AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- Building an AI financial wellness app means combining expense tracking, AI-powered insights, bank integrations, and security compliance in one product.

- To develop an AI budgeting app, you have to do market research, feature planning, UI/UX design, backend and AI development, API integration, security and compliance, and launch.

- The AI financial wellness app development features include a personalized financial advisor chatbot, predictive spending forecasts, NLP-based transaction categorization, and real-time fraud detection.

- Your tech stack needs a solid mobile frontend, a Python or Node.js backend, and AI tools like OpenAI API, TensorFlow, or AWS SageMaker.

- Compliance is not optional; GDPR, PCI-DSS, KYC, and AML must be baked in from day one, not added later.

- The cost to make an AI fintech wellness app can be around $40,000-$250,000.

- The challenges to create an AI-powered financial wellness app are data security, regulatory compliance, AI model accuracy, and banking API reliability.

How do you build an AI financial wellness app? You build a product that looks at a user’s real financial life and gives them advice they can actually act on, instead of just showing them numbers on a screen.

That is the short answer. It is also why this is a good time to build one. Over 92% of firms say their AI investments in finance are meeting or exceeding their expected ROI.

If you are a fintech founder, a CTO, COO, or entrepreneur, you might have questions:

- What features do you actually need for version one?

- Which AI features matter most, and which can wait?

- When does compliance come into play?

- What will this cost, and how long will it take?

This guide answers all of that, in the order you will run into it. We start with who you are creating for, then move to features, tech stack, AI, and bank integrations, and the compliance steps you need before you go live.

What is an AI Financial Wellness App?

An AI financial wellness app is a mobile app that connects to a user’s bank accounts, analyzes their income and expenses, and uses AI to give personalized financial guidance. Basically, it is a basic budgeting app that shows users what they have spent. It tells users what it means and what they should do about it.

Let’s understand this in a simple way. A user asks: “Can I take a vacation in September?” The AI looks at their savings rate, upcoming bills, and income, and gives a real answer based on their actual numbers.

This is how an AI financial wellness app works. From passive data display to active financial guidance. This is why companies, banks, and fintech startups are building these apps. And it is also why the costs are higher than a basic budgeting tool.

Why Build an AI Financial Wellness App in 2026?

The financial wellness app market is growing fast, user expectations have shifted toward AI-driven guidance, and the cost of building has dropped.

The numbers make the case quickly.

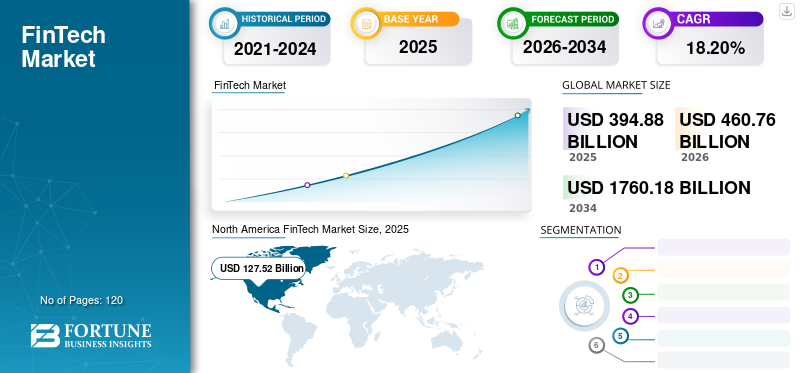

- The global fintech app market was valued at $460.76 billion in 2026 and is projected to reach $1760.18 billion by 2034.

