Banking Software Development

Banking Software Development Payroll Software Development

Payroll Software Development Our Work Process

Our Work Process Awards

Awards

Key Takeaways:

- An AI-powered loan underwriting platform reviews credit data, financial documents, and risk signals, then approves, rejects, or flags a loan automatically.

- The process to make an AI-powered loan underwriting platform is to define the underwriting policy, gather and organize data, pick AI models, build document processing, build the decision engine, integrate with existing systems, then launch.

- The features of the AI-based loan underwriting platform are data ingestion, document processing, AI risk scoring, a decision engine, and a compliance layer.

- The cost to develop an AI loan underwriting platform starts from $30,000 to $250,000+, based on features, data sources, and compliance scope.

- Regulatory compliance like ECOA, Fair Lending, and GDPR need to be part of the design from day one, not added later.

- The challenges to build an AI loan underwriting solution are poor data quality, integration with legacy loan origination systems, model and explainability, unclear regulations across regions, shortage of in-house AI talent.

- Nimble AppGenie delivers AI underwriting platforms for lenders and fintechs, with compliance-ready architecture and integration support for existing loan systems.

Loan underwriting sits at the heart of every lending business. Whether you are a fintech startup, CTO, COO, NBFC, digital lender, or financial institution, your ability to assess risk directly impacts profitability, customer experience, and regulatory compliance.

The problem is that traditional underwriting was not built for today’s lending environment. Manual reviews slow approvals, increase operating costs, and make it difficult to scale. At the same time, borrowers expect faster decisions and more personalized experiences.

This is why lenders are increasingly planning to build an AI-powered loan underwriting platform. These platforms combine machine learning, automation, data analytics, and business rules to help lenders make faster and more accurate decisions while maintaining compliance.

Automated underwriting speeds up approvals by up to 60-70% and reduces operational costs by 30-40%.

But how do you create an AI-powered loan underwriting platform? It starts with understanding why lending businesses need one in the first place.

This guide walks you through the process of an AI-powered underwriting platform development, key features, development costs, and implementation challenges.

What is an AI-Powered Loan Underwriting Platform?

An AI-powered loan underwriting platform is a solution that uses AI to read a borrower’s financial data and recommend a lending decision.

It checks credit reports, bank statements, income records, and sometimes alternative data like rent payments, then scores the applicant’s risk in seconds. It does not replace your underwriting team.

Most lenders still want a person reviewing edge cases, large loans, or anything the model flags as unusual. An AI in a lending platform like this manages repetitive applications, so your team can spend time on the ones that actually need judgment.

Why Is Traditional Underwriting No Longer Enough?

Traditional underwriting struggles because it is too slow and inconsistent for current loan volumes. Research found that underwriters spend 30 to 40% of their time on admin tasks instead of actual risk review. That time adds up on every single file.

The cost shows up in the numbers too. Freddie Mac’s 2024 cost to originate study found lenders with high technology use close loans in about 34 days.

Across the industry, the average cost to originate one loan has climbed to roughly $11,600, up 35% over the past three years. Borrowers notice the wait, and they have other places to go.

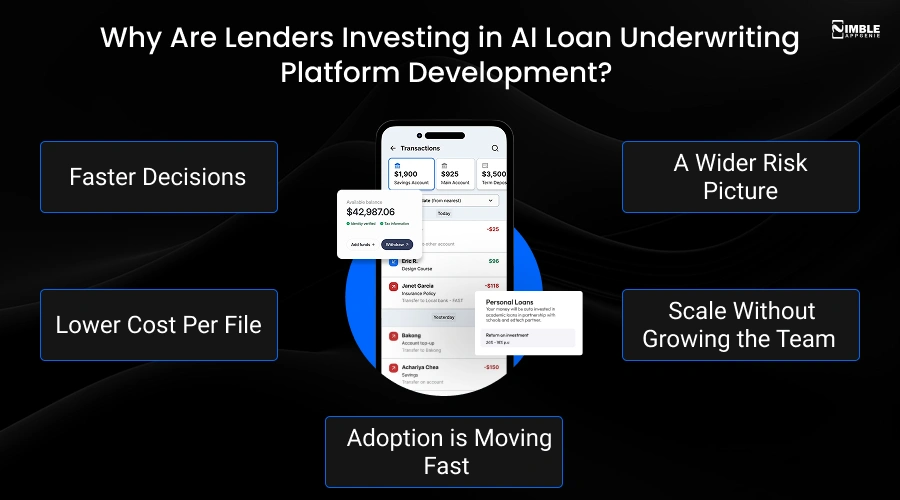

Why Are Lenders Investing in AI Loan Underwriting Platform Development?

