AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- Loan servicing software manages everything that happens after a loan is disbursed: EMI collection, interest calculation, repayment tracking, delinquency, and borrower communication.

- It is different from loan origination software (pre-funding) and broader loan management software (full lifecycle).

- Core features include amortization engines, automated payment processing, delinquency workflows, compliance reporting, and a borrower self-service portal.

- Custom development typically costs $25,000–$150,000+ depending on scope, and takes 4–9 months.

- Nimble AppGenie builds custom loan servicing software for banks, NBFCs, and fintech lenders, with compliance and scalability built in from day one.

Loan servicing software is the system that takes over the moment a loan is funded – it runs EMI collection, repayment tracking, interest calculation, delinquency management, repayment tracking, and borrower communication for the rest of the loan’s life. Get this right, and servicing becomes the part of your lending business that secretly protects your margins.

This guide breaks down what loan servicing software actually does, which features matter, what it costs to build, and how to plan a development roadmap that won’t blow your budget or your timeline.

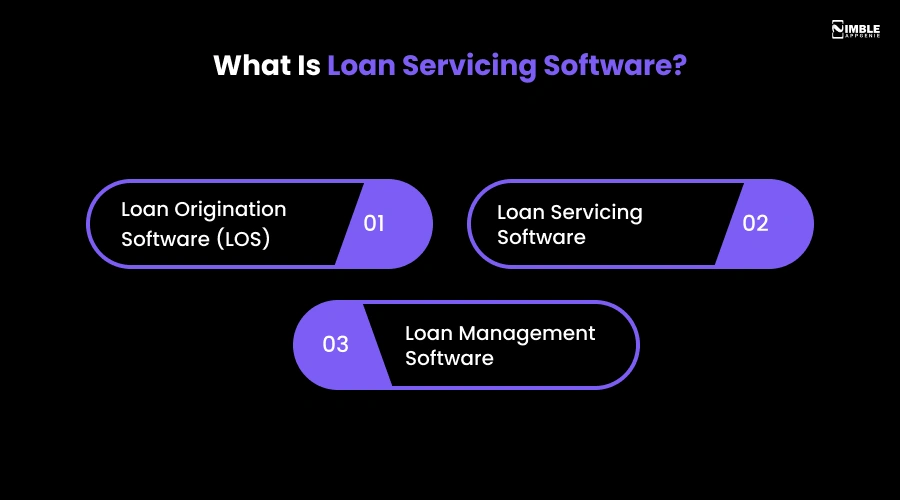

What is Loan Servicing Software?

Loan servicing software is a digital solution used by financial institutions to manage the ongoing administration of loans after disbursement. It handles EMI collection, repayment tracking, interest calculation, customer communication, and delinquency management, ensuring loans remain compliant and current throughout their term.

It’s easy to confuse this with other systems, so below is the quick distinction:

- Loan Origination Software (LOS): It handles everything before funding – application, underwriting, credit checks, disbursement, and approval. Our loan origination software guide covers this stage in detail.

- Loan Servicing Software: It takes over the moment funds are disbursed and runs the loan until it is paid off or closed.

- Loan Management Software (LMS): An umbrella system that usually includes both origination and servicing in one platform. If you are deciding whether to build one unified system, our guide on how to develop loan management software walks through that broader build.

Many lenders begin with a combined LMS and only need to go deep on servicing once loan volume grows, and manual repayment tracking starts breaking down.

Why Loan Servicing Software Matters More Than Founders Expect

Origination gets the attention because it is where the loan gets sold. But servicing is where the loan actually gets paid back or doesn’t. A disconnected or manual servicing process creates real, measurable issues.

- Missed or misapplied payments that damage borrower trust and create reconciliation headaches.

- Compliance reporting that takes days instead of minutes because data lives in spreadsheets.

- Delinquency detected too late (usually at 60-90 days), by which point recovery odds have already dropped.

- No visibility into portfolio health until a report is manually pulled together.

A well-built servicing system fixes all four by keeping payment, repayment, and compliance data in one connected place – automatically.

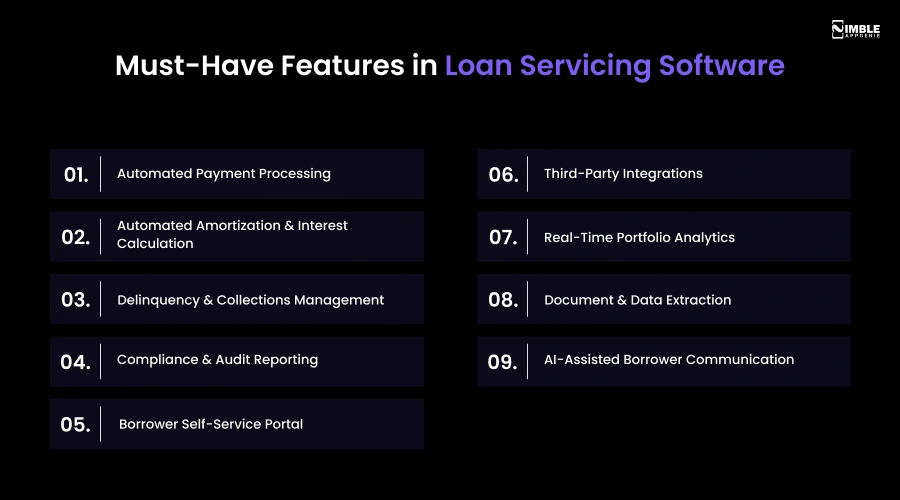

Must-Have Features in Loan Servicing Software

1. Automated Payment Processing

ACH, UPI, card, or wallet-based collections, with automatic handling of partial payments, retries, and failed payments. This is generally the single biggest source of manual work in a servicing team, and the first thing worth automating.