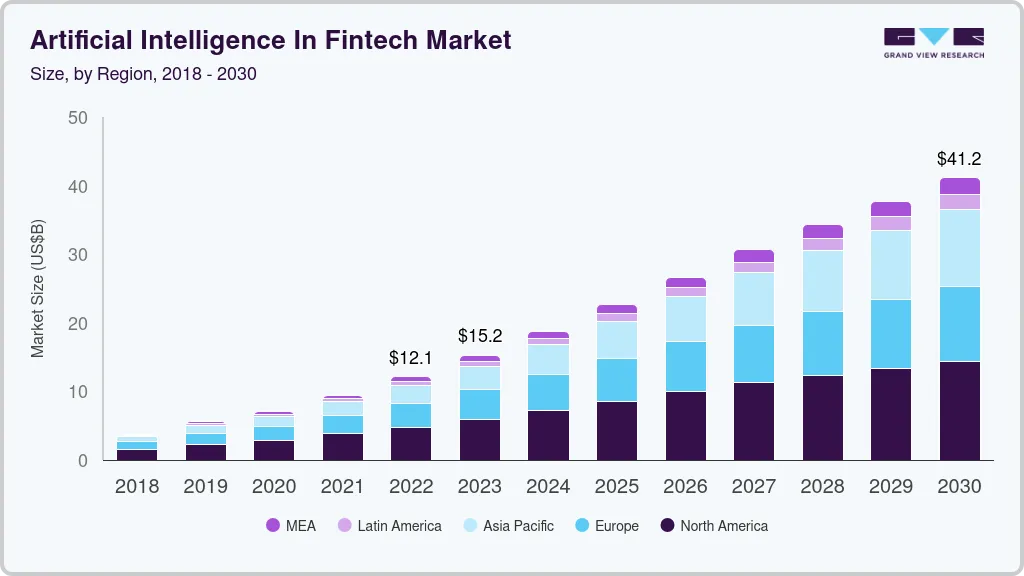

- AI in fintech specifically is on a steeper curve and forecasted to reach $41.16 billion by 2030.

- Meanwhile, 75% of financial firms now use AI, up from 58% in 2022.

- And on the user side: 49% of consumers already say managing money without AI feels outdated.

The market is not coming. It is here.

Why 2026 Specifically is the Right Time to Build?

Three things have converged that did not exist two or three years ago.

- First, pre-built AI APIs have made the AI layer accessible. Two years ago, developing a personalized financial chatbot meant hiring an ML team and training models from scratch. Today, you can wire OpenAI’s API to a user’s transaction history and have a working AI financial advisor in weeks.

- Second, open banking infrastructure is mature. Plaid connects to 12,000+ US financial institutions. TrueLayer covers the UK and Europe. The data pipelines that used to take years to negotiate and build are now available via API with developer documentation.

- Third, user trust in AI for financial decisions has crossed a threshold. In 2022, most consumers were uncomfortable with AI making financial recommendations.

The technology is ready. The infrastructure exists. The market is growing. That combination is what makes 2026 the right time to build.

How the AI Layer Actually Works in Financial Wellness?

The AI layer in a financial wellness app works through four main components. An NLP engine, an ML model, a personalization engine, and a real-time data pipeline.

Let’s have a look at the technical workflow of the app.

- User opens app → Dashboard pulls from database → AI model scores financial health → personalized insights surface on screen.

- User connects bank → Plaid syncs transactions → NLP model categorizes each one → ML model updates spending forecasts → new insights generated.

- User asks chatbot a question → NLP engine classifies intent → backend queries user’s financial data → GPT-4o generates personalized answer with their actual numbers.

- New transaction arrives → streamed through Kafka → fraud detection model scores it in <100ms → suspicious ones flagged instantly.

You can build each of these flows independently. You do not need all four on day one. A smart MVP might start with just the bank sync, transaction categorization, and an AI chatbot. Then add fraud detection and predictive forecasting in the final version.