Lenders invest in AI loan underwriting platform development because it removes approval times, lowers the cost per loan, and widens the data used to judge risk.

These benefits also support businesses looking to develop a loan app with faster and more accurate lending decisions. A 2024 survey found 60% of financial institutions saw measurable cost reductions and productivity gains after putting AI into their operations.

1. Faster Decisions

It improves decision speed. Applications that previously took days can often be reviewed within minutes.

2. Lower Cost Per File

It reduces operational costs by automating routine checks and document reviews. Less manual review means fewer hours billed to every application.

3. A Wider Risk Picture

It improves risk assessment. AI models can evaluate a broader range of variables than traditional scoring approaches.

4. Scale Without Growing the Team

It helps organizations scale without hiring large underwriting teams. The bank data, cash flow, and alternative data sources fill gaps a credit score alone misses.

5. Adoption is Moving Fast

AI loan underwriting can boost borrower experiences by reducing delays and increasing transparency. Competitors who have not started yet will soon.

Key Features of AI-Powered Loan Underwriting Platform Development

A high-performing AI loan underwriting platform needs features that are mentioned below. These features work together to create a streamlined underwriting workflow that supports operational efficiency, security, and compliance for digital lending platforms.

| Feature | What It Does |

| AI-Based Risk Assessment | Reviews a borrower’s financial information and credit history to estimate the risk of lending. |

| Automated Loan Decisions | Helps lenders approve, reject, or review loan applications much faster. |

| Alternative Data Analysis | Look at additional data, such as utility payments or bank transactions, to assess borrowers with limited credit history. |

| Real-Time Credit Checks | Instantly evaluates creditworthiness during the application process. |

| Income and Employment Verification | Confirms a borrower’s income and employment details automatically. |

| Smart Document Processing | Reads and extracts information from documents like bank statements, IDs, and payslips. |

| Advanced KYC and Fraud Detection | It provides the security layers necessary to build payday loan software that prevents identity theft and loan default. |

| Compliance Management | Helps lenders follow industry regulations and internal lending policies. |

| Predictive Risk Analysis | Uses past data to estimate the likelihood of loan repayment. |

| Custom Lending Rules | Allows lenders to set their own approval criteria and risk policies. |

| Explainable AI Decisions | Shows the reasons behind loan approval or rejection decisions. |

| Credit Bureau Integration | Pulls credit reports and scores directly from credit bureaus. |

| Bank Account Verification | Verifies account details and reviews transaction history when needed. |

| Risk-Based Loan Pricing | Suggests suitable interest rates based on the borrower’s risk profile. |

| Workflow Automation | Automates repetitive underwriting tasks and reduces manual work. |

| Portfolio Risk Monitoring | Tracks loan performance and identifies potential risks across the loan portfolio. |

