AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

In a nutshell:

- A peer-to-peer (P2P) lending application directly connects borrowers and lenders, eliminating the need for banks or traditional lending institutions.

- To learn how to create a p2p lending app, you have to understand the benefits provided by these platforms, like high return, low cost, and direct borrower-lender connection.

- The key features of a successful P2P lending app include loan listing with T&C, processing & sanction, interest calculator, etc., which help you master how to build a p2p lending app.

- Exploring the top lending platforms and seeing why they are best can be a successful roadmap to learn how to develop a p2p lending app.

- The strategic steps of creating a p2p lending app, from research & market analysis to app launch is the complete answer to how to create a p2p lending app.

- The cost to create a p2p lending app ranges from $20,000 to $250,000 or more, affected by several factors, including feature choice, technology cost, and others.

- The first step to create a P2P lending app is learning the process & understanding the right monetization strategies, which is what truly determines how the application makes money.

- Keeping up with trends and challenges of the p2p lending platform helps you to stay above the competitive curve and risk parameters.

- Delegating the p2p lending solution to Nimble AppGenie will be the best idea since they have industry expertise and best choice among others.

Direct lending applications have redefined the way people borrow money. Today, technology has made it possible for people to access funds at the convenience of their fingertips, all thanks to P2P lending apps.

The market for such applications has flourished over the past few years, making it a profitable business for financial institutions and individuals. Today, hundreds of applications are available in the market, creating room for more such apps as the market grows.

If you are wondering what these apps are and how you can develop one for your business, this is the post for you! In this one, we will take you through all the steps that you may need to take to create a successful P2P lending app.

Without further ado, let’s start by understanding Peer-to-Peer lending apps closely, what they are, and what benefits they offer.

What is a P2P Lending App and Why Invest in It?

A P2P or Peer-to-Peer lending application connects borrowers to lenders. What makes a P2P lending application different from traditional lending is that it does not depend on banks and lending institutions to enable digital borrowing.

This means that since there are no mandatory middlemen, banking institutions, brokers, etc. The interest rates on borrowing are comparatively lower, making the entire setup more enticing for the user.

Investing in one such application can prove to be a vital decision, as the market for such applications is growing exponentially. The ease of access that it provides to both individuals looking to lend and individuals looking to borrow is what makes these apps so popular.

The benefits of investing in a P2P lending application are :

