AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Nimble AppGenie rolled out an African multi-currency wallet, specifically for the 14 countries and two currencies across the CEMAC and UEMOA.

It allows users to open a digital account, hold and send money in local currencies, get a free virtual Visa card, and make payments across borders, all from their phone.

Let’s uncover behind-the-scenes at how we built the Africa’s multi-currency wallet. What the product does, how we built it, what broke, and what we learned.

Fintech founders, product managers, fintech startup teams, or anyone simply interested in digital payments in Africa, get real insights here from the ground up.

What is an African Multi-Currency Wallet?

The multi-currency wallet is a platform for Central and West Africa. It is basically for users, merchants, agents, employers, and third-party partners. Apart from this, It is available in both French and English. This helps users from different regions to use it very easily.

Today, this wallet has reached a valuation of more than $1.2 million. This shows a growing popularity in the African digital market. It supports 14 countries across two monetary unions mentioned below:

- CEMAC zone (XAF): Gabon, Cameroon, Central African Republic, Chad, Republic of Congo, Equatorial Guinea.

- WAEMU zone (XOF): Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal, Togo.

Additionally, it supports currencies: XAF and XOF. Users can hold XAF or XOF, send money by phone number or QR code, get a free virtual Visa card, and access an IBAN for international transfers.

Besides, two features stand out from what already exists in the market.

- IBAN support: Users get a real IBAN number. This is used in international banking. For someone who has never had a bank account, this is a big deal. It means they can receive payments from anywhere in the world.

- Visa Card: Users get a free virtual Visa card immediately on signup. A physical card is also available for free, delivered within 24 hours through a partnership with ECOBANK Gabon.

| Partnership note: The Visa card is issued through ECOBANK Gabon. This partnership was non-negotiable. Without a licensed banking institution behind the card issuance, the product could not legally operate. |

What We Built Africa’s Multi-Currency Wallet: Full Feature Breakdown

The multi-currency wallet includes four core feature-type modules. The user panel manages individual accounts, KYC verification, deposits via agents or banks, etc. The business panel adds merchant QR codes, bulk supplier payments, and sub-account management.

The agent panel supports cash-in and cash-out with float management and offline mode. Let’s have a look at the different feature panels we have created.

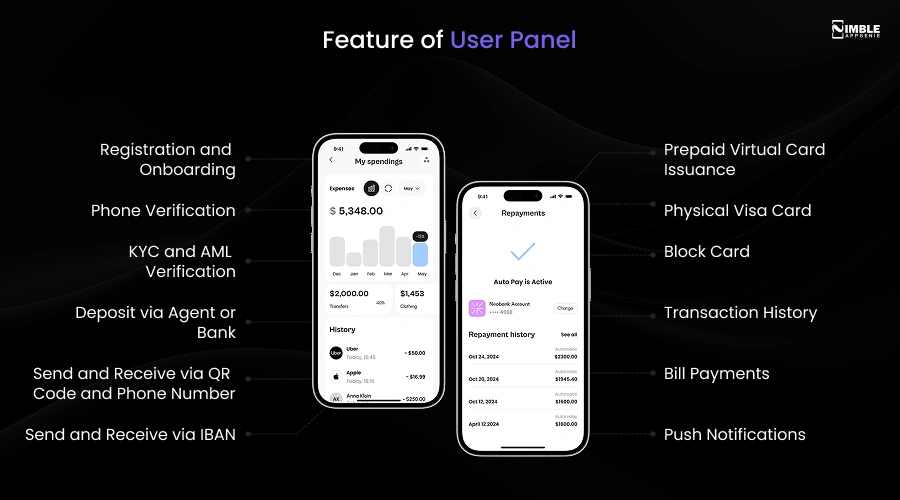

► User Panel

This is what most people interact with. We designed it to work on Android and iPhone devices, work on a slow connection, and take under three minutes to set up.

1. Registration and Onboarding

Users sign up with a phone number, and no bank visit is required. The entire process takes under three minutes.

2. Phone Verification

An OTP confirms the user’s phone number.

3. KYC and AML Verification

Users submit a government ID and a biometric selfie. Identity is verified automatically inside the app through KYC and AML, in real time.

