In a Nutshell:

- Open-loop payment systems allow users to pay with cards, mobile wallets, or bank accounts.

- These systems are used in public transport, retail, and smart cities because they support multiple payment providers.

- One of the biggest challenges of open-loop payment implementation is infrastructure upgrade and coordination among stakeholders.

- User adoption and technology compatibility play a key role in the success of open-loop payment solutions.

- When implemented correctly, open-loop digital payments improve convenience, reduce cash usage, and support scalable payment ecosystems.

Cash usage has declined when it comes to basic payments, as people now keep their debit and credit cards handy. Instant payments have also revolutionized the way users make payments.

Amid all these changes, if there’s one thing that has improved the experience, it’s open-loop payment systems.

Open-loop payment systems are found worldwide, enabling swift, digital payments. One of the most insistent uses of the open-loop payment system is in public transportation. Several governments are working on finding ways to implement it effectively.

In this blog, we will explore open-loop payment systems and try to understand how they work. We will also try to unravel some of the global trends around open-loop payments and their benefits.

Without further ado, let’s get started!

What is an Open Loop Payment System?

An open-loop payment system is an arrangement that allows a user to make payments with any resource, irrespective of it being from the same financial institution.

This means that irrespective of which bank the payment is made from, it will be settled in your account easily. With open-loop payment systems, you can make transactions between accounts from different banks, cards, or wallets.

The system is widely accepted across the globe and is used for a variety of payment methods such as credit cards, debit cards, prepaid cards, gift cards, etc. The best thing about this system is that it allows a merchant to process payments irrespective of which financial institution the payer uses.

Similarly, for the payer, it is easy to use any debit/credit card to make the payment, irrespective of which bank the payee uses.

With open-loop payment systems, daily transactions such as public transportation, grocery shopping, etc., become super convenient. Even the best mobile banking apps support open-loop payments as they open a new horizon for their users.

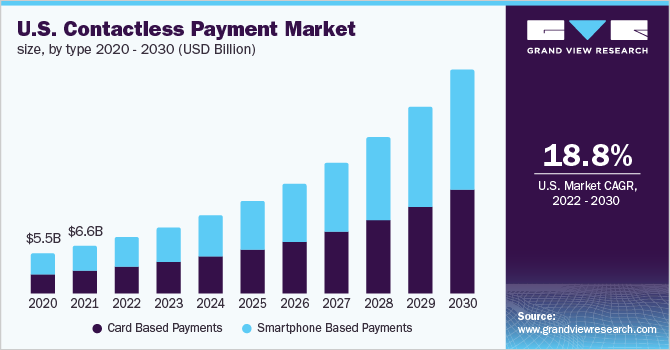

Market Statistics of Open-Loop Payments

- Despite multiple challenges, the usage of open-loop payment solutions has increased over the years. Not only that, according to a report, the entire payments market is expected to grow at a CAGR of 19.1% from 2022-2030.

- One of the most popular use cases of these systems is public transportation across the globe. So much so that around 150 cities across the world are planning to adopt an open-loop payment system by replacing the traditional legacy ticketing system.

- The number of open-loop payment cards used for ticketing is forecast to reach a whopping 136.9 million by the end of this year (2025). It says a lot about the global adoption of open-loop payment technology.

- As far as digital payments are concerned, according to a survey, 2 out of every 3 people are likely to use a contactless payment mode either with their credit/debit cards or with a prepaid card that is not directly linked to their bank account.

Global trends in open-loop payments say that all the countries are ready to adopt the idea of implementing open-loop payments, and there is no doubt that if you own a business, you should implement the same too.