► Rapid Growth Potential

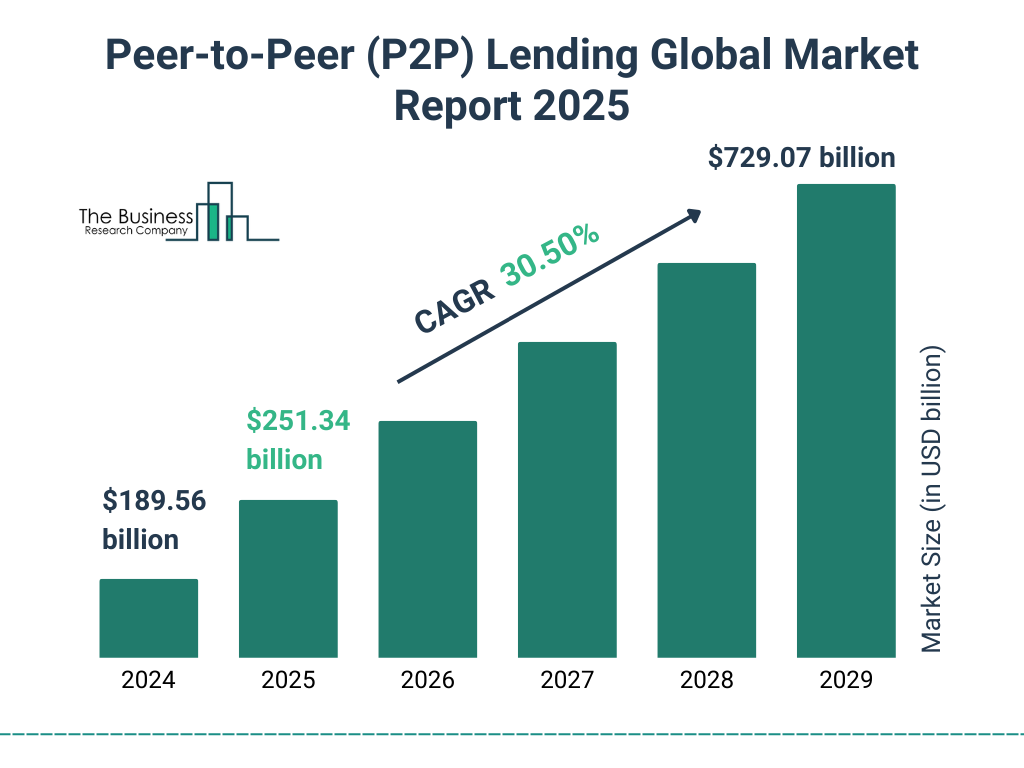

The peer-to-peer (P2P) lending market size has grown exponentially in recent years. The market will grow from $189.56 billion in 2024 to $251.34 billion in 2025 at a compound annual growth rate (CAGR) of 32.6%.

Since the market is growing significantly faster, it offers opportunities for rapid growth. Investing in a growing field can be beneficial in the years to come.

► Multiple Revenue Streams

A P2P lending application offers multiple revenue streams. While you have a primary income in the form of interest and commissions that both lenders and borrowers pay, you can utilize your application for more monetization options, like advertisements, additional services, etc. Helping you earn more from your P2P application.

► Wider Business Reach

One of the issues that traditional lending and banking businesses have faced in the past is limited reach. Thanks to a digital application, you can now reach a wider audience, maximizing your area of functioning.

The app offers exponential reach as it is available on a store and can be downloaded in any region the publisher wants.

► Opens New Business Paths

When you step into the peer-to-peer lending business, you are not only operating with lending but also opening doors to a whole new realm of financial services.

Gradually, with time, you can easily associate with other players in the fintech sector to introduce newer services on your application. Many businesses have done it already, and it clearly helps!

► Fewer Investments & More Profits

To start a P2P lending business, all you need is a digital platform. There’s no need for physical branches, ATM networks, or anything else. All you need to do is take care of the things that really matter, which is an optimized application and all the compliance and regulations.

Once your app is ready, deploy it, and your services will be live instantly! With improved technology right by your side, you can leave a mark by establishing your own P2P lending application.

The best part is that, unlike traditional banking and lending institutions, you need not worry about hiring a loan officer or providing a physical branch; it’s all digital! It is a step in the right direction to invest in a P2P lending application.

What are a few game-changing trends of the P2P lending app for 2026?

While P2P is a new concept altogether, it has seen a great evolution in terms of execution and user interests. Several trends are ready to change the way current P2P applications work.

These include :

- Use of IoT Devices for Ease of Access

- AI & ML Implementation for Insights

- Blockchain & Additional Security Technologies

- DeFi Integration for Expanded Opportunities

- Enhanced Risk Evaluation & Background Check

- AI-based chatbots and analytics.

AI in lending apps can be a game-changer, and the same goes for other technologies. Any cutting-edge peer-to-peer lending app will have these implemented in 2025.

You should always keep looking for the latest loan lending app trends, as these can help you stay ahead of the competition. You can always make the most of these trends when you have a team of expert developers always by your side to guide you with the best practices.

What are the key features of a successful P2P lending app?

Any application becomes popular due to the features that it offers. The same applies to a peer-to-peer lending application. You need to understand that the more convenience you offer through your application, the more people will use it.

However, since it is not a traditional banking app, many people are confused about the loan lending app features.

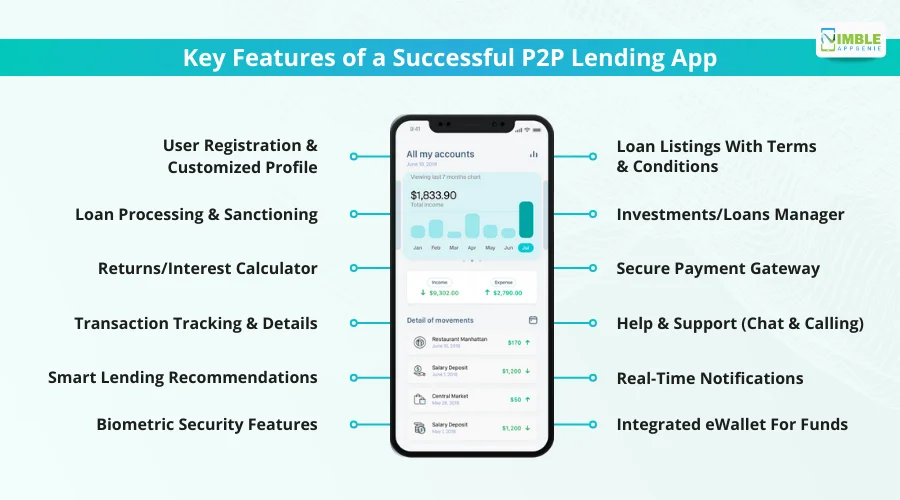

Here are a few must-have features of a P2P lending app to make it successful :

