AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- IBAN was created in 1997 to eliminate routing errors, missing account identification, and undetectable transcription mistakes in international payments.

- An IBAN automatically decodes account details, validates check digits, and routes funds via SEPA or SWIFT without manual intervention.

- PSPs and EMIs use IBAN to issue virtual accounts, prevent fraud, and integrate seamlessly with traditional banking infrastructure.

- IBAN lengths vary by country – from 15 characters in Norway to 34 characters in some Caribbean nations.

- Fintech companies integrate IBAN via BaaS APIs, covering issuance, validation, reconciliation, AML screening, and multi-currency settlements.

- Connect with Nimble AppGenie to build an IBAN-ready fintech app in 2026.

Cross-border payments are the backbone of modern fintech apps, enabling businesses and users to send and receive money globally with speed and security.

But to make international transactions seamless, you need to know about IBAN.

What is IBAN?

An IBAN, or International Bank Account Number, is a globally recognized system used to identify bank accounts across countries and reduce errors in international money transfers.

For fintech companies, integrating IBAN support can simplify payments, improve transaction accuracy, and enhance user trust. As global digital banking and remittance services continue to grow, IBAN-enabled payment systems are becoming a necessity rather than an option.

If you are a user, a fintech startup, or an enterprise looking to integrate IBAN, this is the right place to know it all.

In this guide, we’ll explore what IBAN is, how it works, and why it plays a critical role in enabling fast, secure, and compliant cross-border payments in your fintech app.

What is an IBAN?

IBAN is a globally standardized code used to uniquely identify a specific bank account across borders. This code helps users to identify individual accounts within a bank, which is helpful in international money transfers.

Let’s understand it in more detail.

What Does IBAN Stand For?

IBAN stands for International Bank Account Number and is used to make and receive international payments.

The core purpose of IBAN is to identify bank accounts across borders and perform transactions smoothly.

IBAN was created by the European Committee for Banking Standards (ECBS) in 1997. It was adopted as an international standard ISO 13616, under the International Organization for Standardization (ISO).

Okay! But what’s the need for IBAN? Why was IBAN discovered?

Well, back in 1997 & before, people faced several challenges with the routing and international account transfers.

Here’s a detail.

Why Was IBAN Created?

Earlier, banks were facing issues related to routing errors that even resulted in delayed payments and incurred extra costs to the sending and receiving banks, and often to the intermediate routing, as well as domestic banks.

Additionally, before 1997, differing national standards for bank account identification were a difficult and confusing task for most of the users.

The third reason was that routing information was missing from payments as specified under ISO 9362. Here, the identification of accounts and even the transaction types was left to agreements within the transaction partners.

It doesn’t contain any check digit format, so the transcription errors were not detectable, and it was not possible for the banks to check the routing information before proceeding and submitting payments.

Hence, IBAN was discovered.

It facilitates payments within the European Union and was later implemented by most European countries and numerous other countries in different parts of the world.

If you want to lead among the top fintech apps, you should integrate IBAN, and you should be aware of its working process.

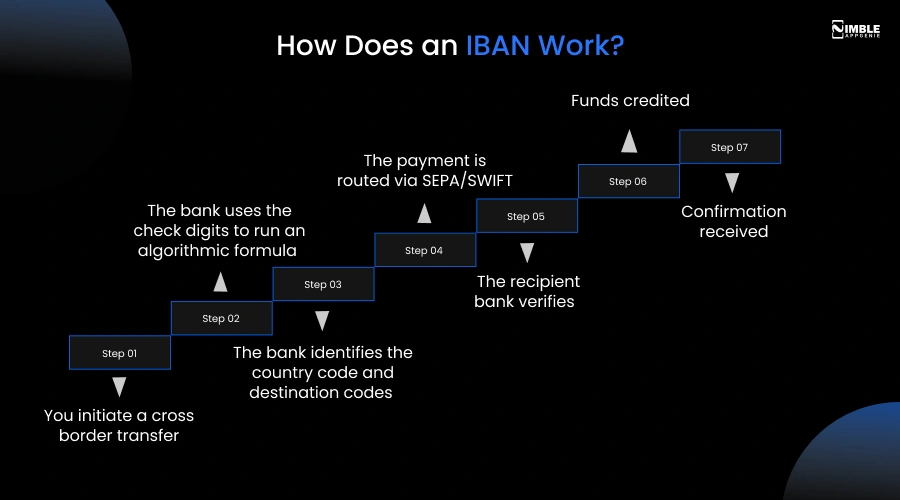

How Does an IBAN Work?