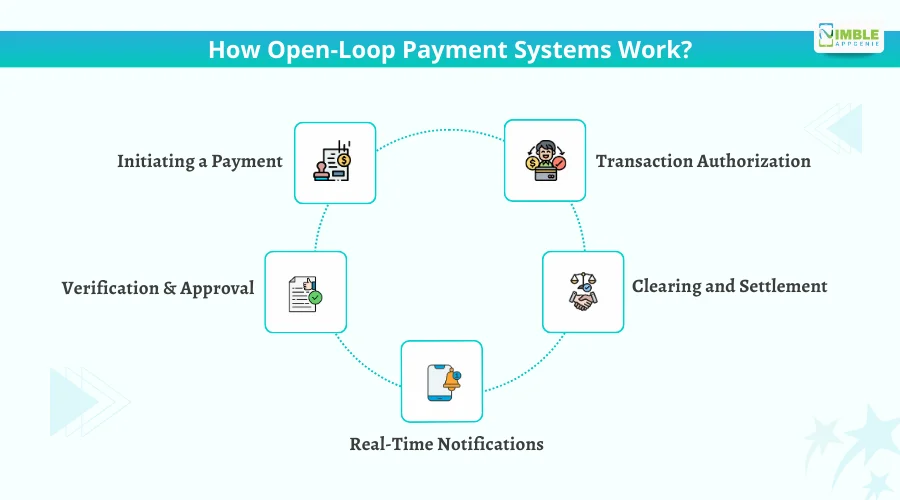

How Open-Loop Payment Systems Work?

The open-loop payment system relies on a real-time payment network, popularly known as the RTP network. This is because the payments settle in real-time and funds are available to use instantly.

An open-loop payment system allows users to make payments using credit cards, debit cards, etc. using a shared network.

Let us take a quick look at the steps involved in an open-loop payment system –

1. Initiating a Payment

To initiate a payment, the cardholder must tap the card at the terminal. This card can be any debit, credit, or prepaid card as per the convenience of the user.

Keep in mind that the card being tapped should be using one of the authorized card payment networks.

2. Transaction Authorization

Once the card is tapped, transaction details are sent to a payment gateway via a transaction processing system, where the information is encrypted for further authentication.

Usually, transactions made with a tap require no authorization from the customer as they have a set limit up to which they can make a transaction contactlessly.

3. Verification and Approval

The encrypted information is shared with the card network to verify with the bank. The bank simply checks the account information and matches it to the customer’s details.

It then verifies if the amount requested is available in the account. After all the checks are done, the transaction is approved.

4. Clearing and Settlement

The funds are cleared by the customer’s bank and settled into the merchant’s account after the entire verification and approval process.

It simply means that the payer has enough funds to transfer and the difference between the merchant’s existing funds and the added funds is settled.

5. Real-Time Notifications

All of it happens in real-time, keeping both the merchant and customer in the loop. The entire process is so quick that it only takes a few seconds to get the confirmation of payment.

These real-time transaction notifications make the entire process relatively reliable as the amount is available to use instantly!

This is how open-loop payments work. Each step signifies a status and hence is crucial for the entire process.

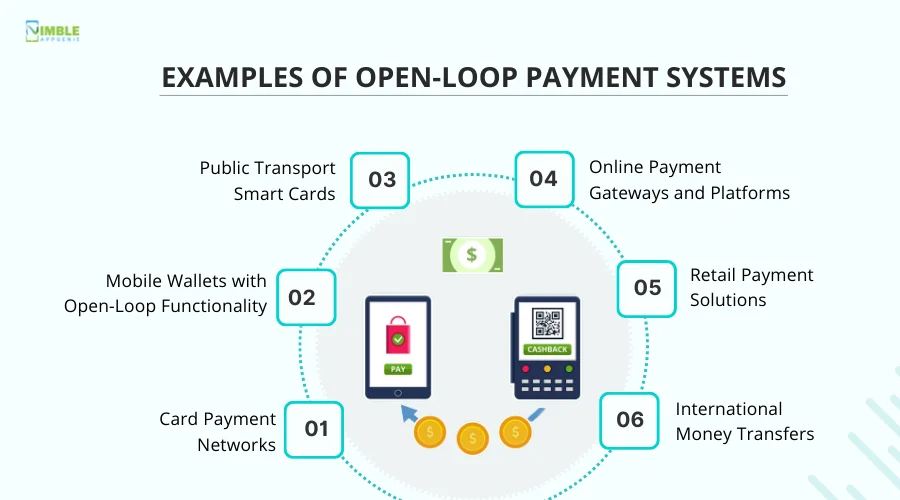

Examples of Open-Loop Payment Systems

Now, you may be wondering what are some examples of open-loop payment systems. Well, we have all used open-loop payments in one way or another.

Let’s take a look at some of the everyday examples where open-loop payment systems are commonly used.

1. Card Payment Networks

The first and foremost example that comes to mind is card payment networks. You see, it is impossible to use a closed-loop payment system when it comes to debit/credit cards.

That is because not every customer may have a card associated with the same bank that you use. Hence, the implementation of open-loop payment solutions is crucial. To support this, card networks such as Visa, Discover, Mastercard, and American Express facilitate the transactions.

