AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Mortgage Lending

Mortgage Lending Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- Intelligent Document Processing (IDP) helps fintech companies handle paperwork faster. It can read, understand, and process documents without heavy manual work.

- It speeds up tasks like KYC checks, loan applications, and invoice processing. What once took days can now be completed in minutes.

- IDP uses AI, OCR, and machine learning to pull important information from documents and turn it into usable data.

- The platform also helps reduce errors. It can detect fraud, verify information, and flag suspicious documents automatically.

- Businesses do not need to build everything at once. Many start with one use case and expand as their needs grow.

- IDP is becoming a key tool for fintech companies because it saves time, lowers costs, and makes it easier to stay compliant with regulations.

How to Build an Intelligent Document Processing Platform for Fintech? Building an intelligent document processing platform for fintech means replacing slow, error-prone manual document handling with AI that reads, classifies, and extracts data at scale. That is the short answer. Here is the fuller picture.

Every fintech product depends on documents. KYC forms. Bank statements. Loan applications. Tax filings. Identity proofs. Invoices. As customer numbers grow, manual processing starts to break down. Documents pile up, reviews slow down, errors increase, and compliance risks grow.

Intelligent Document Processing solves this problem. It combines OCR, NLP, and machine learning to automatically read, classify, extract, and validate data from financial documents. Unlike basic OCR, IDP understands context and improves over time.

Fintech companies that automate document workflows are now building infrastructure that compounds in value as they scale. If you are a CTO, startup founder, or product lead, this guide gives you a clear picture of what is involved and what it takes to build an IDP platform for your fintech.

What is an Intelligent Document Processing Platform?

An intelligent document processing, or IDP, platform is software that uses AI, ML, and NLP to automatically read, classify, extract, and validate data from financial documents. Unlike basic OCR, which just converts text to a digital format, IDP understands context.

It can process unstructured documents like loan applications, KYC forms, and bank statements without predefined templates.

Traditional document processing in fintech relies on people manually reviewing forms, keying in data, and checking for errors. It is slow, expensive, and does not scale. IDP changes that.

It combines three layers of AI:

- OCR converts scanned or photographed documents into machine-readable text.

- NLP understands what the text means in context.

- ML learns from every document it processes and improves over time.

The result is a system that handles KYC packets, credit applications, fraud reports, and regulatory filings at scale, with minimal human review required. One distinction worth being clear on: IDP is not RPA, and it is not basic OCR.

OCR reads text. RPA in finance clicks through interfaces and automates actions. IDP understands documents. It sits at the intelligence layer of the automation stack. You need all three in a full fintech automation pipeline, but IDP is the one that turns unstructured financial documents into structured, usable data.

Why Do Fintech Companies Need an IDP Platform Right Now?

Fintech companies need IDP because the volume and complexity of financial documents have outgrown what manual processing can handle. Loan originations, KYC in fintech verifications, fraud investigations, and compliance audits all depend on fast, accurate document handling.

IDP reduces document processing costs by 30–50% and cuts turnaround time by up to 70%, while reducing the risk of compliance errors.

Startup founders and CTOs often ask,” Is IDP actually necessary, or is it a nice-to-have? The answer depends on your document volume and growth trajectory.

Here is what the numbers show:

- IDP can reduce document processing costs by 60-80%.

- Processing time can be cut by up to 70% compared to manual workflows.

- AI document extraction now reaches 95–99% accuracy on financial documents.

- Gartner forecasts that 50% of IDP solutions will implement Gen AI by 2027.

But the real reason fintech needs IDP right now is simpler than the statistics. Your competitors are building it. The companies that automate document workflows today are building operational infrastructure that becomes increasingly hard for slower movers to replicate.

Three structural pressures make manual document handling unsustainable for fintech:

- Regulatory complexity is increasing.

- Customer expectations are higher.

- Document volume scales faster than headcount.

IDP is the infrastructure that makes scale possible.