IBAN acts as a global standardized postal address for bank accounts. Basically its a code that helps to transfer payments and route payments to the right addresses.

It uniquely identifies the bank’s individual account and the bank globally, ensuring that the international money transfers are routed accurately without any errors.

Here’s what happens behind IBAN:

Step 1: You initiate a cross-border transfer

Step 2: The bank uses the check digits to run an algorithmic formula

Step 3: The bank identifies the country code and destination codes

Step 4: The payment is routed via SEPA/SWIFT

Step 5: The recipient bank verifies

Step 6: Funds credited

Step 7: Confirmation received

Now, let’s get ahead with the reasons why IBAN is important for modern banking and fintech in the following section.

Why IBAN Matters in Modern Banking and Fintech?

As the businesses started to grow, they needed to connect with an international banking system to process the global transfers accurately and efficiently. Therefore, IBAN plays a crucial role in fintech business models.

Let’s understand the need for IBAN under different parameters.

Why PSPs and EMIs Need IBAN Support?

The payment service providers (PSPs) and electronic money institutions (EMIs) need IBAN support because:

- To seamlessly integrate with the traditional banking systems, and for processing cross-border payments.

- The PSPs and EMIs can issue unique and virtual IBANs (VIBANs) to merchants and customers.

- IBAN offers fraud protection and verification by implementing verification of Payee (VoP) services. It heavily introduces misdirected payments to the account that matches the destination.

- With the help of IBAN, the PSPs and EMIs use strict and internationally recognized routing for the account structures that offer transparency, ensuring that funds are clearly verified.

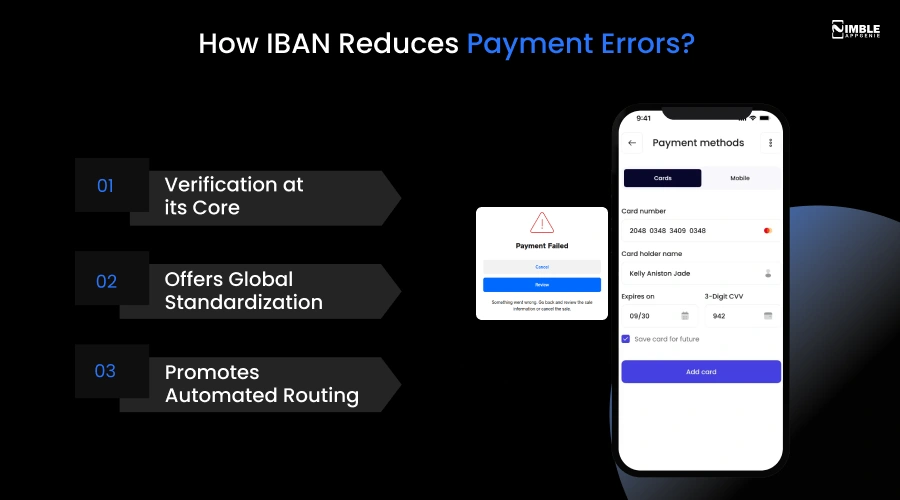

How IBAN Reduces Payment Errors?

IBAN reduces payment errors by using a standardized alphanumeric format and even embedded check digits that help to instantly validate the account data at the source before processing.

Let’s get in-depth:

1. Verification at its Core

The IBAN has a country code and even two numerical digits, which helps to transfer the money across borders using a mathematical formula.

When an IBAN is typed, the payment software instantly recalculates the digits; if there is a typo error, it gives an alert before the transaction.

2. Offers Global Standardization

IBAN is helpful to standardize the account details, where the local formats confuse the banking system and even the users.

The Global standardization of IBAN helps in delivering payments across the globe. It has a unique code that helps to make the universal payments standardized.

3. Promotes Automated Routing

IBAN promotes the automated routing and even minimizes the complete payment errors through combining the standardized account format with the built-in mathematical validation.

It helps to instantly catch typos and is even helpful to map the payment to the correct bank account.

Now, let’s study the benefits of IBAN for cross-border payments in the following section.

