AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

TL;DR

- Embedded banking platform development cost typically falls between $50,000 and $250,000+, depending on features, compliance, and integration depth.

- A basic MVP with core accounts and cards starts around $50K–$90K. Mid-level platforms with lending or multi-currency support run $90K–$160K. Enterprise-grade platforms with full compliance stacks cost $160K–$250K+.

- The biggest cost drivers are BaaS/sponsor bank integration, KYC/AML compliance, card issuing, and security architecture- not the app screens.

- Buying (partnering with a BaaS provider) is cheaper and faster than building from scratch with a full banking license.

- Ongoing costs (compliance, maintenance, partner fees) add 15%–20% of the build cost every year.

- Nimble AppGenie helps fintech founders scope, budget, and build embedded banking features without overpaying for capabilities they don’t need; get a free cost estimate before you commit a budget.

Embedded banking platform development cost is generally the first question founders ask and the hardest one to get a straight answer for. Search results range from $8,000 to $1 million, which is not practical when you are trying to build a budget or pitch to a CFO.

This guide breaks the cost down by feature, hidden expense, and tier, using real 2026 pricing data, so you can know exactly what you are budgeting for before you talk to a development partner. Understanding this cost range is the first real step toward evaluating embedded banking for businesses of any size, not just large enterprises.

If you are comparing this against a general fintech app development cost guide, embedded banking is on the higher end because of compliance work and licensing, not because the app itself is more complex to design.

What Is an Embedded Banking Platform?

An embedded banking platform allows a non-bank business – a SaaS tool, app, or marketplace- to offer real banking features like cards, accounts, and payments inside its own product. The business doesn’t become a bank.

It partners with a Banking-as-a-Service (BaaS) provider and licensed bank, which manages the regulatory side, while the business owns the user experience. Lyft Direct and Shopify Balance are well-known examples of this model in action. This is one branch of the broader embedded finance category, which also covers lending and insurance.

This is one branch of the broader embedded finance platform development category, which also covers embedded insurance and embedded lending; read the full breakdown there if you are still deciding where to start.

Embedded Banking for Businesses: Is It Worth the Investment?

A 2025 Green Dot/PYMNTS survey of 515 senior decision-makers found 94% of enterprises plan to increase their embedded finance investments, with banking (80%) and payments (72%) as the top priorities, ahead of payroll and investing features.

McKinsey projects that by 2030, embedded finance could account for 10–15% of total bank revenues – proof this is not a niche experiment anymore.

Embedded Banking Platform Development Cost – Quick Breakdown

Here is the range, broken into three build tiers. These figures assume you are working with a development partner and a BaaS provider, not applying for your own banking license (that adds significantly more cost and time).

| Development Stage | Estimated Cost | Key Features | Timeline |

| MVP / Starter | $50,000 – $90,000 | Digital accounts, virtual cards, basic KYC, single-currency support, simple dashboard | 3–5 Months |

| Mid-Level | $90,000 – $160,000 | Physical and virtual cards, multi-currency accounts, lending or instant payouts, advanced KYC/AML, analytics | 5–8 Months |

| Enterprise-Grade | $160,000 – $250,000+ | Full compliance stack, fraud detection, multi-market support, custom orchestration layer, dedicated infrastructure | 9–14+ Months |

Embedded Banking Examples

A few real embedded banking examples show how this works in practice:

- Shopify Balance gives merchants business accounts and faster payouts.

- Lyft Direct gives drivers instant-pay bank accounts and debit cards.

- Square Checking lets merchants bank directly through their point-of-sale system.

Each of these is built on a BaaS partner rather than a custom banking license.

Cost By Feature

Instead of one lump number, below is a rough sketch of what each core feature adds to your budget:

Feature Line-Item Estimate

| Feature / Module | Estimated Cost |

| Digital Account Creation + KYC | $15,000–$30,000 |

| Virtual Card Issuing | $10,000–$25,000 |

| Physical Card Issuing + Fulfillment | $20,000–$40,000 |

| ACH / Wire Transfer Integration | $15,000–$35,000 |

| Lending / Instant Payouts Module | $25,000–$60,000 |

| Fraud Detection + Risk Scoring | $20,000–$50,000 |

| Compliance Layer (PCI-DSS, SOC 2, AML) | $20,000–$45,000 |

Building a lending module specifically? See the full loan lending app development cost breakdown.