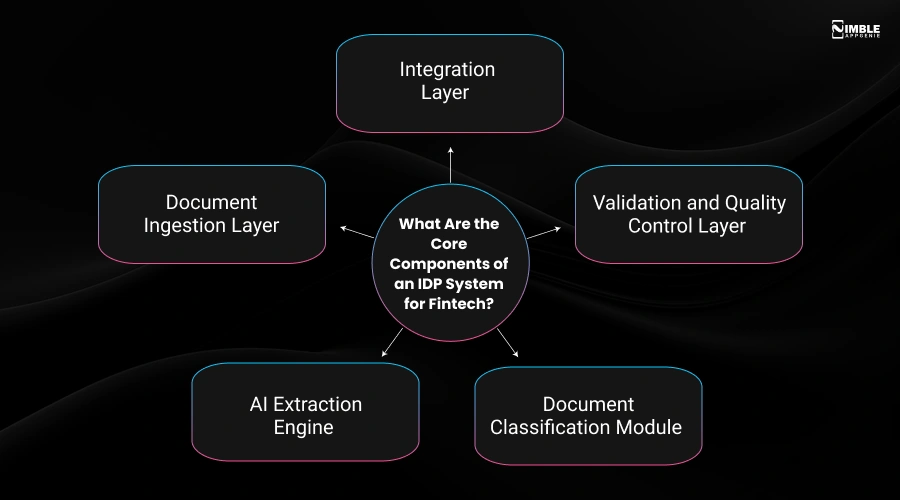

What Are the Core Components of an IDP System For Fintech?

An IDP platform for fintech has five core components: a document ingestion layer, an AI extraction engine, a classification module, a validation layer, and an integration layer. Each component has a specific job. Together, they form a document pipeline that takes raw input and produces structured, validated, usable data.

► Document Ingestion Layer

This is where documents enter the system. In fintech, they arrive from many places: email attachments, mobile app uploads, web form submissions, or scanned files.

The ingestion layer needs to handle multiple formats like PDFs, JPEGs, PNGs, TIFFs, DOCXs, and handwritten notes. It also needs to support real-time ingestion, not just batch processing, because customers expect instant feedback.

► AI Extraction Engine

This is the brain of the system. It uses:

- OCR to convert image-based text into a readable format.

- NLP to understand what each data field means in context.

- ML models trained on financial documents to extract specific entities like amounts, dates, account numbers, and signatures.

The extraction engine should handle both structured documents (forms with fixed fields) and unstructured ones (free-text contracts, emails).

► Document Classification Module

Before data extraction, the system needs to know what type of document it is looking at. A loan application needs a different extraction logic than a bank statement.

Classification uses ML models trained on document categories like KYC forms, identity proofs, invoices, contracts, credit reports, tax filings, and so on. Good classification means the right extraction model is applied every time.

► Validation and Quality Control Layer

Raw extraction output is not ready for downstream use.

The validation layer:

- Cross-references extracted fields against known data.

- Flags anomalies for human review.

- Applies fintech regulations and compliance rules. For example, checking KYC data against AML watchlists.

This is where a human-in-the-loop system fits in. Some exceptions require a person to review and correct before the data moves downstream.

► Integration Layer

Clean, validated data needs to flow into the systems that act on it.

The integration layer connects your IDP platform to:

- Core banking systems

- CRM platforms

- Compliance and audit tools

- Loan origination systems

- ERP platforms

API-first design makes this work easy. A well-built IDP system plugs into your existing fintech stack without requiring a full infrastructure overhaul.

Features of an Intelligent Document Processing Platform for Fintech

An intelligent document processing platform for fintech must include features such as AI extraction, document classification, OCR, PII redaction, AML screening, fraud detection, HITL review, audit logging, and fintech APIs integration. When you integrate these features, they will replace manual document workflows with an automated pipeline.