4. Deposit via Agent or Bank

Users add money through a local agent or by linking a bank account. It’s the bridge between the cash economy and the digital one.

5. Send and Receive via QR Code and Phone Number

Type the number, enter the amount, and confirm. QR codes make face-to-face payments even faster.

6. Send and Receive via IBAN

International transfers in and out using the user’s real IBAN. Most people in this market have never had this before.

7. Prepaid Virtual Card Issuance

Free, issued immediately upon KYC completion. Works for online purchases right away.

8. Physical Visa Card

Users who want a physical card can request one. Delivered within 24 hours via ECOBANK Gabon’s logistics network.

9. Block Card

If a card is lost or compromised, users can block it instantly from the app. No call required, no wait.

10. Transaction History

A clear, full log of every transaction. Users see exactly where their money went.

11. Bill Payments

Utility bills, airtime top-ups, and other local services are paid directly from the wallet.

12. Push Notifications

Real-time alerts for every transaction. Users know the moment money arrives or leaves.

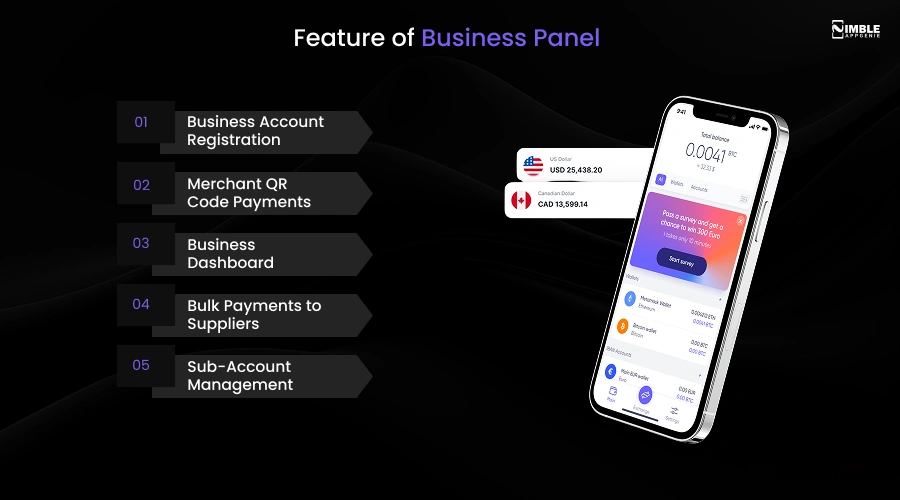

► Business Panel

1. Business Account Registration

Company verification, not just individual KYC.

2. Merchant QR Code Payments

Customers scan and pay. No card terminal needed.

3. Business Dashboard

Real-time view of income, outgoing payments, and balances.

4. Bulk Payments to Suppliers

Pay multiple suppliers in one transaction.

5. Sub-Account Management

Separate accounts for departments, branches, or staff.

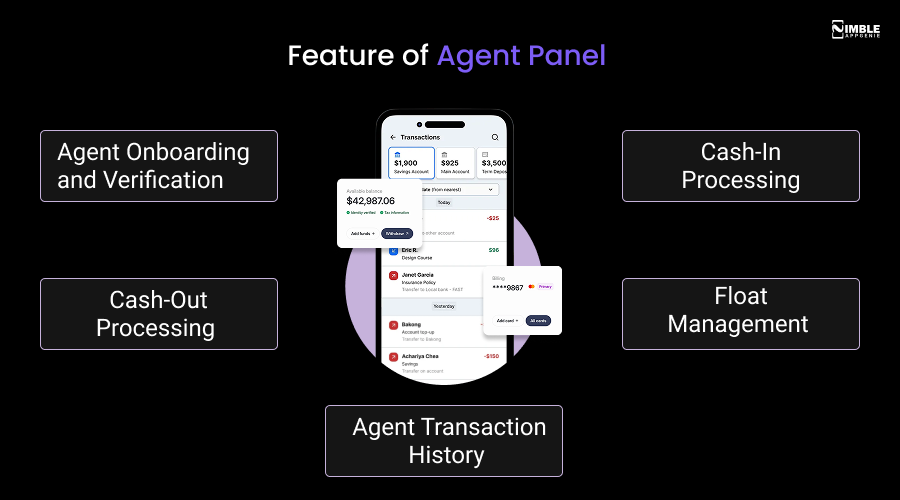

► Agent Panel

An agent is a local shop owner or individual who acts as a cash deposit and withdrawal point. Have a look at the agent panel features:

1. Agent Onboarding and Verification

Agents go through their own verification process, separate from regular users.