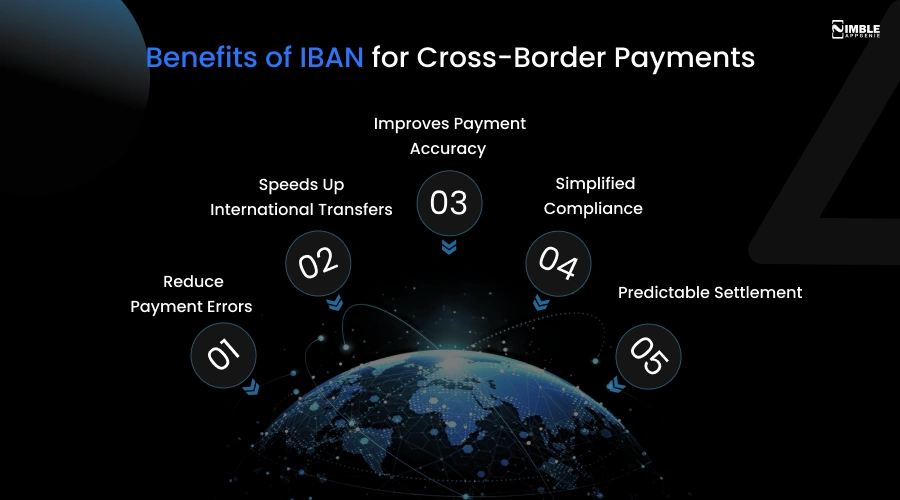

Benefits of IBAN for Cross-Border Payments

The core benefits of IBAN for cross-border payments are that it helps in improving security, reduces transaction costs, and even results in faster processing times.

Here’s a list of complete benefits below:

1. Reduce Payment Errors

With the help of IBAN, one can minimize payment errors via standardized, built-in verification methods.

It provides the users with alerts related to what numbers they have typed and which country code is used. If any of them is wrong, they first ask, then proceed with payments.

2. Speeds Up International Transfers

IBAN speeds up international transfers through reducing the delays occurred in verifying routing, identifying and verifying the account numbers across borders has also been speed up.

It helps in enabling a higher automation process.

3. Improves Payment Accuracy

The implementation of IBAN drastically enhances the payment accuracy by standardizing and proceeding with the account verification process.

It helps in improving the overall payment accuracy and even in performing transactions securely.

4. Simplified Compliance

IBAN effectively helps in simplifying the overall compliance by providing the financial institutions with a complete and verified structure.

It enables low-cost and even standardized euro payments across the participant countries, helping firms to develop a PCI compliance fintech app.

5. Predictable Settlement

IBAN offers more predictable settlement windows, which matters for the high-volume merchants, gig platforms, FX services, and payroll providers.

It even eliminates the routing errors and delays, ensuring that the funds consistently arrive at the correct bank account.

Now, let’s proceed with how an IBAN is structured in the given section.

How is an IBAN structured?

An IBAN do contains upto 34 alphanumeric characters that comprise a country code, two check digits, and a number that comprises the domestic bank account number, branch identifier, and even potential routing information.

The total number of characters can fall between 15 and 34 based entirely on the country.

Here is the visual presentation of IBN Structure:

┌────┬────┬──────┬────────┬──────────┐

│ GB │ 29 │ NWBK │ 601613 │ 31926819 │

└────┴────┴──────┴────────┴──────────┘

│ │ │ │ │

│ │ │ │ └─ Account Number

│ │ │ └──────────── Branch/Sort Code

│ │ └───────────────────── Bank Code

│ └─────────────────────────── Check Digits

└───────────────────────────────── Country Code

To understand the details of “What is an IBAN number?”, let’s learn in the following headings.

IBAN Format Explained

Here is the detail of the IBAN format and what it comprises (the format is explained from left to right, considering IBAN):

- Country Code (2 letters): Identifies the country of the bank holding the account, for example, GE – Germany; FR- France.

- Check Digits: These are two numbers produced through an algorithm that helps to verify whether the IBAN is valid. This is calculated using the MOD 97 algorithm to verify the integrity and even prevent the transcription of errors.

- Bank Identifier/Bank Code: It is a bank identifier number and basically a bank code. It identifies your bank.

- Branch and Sort Code: These are the digits that sometimes follow to indicate the bank branch. This code is often skipped in many countries.

- Account Number: These are the specific numbers that pinpoint your specific bank account.

