AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

TL;DR

- AI microfinance software uses machine learning for thin-file credit scoring, automated KYC, real-time fraud detection, and borrower-facing chatbots, turning a manual, paper-heavy MFI process into a decisioning engine that runs in minutes, not days.

- Studies on AI-driven fraud detection in microfinance report suspicious-activity identification rates around 90%, and AI-based KYC/document automation is cutting loan approval time from days to minutes.

- Custom AI microfinance builds typically run $40,000 for an MVP to $180,000+ for an enterprise platform, higher than a non-AI build because of the scoring model, data pipeline, and explainability layer regulators require.

- The build-vs-buy call isn’t “AI or no AI” anymore; it’s whether you build your own explainable, retrainable scoring engine or bolt a vendor’s black-box AI feature onto a generic platform.

- Nimble AppGenie builds AI-native microfinance software from alternative-data credit scoring to fraud detection and offline-first field-agent tools with explainability and compliance designed in from the first sprint, not patched on before launch.

“Can AI actually approve a microloan for someone with no credit history?” – it’s the question every microfinance organization, NBFC, MFI, and digital lender is asking in 2026, and the honest answer is: yes, if the AI microfinance software behind it is built correctly.

AI is no longer a bolt-on feature for lending platforms serving underserved borrowers – it’s the only practical way to score thin-file applicants, process loan volume, and catch fraud in real time that would otherwise need a team of loan officers.

This guide covers exactly what AI microfinance software needs to do, how to make the build-vs-buy call, what it costs to build, and the steps to get from idea to a compliant, scalable platform.

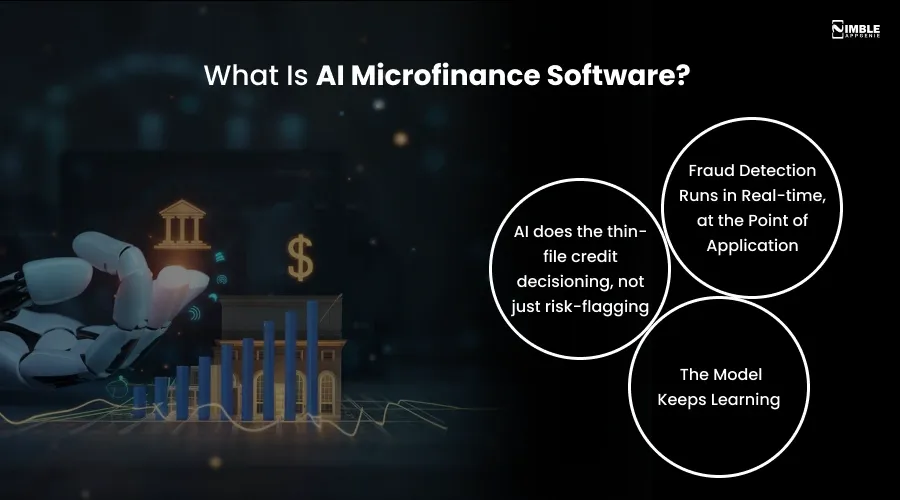

What Is AI Microfinance Software?

AI microfinance software is a lending platform for NBFCs, MFIs, digital lenders, and cooperatives that leverages machine learning across the loan lifecycle – not only as a single feature, but as the decisioning layer running fraud checks, underwriting, borrower support, and collections.

What actually makes a microfinance platform “AI-native” rather than “AI-washed”:

1. AI does the thin-file credit decisioning, not just risk-flagging

Traditional credit bureaus have little to no data on most microfinance borrowers, so the scoring model has to learn from alternative signals – utility payments, mobile wallet activity, behavioral data, and telco usage from the application itself.

2. Fraud Detection Runs in Real-time, at the Point of Application

AI models cross-check device fingerprints, behavioral patterns, and identity documents simultaneously, rather than treating fraud checks as a separate step after underwriting.

3. The Model Keeps Learning

Static scoring models drift as borrower behavior and fraud tactics change – an AI-native platform retrains on new repayment and fraud outcomes on a regular cycle, not once at launch.

A platform that only has a chatbot integrated onto a traditional rules-based scoring engine is not AI microfinance software – it is a lending platform with an AI feature.