2. Cash-In Processing

The agent accepts cash from a user and credits the user’s wallet through the app.

3. Cash-Out Processing

The agent pays out cash to a user who wants to withdraw from their digital wallet.

4. Float Management

Agents track and top up the cash they hold to process withdrawals.

5. Agent Transaction History

A full log of every transaction the agent processes.

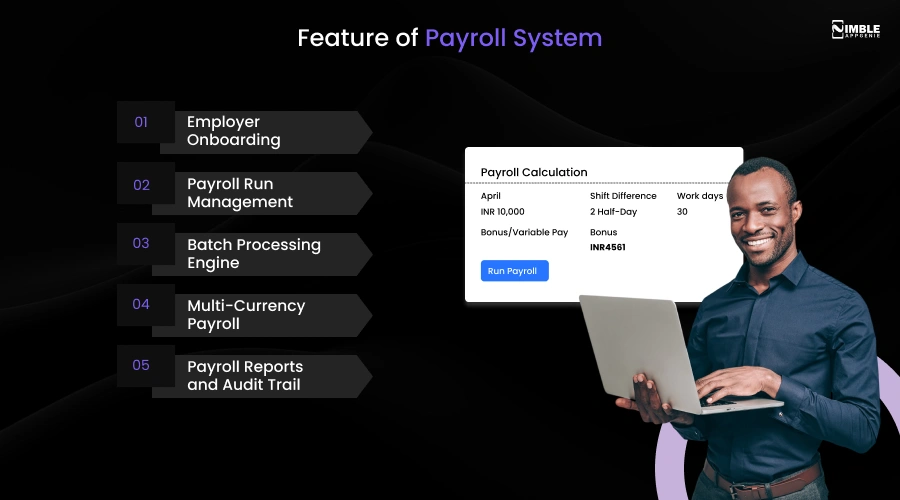

► Payroll System

We created it for employers who need to pay staff across multiple countries and currencies, all at once.

1. Employer Onboarding

Companies register separately with enhanced business verification.

2. Payroll Run Management

Employers create payroll runs, assign employees, and set amounts in one workflow.

3. Batch Processing Engine

One trigger, thousands of payments. The batch engine handles the distribution.

4. Multi-Currency Payroll

Users can pay in XAF, XOF, or both in the same payroll run. The system handles the routing.

5. Payroll Reports and Audit Trail

A full record of every payroll run, exportable for accounting and compliance purposes.

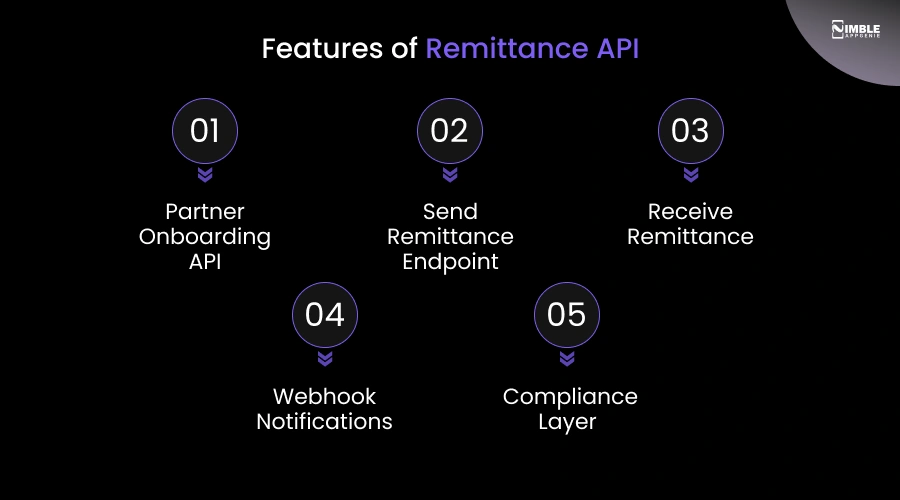

► Remittance API

The Remittance API is a B2B product. It allows licensed partners to integrate with Africa’s multi-currency wallet network to send money into user wallets from outside the platform.