IBAN Length by Country

Let’s check the IBAN length by country in the given table:

| Country | Country Code | IBAN Length | Example IBAN |

| Norway | NO | 15 | NO8330001234567 |

| Belgium | BE | 16 | BE71096123456769 |

| Denmark | DK | 18 | DK9520000123456789 |

| Finland | FI | 18 | FI1410093000123458 |

| Netherlands | NL | 18 | NL02ABNA0123456789 |

| Sweden | SE | 24 | SE7280000810340009783242 |

| Germany | DE | 22 | DE75512108001245126199 |

| United Kingdom | GB | 22 | GB33BUKB20201555555555 |

| France | FR | 27 | FR7630006000011234567890189 |

| Spain | ES | 24 | ES7921000813610123456789 |

| Italy | IT | 27 | IT60X0542811101000000123456 |

| Switzerland | CH | 21 | CH5604835012345678009 |

| Poland | PL | 28 | PL10105000997603123456789123 |

| Portugal | PT | 25 | PT50003310311234567890197 |

| Ireland | IE | 22 | IE06BOFI90008412345671 |

| Austria | AT | 20 | AT483200000012345864 |

| Saudi Arabia | SA | 24 | SA4420000001234567891234 |

| United Arab Emirates | AE | 23 | AE460090000000123456789 |

| Qatar | QA | 29 | QA54QNBA000000000000693123456 |

| Turkey | TR | 26 | TR190006200009112345678901 |

| Pakistan | PK | 24 | PK36SCBL0000001123456702 |

| Malta | MT | 31 | MT31MALT01100000000000000000123 |

| Saint Lucia | LC | 32 | LC14BOSL123456789012345678901234 |

| Russia | RU | 33 | RU0204452560040702810412345678901 |

You might have heard about SWIFT, but what is the difference between these two terms? Let’s understand them in detail in the following section.

IBAN Vs SWIFT/BIC: What PSPs and EMIs Need to Know?

The IBAN identifies the complete bank account itself. However, a SWIFT/BIC does identify the bank itself. It is important to know the difference between IBAN and SWIFT for fintech companies, EMIs, and even PSPs.

Let’s evaluate the key differentiating factors below:

| Factor | IBAN | SWIFT / BIC |

| What It Identifies | The recipient’s specific bank account | The recipient’s bank or financial institution |

| Simple Analogy | Your home address | The city in which your home is located |

| Format | Up to 34 alphanumeric characters | 8 or 11 alphanumeric characters |

| Example | GB29 NWBK 6016 1331 9268 19 | NWBKGB2L |

| Used For | Pinpointing exactly where money should be deposited | Routing the payment to the right bank |

| Required for SEPA? | Yes – mandatory | No – not needed |

| Required for International Wire? | Yes – alongside SWIFT/BIC | Yes – alongside IBAN |

| Error Validation | Built-in – check digits catch mistakes automatically | No built-in validation |

| Used In | 89 countries | 200+ countries |

So, how many countries use IBAN?

There is a total of 87 countries uses IBAN actively according to the official registry managed by SWIFT, as updated by IBAN on 13th many 2026.

Yet, many countries do not use the IBAN number. Let’s identify the countries:

Countries That Do Not Use IBAN

| Country | What They Use Instead | Why They Don’t Use IBAN |

| United States | Routing Number + Account Number + SWIFT | Uses domestic ACH and Fedwire systems |

| Canada | Transit Number + Institution Number | Relies on local banking identifiers |

| Australia | BSB Number + Account Number | Uses its own domestic payment network |

| New Zealand | Bank Number + Account Number | Local banking structure is sufficient |

| China | CNAPS Code + SWIFT | Uses domestic banking infrastructure |

| Japan | Bank Code + Branch Code + Account Number | Operates on national banking standards |

| India | IFSC Code + Account Number | Uses RBI-regulated domestic payment systems |

| Singapore | Bank Code + Account Number | Local payment rails are widely used |

| Hong Kong | Bank Code + Branch Code + Account Number | Uses local clearing systems |

| South Korea | Bank/Branch Codes + Account Number | The domestic banking system differs from IBAN |

| Thailand | Bank Code + Account Number | Uses local electronic payment standards |

| Malaysia | Bank Identifier + Account Number | The domestic payment ecosystem is preferred |

Now, what are the core types of IBAN accounts that can be created?