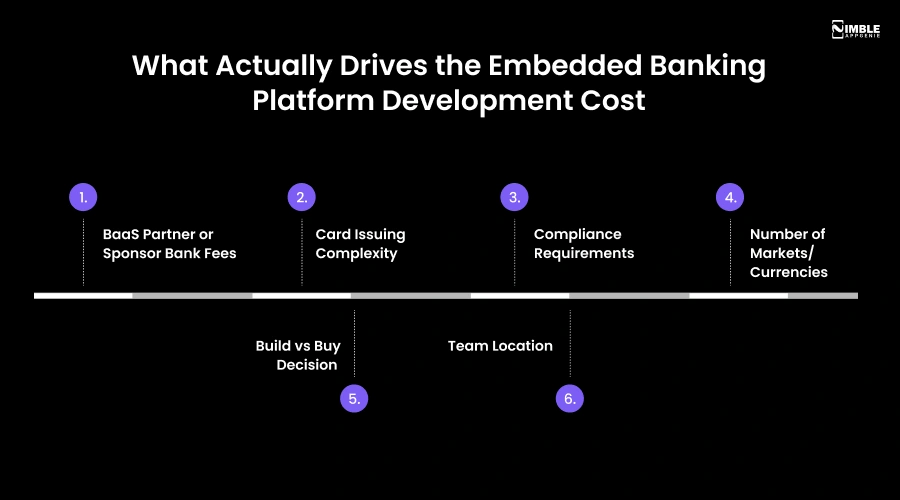

What Actually Drives the Embedded Banking Platform Development Cost

Most quotes vary so much because they are based on different assumptions. These are the real variables:

1. BaaS Partner or Sponsor Bank Fees

You will pay setup and per-transaction fees to whichever bank or BaaS provider handles the regulated edge (Stripe, Unit, Solaris, Treasury, etc.). This is not part of the development cost, but it impacts your total budget.

2. Card Issuing Complexity

Virtual cards are cheap to add. Physical cards involve manufacturing, shipping, and fulfillment partners, which increase costs and timeline.

3. Compliance Requirements

KYC, AML, PCI-DSS, and regional regulations (like PSD2 in Europe) all need dedicated engineering and legal review time.

4. Number of Markets/Currencies

Every new currency and country adds new compliance checks, localization work, and banking rails.

5. Build vs Buy Decision

Building your own licensed infrastructure is far more costly than integrating a BaaS provider’s API. Most startups should not try a full in-house banking license.

6. Team Location

Western Europe: $45–$80/hour; North American teams: $50–$90/hour; and Eastern Europe or Asia-based teams: $25–$50/hour, for similar output.

Your tech stack choice also affects long-term cost; see our finance tech stack guide for what a compliant, scalable stack looks like.

Build vs Buy: The Real Cost Comparison

| Approach | Upfront Cost | Time to Launch | Best For |

| Build in-house (own license) | $500,000+ | 12–24+ months | Large enterprises with regulatory teams already in place |

| Buy / Partner with BaaS provider | $50,000–$250,000 | 3–9 months | Startups, SaaS platforms, marketplaces – most businesses |

For 90% of businesses exploring embedded banking, partnering with a BaaS provider and hiring a development team to build the front-end and integration layer is the financially smarter path.

Hidden Costs Nobody Tells You About

Most cost guides uncover only the build price of an embedded banking platform.

Here, we will show you what hits your budget after launch:

- Ongoing Maintenance: 15%–20% of your initial build cost, every year, for security patches and updates.

- Compliance Audits: Annual security and regulatory audits (PCI-DSS, SOC 2) usually cost $10,000-$30,000 a year.

- Customer Support Infrastructure: Financial products need faster, more careful support than typical SaaS features – factor in staffing.