♦ User Registration & Customized Profile

Every peer-to-peer application should allow user registration and offer users the ability to customize their profiles. There should be different profiles for both borrowers and lenders, as they will have different data to access and different tools to manage their profiles.

♦ Loan Listings With Terms & Conditions

This is a vital feature that allows a borrower to search for loans available. Loan listings help in garnering the attention of the users. These listings should have an overview that appears in search lost and then must have a dedicated page that offers insights on the terms and conditions of the loan.

♦ Loan Processing & Sanctioning

Loan processing and sanctioning are mandatory features for any lending application. These features bring gamification in loan lending apps and help them appear more interactive to the user.

If you are a lender, you should be able to initiate and manage loan processing easily, and being a borrower, you should get crucial information such as an ETA of bank transfer, status of sanction, etc.

♦ Investments/Loans Manager

There should be a proper section in the app that offers management tools for investments and loans for each type of user.

A lender should be able to see a consolidated view of all the funds that they have invested yet, when will they recoup all of it, and how much is going to their profit throughout the time.

Similarly, for borrowers, it should show information on how many loans are currently open, what the repayment dates are, when these loans close, etc.

♦ Returns/Interest Calculator

A dedicated calculator that allows borrowers to identify how much interest they would have to pay on a particular amount could be a good integration into the app.

On the other hand, a returns calculator allows the lender to learn what type of profit they will make on lending a certain amount for a certain time at a particular interest rate. This makes the app more interactive and insightful.

♦ Secure Payment Gateway

Any application that involves lending, investments, and transactions must have an integrated payment gateway. This allows users, especially borrowers, to pay their outstanding debt directly from the application.

Sure, they can create a recurring payment directly from their account; however, in case they want to do it manually at any hour of the day, any day of the week, the payment gateway can be really helpful.

♦ Transaction Tracking & Details

Tracking transactions refers to monitoring the status of any transaction that you have made. In a P2P lending application, this feature is a basic necessity as both borrowers and lenders need to track where their money is.

Not to mention, it also maintains transparency and clarity about the transaction details between the two parties to ensure there is no confusion.

♦ Help & Support (Chat & Calling)

People often get restless when they do not get proper support and help in times of distress. In fintech, it is one of the biggest reasons why people tend to migrate from one app to another. Proper help and support, be it via chatbots or human associates, must have a dedicated help and support section that is available 24/7.

While these are the key features that every P2P lending application should offer, there are some advanced features that you can opt for when planning to develop a successful lending application.

♦ Smart Lending Recommendations

Lending recommendations to investors can be a game-changer. Whenever an individual applies for a loan, there should be a complete background check that runs automatically with AI & ML to let the lender know whether they should clear the loan or not. These smart recommendations will definitely help in optimizing the lending process.

♦ Real-Time Notifications

Notifications and alerts are definitely a crucial feature for any app; however, by making all these notifications real-time, you can enhance the experience of the user to a great extent.

Real-time notifications such as where exactly your application has reached, what the lender is currently doing, has he seen your request, is he actively processing the borrow request, if the lender is offline, etc.

♦ Biometric Security Features

Financial transactions and information about any individual are extremely sensitive information. Hence, offering biometric security services such as fingerprint to unlock or facial recognition to access a certain section of the application can take the security of your application to the next level.

♦ Integrated eWallet For Funds

Many people have a trust issue with connecting their bank accounts with a random application. You can reduce this problem completely with e-wallet development by offering an integrated e-wallet through which people can make their loan repayments easily.

This way, their banking details also stay intact, and they can use the application easily. With all these features powering your application, you can easily make it to the top of the business and attain the utmost profits.

However, the implementation of features matters a lot, which is also the reason why you should choose the best developers available in the market!

What are some of the top P2P lending platforms?

Success in peer-to-peer lending is not something that people have seen before. Several active platforms offering P2P lending services have been thriving in the industry, making new records and reaching new heights every day.

If you are planning to build a successful P2P lending app, there’s no harm in learning about your competition.