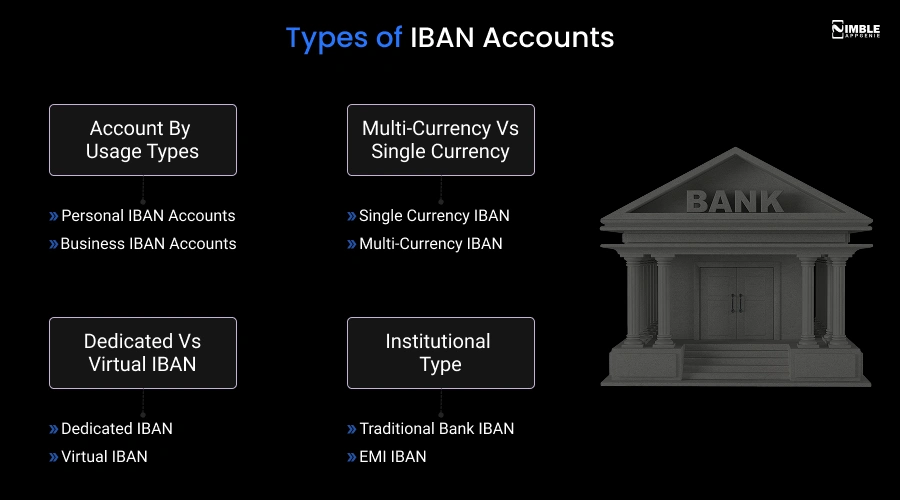

Types of IBAN Accounts

The types of IBAN accounts can be classified into the following categories:

1. Account By Usage Types

These types of accounts can be segregated into personal IBAN and business IBAN accounts.

-

Personal IBAN Accounts

This is a standard bank account that is assigned to an individual and consists of up to 34 alphanumeric characteristics. The major features of this type of account are cross-border transfers and day-to-day transfers, which are dedicated to individuals.

-

Business IBAN Accounts

The business IBAN accounts are designed for companies, allowing corporate features such as multiple user access, bulk payroll processing, and integration with the accounting software.

2. Multi-Currency Vs Single Currency

Here, the type of classification is based on currency parameters. Let’s classify them below.

-

Single Currency IBAN

Single-currency IBAN accounts are primarily denominated in one currency. Additionally, these are perfectly fine for the domestic transfers, although they can also incur conversion fees while performing international transactions.

-

Multi-Currency IBAN

These Multi-currency IBAN helps the users to receive, hold, and send diversified currencies such as EUR, USD, or GBP from the same account. These type of accounts bypasses the diversified conversion fees.

3. Dedicated Vs Virtual IBAN

Let’s determine the dedicated vs Virtual IBAN, below:

-

Dedicated IBAN

It is a unique personal IBAN that is tied directly to your specific account. Any fund sent here belongs to the user. It guarantees that all the incoming payments route directly to the user’s account.

-

Virtual IBAN

Virtual IBAN is a unique, digital payment identifier that is assigned to a customer or transaction, which automatically routes the incoming funds to a single master bank account.

4. Institutional Type

The institutional type can be further classified into traditional and EMI:

-

Traditional Bank IBAN

A traditional bank IBAN is a standardized code that is used to securely identify a specific bank account across national borders. These accounts are primarily used in Europe, the Middle East, and even parts of the Caribbean.

-

EMI IBAN

EMI IBAN is a licensed fintech firm that provides digital banking services such as payment processing, e-wallets, and even virtual accounts.

As a user of IBAN, if it’s difficult for you to find your IBAN number, let’s explore the next section.

Where Can You Find Your IBAN?

To find an IBAN, you can log in to your online banking account, and you can check your bank statement. If you still don’t get it, connect with your bank or related customer service support.

Additionally, you should note that an IBAN being in the right format doesn’t guarantee that it exists, and even that it is the right IBAN for a particular account.

You must use the right IBAN code when sending money. If you get the code wrong, it can impact your complete transaction, and you might lose your money in a wrong transfer.

With the official tool, you can calculate it by yourself.

Now, let’s get ahead with the common IBAN payment errors in the following section.