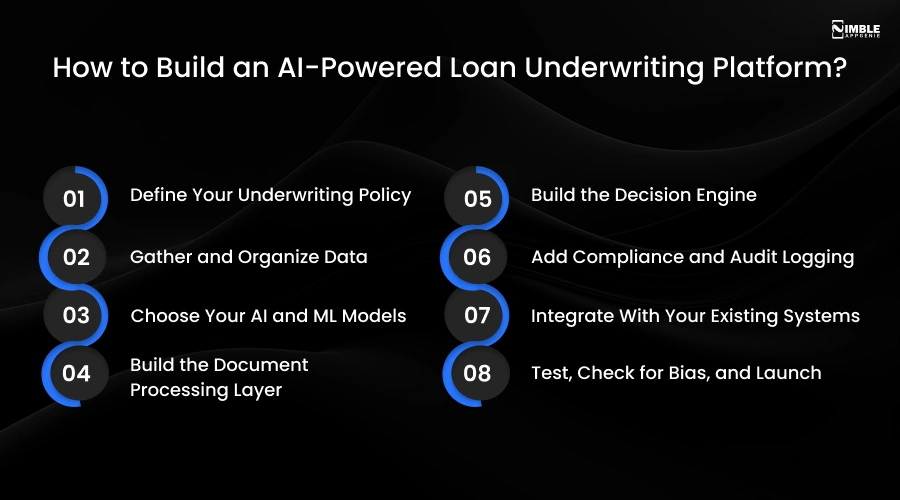

How to Build an AI-Powered Loan Underwriting Platform?

To develop an AI-powered loan underwriting platform, it takes eight stages: define your underwriting policy, gather and organize your data, pick your AI models, build document processing, build the decision engine, add compliance logging, integrate with your existing systems, then test and launch.

Now, let’s understand the AI loan underwriting platform development process.

Step 1: Define Your Underwriting Policy

First of all, write down your current lending rules. What credit score do you accept? What debt-to-income ratio is too risky? And what documents do you ask borrowers for? Write all of it down, even if it feels obvious. This list becomes the rulebook your AI will follow.

If you skip this step, your AI has nothing to measure against. Most underwriting projects that go off track later missed this step at the start.

Step 2: Gather and Organize Data

Next, gather all the data you will use, like credit reports, bank statements, payroll slips, tax returns, and anything else, like rent or utility payments. Then clean it up. Old loan files are messy. Fields are missing, entries are duplicated, and formats do not match.

This part feels boring, but it matters more than people think. AI models trained on messy data make messy decisions, so this stage takes longer than most teams expect. If your historical loan data has gaps or errors, fix that before model training starts.

Step 3: Choose Your AI and ML Models

Now choose the AI models that will actually score risk. For most lenders, a simple model like logistic regression works well, because it is easy to explain to a regulator, and that matters a lot in lending. For trickier risk patterns, a model like XGBoost can help.

You might also add a separate model for spotting fraud and one for reading documents. One rule to remember: if a model cannot explain why it made a decision, do not use it. Regulators and customers will both ask why.

Step 4: Build the Document Processing Layer

This step to build an AI-powered loan underwriting platform is about getting rid of manual data entry. You will build a system that reads uploaded files and turns them into numbers and text your platform can use.

Tools like AWS Textract, Google Document AI, or custom-trained models handle this, so you do not need to build this from scratch. Once it is working, nobody on your team should ever need to copy numbers from a PDF into a spreadsheet again.

Step 5: Build the Decision Engine

The decision engine combines your AI risk score with your rules engine. For example, the AI model gives a risk score of 720, but your policy says anyone below 650 is auto-rejected and anyone between 650 and 700 needs manual review.

The decision engine runs that logic and returns one of three outcomes: approve, decline, or send to an underwriter for a closer look.

Step 6: Add Compliance and Audit Logging

Every decision needs a record of what data was used, what score came out, and why the system decided what it did. In the US, the Equal Credit Opportunity Act requires lenders to give applicants a specific reason for denial, not a vague rejection message.

You should build this logging in from day one. Also, if you add it after launch, it is expensive, and regulators will ask for it eventually.

Step 7: Integrate With Your Existing Systems

Your AI-powered loan underwriting platform needs to talk to your loan origination software, core banking platform, credit bureaus, and bank data providers like Plaid or MX.

The development team can use APIs for these connections. If you are working with legacy systems, this integration step often takes longer than building the AI itself, so plan for it.

Step 8: Test, Check for Bias, and Launch

Before going live, test the model on old loan files and see how its decisions compare to what really happened. Also check for biases that ensure approval rates do not differ unfairly between groups of people.

Once that is done, launch with a small batch of applications first, not your whole pipeline. Watch how it performs closely, and keep retraining the model as real data comes in. Launch is not the finish line; it’s really just the start of monitoring.

What Tech Stack Do You Need for an AI-Powered Loan Underwriting Platform Development?