Here is a quick overview of the top P2P lending platforms :

1. Funding Circle

Based in the UK, Funding Circle is one of the best loan lending apps that offer loan opportunities to small businesses. It serves as a connecting platform between investors and businesses.

This way, small businesses can reach out to genuine investors for business loans at flexible rates and terms. This way, they reduce default risks as they have proper information on the businesses.

2. Prosper Funding

Founded in 2005, Prosper Funding has made a great name for itself in the peer-to-peer lending industry. It offers great flexibility to both lenders and borrowers, allowing investors to offer multiple small loans to different borrowers from the same profile.

What works for Prosper Funding is the community-driven approach that helps it create a personal connection with the users.

3. Dave

With its convenient features such as Extra Cash, Checking Account, and Side Hustle, Dave is a short-term lending application that allows borrowers to reach out to the investors in their area.

It is more of a local business that can help small and budding businesses to get funds when in need. With all these apps making waves in the market, the overall P2P lending has become more accessible for users.

While you might not have the first mover advantage in the field due to existing competitors, these apps open doors for new apps like yours.

Think about it, one of the core issues that first movers face is spreading awareness about the services and how they work.

But thanks to these apps, that will not be a problem for you. As far as the competition is concerned, you need not worry, as the market has a lot of users who are looking for something else.

That is where your app can help. All of these apps have their pros and cons. What you need to do is identify their gaps and fulfill them!

How to Develop a Successful P2P Lending App?

To develop a successful P2P lending app, you need to go through a series of steps that will help you create the appropriate solution. You will also need a Lending Software Development Company to back you up for the development process.

Here is the Process to develop a successful P2P Lending App :

➤ Research and Market Analysis

The first thing you need to do is identify the gaps in the market. For that, you need proper research and market analysis. Check out the existing apps, go through them, and try finding things that they do best and things they lack.

Understand the issues that people are facing and create a plan. Before entering any field, you should be familiar with how things work in that field. It is the first step, but it definitely lays the foundation for further steps.

➤ Identify the Features

Features are the backbone of any application. Through your research, you will come across several features that are common to all the apps. You can innovate in choosing the features, as it will also help you create a unique value proposition for your application.

Offering features that no one else in the market offers gives you an edge. However, you have to be smart and evaluate whether the feature you plan to add is financially feasible, follows all the compliance requirements, and, most importantly, is helpful for the user.

➤ Choosing a Tech Stack

In this step, you need to decide what type of technologies will power your application. Technologies that are combined to create an application are called its tech stack.

Choosing a loan lending app tech stack becomes easier when you have experienced developers to help you out. Listing features in the previous step also comes in handy as you now have a vision of what features you want to implement and can select technologies accordingly.

There are 4 components for which you have to choose technologies. These are :

- Front-End: This component requires designing technologies as it refers to the entire user interface and experience of the user.

- Back-End: This is where all your processing is done. Functionalities are defined in the backend so that everything can be connected.

- Database: You need a database system to store everything from user data to the information generated during app usage.

- APIs: These are added features that you can simply integrate in your application without having to build them from scratch.

➤ Designing the App

Once you have decided on the tech stack, all your groundwork is done. Now, what you have to do is give shape to your vision by deciding on the design of your application.

The development company you have hired will help you identify the perfect balance between functionality and aesthetics of your app, making it a good experience for the user, without having to suffer in finding crucial features.

A well-designed application is something that can help you garner a lot of attention, hence ensure you pay attention to this step.

➤ Developing Functionalities

After the design is chosen, let the developers work on developing the functionalities that you have chosen. Implementing all the features that you have thought of will take time, as it is definitely not easy. Task.

If you have professional developers with experience in P2P app development, you can expect the process to be over soon; however, keep in mind that this is going to be the most time-consuming step of the development process, and hence, you should not rush it, as it may hamper the usability of your application.

➤ Testing & Compliances

Compliance and regulations are important to take care of while developing a peer-to-peer lending application.

When the development process is over, you need to check that the application is compliant and follows all the guidelines and regulations. After making all the checks, it’s time to run all the functionalities of the application and test it in all environments.

You need a team of quality assurance professionals who can check your app for several use cases, identify the mistakes to avoid while developing a loan lending app, and ensure that the final application is free of bugs.

➤ Deployment, Support & Maintenance

Once your application is developed and free of all bugs, you can prepare for deployment. The deployment process requires you to meet the guidelines of the stores where you have to publish the application for people to access.

