AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- AI personalization is now a chief product strategy for neobanks, not just a feature add-on.

- Revolut launched AIR, an in-app AI assistant, to 13 million UK users in April 2026. It handles spending analysis, subscription management, card freezing, and travel support.

- Monzo treats fintech app personalization as its newest and most ambitious ML investment area, covering lending, credit, savings, and spending insights across 14 million customers.

- Chime reduced cost-to-serve by nearly 30% and increased revenue per active member by 23% over three years by embedding AI across its platform.

- More than 750 digital-only banks worldwide now serve 1.8 billion customers. According to Accenture’s 2025 Banking Consumer Study, these neobanks are setting the benchmark for both convenience and personalization, and traditional banks have not distinguished themselves on either front.

- Nimble AppGenie helps fintech startups and enterprises build AI-powered mobile apps that close this personalization gap, from smart dashboards to ML-based financial coaching.

- The blog is aimed at fintech founders, product managers, and digital banking decision-makers considering AI integration.

More than 750 digital-only banks worldwide now serve 1.8 billion customers. According to Accenture’s 2025 Banking Consumer Study, these neobanks are setting the benchmark for both convenience and personalization, and traditional banks have not distinguished themselves on either front.

Budget is not the reason here. Most large banks overspend on technology for neobanks. So, the remaining cause is architecture and how they utilize the data they already hold.

AI personalization in fintech apps is where Top digital-first financial technology companies, Revolut, Monzo, and Chime do things differently. They didn’t add AI personalization on top of an existing system. They created their products around it.

AI personalization has become a defining trend across the Global FinTech Market, with digital-first financial technology companies such as Revolut, Monzo, and Chime building their platforms around intelligent, personalized user experiences rather than simply adding AI capabilities to existing systems.

Every in-app action, transaction, and saving goal feeds the model. As a result, AI personalization in banking apps makes the user experience smarter with every use.

This blog breaks down exactly what these three neobanks do with AI personalization in fintech apps – what they built, what fintech builders can learn from it, and what the numbers show.

What AI Personalization in Banking Actually Means

Let’s make it simple. AI personalization in banking means the app changes what it recommends to you or what it shows you based on your individual behavior, specifically you, not a segment of users like you.

The data inputs are: spending categories, transaction history, saving goals, income patterns, in-app navigation behavior, and sometimes external signals like time of the day or location. The AI processes all of this and makes decisions, usually through machine learning models, about what to come up with next.

In practice, outputs look like: a savings challenge tailored to your income cycle, a notification that your grocery spending is up 40% this month, an assistant that knows you always buy travel insurance before a trip and prompts you before you even think to ask, or a credit limit adjustment based on how you have managed money over the past year.

The business case is powerful. McKinsey data reveals that financial institutions that invest in AI personalization witness 10-20% increased customer lifetime value. This is a survival metric for neobanks running on thin margins.

Now, here is how Revolut, Monzo, and Chime each approach it differently.

Revolut: From Proprietary AI Infrastructure to In-App Intelligence

This section will answer your question: How does Revolut use AI to personalize the user experience? Revolut has 70+ million retail customers globally across 40+ countries.

That figure indicates it generates a large amount of behavioral data every day, and in 2025 and 2026, the company made two important moves to reap its benefits.

► AIR: Revolut’s In-App AI Assistant

In April 2026, Revolut launched AIR, an in-app assistant, to 13 million UK customers. AIR is the first consumer product created by Revolut’s dedicated internal AI unit.

AIR, Revolut AI assistant manages investment tracking, spending analysis, card freezing, subscription management, in-app eSIM purchases, and travel support. It works within the app, leveraging only the data the customer can already see, like their card transactions and investment holdings.

Revolut has a zero data retention policy with any third-party AI providers empowering AIR. Sensitive acts, like moving money or freezing a card, need biometric approval before they are executed. Well, the company hasn’t revealed which AI providers strengthen the product.

| Is Revolut’s AI assistant available to all users? AIR is not available globally yet. As of April 2026, it is in the UK rollout. Revolut’s co-founders first defined the vision at their Revolutionaries event in November 2024. UK CEO Francesca Carlesi confirmed publicly in June 2025 that the launch was close. |

► PRAGMA: Revolut’s Foundation Model

In April 2026, Revolut published PRAGMA – a family of encoder-style transformer foundation models trained on banking event data, which doesn’t contain personally identifiable information. Their dataset is from 26 million user records spanning 111 countries, collecting 24 billion events that total 207 billion tokens.