To build an AI-powered loan underwriting platform, you need technologies that support credit assessment, risk analysis, automation, and compliance. The following loan lending tech stack is commonly used for developing AI-driven underwriting platforms.

| Layer | Common Tools and Technologies |

| Backend and AI | Python, Java, Node.js |

| Risk scoring models | XGBoost, scikit-learn, TensorFlow, PyTorch, logistic regression |

| Document processing (IDP/OCR) | AWS Textract, Google Document AI, Azure Form Recognizer |

| LLM layer | Claude or GPT-based models for document summaries and decision explanations |

| Data storage | PostgreSQL, Snowflake, MongoDB |

| Bank data integration | Plaid, MX, Yodlee |

| Credit bureau APIs | Experian, Equifax, TransUnion |

| Frontend | React, Angular, Vue.js |

| Data pipelines | Apache Kafka, Airflow |

| Cloud infrastructure | AWS, Microsoft Azure, Google Cloud |

| Security and compliance | AES-256 encryption, audit logging, and role-based access control |

Including the right finance tech stack can help you to cover the optimized technologies used to build an AI loan underwriting platform. Now, without evaluating the right cost, you cannot frame the budget.

Hence, let’s get into the next section.

How Much Does It Cost to Build an AI Loan Underwriting Platform?

The cost to develop an AI-powered loan underwriting platform typically is between $30,000-$250,000 or more. An MVP with basic AI scoring and document processing costs less.

However, if you want a mid-tier platform with alternative data, fraud detection, and LOS integration can be higher. But if you want an enterprise platform with multi-jurisdiction compliance and full automated mortgage software development can exceed $250,000.

The table below showcases the breakdown of the cost to build an AI-powered loan underwriting platform.

| Tier | What’s Included | Estimated Cost |

| MVP | Basic AI credit scoring, simple document upload, manual review for edge cases | $30,000 – $80,000 |

| Mid-tier | Alternative data, fraud detection, automated decisioning, LOS integration | $80,000-$180,000 |

| Enterprise | Multi-jurisdiction compliance, full automation, advanced fraud and bias monitoring, custom model training | $180,000-$250,000 |

What pushes the number up is not usually the AI model itself. It’s the number of integrations, the compliance scope for your region, and how much of your current system you need to work around.

Most startups begin at the MVP tier and add features once they have real usage data to act on. You can also start with MVP development and then gradually build the full AI automated platform to reduce the AI-Powered loan underwriting platform development cost.

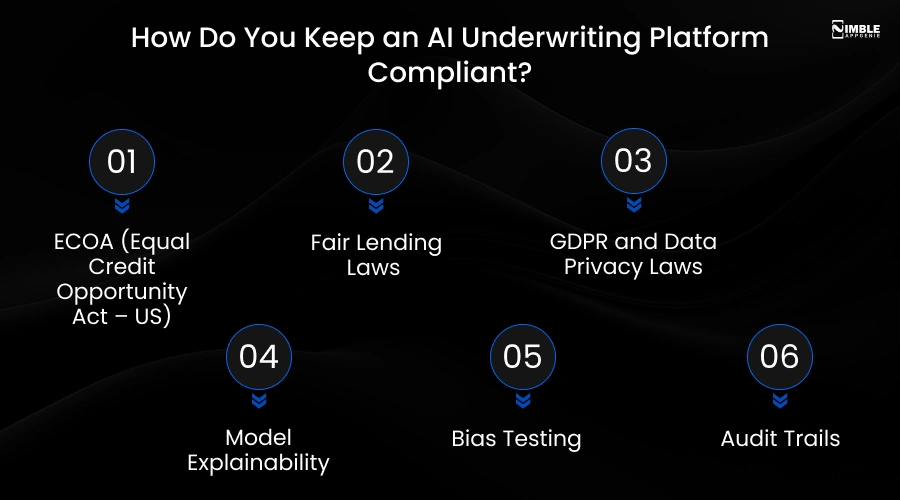

How Do You Keep an AI Underwriting Platform Compliant?

To keep an AI underwriting platform compliant, you need to follow fair lending and anti-discrimination laws, give applicants a specific reason for any denial, protect personal data under privacy laws like GDPR, and keep an audit trail of every decision and model version used.

Let’s check out the compliance requirements before you build an AI-powered loan underwriting platform.