Here is the feature list for an Intelligent Document Processing Platform for Fintech:

| Feature | Why It Matters for Fintech |

| Multi-Source Document Ingestion | Documents arrive from email, mobile, web, and APIs. One ingestion layer handles all of them without manual sorting. |

| AI Data Extraction | It pulls specific fields, names, amounts, account numbers, and dates from any document type without manual data entry. |

| Document Classification | It identifies the type of document before extraction begins. Wrong classification means wrong extraction. |

| OCR Engine | The foundation of the entire system. Without accurate text recognition, nothing downstream works correctly. |

| Confidence Scoring | Every extraction gets a score. Low-confidence outputs go to human review instead of moving forward unchecked. |

| Validation Engine | It checks that the extracted data is logically correct before it reaches any downstream system or compliance process. |

| PII Detection and Redaction | It hides personal data automatically where it is not needed. Core requirement for GDPR and data minimisation compliance. |

| AML Watchlist Screening | Screens extracted names and entities against sanctions lists in real time. Non-negotiable for regulated fintech. |

| Human-in-the-Loop (HITL) Review | Routes uncertain extractions to a reviewer. Keeps accuracy high without slowing down the entire pipeline. |

| Audit Trail and Logging | Every document gets an immutable processing record. Required for AML reporting and regulatory audits. |

| KYC Document Verification | It checks identity documents for expiry, authenticity, and data consistency. Directly reduces onboarding time. |

| Fraud and Tamper Detection | Identifies altered or forged documents using computer vision. Catches fraud that manual review often misses. |

| REST API Layer | It connects IDP output to core banking, LOS, CRM, and ERP systems. Without this, extracted data goes nowhere useful. |

| Auto-Scaling Infrastructure | Document volumes spike. The platform must handle peak load without slowing down or failing. |

| Extraction Accuracy Monitoring | It tracks model performance over time. Catches accuracy drift before it creates compliance or operational problems. |

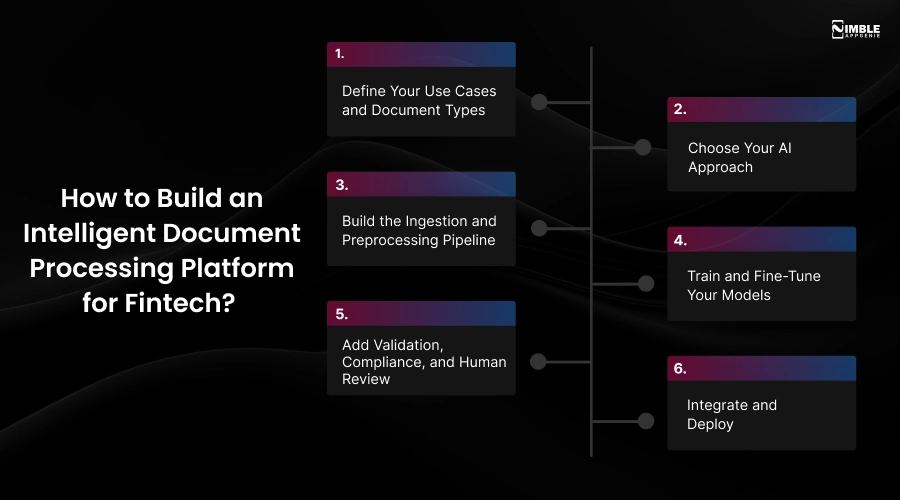

How to Build an Intelligent Document Processing Platform for Fintech?

To develop an intelligent document processing platform for fintech, follow these steps: define use cases and document types, choose an AI approach, build the data ingestion and preprocessing pipeline, train or fine-tune ML models, add validation, compliance checks, and a human review, and integrate and deploy. You can start with a focused pilot on one document type before scaling.

CTOs and product leads often ask: “How long does it take to build an IDP system from scratch, and where do we start?” The answer depends on the scope, but the process is the same regardless of scale.