Most fintechs and banks use separate, task-specific models for things like fraud detection, credit scoring, and product recommendations. Every model is created and maintained independently, which is expensive and slow.

PRAGMA replaces that with a single shared backbone. There’s just one model adapted across tasks. The outcome beat Revolut’s internal baselines: +130.2% lift in Credit Scoring PR-AUC, +64.7% improvement in Fraud Recall, and +79.4% gain in Communication Engagement PR-AUC.

In plain text, this means Revolut’s AI is now good at anticipating who will default on a loan, identifying fraud before it happens, and knowing which product to offer to which user, all from the same underlying model.

► The Business Outcome

The results show up in the numbers. In 2024, Revolut expanded its customer base by 34% year-on-year while increasing customer support costs by just 5%. That gap, the growth without a promotional cost boost, is what a mature AI personalization in fintech apps yields.

Revolut also leverages behavioral data to personalize email and push notifications; users tracking crypto get price-threshold alerts; frequent international travelers get fee-free transaction offers. It’s not generic, but specific.

Monzo: Making Intelligence Feel Invisible

| Monzo’s 14 million customers spent £19 million on AI platforms, like OpenAI, in 2025, 85% year-on-year up from £8 million in 2024. That investment reflects how heavily Monzo is betting on personalization systems. |

Monzo’s stated objective for ML is specific: make intelligence feel invisible. The goal is to hide ML complexity behind a product experience that simply works. That framing transforms everything they build.

► Where Monzo Uses ML

According to Monzo’s 2025 ML blog, Monzo’s machine learning investment covers five areas: financial crime operations, fraud detection, customer operations, credit decisioning, and personalization, their newest area.

The fintech app personalization work spans each product vertical: credit limits, lending, investments, and savings. The goal is to customize pricing, limits, and advice to every individual’s situation, not only to a user’s category.

► What Personalization Looks Like in the Monzo App

Monzo’s spending insights feature automatically sorts transactions and tracks budgets without the user having to set anything up. According to Monzo’s report, this feature is used by 70% of its customers, a remarkably high adoption rate for a financial tool that requires no manual setup.

How do fintech apps use machine learning for savings recommendations? Let’s consider this app to answer this.

Monzo’s Pots features allow users to create named savings goals within the app. What makes this captivating from an ML perspective: Monzo leverages unsupervised machine learning to analyze how users name their Pots – ‘New car,’ ‘Holiday fund’, or ‘Emergency buffer’, and uses those signals to offer personalized savings recommendations in banking apps and investment tips.

These small signals lead to high-value output. In January 2026, Monzo released Year in Monzo – a personalized annual spending summary inside the app, broken down by quirks, quests, and money habits.

It covered categories from AI platform spending to everyday travel to live entertainment.

► ML in Operations

On the support edge, Monzo uses ML to direct customer queries and suggest optimal responses to support agents in real time. This accelerates resolution without completely removing the human intervention, which matters when customers are dealing with financial stress.

| Monzo’s personalization is built to be invisible. The user doesn’t configure it. They don’t see the model. They just get a notification, an insight, or a recommendation that actually makes sense for them. That is the product standard Monzo is building toward. |

Chime: AI as a Cost Lever and a Growth Engine

Chime went public on Nasdaq (ticker: CHYM) in June 2025 at a fully diluted valuation of $11.6 billion. Full-year 2025 revenue grew 31% year-over-year to $2.2 billion, exceeding the company’s guidance.

How is Chime using artificial intelligence?

Over the past three years, by leveraging AI, Chime diminished cost-to-serve by about 30% and boosted revenue per active member (ARPAM) by 23%, all while boosting customer satisfaction scores. That’s a rare combination: lower cost and better experience at the same time.

► How Chime Built AI Into Its Core

Chime processes 1+ billion transactions every year, and that data feeds directly into its personalization models continuously, but not as a batch job. The infrastructure powering this is ChimeCore, Chime’s proprietary technology platform.

AI is not bolted on as a feature, but embedded at the platform level. In 2025, Chime launched generative AI voice and chatbots for member support. Today, more than 70% of member support interactions start with AI-powered self-service.