Today, you can find translation machines that support both Visa and Mastercard payments, irrespective of which banks have issued those cards.

2. Mobile Wallets with Open-Loop Functionality

With digital payments making their way into everyday life, several mobile wallets currently support open-loop functionality. These wallets simply allow a user to send money and make a transaction from their wallet to the receiver’s wallet, irrespective of which payment application they use.

The best examples of mobile wallets with open-loop functionality are Apple Pay and Google Pay Wallet. Any user can simply add their cards to these wallets and then use any outlet to make payments. This helps make payments super easy for the users, as all they have to do is tap!

3. Public Transport Smart Cards

Public transport smart cards are another great example of using open-loop payment systems. The convenience of using a single card for all your transportation needs comes from implementing open-loop payment systems.

The best way to enable a hassle-free experience for a traveler is to keep them free from unnecessary queues and give them a quick ticketing solution.

The open-loop payment system meets all these requirements, making public transport smart cards the best way to travel around.

4. Online Payment Gateways and Platforms

With online payment gateways and platforms being powered by open-loop payment systems, the possibilities for businesses have become endless.

Users can easily use the payment of their choice, and merchants can accept payments from anywhere in the world, irrespective of what financial institution the user is associated with.

By integrating an online payment gateway, even the smallest of businesses can enable payments conveniently.

5. Retail Payment Solutions

Retail payment solutions that allow merchants to accept payments from more and more banks are the perfect example of open-loop payment solutions. Being a retailer, one cannot imagine the number of transactions they have daily.

Now, among those transactions, if a retailer is only allowed to accept payments from a certain financial institution (like in closed-loop payments), then he/she will have to bear a lot of loss, considering not every consumer will be using the same bank.

However, thanks to open-loop payment infrastructure, a retailer can use a single payment machine to process them all!

6. International Money Transfers

International money transfers have always been a point of contention for several businesses, as they often cannot find a simple way to go through with them. Thankfully, with open-loop payment solutions, merchants can simplify international transactions.

This is possible as the card payment networks used on open-loop platforms are not limited to a single country or region. They are accessible throughout the world, helping the system enable international money transfers.

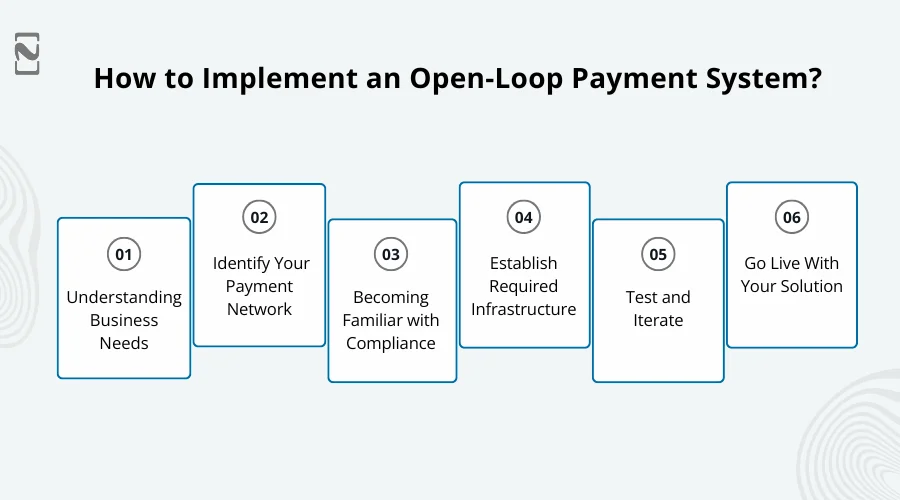

How to Implement an Open Loop Payment System?

To implement open-loop payments in your business, you need to have clarity on how your business can use them and how you can make the most of them. Once you are sure that it will be a beneficial decision, you can move to implement the solution.

Here are the steps you need to take for a proper open-loop payments system implementation –

Step 1: Understanding Business Needs

When implementing any payment system, be it a closed-loop or open-loop, the first step you need to take is to identify the current needs of your business.

Identify where exactly in your business you need open-loop payment systems are required. The more clear you are about the implementation, the better results it can yield for you.

Step 2: Identify Your Payment Network

To implement an open-loop payment system in your business, you need to have a payment network that gives you the ability to accept payments.