2. Automated Amortization & Interest Calculation

The engine that calculates interest, repayment schedules, and principal splits for every loan type you support, so this needs to be built and tested meticulously, not bolted on later.

3. Delinquency & Collections Management

Automatic days-past-due (DPD) tracking, configurable collection strategies, and tiered escalation workflows. The earlier delinquency is flagged, the better the recovery rate – this is not a feature to leave for “phase two”.

4. Compliance & Audit Reporting

Built-in reporting for regulatory frameworks relevant to your market (Reg Z, Metro 2 credit-bureau reporting, GDPR, or local lending regulations), plus a full audit trail on every account action.

5. Borrower Self-Service Portal

Let borrowers check balances, make payments, view repayment schedules, and request modifications without calling support. This alone can cut support ticket volume significantly.

6. Third-Party Integrations

APIs into your loan origination system, credit bureaus, core banking platform, and payment processors. Our guide to fintech APIs covers what to look for when connecting these systems.

7. Real-Time Portfolio Analytics

Dashboards showing delinquency trends, portfolio performance, and roll rates without requiring a data team to pull a report every time leadership asks a question.

8. Document & Data Extraction

For lenders dealing with high document volume – hardship applications, loan modification requests, income verification – intelligent document processing can extract and validate data automatically instead of manual review.

See our guide on building an intelligent document processing platform for how this fits into a servicing workflow.

9. AI-Assisted Borrower Communication

Automated payment reminders, routine borrower queries, and delinquency alerts are handled without a human agent, escalating only edge cases. If you are exploring this, our breakdown of AI chatbots in fintech customer service is a useful next read.

Loan Servicing Software Development Cost

Cost depends heavily on scope, the loan types supported, and the number of systems you are integrating with.

Here’s a realistic cost range for loan service software development in 2026:

| Project Scope | Estimated Cost | Estimated Timeline |

| MVP (single loan type, basic collections) | $25,000 – $45,000 | 3–4 months |

| Mid-tier (multiple loan types, integrations, portal) | $45,000 – $90,000 | 5–7 months |

| Enterprise-grade (multi-entity, compliance-heavy, AI features) | $90,000 – $200,000+ | 8–14 months |

These figures move based on how much of your servicing logic is custom (non-standard loan products, unusual amortization rules) versus configurable, and how many legacy systems you need to connect to.

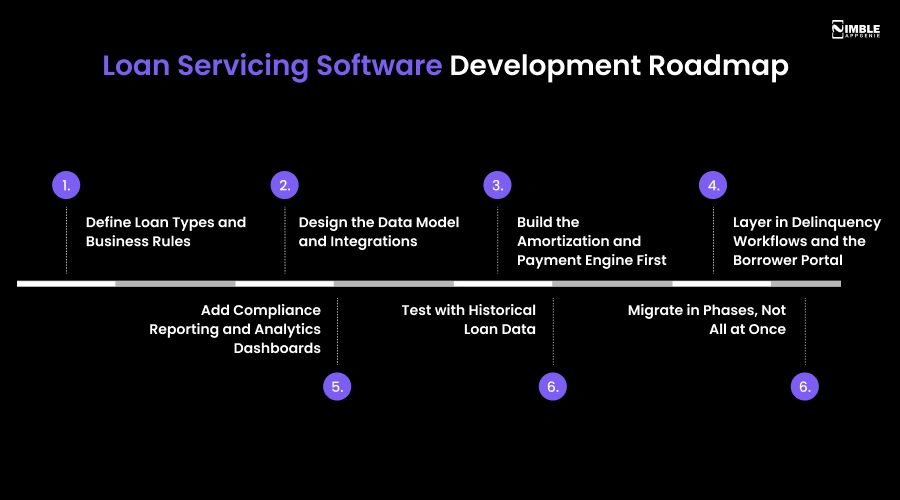

Loan Servicing Software Development Roadmap

Follow the steps below to build loan servicing software for your lending business.

- Define Loan Types and Business Rules: Every repayment structure, modification policy, and penalty rule needs to be mapped before a line of code is written.

- Design the Data Model and Integrations: Decide how servicing connects to your LOS, credit bureaus, and core banking system.

- Build the Amortization and Payment Engine First: This is the base everything else sits on – get it wrong and every downstream feature inherits the bug.

- Layer in Delinquency Workflows and the Borrower Portal: These typically come next once payment logic is solid.

- Add Compliance Reporting and Analytics Dashboards: Build these in from the start rather than retrofitting them under audit pressure later.

- Test with Historical Loan Data: Run old accounts through the new system and compare results against your existing records before going live.

- Migrate in Phases, Not All at Once: Move a small portfolio segment first, confirm accuracy, and then scale up.

Build Loan Servicing Software With Nimble AppGenie

Nimble AppGenie, a fintech software development company, designs and builds custom loan servicing software for banks, NBFCs, and fintech leaders. Our team builds full-stack amortization engines, delinquency workflows, borrower portals, compliance reporting, and automated payment processing tailored to your loan products rather than forcing your business into a rigid template.

If you are also evaluating origination or full lifecycle management, our lending software development services cover the comprehensive picture from application to payoff.

Whether you are replacing a legacy servicing stack or building your first system from scratch, our fintech developers can walk you through scope, cost, and a realistic timeline based on your loan portfolio.

Conclusion

Loan servicing software is where lending businesses actually protect their margins, not at origination, but in the months and years after a loan is funded.

Lenders who invest in automated collection, solid amortization logic, and early delinquency detection are the ones who retain borrowers and avoid compliance headaches down the line.

If you are planning to build or upgrade your service system, get the payment engine and compliance reporting right first, before everything else on that foundation.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.