After deploying, you have to stay active in managing the application. As more and more people are using it is important to ensure that the quality of the user experience does not deteriorate.

Maintenance and support are crucial to maintain a bug-free environment for your application. Once you are through all the steps, you will have a well-designed P2P lending application with you, ready to market.

Keep in mind that since this is a lending application, you should try and close a few lenders to fund the application in the beginning. Once you have closed the investments, the app is ready to provide the services.

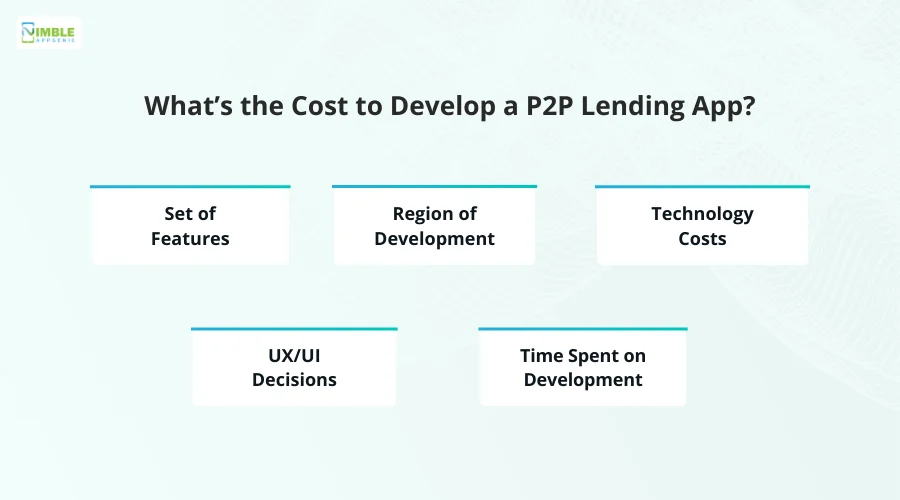

What’s the Cost to Develop a P2P Lending App?

To develop a P2P lending application, you need to have a proper budget allocation. Since this is a lending application, you will need funds to start the lending process on your application; however, we will not be counting that cost into the development process.

Depending on your pro, the application development process can cost you anywhere from $20,000 to $250,000 and more. The range is determined based on several factors.

These factors include :

• Set of Features

The features you select can affect the cost of development as not every feature can be executed on a specific budget. Some may prove to be costlier to implement.

• Region of Development

The region where the development team you hire exists also has an impact on the cost of development, as the per-hour rates vary from region to region. The cost may be less in the Asian regio,n whereas if you go towards Europe, you will have to pay more!

• Technology Costs

Technologies are not cheap to implement. You need professional help to implement a functionality, and when it comes to tech, there has to be a field expert. Also, the resources required to implement technologies like machines, computing power, etc., are expensive!

• UX/UI Decisions

The type of user interface/ user experience you choose is also a factor that must be considered while deciding on the cost to develop a loan lending app. The more complicated a design is to execute, the higher the cost!

• Time Spent on Development

When you are paying experts based on the number of hours they have worked, the time spent on development is definitely going to be a key player.

Sure, there has to be a set timeline that you decide on; however, this too should be decided beforehand. These factors determine the ultimate cost of your development process. You can try several development services to get an idea.

The complexity of the application is another crucial factor, as you need to decide whether you are going to opt for a basic application or a high-complexity advanced app that will automatically take more time, costing you more.

How Do P2P Lending Apps Make Money?

Peer-to-peer lending applications are a great way to make money as they offer so many options for monetization. Some of the ways P2P lending apps make money include-

1. In-App Purchases

By offering additional features like credit score checkers, expedited help, etc.

2. Advertisements

By allowing other similar apps to advertise on your application.

3. Subscriptions

You can create a premium subscription offering an ad-free experience with additional advanced features.

4. Origination Fees

When offering money lending services, you can charge an origination fee that helps you cover the entire process. It is also called a processing fee.

5. Service Fees & Penalties

These are regular fees your platform can charge when offering a sort of transactional service. Platforms can also add penalties when a transaction is delayed by the user, making it an added income.

With all of these streams of revenue, P2P applications are one of the best ways to make money in 2026. Even proper financial institutions have gone the digital route by creating applications that offer loans.