1. Partner Onboarding API

Partners integrate through a standard API with documented endpoints.

2. Send Remittance Endpoint

One API call to send money to any African wallet.

3. Receive Remittance

Users receive incoming transfers from international partners directly into their wallet.

4. Webhook Notifications

Real-time status updates for every transaction. Partners know when transfers succeed or fail.

5. Compliance Layer

It has built-in AML and sanctions screening for every partner transaction.

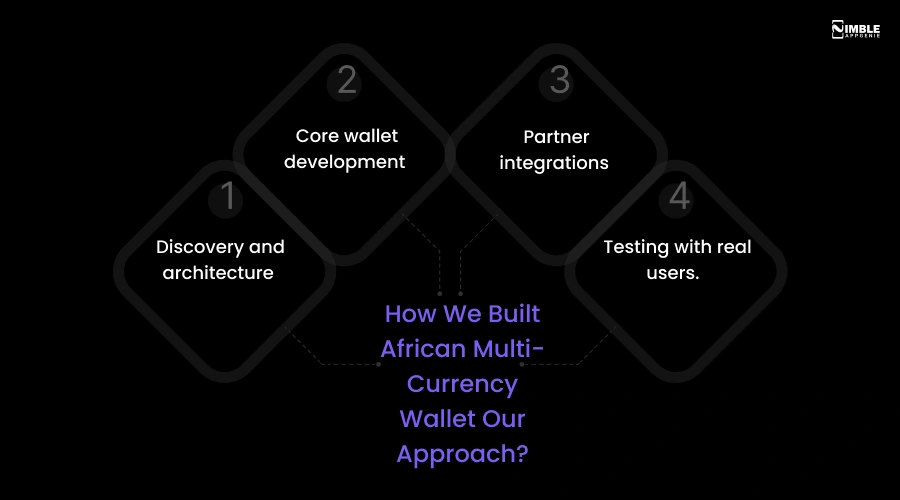

How We Built Africa’s Multi-Currency Wallet: Our Approach?

Nimble AppGenie, an eWallet app development company, built a multi-currency wallet for the African market in four phases.

Every technical decision was tested against one constraint: Does this work on an affordable Android phone? Does this work on a 3G connection? Will it work in a market where the power cuts out mid-transaction? Let’s now see how we have created Africa’s multi-currency wallet.

1. Discovery and Architecture

We started by asking three questions:

- Who is using this app?

- What is their relationship with digital money today?

- What does financial regulation look like in all 14 countries?

- What infrastructure do we need that does not already exist?

The answers were clear. Most users are first-time digital wallet users. Regulations vary by country but share a common KYC and AML baseline. Also, the infrastructure gap, like no Visa card issuance, no IBAN, no agent banking API, meant we had to create or partner for almost everything.

2. Core Wallet Development

Our dedicated development team built the core e-wallet first. Everything else depends on it. The tech stack we use is:

- React Native

- Node.js

- PostgreSQL

- Redis

Every decision ran through one filter. Does this work on a mid-range Android phone, on 3G, with an unrealistic connection? If not, we found another way.

3. Partner Integrations

Three integrations defined what the product could actually do.

- ECOBANK Gabon: Our licensed banking partner for Visa card issuance. Without a licensed bank, there is no card product. We integrated directly with their card management API for both virtual and physical issuance.

- Biometric KYC Provider: Users submit an ID photo and a selfie for two-factor authentication. The system compares them automatically. No manual reviews in the standard flow.

- IBAN Infrastructure Partner: Every user who completes full KYC gets a real, functional IBAN assigned to their account.

4. Testing and Launch

We tested in two stages. Internal QA first, every feature, every edge case, every failure scenario. Then a closed beta with real users in the target markets.

The beta phase showed us things internal tests never could. The navigation patterns we assumed were obvious turned out to be confusing. Flows we thought were fast felt slow to first-time users. We changed things, then tested again.