♦ Define Your Use Cases and Document Types

Do not try to build a platform that manages everything at once. You can start with particular documents that cause the most issues in your current workflows.

The common starting points for fintech are:

- KYC Verification

- Loan Origination

- Invoice Processing

- Compliance Reporting

For each document type, you should define: what data fields you need to extract, what format documents arrive in, what validation rules apply, and where the extracted data needs to go. These decisions shape every technical choice you make later in the development process.

Read on if you are ready to develop an AI due diligence platform that simplifies document verification and compliance checks.

♦ Choose Your AI Approach

You have three options to build an intelligent document processing platform:

- Build from scratch: Custom models trained on your own data. High accuracy for your specific documents, higher cost, and longer time.

- Use pre-trained APIs: AWS Textract, Google Document AI, and Azure Form Recognizer. Faster to deploy, works well for standard document types, and has less control over edge cases.

- Hybrid: Use pre-trained OCR and NLP as a base, fine-tune for your document types. This is what most fintech development IDP platforms do.

For most fintech startups, the hybrid path is the right starting point.

♦ Build the Ingestion and Preprocessing Pipeline

Now, the dedicated development team sets up how documents enter the system.

This includes:

- Ingestion endpoints like email parsing, API uploads, file watchers, etc.

- Format handling covers PDFs, images, and scans into a unified processing format.

- Preprocessing includes denoising, enhancing contrast, and detecting page orientation.

- Document routing means sending each incoming file to the right processing pipeline.

A robust ingestion layer prevents failures downstream. Poor input quality is the leading cause of poor extraction accuracy. Fix it at the source.

♦ Train and Fine-Tune Your Models

If you are using custom or fine-tuned models, which you should be for development use:

- Collect at least 500 to 1,000 labeled examples per document type from your actual document set.

- Label key extraction fields: names, dates, monetary amounts, account numbers, signatures, and document-specific fields.

- Train your classification model first, then your extraction models per document type.

- Validate on a held-out test set; target 90%+ accuracy before production deployment.

- Build a feedback loop: when a human reviewer corrects an extraction error, that correction becomes training data.

Quality of training data is the single biggest determinant of IDP accuracy. Do not use generic public datasets if your documents have specific formats or financial terminology.

♦ Add Validation, Compliance, and Human Review

This is the layer that separates a working prototype from a development-grade system:

- Validation rules: Check that extracted values are logically correct.

- Compliance checks: Run extracted identity data against KYC/AML databases, apply GDPR redaction for PII fields.

- Confidence scoring: Tag extractions with a confidence score. Low-confidence extractions go to human review.

- HITL interface: A clean UI where reviewers can see the original document alongside extracted fields and correct errors.

This step is consistently underbuilt in first-version IDP platforms. You should develop it properly from the start.

♦ Integrate and Deploy

Lastly, you should integrate your IDP output into the downstream platform:

- Core banking or loan origination software via REST API.

- CRM for customer record updates.

- Compliance tools for audit trails and regulatory reporting.

- Analytics platforms for processing metrics and model performance.

Deploy to a cloud environment with auto-scaling. Document volumes spike at onboarding events, regulatory deadlines, and promotional periods. Your infrastructure must handle peak load.

You can start with a pilot: one document type, one workflow, one team. Measure accuracy, processing speed, and exception rate. Then expand to additional document types once the first pipeline is performing well.

Tech Stack Required to Develop an Intelligent Document Processing Platform for Fintech

The tech stack to create an intelligent document processing platform for fintech depends on your document types, team skills, budget, and whether you need to own your models or can rely on third-party APIs.

