting customer payments or subscriptions.

- The amount is under $1 million.

- You have 1-3 business days of flexibility.

- Payment is within the US.

- You want the ability to reverse if something goes wrong.

You can use a wire transfer when:

- Payment must arrive the same day.

- Paying international vendors or contractors.

- Real estate closings or large asset purchases.

- The amount exceeds your bank’s ACH daily limit.

- The recipient specifically requires a wire.

- One-time, high-value transaction.

- Speed matters more than the transfer cost.

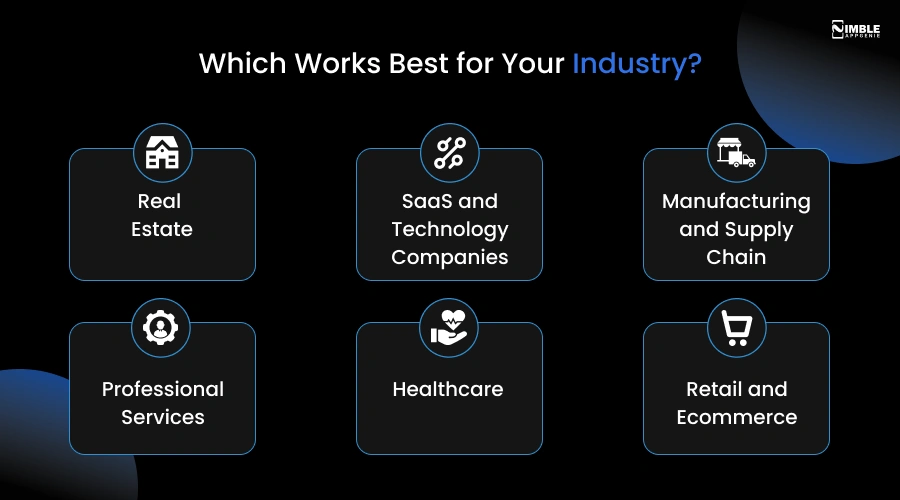

Which Works Best for Your Industry?

The right choice often depends on what your business does. Let’s take a look at the quick breakdown by industry.

1. Real Estate

You can use wire for closings, down payments, and escrow. These are large, time-sensitive, one-time transactions where the recipient typically requires a wire.

However, you can use ACH for collecting required rent from tenants or paying property management fees on a schedule.

2. SaaS and Technology Companies

Use ACH to collect subscription payments from customers and pay recurring vendor bills. For enterprise software deals with a large upfront license fee, a wire transfer is often the cleaner option. It is faster and expected by the recipient.

3. Manufacturing and Supply Chain

You can use ACH for domestic suppliers you pay on a regular schedule. But you can use wire for international suppliers who need payment in foreign currency or who need funds before shipping.

4. Professional Services

Law firms, accountants, and consultants often collect retainers via wire, especially for large client engagements. Recurring invoices and smaller fees are well-suited to ACH.

5. Healthcare

Insurance reimbursements and Medicare payments typically arrive via ACH. Payments between healthcare facilities or for equipment purchases often go through wire transfer.

6. Retail and E-commerce

Domestic vendor payments and supplier invoices work well with ACH. Overseas inventory purchases typically need international wire transfers or fintech alternatives.

ACH, Wire, RTP, and FedNow: The Four-Way Comparison

Two newer payment rails are becoming more widely available: Real-Time Payments and FedNow. They are worth knowing about if you are building transaction processing systems or evaluating future options.

What is RTP?

RTP is run by the clearing house. It processes payments instantly, 24 hours a day, 7 days a week, 365 days a year. Funds arrive in seconds, not hours or days. The per-transaction limit is $1 million.

What is FedNow?

FedNow is the Federal Reserve’s instant payment network, launched in 2023. It works similarly to RTP, offering real-time settlement around the clock. The current per-transaction limit is $500,000, though individual banks may set lower limits.

Neither RTP nor FedNow is universally available yet. Not all banks support them. But adoption is growing quickly.

| Feature | Standard ACH | Wire | KTP | FedNow |

| Speed | 1-3 business days | Same day (domestic) | Seconds | Seconds |

| Costs | $0.20-$1.50 | $15-$50 | $0.01-$0.05 | Low |

| Max per transaction | $1M (same-day) | No federal cap | $1M | $500K |

| 24/7 available? | No | No | Yes | Yes |

| International? | No | Yes | No | No |

| Reversible? | Yes (limited window) | No | No | No |

If your bank supports RTP or FedNow, it can be a compelling middle ground: wire-like speed at a cost closer to ACH. You can ask your bank whether these rails are available for your account type.