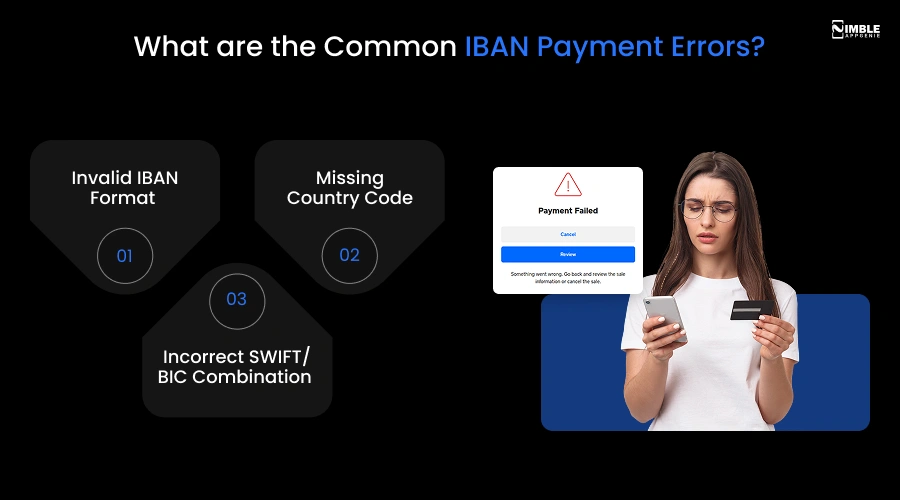

What are the Common IBAN Payment Errors?

The common IBAN payment errors are typing errors, formatting issues, and even the incorrect SWIFT/BIC combination.

From learning what an IBAN number is? Let’s get ahead with the issues you might encounter:

1. Invalid IBAN Format

If the format chosen is incorrect, such as you have used a branch code instead of a digit code and have typed the bank account number incorrectly, then this can be one of the major issues to avoid.

2. Missing Country Code

A missing country code can be a specific challenge that can further result in a transaction failure. Additionally, a mismatched billing address, failed routing, the currency and regional restrictions, and even the API verification error can be IBAN payment issues.

3. Incorrect SWIFT/BIC Combination

If the combination of the bank address and the account number is not correct, this can result in a payment failure. This can result in an automated compliance rejection, and even might cause the payment to be lost.

But, the question remains for IBAN users like you: how does IBAN enable seamless cross-border payments within the fintech app?

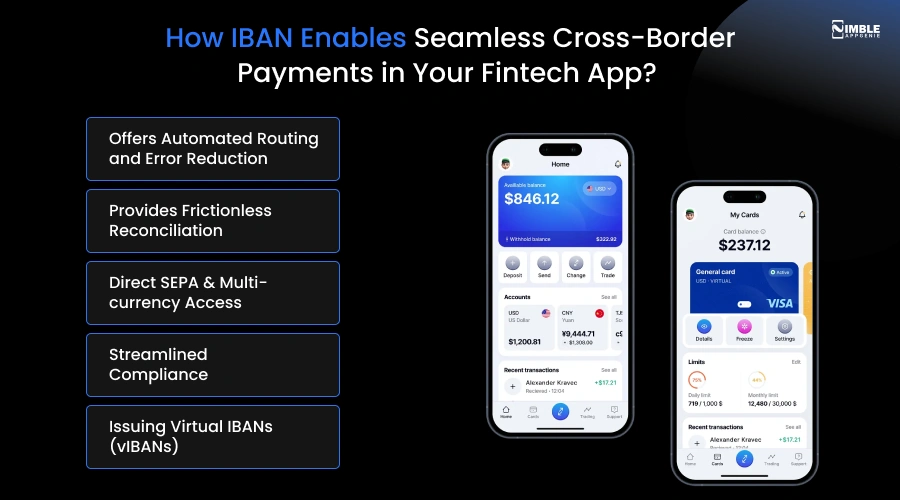

How IBAN Enables Seamless Cross-Border Payments in Your Fintech App?

IBAN enables seamless cross-border payments in fintech apps by providing a globally standardized format.

This helps to automate routing, reduce transaction errors, and integrate with secure international payment systems, including SWIFT and SEPA.

Here’s how IBAN enables seamless cross-border payments:

1. Offers Automated Routing and Error Reduction

IBAN does offer automated routing to users. This routing was not founded in the traditional cross-border wires.

With the help of automated routing, the algorithms can instantly validate an IBAN at the app interface level, preventing users from sending money to the wrong account.

2. Provides Frictionless Reconciliation

If your app caters to businesses or platforms that process large volumes of international invoices or client funds.