- BaaS/Partner Transaction Fees: Per-card, per-account, and per-transaction fees from your banking partner scale with usage.

- Fraud Losses: Even with detection systems, budget a small reserve for fraud-related losses in year one.

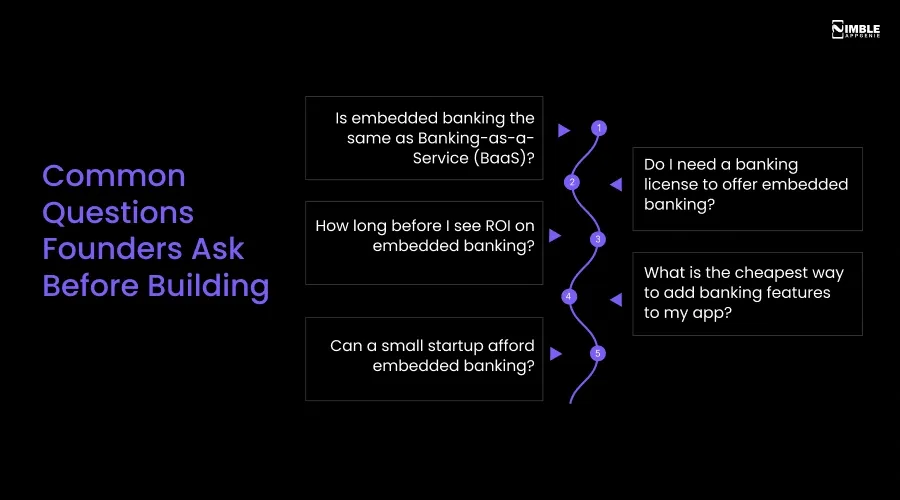

Common Questions Founders Ask Before Building

These are the questions that come up most often when founders research embedded banking costs:

- “Is embedded banking the same as Banking-as-a-Service (BaaS)?”

Not exactly. BaaS is the infrastructure/licensing layer. Embedded banking is the result – banking features inside your app, often built on top of a BaaS provider.

- “Do I need a banking license to offer embedded banking?”

No. Most businesses partner with a licensed bank or BaaS provider instead of getting their own license.

- “How long before I see ROI on embedded banking?”

Most platforms see revenue (interest, interchange, or subscription upgrades) within 6-12 months of launch, depending on user adoption.

- “What is the cheapest way to add banking features to my app?”

Integrating an existing BaaS provider’s APIs (like Unit or Stripe Treasury) instead of building custom infrastructure or applying for a license.

- “Can a small startup afford embedded banking?”

Yes – an MVP-tier build starting around $50K makes this accessible to funded startups, not only large enterprises. Compare this to what it costs to build a neobank app like Monzo or an app like SoFi for reference points.

How to Reduce Cost Without Cutting Corners

- Start with an MVP: Launch core accounts and cards first, add lending or multi-currency later.

- Choose a BaaS partner with strong pre-built compliance tooling instead of building KYC/AML from scratch.

- Work with a development team experienced in fintech – inexperienced teams underestimate compliance work, which causes budget overruns. Plan your platform’s maintenance costs in your first-year budget, not as a surprise later.

Why Build Your Embedded Banking Platform With Nimble AppGenie

Nimble AppGenie is a fintech app development company that has worked on 350+ projects, including digital banking apps, eWallets, and embedded finance integrations. The team builds on proven BaaS integration instead of reinventing compliance infrastructure, which keeps client costs closer to the lower end of the range in this guide.

Explore the comprehensive fintech software development services page to see the banking, eWallet, and neobank work behind these numbers.

Conclusion

Embedded banking platform development cost is not a single number – it depends on how much compliance you need, which features you build, and whether you build or partner with a BaaS provider.

For most businesses, a $50K–$160K MVP-to-mid-tier build, supported by a proven BaaS partner, is the realistic and profitable starting point. Skipping the guesswork now saves you from budget overruns later.

If you are ready to move from research to a real project plan, Nimble AppGenie can scope your embedded banking platform and give you an accurate cost estimate based on your product – not an industry average.

Get in Touch for a Free Consultation

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.