The Market Reality: Why AI, Why Now

Microfinance has always had a data issue – most of its target borrowers have no formal credit history for a traditional bureau to score.

Research on AI-driven microfinance solutions has found AI-based fraud detection identifying suspicious activity at about a 90% rate, a meaningful switch from manual review processes. Alone, AI-based loan management systems are widely known for cutting loan approval timelines from days to minutes by automating document verification and KYC checks.

Simultaneously, the same research flags real risks any build has to plan for: algorithm bias against protected groups, the regulatory pressure now building around explainable AI in lending decisions, and data privacy exposure from alternative data sources.

That combination – real gains, real risks – is exactly why the architecture decision matters more than the AI feature first.

Build vs. Buy: The AI-Specific Version of This Call

The build-vs-buy decision for microfinance software used to be about origination and servicing workflows. In 2026, it’s really about one thing: who owns and can explain your scoring model.

| Option | What you get | The AI trade-off |

| Off-the-shelf (Mifos X, Mambu, Musoni, TurnKey Lender) | Fast go-live, proven core lending workflows | AI scoring is usually a generic, vendor-controlled model -you can’t retrain it on your own repayment data or explain its logic to your credit committee. (If you are evaluating a non-AI origination or servicing platform instead, our Loan Origination and Loan Servicing guides cover those in depth.) |

| White-label with AI add-ons | Pre-built compliance and servicing modules, AI bolted on as a feature | Faster than custom, but the AI layer is rarely built around your alternative data sources or your regulator’s explainability requirements |

| Custom AI-native build | Full ownership of the scoring model, fraud engine, and data pipeline | Higher upfront cost and longer timeline, but the model improves as your repayment data grows and produces reason codes your regulator can actually audit |

If your AI credit-scoring approach is meant to be a competitive advantage – reaching borrowers other lenders reject, at lower default rates – a vendor’s black-box model working against you two years in is the most common reason MFIs end up re-platforming.

That’s the particular failure mode a custom, explainable build avoids.

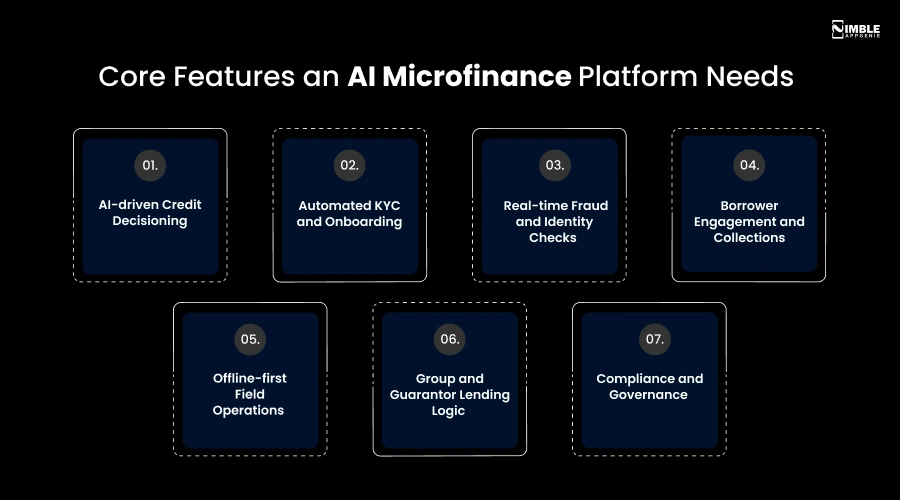

Core Features an AI Microfinance Platform Needs

Below are AI Microfinance software features to consider to build a competitive platform.

1. AI-driven Credit Decisioning

- Alternative-data scoring using utility payments, mobile wallet history, application-behavior signals, and telco usage.

- Continuous model retraining on new payment and default data, with drift monitoring.

- Explainable scoring with reason codes your credit committee and regulator can review, not a black-box output.

2. Automated KYC and Onboarding

- Document capture and verification automated end-to-end, cutting manual review from days to minutes.

- Biometric verification for borrowers without formal ID documentation.

3. Real-time Fraud and Identity Checks

- Automatic risk-score adjustment and step-up verification for flagged applications, without adding friction for legitimate borrowers.

- Device fingerprinting, behavioral biometrics, and identity-document cross-checks run at the same time with underwriting, not after it.