With the help of vIBAN, the complete transaction is instantly and securely matched to the correct ledger, eliminating the need for manual reconciliation and invoice-matching.

3. Direct SEPA & Multi-currency Access

If the fintech app operates within Europe, the IBAN is the backbone of the single Euro payment area (SEPA). It allows seamless, low-cost Euro transactions.

However, the multi-currency access lets you hold and manage different global currencies simultaneously.

4. Streamlined Compliance

The cross-border payments are subject to the strict anti-money laundering (AML) and KYC frameworks. Here, IBANs contain verified, country-specific identifiers and API integrations that can easily track exactly which jurisdictions a payment is flowing.

It eases the burden of global regulatory reporting.

5. Issuing Virtual IBANs (vIBANs)

For the fintech firms that are dealing in different industries of e-commerce, freelancers, or multi-jurisdictional marketplaces, maintaining physical bank accounts can be costly.

Hence, a fintech partners with EMIs or a BaaS provider to issue vIBANs to its users. It helps the users with “local” account details for receiving global payments and avoiding high intermediary fees.

If you are an entrepreneur or businessman looking forward to creating a fintech app, then how can you integrate IBAN infrastructure? Let’s get ahead with the following section.

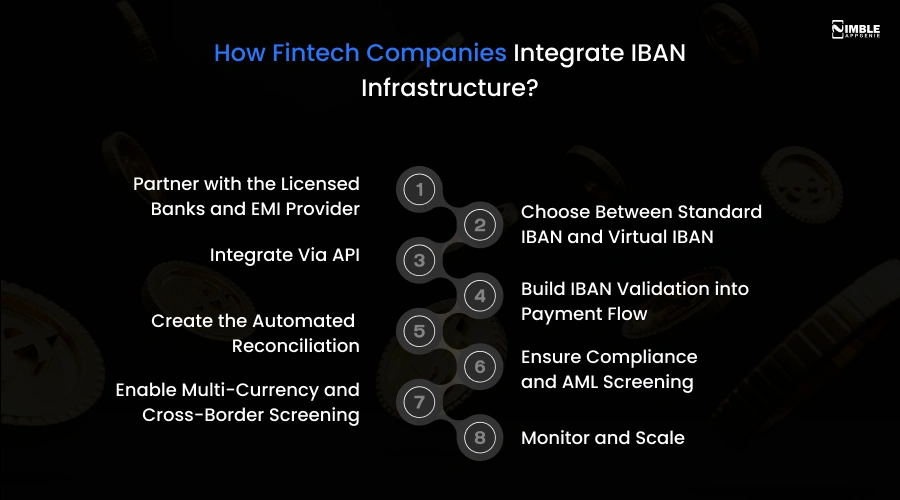

How Fintech Companies Integrate IBAN Infrastructure?

The fintech companies do integrate an IBAN infrastructure primarily through banking-as-a-service (BaaS) API. With the help of an API, these types of providers do allows the fintech to issue the direct and virtual IBANs.

Here, fintech firms often ask: how do fintech companies integrate IBAN infrastructure?

Let’s get ahead with the complete list of steps below:

Step 1: Partner with the Licensed Banks and EMI Provider

- Fintech companies cannot issue IBAN on their own.

- They partner with licensed banks and EMI providers.

- These partners hold the regulatory authority to issue IBANs.

Step 2: Choose Between Standard IBAN and Virtual IBAN

- Standard IBAN: Tied to an actual bank account. Best for neobanks and digital wallets that hold funds directly.

- Virtual IBAN (vIBAN): This is a unique identifier connected to the master account. This is best for PSPs, marketplaces that need to assign individual account references to thousands of users or merchants without opening individual bank accounts for each.

Step 3: Integrate Via API

- Modern BaaS providers and EMIs do offer IBAN issuance through RESTful APIs in fintech.

- Trigger instant reconciliation at the transaction level.

- Helps to handle multi-currency settlements across different IBANs.

Step 4: Build IBAN Validation into Payment Flow

- The platform must validate the IBAN before any payment is processed.

- Check the digit verification, running the MOD-97 algorithm to confirm the IBAN is mathematically correct.

- Opting for existence verification, confirming that the IBAN is active and belongs to a real account via third-party validation.

Step 5: Create the Automated Reconciliation

- It is all about creating ingestion translation statements and matching them against the internal ledgers.