The table below showcases the fintech tech stack required for an IDP platform.

| Layer | Technology Options |

| OCR Engine | Tesseract (open-source), AWS Textract, Google Document AI, Azure Form Recognizer |

| NLP / Extraction | spaCy, Hugging Face Transformers, OpenAI API, LlamaIndex |

| ML Framework | Python + TensorFlow, PyTorch, scikit-learn |

| Document Storage | AWS S3, Azure Blob Storage, Google Cloud Storage |

| Orchestration | Apache Airflow, Prefect, AWS Step Functions |

| Database | PostgreSQL (structured data), MongoDB (unstructured), Elasticsearch (search) |

| API Layer | FastAPI (Python), Node.js + Express, GraphQL |

| Review Portal (HITL) | React.js, Next.js |

| Compliance / Security | HashiCorp Vault (secrets), AWS CloudTrail (audit logs), field-level encryption |

| Monitoring | Prometheus + Grafana, AWS CloudWatch, Datadog |

Note: Most intelligent document processing platforms for fintech use pre-trained cloud OCR as a base layer and build classification, extraction, and validation models on top. This is the hybrid approach, faster time to market than a fully custom build, more control than a pure SaaS vendor solution.

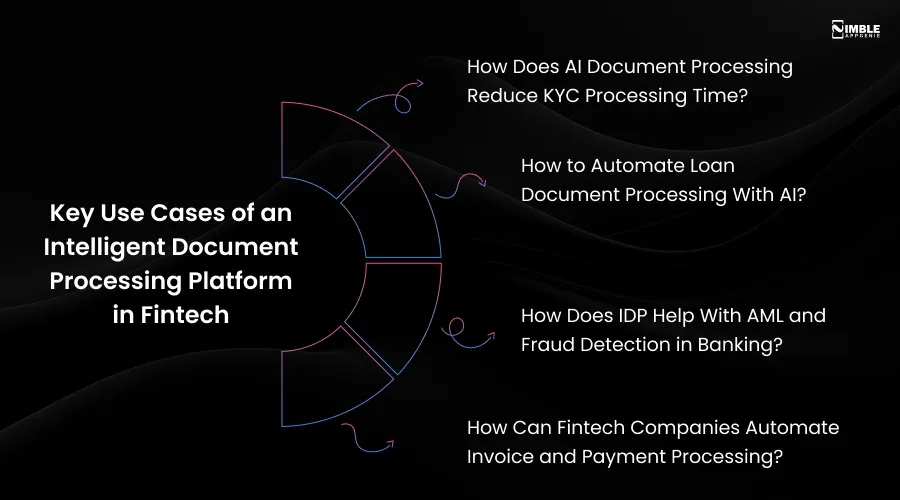

Key Use Cases of an Intelligent Document Processing Platform in Fintech

The major use cases of IDP in fintech are KYC and identity verification, loan origination, AML and fraud detection, invoice and payment processing, and regulatory compliance reporting. IDP is most valuable wherever document volume is high and manual review creates bottlenecks.

1. How Does AI Document Processing Reduce KYC Processing Time?

AI document processing reduces KYC processing time by automatically reading and verifying customer documents like IDs, passports, proof of address, and bank statements. Without automation, a KYC review can take 2-3 business days.

With IDP:

- Classifies submitted documents.

- Extracts name, date of birth, address, and document number.

- Cross-checks against internal records and third-party databases.

- Flags expired documents, mismatches, or signs of tampering.

The result: KYC reviews that took days now complete in minutes. That directly improves user retention.

2. How to Automate Loan Document Processing With AI?

AI can automate loan document processing by using OCR, ML, and data extraction tools to read, verify, and organize documents.

IDP in loan origination:

- Extracts income data and calculates debt-to-income ratios automatically.

- Identifies inconsistencies across submitted documents.

- Routes clean data to underwriting models.

By combining IDP with an AI loan underwriting platform, lenders can reduce manual reviews, improve accuracy, and shorten time-to-decision, one of the most important conversion metrics in lending.

3. How Does IDP Help With AML and Fraud Detection in Banking?

IDP improves document-based fraud detection by up to 50%.

It does this in multiple ways:

- Computer vision detects altered or tampered documents, pixel-level inconsistencies, mismatched fonts, and signs of digital editing.