Potential payment networks can be Visa, MasterCard, or PayPal, depending on your requirements. When choosing a payment network, make sure they have global exposure, unbreachable security measures, and friendly transaction fees for better results.

Step 3: Becoming Familiar with Compliance

Before implementing an open-loop payment system, it is crucial to understand the regulatory requirements it requires. The system you integrate must be compliant with PCI DSS, a standard for secure card payments.

This is only one of the many different compliance requirements that may be required when implementing an open-loop payment system.

Step 4: Establish Required Infrastructure

After you have understood the requirements and identified key partners in finding the right open-loop payment system partners, it is time to build an infrastructure that allows smooth integration.

You need a payment gateway, an app that gives you insights into the regular transactions, and a POS software that allows your users to interact with the open-loop payment system that you have implemented.

You can find an outsourced fintech development partner to guide you with a custom solution, or you can find an existing third-party tool that gets the job done.

Step 5: Test and Iterate

Once you have got yourself an infrastructure to host open-loop payment services, the implementation is almost ready to be deployed.

The only thing you need to do is test the entire system and iterate on user feedback to achieve an optimal performance. This testing will help you understand the degree of efficiency.

When you have custom development experts, you can simply share your feedback, and they can make the changes, whereas with third-party software, changes based on feedback can be limited.

Step 6: Go Live With Your Solution

With all of that, it is now time to make your open-loop payment system “open” for all! Go live with the solution that you have implemented and start using the system to identify its potential.

You can tweak the system as per your everyday usage, making it more customized to your needs. Using the solution will provide you with better insights into its effectiveness.

By performing these steps, you can get your hands on a well-defined open-loop payment system, allowing your business to make the most out of existing payment methods, while making it easier for the customers to stick to their preferred mode of payment.

What Are the Benefits of Open-Loop Payment Systems?

An open-loop payment system, when implemented properly, can do wonders for any merchant. From basic retail payments to public transportation, everyone around the globe is using open-loop payment systems.

There is no doubt that there are several benefits of open-loop payment systems.

Some of the most common benefits that you may find include –

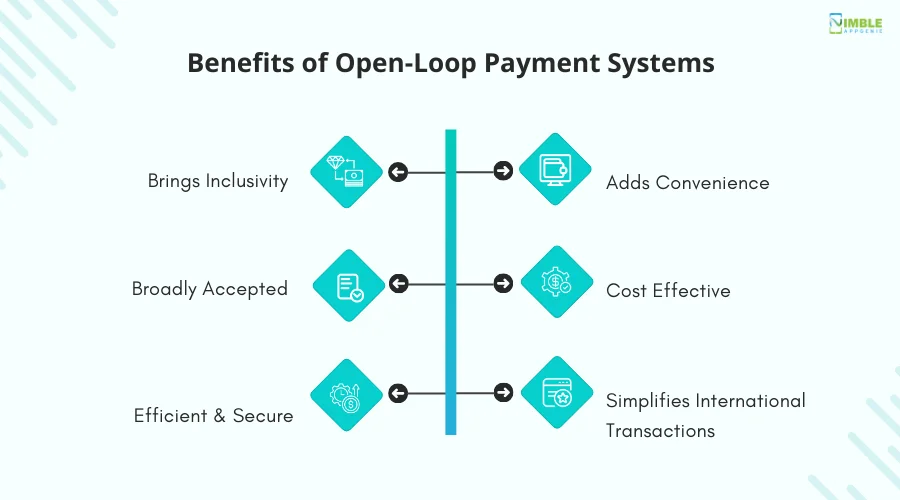

1] Brings Inclusivity

Open-loop payment systems allow every individual who uses a card or a digital mode of payment to transact, making it a completely inclusive system.

You do not have to be a dedicated member of any bank or organization to be able to access the system; it is inclusive and open for all!

2] Adds Convenience

With open-loop payments, you have the flexibility of making payments anywhere without having to worry about unnecessary details.

Being able to pay for anything with your account, regardless of what bank the receiver uses, is a big convenience that open-loop payment systems offer.

3] Broadly Accepted

Open-loop payment systems are accepted by merchants globally, making it easier for consumers to buy goods and services anywhere in the world.

For example, if you are in a different country and only have a card to make all your payments, you can do the same at any merchant, thanks to open-loop payments.

4] Cost-Effective

Handling cash is not as easy as it appears. There are several types of costs that a merchant has to bear. Not only does this reduce the cost involved in cash handling, but it can also reduce the land cost of any ticketing infrastructure.