- Configure standardized matching rules with an automation platform, such as numeric or automation anywhere.

- Each incoming payment carries a unique IBAN reference that matches automatically to the correct user.

Step 6: Ensure Compliance and AML Screening

- Every IBAN-based transaction should pass through AML and KYC checks.

- Fintech firms integrate tools that can flag unusual transaction patterns in real time.

- Can maintain a full audit trail of every payment for regulatory reporting.

Step 7: Enable Multi-Currency and Cross-Border Screening

- The advanced IBAN integration goes beyond the single-currency domestic payments.

- The fintech platforms do integrate FX layers on top of IBAN infrastructure to support the multi-currency accounts.

- Helps to receive funds in multiple currencies.

Step 8: Monitor and Scale

- The platform monitors IBAN performance, tracks payments, and even settlement delays.

- As the user base grows, the virtual IBAN infrastructure scales via the BaaS partner’s API.

- Grow the infrastructure without banking overhead.

Struggling to Create an IBAN-Ready Fintech App? Nimble AppGenie Can Help!

If you are an entrepreneur or a business owner struggling to create an IBAN-ready fintech app, then connecting with Nimble AppGenie can be helpful.

Nimble AppGenie is the leading fintech app development company, building a fintech app with IBAN integration. We connect with banks to ensure that you get a seamless fintech app that caters to your diversified audience.

We offer an IBAN-ready app by providing the following solutions:

1. Offering API & Banking Infrastructure

We integrate with leading BaaS providers to allow your app to generate, manage, and process virtual IBANs.

2. Regulatory Compliance

Nimble AppGenie can help you to build a built-in compliance engines that streamline KYC and AML processes, ensuring that your app meets global financial regulations.

3. Security & Fraud Prevention

With the help of AI-driven anomaly detection, their development helps protect the accounts from unauthorized access and fraud.

4. Provides Cross-Platform Compatibility

Nimble AppGenie offers cross-platform compatibility and deploys scalable mobile and web applications as per the client’s requirements.

5. Multi-Currency Processing

The team designed architectures that are designed for foreign exchanges and cross-border settlements, allowing users to hold different currencies linked to their IBAN.

Conclusion

IBAN is no longer just a European banking standard; it is the backbone of modern cross-border payments and fintech infrastructure.

Whether you are a PSP, EMI, neobank, or fintech startup, understanding and integrating IBAN correctly directly impacts your payment accuracy, compliance standing, and user experience.

From virtual IBANs to automated reconciliation, the opportunities IBAN unlocks are significant for the users. Connecting with a trusted firm can help build an IBAN-ready fintech app.

FAQs

IBAN stands for International Bank Account Number, which is a globally standardized code used to uniquely identify a specific bank account across borders, making international money transfers accurate and seamless.

IBAN stands for International Bank Account Number. It was created by the European Committee for Banking Standards (ECBS) in 1997 and adopted as an international standard under ISO 13616.

An IBAN can contain between 15 and 34 alphanumeric characters, depending on the country. For example, a UK IBAN contains 22 characters while a French IBAN contains 27 characters.

No — IBAN identifies a specific bank account while SWIFT/BIC identifies the bank itself. Most international wire transfers require both working together to route payments accurately.

You can find your IBAN by logging into your online banking portal, checking your bank statement, or contacting your bank’s customer support directly.

As of 2026, 87 countries actively use IBAN, primarily across Europe, the Middle East, and parts of the Caribbean. Major economies like the US, Canada, Australia, India, and China do not use IBAN and rely on their own domestic payment identifiers instead.

A virtual IBAN (vIBAN) is a unique digital payment identifier linked to a master bank account, allowing PSPs and fintech platforms to assign individual account references to thousands of users or merchants without opening separate bank accounts for each one.

IBAN offers seamless cross-border payments in a fintech app through offering automated routing and error detection, providing frictionless reconciliation, and direct SEPA and multi-currency access.

Madan is the Backend Solutions Architect at Nimble AppGenie, specializing in the design of secure, high-concurrency systems that power complex mobile ecosystems. With deep expertise in server-side logic and database management, he ensures every platform is built with enterprise-grade security. In his free time, he is an avid researcher of emerging technologies; he spends his time deconstructing the latest backend frameworks and reading technical papers to ensure our solutions remain at the absolute forefront of industry innovation.

Table of Contents

No Comments

Comments are closed.