- Cross-referencing extracted data against other submitted documents reveals synthetic identity fraud.

- Entity names and account numbers from extracted documents are screened against AML watchlists automatically.

- Every document processed generates an immutable audit trail that satisfies AML reporting requirements.

For compliance officers, IDP turns document review from a manual checkpoint into a continuous, automated process.

4. How Can Fintech Companies Automate Invoice and Payment Processing?

Invoice payment processing is often the first IDP use case fintech companies automate because the ROI is immediate and measurable. Structured invoice data, vendor name, invoice number, line items, totals, and due dates are relatively straightforward for AI to extract.

IDP extracts invoice data, matches it against purchase orders, flags discrepancies, and routes approved invoices for payment. Manual accounts payable processes that took days are reduced to hours.

Should You Build or Buy an IDP Platform for Your Fintech?

Whether to build or buy an intelligent document processing platform for fintech depends on document complexity, required customisation, and growth stage. Buying a SaaS IDP solution is faster and works for standard document types.

Building a custom platform gives full control over accuracy, compliance design, and integration, but takes 4–9 months and costs more upfront. Most fintech enterprises start with a vendor solution and move to a custom build as document volume and complexity grow.

This is the question CTOs and founders ask most often: should I build this ourselves or buy an off-the-shelf solution?

| Factor | Build Custom | Buy / SaaS IDP |

| Time to deploy | 4–9 months (MVP) | Days to weeks |

| Upfront cost | Higher ($50K–$250K+) | Lower (monthly subscription) |

| Customisation | Full control | Limited to vendor features |

| Accuracy on your docs | Trainable to your data | Generic models may need fine-tuning |

| Compliance control | You design it | Vendor controls compliance architecture |

| Vendor dependency | None | High |

| Scalability cost | Predictable at scale | Can become expensive at high volume |

| Best for | Scale-stage fintech with unique document types | Early-stage fintech with standard use cases |

The third option is a hybrid approach. It is what most fintech IDP development platforms end up using. You can use a pre-trained OCR or NLP API as the foundation, then build your classification, validation, and integration layers on top.

If your fintech processes high volumes of proprietary or complex documents, a custom build pays off faster than you might expect.

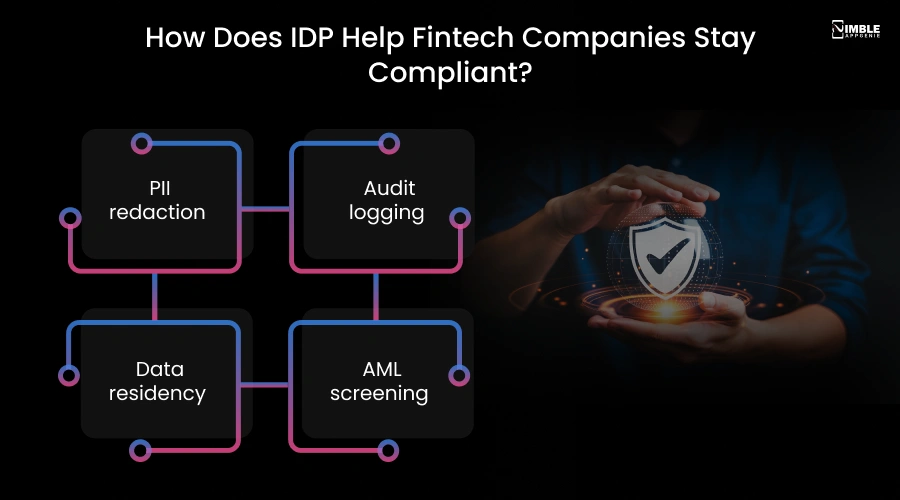

How Does IDP Help Fintech Companies Stay Compliant?

IDP helps fintech companies stay compliant by automating document verification against regulatory standards. It creates structured audit trails for every document processed, automatically redacts PII where required, screens extracted data against compliance databases, and reduces human error.