Simply enabling an open-loop payment system can help in reducing the handling charges, along with different infrastructure costs to nil.

If you get proper support from professionals, it may take you less time and cost to develop an e-wallet app that offers an open-loop facility than your legacy payment system.

5] Efficient & Secure

The method is efficient as it works on a shared network like the RTP network. This means that payments are settled in real-time, with instant confirmation from the associated banks and financial institutions.

The entire process uses the best encryption and security features, such as tokenization, fraud detection, etc., making it secure and safe in real-time.

6] Simplifies International Transactions

One of the key benefits of using open-loop payment systems is that it enables international transactions smoothly. A merchant can easily accept payments from a card belonging to a person from another country as long as they are on the same card payment network.

This has opened doors for even the smallest of businesses to reach a wider audience with the help of cross-border open-loop payments.

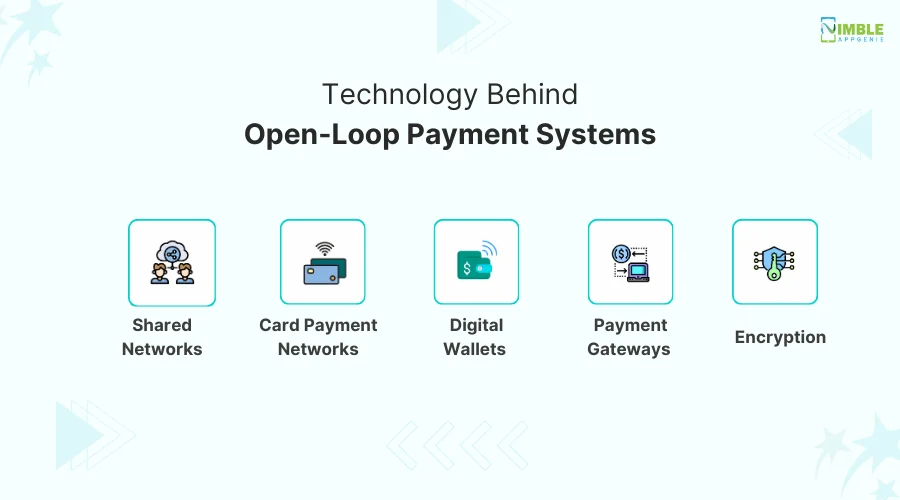

Technology Behind Open-Loop Payment Systems

Reading about the benefits of open-loop payment systems might have gotten you curious about the technology behind open-loop payments. Well, there are a bunch of different technologies and APIs that enable this system to work seamlessly.

These include:

1. Shared Networks

Shared networks such as RTP are necessary for these transactions to go through. These networks provide a common ground for all the steps involved in the mobile payment process and are available 24/7 to ensure that every payment goes through, irrespective of banking hours.

2. Card Payment Networks

Card payment networks such as Visa, Mastercard, Discover, American Express, etc. serve as the middleman between the cardholder’s bank and the merchant’s bank. These networks connect with the financial institution associated with the card for authorization of payments.

3. Digital Wallets

Open-loop payment technology is convenient to use as it can be used anywhere. Digital wallets offer an interface to this virtual platform that can be used to save all the payment information and cards to practically make a payment without carrying your physical card or wallet.

The e-wallet app features do not end here, as it can also allow a user to make transactions without even exposing their current bank details, keeping them completely safe from fraud.

Also Read: How to Create a Digital Wallet App?

4. Payment Gateways

Similar to offline point-of-sale terminals, payment gateways are online services that allow a merchant to accept payments directly into their bank account.

These gateways serve as a bridge between the merchants and their banks, allowing the customers to directly make payments to them, irrespective of what financial institution they are associated with.

5. Encryption

Encryption is one of the most important components of an open-loop payment system. This is because it ensures that delicate information, such as your credit card details, banking information, etc., stays intact in the network. It converts all the information into code so that it stays intact from unauthorized access.

All of these, when combined, can help you implement an open-loop payment system that is robust and highly efficient. You always have the option to integrate newer technologies into the system to make it more effective.

API integration for open-loop payment technology is significantly easier for any development professional, hence it is simple to implement as well.

What Are the Challenges in Implementing Open-Loop Payment Systems & Solutions?

While the open-loop approach for payment seems the ultimate solution to all the hassle, it is not easy to implement. Several challenges often cause issues in the implementation of open-loop payment systems.