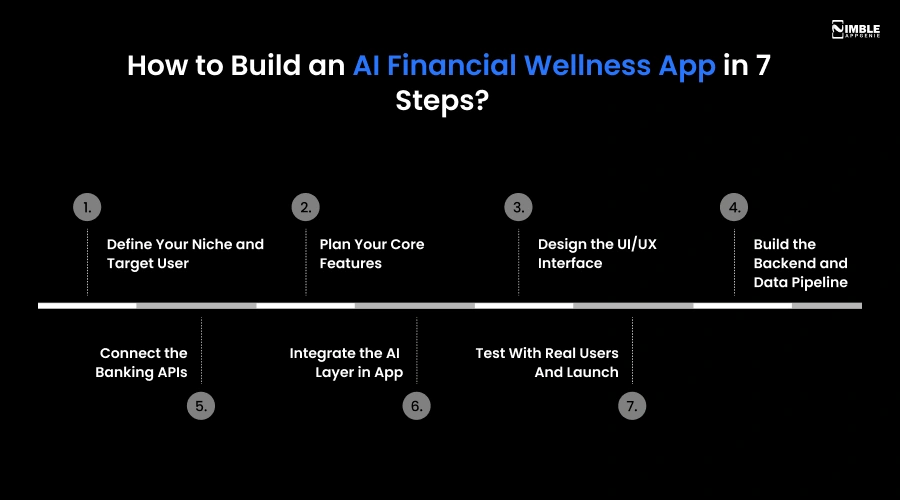

How to Build an AI-Powered Financial Wellness App in 7 Steps?

To develop an AI financial wellness app, you have to define a niche, plan core features, design UI/UX, build a backend, integrate AI models, integrate an AI layer, and test and launch.

1. Define Your Niche and Target User

Firstly, you have to be clear on who you are building for and what problem you are solving. This matters the most. The most common reason fintech apps fail is that they try to serve everyone and end up serving no one.

You can ask these questions first:

- Is this for individual consumers, employees, or enterprise clients?

- What is the core financial pain point? Debt management? Saving for a goal? Paycheck-to-paycheck stress? Investment tracking?

- What does your ideal user look like? Age, income level, and financial literacy?

- Are you creating a standalone app or embedding into an existing platform?

Your answers will shape every decision downstream, including features, AI models, compliance needs, and monetization.

2. Plan Your Core Features

Feature planning is where most teams overbuild. They list every feature they can imagine, budget for all of it, and run out of money before launch. Instead, split your features into two lists: what you need on day one, and what you add after you have real users.

A first version needs six to 10 features, like bank connection, expense tracking, transaction categorization, goal setting, and a basic financial advisor chatbot. That’s it.

Now, write each feature as a user story. “As a user, I want to see where my money went this week without entering anything manually.” That format keeps the team honest about what they are building and why.

3. Design the UI/UX Interface

This is where many teams waste months. They build the backend first, then struggle to design a frontend around it. Do it the other way around.

You should start by creating a wireframe in Figma and mapping the user journey from download to first value moment. How fast can someone connect their bank account and see something useful? It should take under two minutes.

If your onboarding takes longer than that, users leave before they ever experience the AI. Design the AI output first, too. What does a personalized insight look like on screen? Write the copy before you build the model.

4. Build the Backend and Data Pipeline

Now you build what users never see but depend on entirely. Your backend handles user authentication, stores transaction data, manages API connections, runs AI model calls, and fires notifications.

The dedicated development team can use Python with FastAPI if AI is central to the product; Python’s ecosystem for ML is unmatched. Besides, use PostgreSQL for your main database. Add Redis for caching real-time data.

One decision that matters here is to go API-first. Develop clean, documented internal APIs before building the frontend against them. This makes adding features later, connecting third-party services, and scaling your team dramatically easier.

5. Connect the Banking APIs

This is where your app gets real data, and where most of the integration complexity lives. Plaid is the standard for US apps. It connects to over 12,000 banks and gives you read-only access to transactions, balances, and income.

The integration has two parts: Plaid Link. It is a pre-built UI that handles the bank login flow for the user and your backend calls to pull and sync transaction data.

One thing teams underestimate: transactions arrive as raw merchant strings. “SQ*BLUE BOTTLE 415-” is not useful to a user. Your AI categorization layer needs to run on every incoming transaction before anything surfaces on screen.

6. Integrate the AI Layer in App

This is the step that makes it a financial wellness app rather than a glorified spreadsheet. You can start with what you can integrate quickly. Just use OpenAI’s API for the chatbot, feed it the user’s transaction history and financial context in the prompt, and it returns personalized answers.