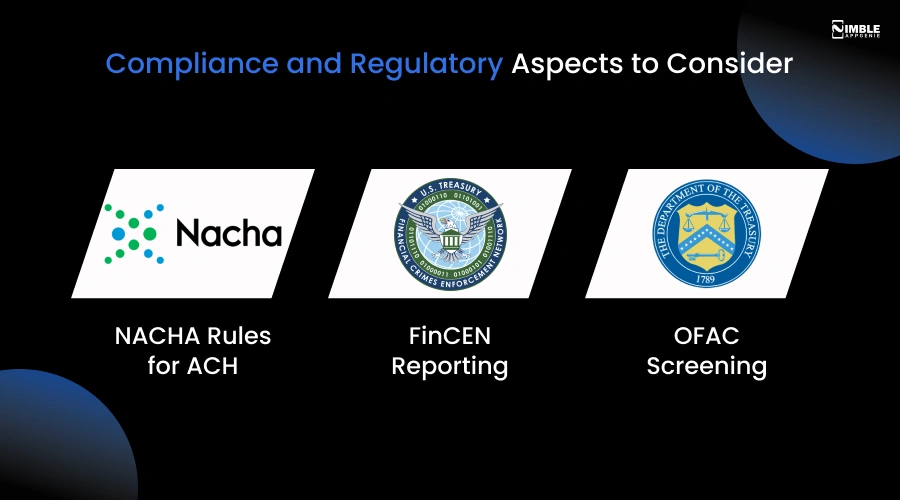

Compliance and Regulatory Aspects to Consider

Most businesses do not need to worry about fintech regulations and compliance until they do. Here is what to know in advance.

1. NACHA Rules for ACH

If your business originates ACH payments, you need a relationship with an Originating Depository Financial Institution.

That is typically your bank. Your bank is responsible for ensuring you comply with Nacha’s operating rules. It includes proper authorization from recipients before pulling funds.

2. FinCEN Reporting

Banks must file Currency Transaction Reports for cash transactions over $10,000. Wire transfers are not cash, so CTRs do not apply directly.

However, wire transfers above $3,000 require bank-level recordkeeping under the Bank Secrecy Act. Unusual patterns can trigger a Suspicious Activity Report.

3. OFAC Screening

Your bank screens every international wire against the OFAC sanctions list. If a name, entity, or country matches, the payment is blocked or delayed. This is why some international wires take longer than expected without a clear explanation.

How Nimble AppGenie Helps You Build Secure and Scalable Payment Systems?

If you are developing a mobile app or digital platform that manages payments, the choice between ACH and wire is not just a business decision. It is a technical architecture decision.

Getting it right from the start means fewer compliance issues, lower transaction costs, and a better experience for your users. As a fintech app development company, Nimble AppGenie creates and integrates payment systems for startups and growing businesses.

If your app needs to support ACH direct deposits, wire disbursements, subscription billing, or real-time payment rails like RTP and FedNow, we design the infrastructure to match your use case.

What Can We Help With?

- Choosing the right payment rail for your software solution

- Integrating payment APIs like Plaid, Stripe, Dwolla, JPMorgan, and others

- Building compliant payment flows with proper authorization and audit trails

- Designing fraud prevention controls into your payment architecture

- Structuring payment systems for fintech apps, marketplaces, and SaaS platforms

Nimble AppGenie helps you build a payment infrastructure that scales without requiring a full rebuild at the next stage.

Conclusion

ACH vs Wire transfers serve different purposes. They are not competing products, and they are tools for different jobs. Use ACH for routine, recurring, domestic payments where cost matters and you have a day or two. It is cheap, reversible, and built for volume.

Additionally, you can use wire when you need same-day delivery, the payment is international, the amount is very large, or the recipient specifically requires it. Just make sure your controls are in place before you hit send.

If your bank supports RTP or FedNow, it is worth asking about them. They offer wire-like speed at ACH-like costs, and adoption is growing fast. Most businesses will use both over time. The key is knowing which to reach for and when.

FAQs

Standard ACH takes 1 to 3 business days. Next-day ACH settles the following business day. Same-day ACH settles the same day if submitted before 4:45 PM ET.

Domestic wires typically arrive the same day, within a few hours of submission. International wires take 1 to 5 business days, depending on the destination and the number of intermediary banks involved.

No. ACH is a US-only network. International ACH Transfers technically exist but are rarely supported for most business use cases. For cross-border payments, use a wire transfer or a fintech alternative.

ACH is almost always the right choice for payroll. It is lower cost, supports recurring payments, and integrates with most payroll software. Wire transfers are not designed for high-volume recurring payments.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.