Let’s take a look at some of them:

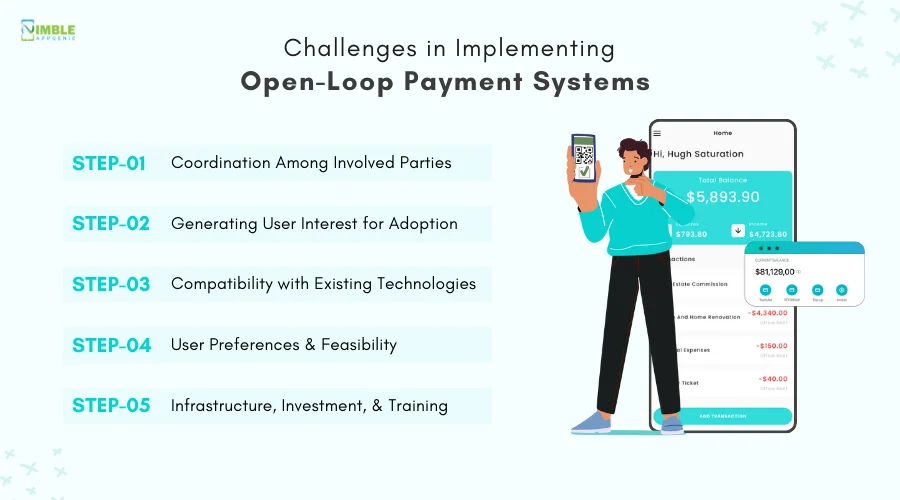

Challenge #1: Better Coordination Among Parties

To solve coordination issues, all involved parties need a common framework. Banks, payment networks, service providers, and merchants should follow shared rules and standards.

Additionally, using well-known payment networks and APIs can help different systems talk to each other easily. Also, regular meetings, clear roles, and legal agreements can help avoid confusion and delays.

Challenge #2: Increasing User Adoption

User adoption improves when people clearly understand the benefits. You can take simple steps like faster payments, shorter queues, and no need to carry cash.

Pilot programs, awareness campaigns, and on-the-ground support can help users slowly adapt. You can offer both old and new payment options during the early phase to make the transition easier.

Challenge #3: Handling Technology Compatibility

To overcome compatibility issues, your systems should support multiple payment methods. You can include cards, QR codes, wearables, and basic mobile phones where possible.

Instead of forcing users to upgrade devices, service providers can design flexible systems that work with both old and new technologies. This ensures no user is left out.

Challenge #4: Respecting User Preferences

User comfort should always come first. Open-loop payments should be optional, not mandatory. You should allow users to choose between tickets, cards, or digital payments to build trust.

Additionally, clear instructions, simple interfaces, and visible help points can reduce hesitation in crowded or public spaces.

Challenge #5: Managing Infrastructure, Cost, and Training

A phased rollout helps reduce cost and risk. Instead of replacing everything at once, you can upgrade the infrastructure step by step.

Besides, staff training should focus on basic system handling and issue resolution. You can partner with experienced payment providers that can reduce your investment burden and ensure compliance with regulations.

While the challenges may vary in different regions and sectors, the benefits do stay the same; implementing open-loop payment systems is a must for every merchant with an online/offline store.

How Nimble AppGenie Can Help Develop Open-Loop Payment Solutions?

The future of open-loop payment technology is all set to take the world by storm. You too can become a part of this growing sector by introducing your e-wallet app that enables all users to easily adopt the idea of open-payment systems across the globe.

At Nimble AppGenie, we offer some of the finest e-wallet app development services that can help you explore all the options related to open-loop payment solutions and how you can implement them.

If you are looking for assistance and want to develop an open-loop payment solution, this is your best chance. Reach out today to share your digital wallet app ideas, and we assure you that we will turn them into reality!

Conclusion

The idea behind open-loop payment systems is to add to the convenience of users and reduce the hassle of daily transactions.

One of the biggest opportunities that arises with the rise of open-loop digital wallet payments is to be a part of the revolution by introducing your e-wallet app.

The concept is futuristic, the use cases are sustainable, and the opportunities to grow are endless.

Sure, there are a few challenges in the adoption of the idea and implementation, but, they are manageable in front of the comfort and convenience that the system brings on board. All in all, we can say that open-loop payment systems are here to stay!

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.