Besides, you can use a Hugging Face text classification model for transaction categorization. These two alone take a basic app and make it feel genuinely intelligent.

After launch, add the deeper models. XGBoost for spending predictions.

Also, you can use a behavioral ML model for personalized recommendation scoring, anomaly detection for fraud, and build in layers.

7. Test With Real Users And Launch

Testing a financial wellness app is not just about finding errors and bugs. It is about ensuring financial data is accurate, AI models perform as expected, and security holds under real conditions. Run a closed beta with 100 to 500 real users before public launch.

Watch them use the app. Where do they hesitate? What do they ignore? What do they ask about that is not in the app yet? Also, pay close attention to AI accuracy during beta. Real users will ask the chatbot questions you did not anticipate.

You have to fix these issues before they hit scale. A wrong financial insight that goes to 100 users is a lesson. The same mistake at 100,000 users is a crisis. Once the app is tested, you can launch it on the respective platforms.

Core Features for an AI Financial Wellness App

The must-have features to build a financial wellness app powered with AI are expense tracking, bank account integration, an AI chatbot, transaction categorization, predictive spending forecasts, and so on. These AI fintech features help users better understand their finances and make smarter financial decisions.

Take a look at the feature table.

| Features | What It Does |

| Expense Tracking & Budgeting | Tracks income, spending, and sets monthly limits. Alerts users when they overspend. |

| Bank Account Integration | Connects to real bank accounts via Plaid or Yodlee. Pulls live transaction data automatically. |

| AI Financial Advisor Chatbot | Users ask money questions in plain language and get personalized answers based on their own data. |

| Transaction Categorization | Sorts raw merchant names (SQBLUE BOTTLE, AMZNMKTP) into categories like food, shopping, and transport. |

| Personalized Financial Insights | Surfaces specific, actionable tips: “You spent 38% more on dining this month.” |

| Predictive Spending Forecasts | Predicts what the user will spend next month, broken down by category. |

| Financial Goal Setting & Tracking | Users set savings goals, debt payoff targets, or emergency fund milestones. The app tracks progress. |

| Real-Time Fraud Detection | Monitors transactions as they arrive and flags suspicious ones instantly. |

| Notifications and Nudges | Timely push alerts for bill due dates, overspending, savings milestones, and opportunities. |

| Dashboard (Financial Health Score) | One screen showing the total picture, income, spending, savings rate, goal progress, and alerts. |

What is the Best Tech Stack For AI Financial Wellness App Development?

The best tech stack for developing an AI-powered financial wellness app is React Native, Python, PostgreSQL, TensorFlow, OpenAI, Plaid, and AWS. This fintech tech stack helps you build a secure and feature-rich AI financial wellness application.

Let’s have a look at the tech stack.