Can IDP help with GDPR and PCI DSS? Yes, but only if those requirements are built into the system architecture, not layered on top after deployment.

The key compliance functions your IDP platform must cover:

➤ PII redaction

The system should automatically identify and mask personal data fields in extracted outputs when downstream systems do not need them. Names, national ID numbers, account numbers, and dates of birth are all PII under GDPR.

➤ Audit logging

Every document processed must generate an immutable log — who submitted it, when it was processed, what was extracted, what was corrected, and who approved it. This is non-negotiable for AML and regulatory audit purposes.

➤ Data residency

Documents must be stored and processed only in geographic regions permitted under GDPR or applicable local data protection laws. Cloud architecture decisions must reflect this.

➤ AML Screening

Entity names, account numbers, and transaction details extracted from documents should be automatically screened against watchlists. Matches are flagged for human review before the process continues.

The difference between what is legally required and what is an IDP system default varies by vendor. If you are building custom or choosing a vendor, map your specific regulatory obligations to platform capabilities before committing.

How Much Does It Cost to Build an Intelligent Document Processing Platform for Fintech?

The cost to build an intelligent document processing platform for fintech ranges between $40,000-$250,000+depending on complexity, document types, and whether you use pre-trained AI models or develop custom ones. If you develop a basic MVP using cloud OCR and NLP APIs costs less.

However, if you want a full custom platform with proprietary ML models and compliance infrastructure, the cost will increase.

| Development Type | Estimated Cost | Timeline |

| MVP/Pilot | $40,000-$80,000 | 4-8 weeks |

| Mid-tier custom development | $80,000-$160,000 | 3-5 months |

| Full custom platform | $150,000-$250,000 | 6-9 months |

These are rough estimates. The actual IDP fintech development cost depends on your team’s location, the complexity of your document types, and the compliance requirements you need to meet.

Here are the factors that affect the intelligent document processing platform development for fintech.

- Complex or proprietary document formats.

- Multilingual document support.

- Real-time processing requirements.

- Deep compliance infrastructure.

- Number of system integrations required.

The best approach: define your use cases tightly, build an MVP with a narrow scope, validate accuracy and ROI, then scale.

How Can Nimble AppGenie Help You Build an IDP Platform for Fintech?

Nimble AppGenie is a fintech software development company with 8+ years of experience creating AI-powered financial platforms for startups and enterprises. We provide end-to-end IDP platform development with a compliance-first approach covering GDPR, PCI DSS, KYC, and AML requirements.

We have worked with fintech startups and enterprises across lending, neobanking, payments, and compliance, building platforms that handle real document volumes under real regulatory pressure.

Our team understands what a KYC pipeline actually requires, how loan origination workflows connect to document processing, and what compliance-by-design means in practice versus on a slide deck.

What we build:

- Custom IDP platform development, architecture, ML model training, extraction engine, validation layer, HITL interface, and system integrations.

- AI-powered fintech applications, including neobank platforms, lending software, eWallet apps, and payment solutions.

- Compliance-first development, GDPR, PCI DSS, KYC, AML, and CCPA requirements built into the core, not bolted on after.

- MVP development for fintech startups that need to validate their document automation use case before committing to a full build.

- Integration with existing core banking systems, CRM platforms, and loan origination systems.

If you are at the stage of evaluating whether to build or buy, deciding on a tech stack, or ready to scope a development, talk to our fintech development team. We have worked through the same decisions with 350+ clients globally.

Conclusion

Intelligent document processing platform development for fintech is not a small investment. But the return is real: faster onboarding, lower compliance costs, and document workflows that scale without adding headcount.

To build an intelligent document processing platform for fintech, you can start with an MVP, choose one document type, build a working pipeline, and measure accuracy. At last, you can expand.

However, if you need a technology partner who knows fintech from the inside, consult an experienced team that can help you scope the right architecture and build a system that works in production, not just in a demo.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.