4. Borrower Engagement and Collections

- Predictive delinquency flagging that surfaces at-risk accounts before they miss a payment, not after.

- AI-powered chatbots and virtual assistants for common queries, repayment reminders, and loan-status updates in local languages.

5. Offline-first Field Operations

- Mobile agent apps that capture onboarding and repayment data offline and sync and rescore once connectivity returns.

6. Group and Guarantor Lending Logic

- AI-adjusted group risk scoring based on individual and group repayment history.

- Cross-liability tracking that factors into both individual and group credit decisions.

7. Compliance and Governance

- Audit-ready logs of every AI-driven decision, with human-override tracking.

- Automated fairness testing to monitor for disparate approval-rate impacts across borrower groups.

Recommended Tech Stack for AI Microfinance Software Solution

Consider the below tech stack to build a software solution for microfinance.

| Layer | Common choices |

| Backend | Node.js, Java (Spring Boot), or Python (Django) for the ledger and workflow engine |

| AI / ML | Python-based ML pipelines (scikit-learn, XGBoost, or deep learning depending on data volume), with SHAP or similar for explainability |

| Mobile (agent + borrower apps) | Flutter or React Native, offline-first sync |

| Database | PostgreSQL for transactional data, with a feature store for ML inputs |

| Fraud detection | Real-time inference layer (device fingerprinting, behavioral analytics) at the point of application |

| Chatbot/engagement | LLM-based conversational layer, scoped to lending FAQs and local languages |

| Cloud infrastructure | AWS, Azure, or GCP with region-specific data residency and model-serving infrastructure |

| Integrations | Mobile money APIs (M-Pesa, MTN MoMo), credit bureau and KYC/AML providers, SMS/USSD gateways |

| Security | AES-256 at rest, TLS 1.3 in transit, role-based access control, HSM/KMS key management |

Step-by-Step: How to Build AI Microfinance Software?

Go through the steps below to develop AI microfinance system software:

Step 1: Define the Lending Model before the AI Model

Individual, group, or agent-based lending changes what data your scoring model needs and how group risk gets calculated.

Step 2: Inventory your Alternative Data Sources

Confirm which data you can legally and reliably access per market – mobile wallet, utility, and telco before designing the scoring pipeline around it.

Step 3: Build the Scoring Model with Explainability from Day One

Design reason codes and audit trails into the model architecture, not as a report generated after the fact.

Step 4: Layer in Fraud Detection at the Point of Application

Integrate device and identity signals into the same decisioning flow as credit scoring, not as a separate downstream step.

Step 5: Automated KYC and Onboarding

Document and biometric verification should run through the same pipeline feeding your scoring model.

Step 6: Pilot on a Limited Cohort and Monitor for Bias

Run fairness testing on approval rates across borrower segments before a full rollout – this is also where regulators will look first.

Step 7: Deploy Collections and Engagement AI

Chatbots and predictive delinquency flagging come after the core lending and scoring engine is proven, not before.

Step 8: Set a Retraining Cadence

Monthly or quarterly retraining against new repayment and fraud outcomes keeps the model from drifting as borrower behavior shifts.

How Much Does It Cost to Build AI Microfinance Software?

AI features add real cost mainly in data pipeline work and explainability tooling, but they are also where most of the ROI comes from. Realistic 2026 ranges:

| Build type | Estimated cost | Timeline |

| MVP – core lending + basic AI credit scoring | $40K – $70K | 4–5 months |

| Mid-scale – AI scoring, fraud detection, group lending, mobile money | $70K – $130K | 6–8 months |

| Enterprise – full AI stack, chatbots, predictive collections | $130K – $180K+ | 8–12 months |

The line items that push AI builds above a standard microfinance build: data engineering to structure alternative data sources, explainability tooling, model training and validation, and ongoing retraining infrastructure.

Vendors quoting “AI microfinance software” without pricing these separately usually mean a chatbot bolted onto a rules-based system.