| Component | Technology |

| Mobile Frontend | Flutter or React Native |

| Web Frontend | React.js / Next.js |

| Backend | Python (FastAPI) or Node.js |

| AI / ML (Custom) | TensorFlow, PyTorch, XGBoost |

| NLP | Hugging Face Transformers, spaCy |

| Primary Database | PostgreSQL |

| Message Streaming | Apache Kafka |

| Banking APIs | Plaid (US), Yodlee (Global), TrueLayer (EU/UK) |

| Cloud Infra | AWS or Google Cloud |

| Authentication | Auth0, Firebase Auth, or custom OAuth 2.0 |

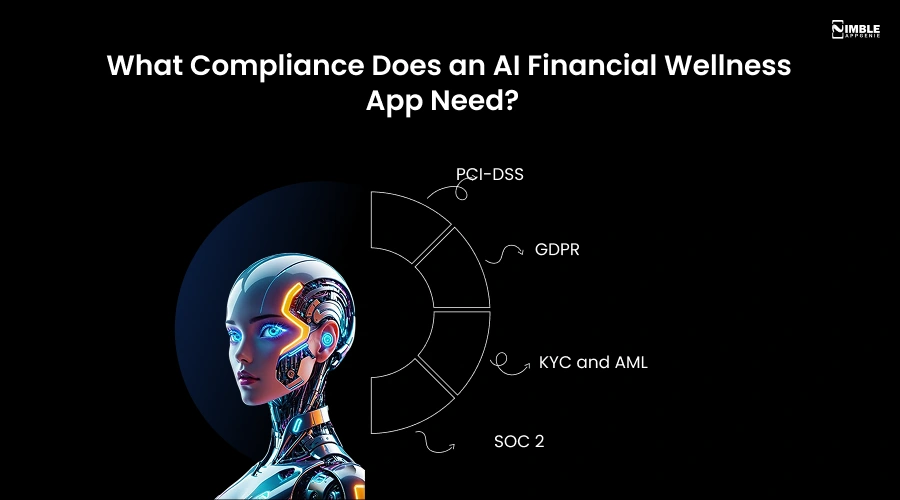

What Compliance Does an AI Financial Wellness App Need?

An AI financial wellness app should comply with GDPR, PCI DSS, KYC, AML, and SOC 2, depending on where it operates. These regulations affect how you collect, store, protect, and delete user data, so compliance should be planned before development begins.

Here are the major mobile app data privacy compliance requirements you must consider.

► PCI-DSS

If your AI financial wellness app stores, processes, or transmits card data, PCI-DSS applies. The standard exists to prevent card fraud and data theft. The practical way to handle this is not to store data yourself.

You can use Stripe, Plaid, or another certified payment processor to manage it. When a certified third-party holds the card data, your PCI-DSS scope shrinks. This is the right decision for almost every app.

► GDPR

GDPR compliance gives users control over their own data. They can ask what you hold, request a correction, or tell you to delete everything. Your app must be able to do all three.

In practice, this means that you collect only the important data, store it, tell users why you need it, and build a working data deletion flow before you launch.

► KYC and AML

KYC means verifying who your user actually is before they access financial services. You need a government ID check, sometimes a selfie match, and basic address verification.

AML means monitoring for patterns that look like money laundering. Financial apps that manage money must flag suspicious activity and report it to regulators.

You can also use third-party KYC providers rather than building this yourself. They manage the document scanning, liveness detection, and watchlist checks. You get the result via API.

► SOC 2

If your financial wellness app is B2B, you will be asked for your SOC 2 report before most enterprise buyers will sign a contract.

SOC 2 compliance is a security audit. It confirms that your systems and processes meet a defined standard for data security, availability, and confidentiality. You can start the process in advance.

An SOC 2 audit takes months and needs you to have documented, functioning security controls in place before the auditor arrives.

How Much Does it Cost to Build an AI Financial Wellness App?

The cost to develop an AI financial wellness app ranges from $30,000-$250,000, depending on app complexity, feature sets, tech stack, and development team. A lean MVP version with core AI features costs less, while a full-featured enterprise platform with custom AI models costs more.

The table below shows the cost to build a financial wellness app powered with AI, showing an estimation for different levels of complexity.

| Build Type | What Is Included | Cost Range | Timeline |

| MVP version | Expense tracking, bank integration (Plaid), AI chatbot (API-based), basic insights dashboard, goal setting | $40,000 – $80,000 | 3–4 months |

| Mid-Range | Everything in MVP + transaction categorization, ML, spending predictions, personalized AI insights, multi-bank support, notifications | $80,000 – $150,000 | 4–7 months |

| Enterprise or Full | Everything above + custom AI models, fraud detection, compliance layers, white-label options, employer dashboard, HR system integrations | $150,000 – $250,000+ | 7–9 months |

These are realistic ranges. The actual AI financial wellness app development cost depends on the specific features you choose, the AI models you integrate, and your compliance needs.

Key Drivers of Cost of AI-Powered Financial Wellness App Development

The factors that affect the cost are given below. You should also consider these factors while allocating a budget for your project.

- AI Integration: Adding AI increases $10,000-$50,000 over a standard app development, depending on whether you use pre-built APIs or custom-trained models.