Resolution rates improved from 50 to 70%, meaning more than two-thirds of customer questions are now resolved instantly.

► The Financial Health Score

Chime’s AI-powered Financial Health Score is a clear example of how they think about fintech app personalization differently from the other two. Besides tracking spending, it looks at the complete picture of a member’s financial situation – savings, spending, income, and credit and surfaces a score with particular, actionable recommendations.

The target is not just engagement, it’s financial results. Chime’s target is to help Americans check their financial progress. For that, Chime AI features are built that go beyond just showing impressive metrics on a dashboard.

► AI Across the Organization

90% of Chime employees use AI every week across product, engineering, and marketing. Chime’s co-founder Ryan King framed this directly. AI is a superpower, and those who use it to serve users better will be the winners.

Chime also leverages AI to automate A/B testing and content personalization in marketing, minimizing dependencies on external agencies and reducing turnaround times. This has resulted in millions of dollars in cost savings.

| Chime’s approach is worth exploring because it treats AI as infrastructure, not a feature set. The personalization in fintech apps is a fundamentally different architectural decision. |

Revolut vs Monzo vs Chime AI Comparison: What Each Does Differently

Fintech brands often ask: What is the difference between Revolut, Monzo, and Chime’s AI approaches?

Here’s the answer.

| Revolut | Monzo | Chime | |

| AI Focus | Proprietary foundation model (PRAGMA) | Invisible ML product integration | AI as a cost and growth engine |

| Key Feature | AIR in-app assistant (April 2026) | Spending insights, Pots, Year in Monzo | Financial Health Score, AI voice/chatbots |

| Data Scale | 40B events, 25M users (PRAGMA training) | ML across 14M customers | 1B+ transactions per year |

| Business Outcome | 34% customer growth, 5% support cost growth | £1B+ revenue, 70% engagement on spending insights | 30% cost-to-serve reduction, 23% ARPAM increase |

| Primary Market | Global (70M users, 40+ countries) | UK, expanding to the EU | US (mainstream Americans) |

Which neobank has the best AI features overall?

Well, no single neobank wins on all the dimensions. Each has a distinct strength, and each reflects a different philosophy about what AI personalization in fintech apps is for.

Revolut is building AI at the infrastructure level, a base model that handles fraud, credit, and recommendations from a single backbone.

Monzo aims to make that intelligence disappear into the product experience.

Chime is leveraging AI to close the gap between what users want and what the bank can deliver profitably.

If you are earlier in the process and still mapping out your product, our guide – everything you should know about neobank app development covers the full stack from compliance to core banking integrations.

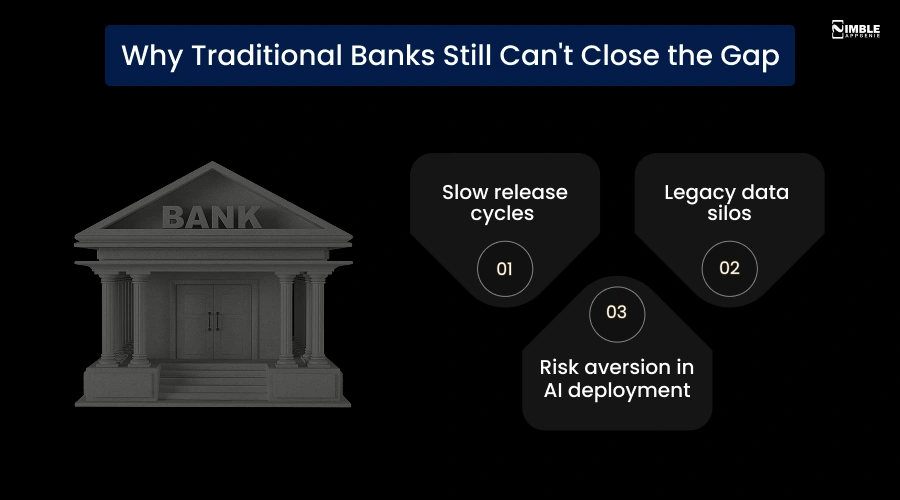

Why Traditional Banks Still Can’t Close the Gap

The 73% vs 22% personalization gap is not a budget issue. Most large banks invest more in technology than all three AI-powered neobanks combined. The problem is structural.

1. Slow release cycles

Neobanks ship features in days, while traditional banks take months per release because of the approval, testing layers, and compliance involved. By the time a personalized feature reaches the customer, the insights that triggered it are old.