1. ECOA (Equal Credit Opportunity Act – US)

Under ECOA, lenders must provide a clear reason when a loan application is rejected. They cannot simply say that an AI system made the decision. Borrowers should understand which factors affected the outcome so the process remains transparent and fair.

2. Fair Lending Laws

AI underwriting models must treat all applicants fairly and avoid discrimination based on race, gender, age, disability, or other protected characteristics. Regular monitoring is important to ensure the system does not unintentionally create unfair lending decisions.

3. GDPR and Data Privacy Laws

Mobile app data and privacy regulations require lenders to be transparent about how applicant information is collected, stored, and used. In many regions, applicants also have the right to request information about automated decisions that impact their loan applications.

4. Model Explainability

AI models should be able to explain how a lending decision was reached. Tools like SHAP and other explainability frameworks help lenders identify the key factors that influenced an approval or rejection. This makes decisions much easier to understand and justify.

5. Bias Testing

Regular bias testing helps identify whether certain groups are being unfairly favored or disadvantaged by the AI model. By reviewing approval patterns and outcomes, lenders can make adjustments to improve fairness and reduce the risk of discrimination.

6. Audit Trails

Every underwriting decision should be recorded along with the data used, model version, and decision history. Maintaining detailed audit trails helps organizations meet regulatory requirements and makes it easier to review decisions during audits or investigations.

Compliance is not a one-time checklist. Your model changes every time it is retrained, so build the checks into your pipeline. Every new version gets tested before it goes live, not after.

Build vs Buy: Which Should You Choose?

You can buy an existing platform if you need a quick launch with standard underwriting rules. However, you can build a custom platform if your underwriting model, data sources, or compliance needs are specific to your business.

Most fintechs with a unique lending product end up with custom development. You can check out the table below of build vs buy comparison that can help you choose better.

| Option | Best For | Trade-off |

| Buy (off-the-shelf) | Quick launch, standard loan types | Limited customisation, ongoing licence fees, less control over the model |

| Customise existing platform | Lenders with some unique rules, standard infrastructure | Faster than building from scratch, but still capped by the base platform |

| Build custom | Fintechs with unique data or niche lending products | Higher upfront cost and time, full control over model, data, and integrations |

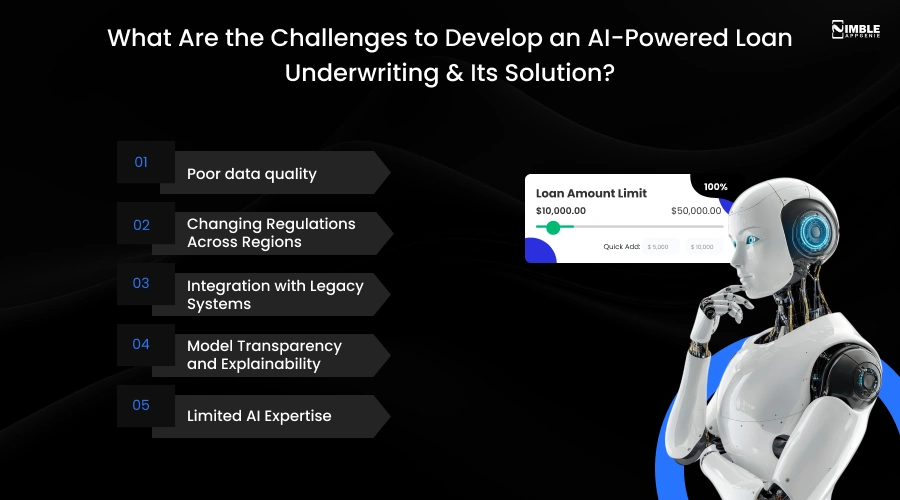

What Are the Challenges to Develop an AI-Powered Loan Underwriting & Its Solution?

The main challenges you may face while developing an AI-powered loan underwriting platform are:

- Poor data quality

- Integration with legacy loan origination systems

- Model and explainability

- Unclear regulations across regions

- Shortage of in-house AI talent

Most of these can be managed with the right planning and a dedicated development team. Addressing these challenges in advance can reduce project risk and improve implementation outcomes.