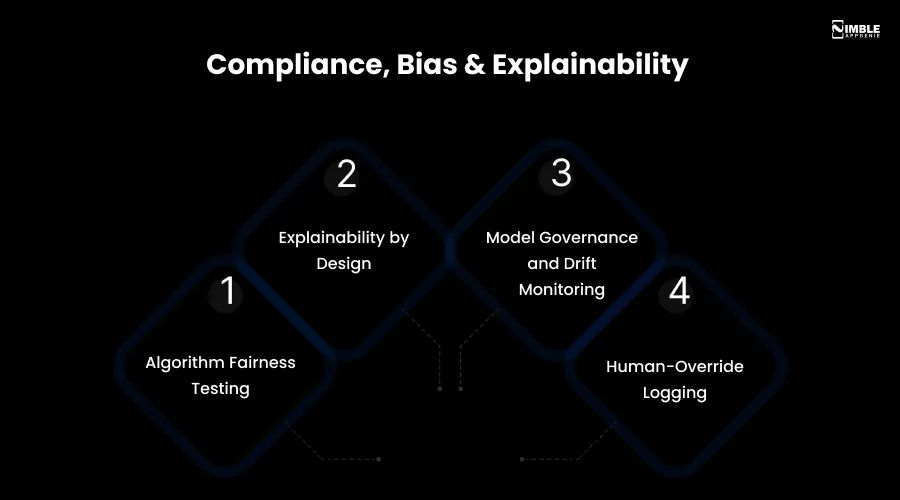

Compliance, Bias & Explainability

Beyond the standard KYC/AML and data-residency requirements every microfinance platform needs, AI adds its own compliance layer:

- Algorithm Fairness Testing: Automated, ongoing checks for disparate approval rates or pricing impact across borrower groups are becoming a regulatory expectation.

- Explainability by Design: Regulators and credit committees increasingly expect reason codes for AI-driven credit decisions, not a raw score.

- Model Governance and Drift Monitoring: A model trained on last year’s repayment behavior can degrade as conditions change – document retraining cadence as part of your compliance posture.

- Human-Override Logging: Every AI decision that gets manually overridden should be auditable and logged, usually the first thing a regulator asks to see.

| Treat this as an extension of your existing KYC/AML and data-protection architecture, not a separate workstream; regulators are increasingly reviewing them together. |

Common Mistakes to Avoid While You Build Software for Microfinance

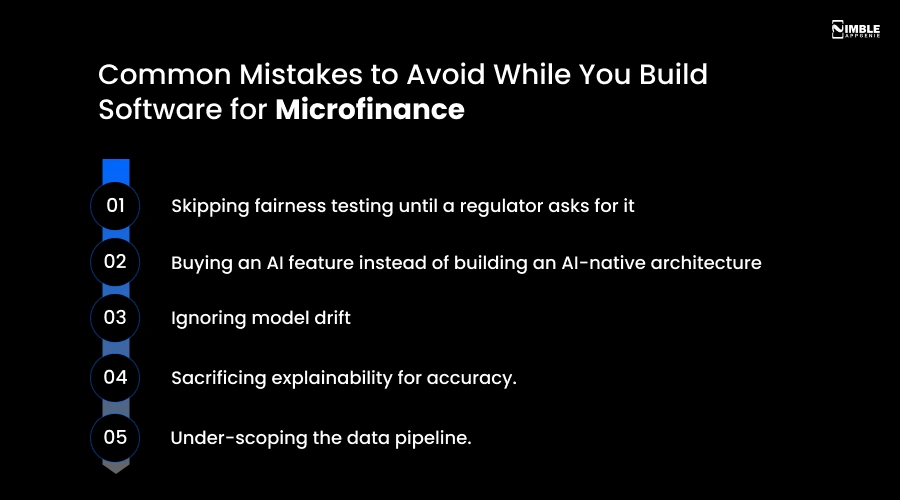

- Skipping fairness testing until a regulator asks for it. By then, you are re-auditing a live portfolio instead of validating a model pre-launch.

- Buying an AI feature instead of building an AI-native architecture. A chatbot layered on top of static-rules-based scoring is not the same as a model that learns from your repayment data.

- Ignoring model drift. A scoring model that was accurate at launch degrades as fraud tactics and borrower behavior evolve.

- Skipping fairness testing until a regulator asks for it. By then, you are re-auditing a live portfolio instead of validating a model pre-launch.

- Sacrificing explainability for accuracy. A marginally more accurate black-box model your credit committee can’t interrogate is a liability, not an advantage.