More than 1000 people registered on the waitlist before the public launch. That was our first confirmation that the product was solving a real problem.

| The single most important decision we made: design compliance from day one. Every feature was built around the regulatory requirement. We did not adjust to fit afterward. That is what made a 14-country rollout possible without rebuilding anything. |

Technology Stack Behind Africa’s Multi-Currency Wallet

We have used the tech stack to create a multi-currency wallet for Africa. Let’s take a look at the tech stack table.

| Category | Technologies / Services Used |

| BACKEND | PHP, Laravel 10 |

| MOBILE APPLICATION | iOS (Swift), Android(Kotlin) |

| USER VERIFICATION & SECURITY | Infobip – WhatsApp OTP Verification

Smile KYC – KYC Verification Smile KYC – AML Screening & Compliance Checks |

| PAYMENT & FINANCIAL SERVICES | GIMAC – Wallet & Payment Services

GIMAC + BDA + Onafriq – Bulk Payment Processing Onafriq – Card Services Integration |

| CLOUD & INFRASTRUCTURE | Microsoft Azure

CloudFront |

| DATABASE | MySQL |

Challenges We Faced During African Multi-Currency Wallet Development & How We Solved Them

The challenges we faced while developing an African multi-currency wallet are:

- Managing two separate currencies within one system

- Running KYC compliance in 14 jurisdictions

- Integrating a physical agent cash network with real-time reconciliation

- Partnering with ECOBANK Gabon for Visa card issuance

- Issuing IBANs for users who have never had a bank account

- Building an app that performs reliably on slow connections

Challenge 1: Multi-Currency Architecture

XAF and XOF share the same value and the same euro peg. But they are separate currencies issued by separate central banks. You cannot use one in a country that runs on the other.

What we did:

We built a currency routing layer between the user interface and the transaction engine. It identifies the origin and destination zone for every transfer and routes it correctly. The user sees a simple payment screen. Behind it, two separate ledger systems are processing the transaction.

Challenge 2: KYC and AML Across 14 Jurisdictions

Compliance was not something we could bolt on at the end. It had to be built in from the start. Each country in the network has its own regulatory requirements for digital financial services. But we needed a baseline that satisfied all of them.

What we did:

We implemented biometric selfie verification combined with document scanning. The user takes a photo of their ID and a selfie. The system compares them, validates the document, and completes KYC in real time.

| Key insight: Compliance and speed are not opposites if you design the flow carefully. The trick is knowing which checks must happen before first use and which can complete in the background. |

Challenge 3: The Agent Network Integration

When an agent accepts cash from a user, three things have to happen at once: the agent’s float is debited, the user’s wallet is credited, and the transaction is logged. Any lag creates disputes and breaks trust.

What we did:

We built a real-time reconciliation layer that processes agent transactions in under two seconds. For poor-connectivity areas, the app queues transactions locally and syncs when a connection returns, with automatic conflict resolution.

Challenge 4: Visa Card Issuance

You cannot issue Visa cards without a licensed banking partner. That is not a technical problem; it is a legal one. And it has to be solved before any technical work on the cards can begin.

What we did:

We partnered with ECOBANK Gabon as the card-issuing institution. Virtual cards are generated via API the moment a user completes KYC, instantly. Physical cards connect to a logistics pipeline: request to deliver in 24 hours.

Challenge 5: IBANs for People Who Have Never Had a Bank Account

An IBAN account or International Bank Account Number is what lets any bank in the world send money directly to you. For most African users, being assigned one was the first time they became a named participant in the global financial system.

What we did:

We integrated with an infrastructure partner who could issue and manage IBANs linked to wallet accounts. Every user who completes full KYC gets one, live and functional for incoming international transfers.

Challenge 6: Building for Low Connectivity

The average smartphone in Gabon or Chad is not a high-end device. Most users are on affordable Android phones, on 3G connections, in areas where signal drops regularly. Developing for this environment meant making deliberate choices:

What we did:

We made four decisions that made the difference:

- Small app size: It is accessible on limited data plans.

- Compressed API calls: Every request is optimised to reduce data usage.