1] Poor Data Quality

AI models rely on accurate and complete data to make reliable decisions. Missing, outdated, or inconsistent data can lead to incorrect risk assessments.

Solution:

Regular data cleaning, validation checks, and integration with trusted data sources help boost data quality and model performance.

2] Changing Regulations Across Regions

Lending and fintech regulations differ from one country or region to another and are constantly evolving.

Solution:

Developing compliance frameworks into the platform and regularly updating policies can help ensure the system remains aligned with local legal requirements.

3] Integration with Legacy Systems

Many financial institutions still use older loan origination software and banking systems that may not easily connect with modern AI platforms.

Solution:

When you leverage fintech APIs, middleware solutions, and phased integration strategies, it can help bridge the gap without disrupting existing operations.

4] Model Transparency and Explainability

Loan decisions must be understandable to both lenders and borrowers. Some AI models can act like a black box. This makes it difficult to explain why an application was approved or rejected.

Solution:

So, it is vital to implement explainable AI tools and clear decision reports that can help improve transparency and trust.

5] Limited AI Expertise

Many organizations lack experienced AI and machine learning professionals needed to build and maintain underwriting models.

Solutions:

You should partner with experienced mobile app development teams, hire specialists, or use proven AI platforms that can help overcome this challenge and speed up implementation.

How Nimble AppGenie Helps You Build an AI-Powered Loan Underwriting Platform?

Creating this kind of platform takes people who understand AI, fintech compliance, cloud infrastructure, and how to connect with legacy banking systems.

Nimble AppGenie is a trusted AI lending software development company that works with fintech startups, NBFCs, and banks to build lending and underwriting platforms. Here’s what our team handles when you bring a loan underwriting project to them:

- Underwriting policy mapping: We work with your risk and compliance teams to translate your existing rules into a decision engine.

- AI model development and integration: We develop or integrate credit risk models, document processing, and fraud detection.

- Compliance-first architecture: We build explainability, audit trails, and data privacy controls from the first sprint and do not add it later.

- Integration with existing systems: We connect the new AI layer to your current LOS, core banking systems, credit bureaus, and bank data providers like Plaid.

- Ongoing support: We monitor, model, retrain, and update as your loan portfolio and regulations change.

If you are a fintech founder, CXO, CTO, CFO, or COO planning to add AI to your underwriting process, whether from scratch or as an upgrade to an existing system, our fintech team can scope the project, estimate cost and timeline, and build it alongside your compliance team. Get a free consultation with Nimble AppGenie to scope your AI underwriting platform.

Conclusion

Developing an AI-powered loan underwriting platform is not about replacing your underwriting team. It is about giving them better tools and handling routine decisions automatically.

You should start with your existing underwriting policy, choose the data sources and models that fit your loan products, and create compliance from day one.

Therefore, if you are ready to build an AI-powered loan underwriting platform, a dedicated fintech software development partner can help you plan the solution. They can also help choose the right tech stack and get it integrated with your existing systems.

FAQs

The time to create an AI underwriting platform is 4 to 8 months, depending on scope. An MVP with basic scoring and document processing can be ready in 3 to 5 months. If you add alternative data, fraud detection, and full LOS integration, the time can extend to 6 to 9 months.

The cost to make an AI-powered loan underwriting platform can range between $30,000-$250,000. This cost can fluctuate depending on your project requirements.

No. AI underwriting handles the bulk of standard applications automatically, but most lenders keep human underwriters for edge cases, disputes, and applications the AI flags as uncertain. AI plus human review is the current standard approach.

AI underwriting typically uses credit bureau reports, bank transaction data via providers like Plaid, income and employment data, tax documents, and sometimes alternative data such as utility payments or rental history for applicants with thin credit files.

To develop an AI-powered loan underwriting platform, you have to:

- Define your underwriting policy

- Gather and organise your data

- Choose your AI and ML models

- Build the document processing layer

- Build the decision engine and add compliance

- Integrate with your existing systems

- Test, monitor, and launch the platform

Buy or customise an existing platform if your underwriting needs are standard and you need to launch quickly. But it is best to build a custom platform if your loan product, data sources, or compliance requirements are particular to your business; most fintechs with a niche product choose this route.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.