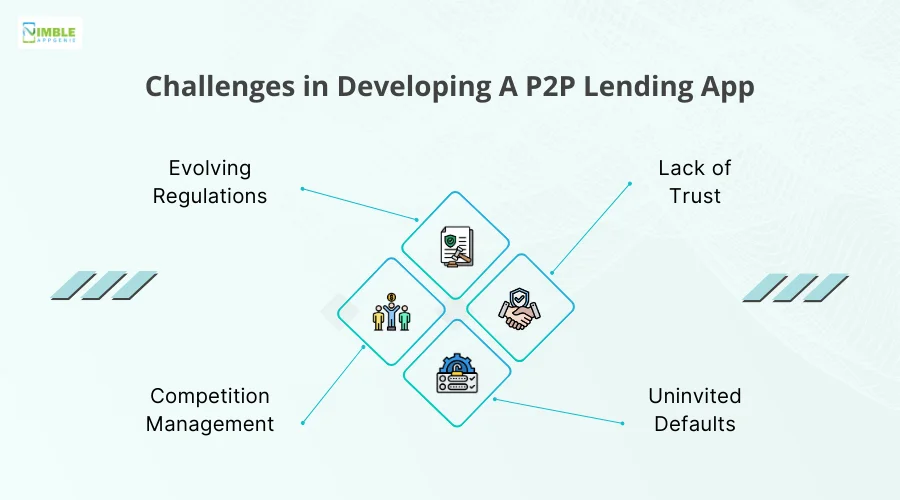

What are the development challenges of a P2P Lending app?

When you plan to develop a loan lending app, several risks come along with it. These risks often have to do with the business aspects; however, challenges in developing a P2P money lending app are also something that you should consider.

These challenges include :

➤ Evolving Regulations

If you are planning a platform that offers financial services of any sort, there are many strict requirements that you have to fulfill else your application is always at risk of being removed from the store or being blacklisted by the government. The real issue here is that these regulations can change at any time, which means you have to stay diligent.

➤ Lack of Trust

When you do not have a physical presence, it can become extremely difficult for a user to trust you with money matters. To convert an individual into a user, you have to generate trust among them, which can be a huge challenge.

While already existing apps have defined how things work, several users still find it difficult to trust an online platform for lending and borrowing money.

➤ Competition Management

With so many people eyeing the growing market for peer-to-peer money lending, competition has grown fiercely in the past few years. Hence, you may find it challenging to manage the competition and emerge in the crowded market.

You have to pay attention to your app features and spend more on marketing as the challenge of visibility is something that haunts a lot of businesses.

➤ Uninvited Defaults

In every money-lending application, the most common issue is payment defaults by the borrower. This happens because P2P lending platforms do not require any sort of collateral.

Now this challenge can only be managed with proper risk analysis and thorough creditworthiness checking. However, minimizing defaults is something every app, new or old, has struggled with.

To be ahead of all these challenges, you need to ensure that you are using the latest technologies and work on creating a community so that if something goes south, you have a community that trusts you and aligns with you!

Why Choose Nimble AppGenie For Your P2P Lending App?

After learning everything about how these applications work and the opportunities that Peer-to-Peer lending apps offer, you might have made up your mind on whether you want to create your own application. And if you plan to go for P2P lending platform development services, then Nimble AppGenie is hands down the best option you have!

We offer expert fintech app development services that not only help in the development of the app but also make it their priority to guide you through various details about the industry.

Since the education about how P2P lending works is relatively less, it is really crucial that you delegate the development to someone who has already worked on a similar project.

Reach out today to get more insights on how you can turn your idea into a full-fledged, profitable peer-to-peer money lending mobile app!

Conclusion

We hope that this post has provided you with ample insights on how to create a successful P2P lending application. The idea of enabling individuals to borrow and lend from each other while regulating the entire process through a digital platform is truly remarkable and offers a great opportunity for generating profits.

Sure, there are several things that you have to take care of when developing the app; however, with proper guidance and expert developers, everything can be done successfully. As far as the future of these apps is concerned, it seems that they are going to change the way lending works completely.

With new technologies like AI, ML, IoT, and Blockchain, all the transactions on the applications are set to become more efficient, convenient, and secure.

FAQs

Technologies that usually power a Peer-to-Peer lending app include –

1. For iOS: Swift 5, UIKit, MVVM+C,

2. For Android: Kotlin, Android Studio/Eclipse,

3. For Admin Panel: Node.js, React,

4. Payment Gateway: Stripe, PayPal

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.