2. Legacy data silos

Most traditional banks have data spread across dozens of disconnected systems, including CRM platforms, core banking systems, card processors, and loan origination tools. The data exists, but you can’t build real-time personalization on top of systems that batch-process overnight.

3. Risk aversion in AI deployment

Because of the regulatory pressure, banks are more cautious about AI deployment in credit decisions or financial advice without deep validation. Neobanks face the same regulations, but they built their compliance functions with AI in mind from day one.

Monzo and Revolut both maintain dedicated compliance engineering teams that align AI models with shifting regulations on a frequent basis.

This is not a permanent benefit for neobanks. Traditional banks can close this gap, but it needs architecting their data layer, not only adding an AI layer on top of what already exists.

Neobank Vs Traditional Bank AI Experience

Traditional banks have the data but not the architecture to act on it. Neobanks were built mobile-first with connected data systems from day one. That difference shows up directly in the fintech user experience AI.

| Traditional Banks | Neobanks | |

| Data systems | Siloed, disconnected | Unified, real-time |

| Feature release | Months | Days |

| Personalization | Generic, segment-based | Individual, behavior-driven |

| AI integration | Bolted on | Built in from day one |

| Support | Human-first | AI-first, human backup |

| Compliance + AI | Sequential | Built together |

What Fintech Builders Can Take From This

If you want to build a fintech product, here are four things you should take seriously from how the three neobanks work.

1. Personalization Is Architecture, Not a Feature

Chime’s outcome comes from embedding AI at the platform level, ChimeCore, not from adding a personalization widget to an existing app. If you are building something new, design the data layer keeping personalization in mind from the start, as considering it later is slow and costly.

2. Start With What’s Visible

Monzo’s spending reports have 70% adoption because they need nothing from the user; they just work. Start with neobank AI features that deliver value automatically, such as spending categorization, anomaly alerts, and budget tracking.

These build trust. Once users trust the app’s intelligence, they accept more sophisticated personalization.

3. Small Signals Matter

Monzo utilizes unsupervised ML to determine how users name their savings Pots. This is not a big data stream; it’s a small text signal. But it unveils intent.

Look for low noise, high-signal data points in your AI product and build models around those before going after complex behavioral datasets.

4. Measure Personalization in Business Outcomes

Chime doesn’t only measure NPS or engagement, they measure revenue per active member and cost to serve. If your personalization feature doesn’t show up in retention, ARPU, or support cost reduction, they are not working yet.

Create the measurement framework before you build the features.

What This Means If You Are Building a Fintech Product

The gap between what users want and what most apps deliver is still wide. If you are closing that gap with a new product, Nimble AppGenie’s AI consulting services can help you move from concept to production faster.

Revolut, Monzo, and Chime have years of data, dedicated ML teams, and billions in revenue to fund their AI work. But most fintech startups don’t have that runway.

The architecture decisions these neobanks made are not exclusive to companies of their size. The same principles, like connected data pipelines, behavior-driven features, and AI, are embedded at the platform level rather than bolted on and can be applied from day one on a much smaller budget, if the product is built the right way from the start.

That is what Nimble AppGenie, a fintech app development company, does. We build fintech mobile apps with AI personalization engineered into the core, building spending intelligence, ML-based recommendations, smart notifications, and financial health features not added as an afterthought once the product is live.

Whether you are building a neobank, a personal finance app, or an AI-powered financial tool, the decisions you make in the first few months of development will determine how much the product can grow. Getting the architecture right early is far cheaper than rebuilding it later.

If that is where you are, early stage, scoping your product, or rethinking what you already have, get a free 30-min consultation from our mobile app development team. We can help you scope the right AI architecture for your fintech product before you write a single line of code.

The Bottom Line

The neobank personalization race is not slowing down. Revolut is expanding AIR beyond the UK. Monzo is moving its ML work into lending and investments. Chime is scaling ChimeCore to support a growing member base that now surpasses 9.5 million active users.

For anyone building in fintech today, the gap between what these products deliver and what traditional apps offer is going to get wider. Users who experience products like Monzo’s spending insights or Chime’s Financial Health Score are less likely to return to static banking experiences.

The question for builders is not whether to add AI personalization. It is when and whether you build it in from the start or try to add it later, which is expensive and slow.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.