- Under-scoping the data pipeline. Alternative data sources need to be structured and cleaned before a model can use them – usually the most underestimated line item.

Further Reading: Loan Management Software Development · Digital Microfinance in Africa

Why Build AI Microfinance Platform With Nimble AppGenie

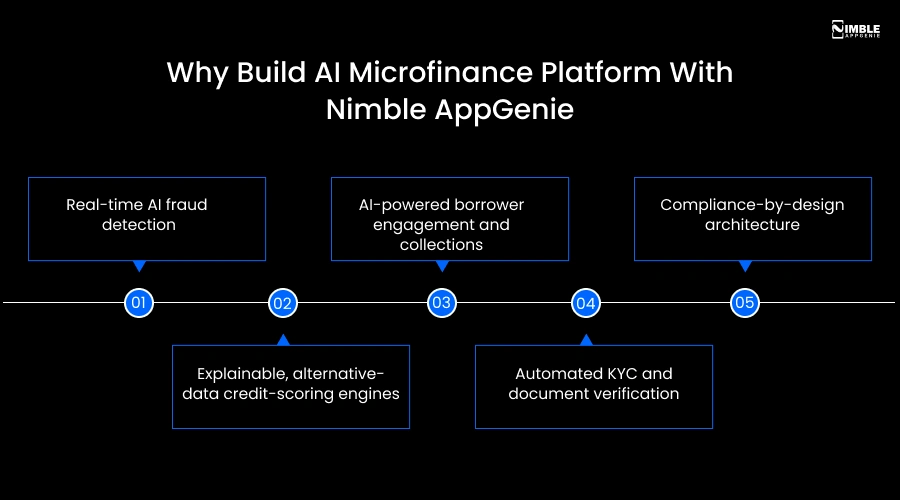

Nimble AppGenie has been building fintech and lending platforms since 2017, with dedicated experience in microfinance and agent-banking systems for financial inclusion across Africa and other emerging markets. Our AI microfinance builds include:

- Real-time AI fraud detection integrated into the application flow, not bolted on after underwriting.

- Explainable, alternative-data credit-scoring engines built around your own borrower and repayment data – not a vendor’s generic model.

- AI-powered borrower engagement and collections, including chatbots and predictive delinquency flagging.

- Automated KYC and document verification, cutting onboarding from days to minutes.

- Compliance-by-design architecture, with fairness testing and audit logging mapped to your regulator’s requirements from the first sprint.

We scope every AI microfinance engagement around your lending model and data sources first, so the scoring engine improves with your portfolio instead of demanding a rebuild as you scale.

Conclusion

Building AI microfinance software in 2026 comes down to one real decision: whether you own or can explain your scoring model, or you are renting a vendor’s black box and hoping it works for your borrowers.

Get the lending model, explainability architecture, and data pipeline right from the first sprint, and AI becomes the thing that allows you to reach borrowers other lenders can’t score, profitably and compliantly. Get it wrong, and you are back here in two years re-platforming a system you can’t audit.

FAQs

Yes, AI credit-scoring models built for microfinance use alternative data (mobile wallet activity, utility payments, telco usage, and application behavior) instead of bureau history, which is exactly the data traditional scoring can’t use for thin-file borrowers.

Custom builds typically range from $40,000 for an MVP to $180,000+ for an enterprise platform, higher than a non-AI build because of data pipeline work, model training, and explainability tooling.

If your ability to reach borrowers other lenders reject at acceptable default rates is core to your business, a custom model that retrains on your own repayment data is worth the extra build time. A vendor’s generic AI feature is harder to explain to your credit committee and can’t improve on your specific portfolio.

Research on AI-driven fraud detection in microfinance settings has reported suspicious-activity identification rates around 90%, a meaningful improvement over manual review, though results vary by data quality and model design.

Yes, and it’s one of the most-cited concerns in microfinance AI adoption. Automated, ongoing fairness testing across borrower segments needs to be built into the model from the start, not added after a regulator raises it.

Most lenders retrain monthly or quarterly against new repayment and fraud outcomes, since borrower behavior and fraud tactics shift over time and a static model degrades in accuracy.

No, a chatbot is one feature. AI microfinance software uses machine learning across underwriting, fraud detection, and collections, with the model retraining on real outcomes over time, not just at launch.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.