- Offline tolerance: The app queues actions and syncs when the connection returns.

- Clear failure messages: If something cannot complete without connectivity, the app tells the user plainly instead of hanging.

Every challenge here came down to the same thing: stop assuming infrastructure that does not exist. We build for what users actually have, not what you wish they had.

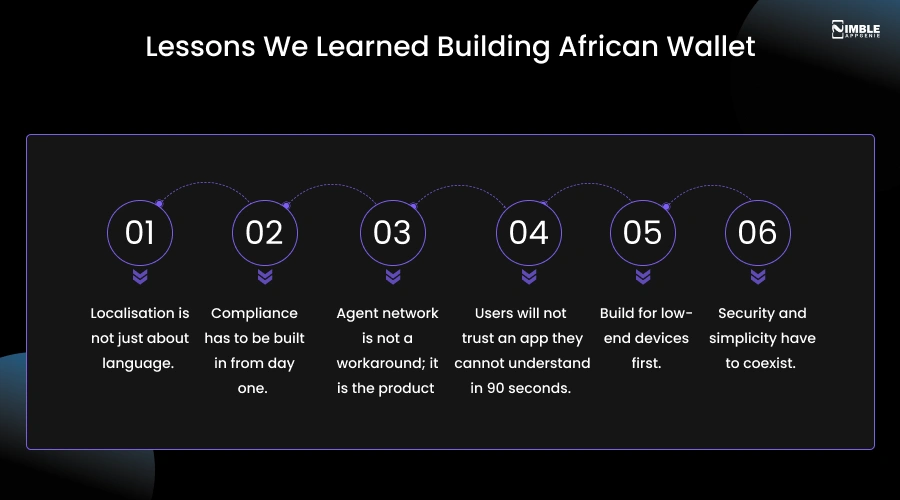

Lessons We Learned Building an African Multi-Currency Wallet

The biggest lessons we learned from building an African multi-currency wallet are that localization goes deeper than language, and compliance must be designed in from day one.

Agent networks are still vital because cash will not disappear overnight. Users will not trust an app they cannot understand in 90 seconds. A licensed banking partner is not optional; it is the legal foundation. Build for low-end devices first, and security and simplicity must coexist; neither can be satisfied.

1. Localization is not just about language

We knew the app needed to be in French. That was the obvious part. What we underestimated was how much else needed to be localised.

For instance, date formats, currency displays, field ordering, and how users expect to see their account number. Every assumption we brought from other markets had to be questioned.

2. Compliance has to be built in from day one

If you treat compliance as something to manage after you have finished multi-currency wallet development, you will rebuild half the product.

We made it a core design constraint from the first day. It costs time upfront. It saved far more time later.

3. Agent network is not a workaround; it is the product

Cash is not disappearing from Central Africa soon. The agent network is what makes a digital wallet useful for people whose income arrives in physical notes.

Without it, you are building a product for the small minority who already have bank accounts.

4. Users will not trust an app they cannot understand in 90 seconds

We tested several onboarding flows. Users dropped off when the app asked for too much too early, or used unfamiliar financial language.

The final version feels almost obvious. Getting there required multiple rounds of testing with real users in the target markets.

5. Build for low-end devices first

If your app works well on a mid-range 2021 Android phone with 3G connectivity, it will work well everywhere. If you build for a high-end device first and try to scale down later, you will be doing that work twice.

6. Security and simplicity have to coexist

Security requirements pushed toward adding friction: more verification steps, more confirmation screens, more warnings. User experience pushed toward removing friction.

We had to find the minimum security footprint that still fully protected users. That balance takes real design work. There is no formula for it.

The Outcome: What African Multi-Currency Wallet Delivers Today?

The African multi-currency wallet is live and operating across its target markets. Over 1,000 people joined the waitlist before the app opened to the public. In a market where fintech adoption builds slowly and trust is hard to earn, that number was meaningful.

The ECOBANK Gabon partnership is live. Virtual Visa cards are being issued. Physical cards are being delivered. What users say most often: it is simple, it is fast, and they trust it.

Those three things do not always go together in a fintech app. Getting all three right in this market, on this kind of infrastructure, was the real fintech development challenge.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.