- Compliance and Security: GDPR setup, KYC integration, penetration testing, and security audits add $10,000-$40,000.

- Banking API costs: Plaid charges per connection. It is typically $500-$1000 per user per month. Budget for this as an ongoing operating cost.

- Developer team location: Asia-based teams charge $20-$50/hr vs $100-$130/hr in North America. Same output, significantly lower cost when you choose the right partner.

- Post-launch maintenance: Plan to spend 15-20% of your development cost per year on updates, infrastructure, security patches, and new features.

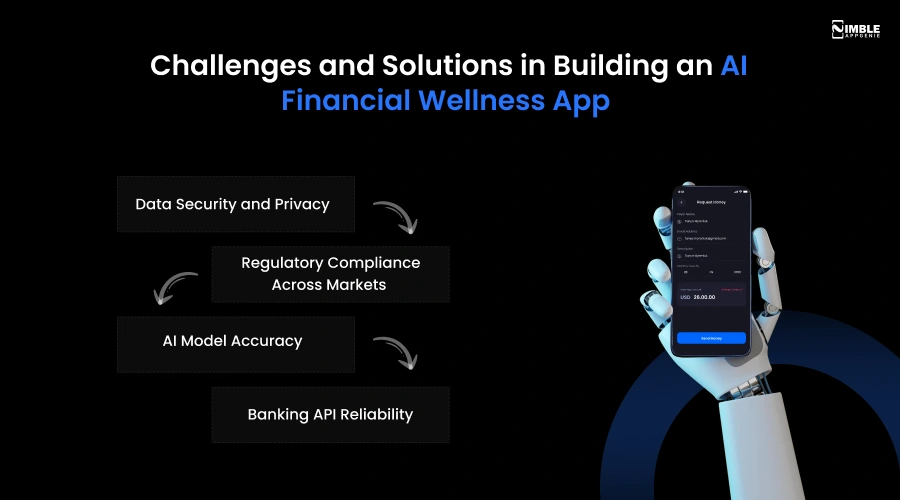

Challenges and Solutions in Building an AI Financial Wellness App

The challenges to build an AI financial wellness app are data security and privacy, regulatory compliance, AI model accuracy, and banking API reliability. You can manage these challenges with strong security, well-trained AI models, and trusted banking integrations.

Now, let’s understand what challenges you might face in detail with solutions.

1. Data Security and Privacy

Users hand over their bank login credentials or account access. That is the most sensitive data in their lives. A breach does not just lose you customers; it ends your company.

Solutions :

You can use AES-256 encryption for all stored data and use TLS 1.3 for all data in transit. Since mobile app security is crucial, never store raw bank credentials. Only use Plaid’s tokenized connection instead. Besides, you can implement MFA for every user and run penetration tests before launch.

2. Regulatory Compliance Across Markets

GDPR, CCPA, PCI-DSS, KYC, AML, and the EU AI Act all apply, and they differ by market. If you miss anyone, you will have to pay fines, forced shutdowns, or blocked distribution.

Solutions :

You should map your target markets before the development. Bring in a compliance consultant during the design phase. Also, build consent management, data deletion flows, and audit logs into the architecture from day one.

3. AI Model Accuracy

A chatbot that gives bad financial advice, or a categorization model that sorts rent payments under dining, destroys user trust fast. Bad AI is worse than no AI.

Solutions :

Do not train models on generic data. Just use labeled financial transaction datasets for categorization. Fine-tune your chatbot with real queries from your target user segment. Besides, build a feedback loop so users can flag wrong answers. Monitor AI fintech chatbot accuracy continuously after launch.

4. Banking API Reliability

Plaid, Yodlee, and other banking APIs go down. Banks change their authentication flows. A connection that worked yesterday breaks today. When bank sync fails, your entire app’s value proposition breaks.

Solutions :

You should build fallback logic for every API call. Notify users clearly when sync fails rather than showing stale data. You can also use multiple banking API providers where possible. Now cache the last successful data pulls so users always see something useful.

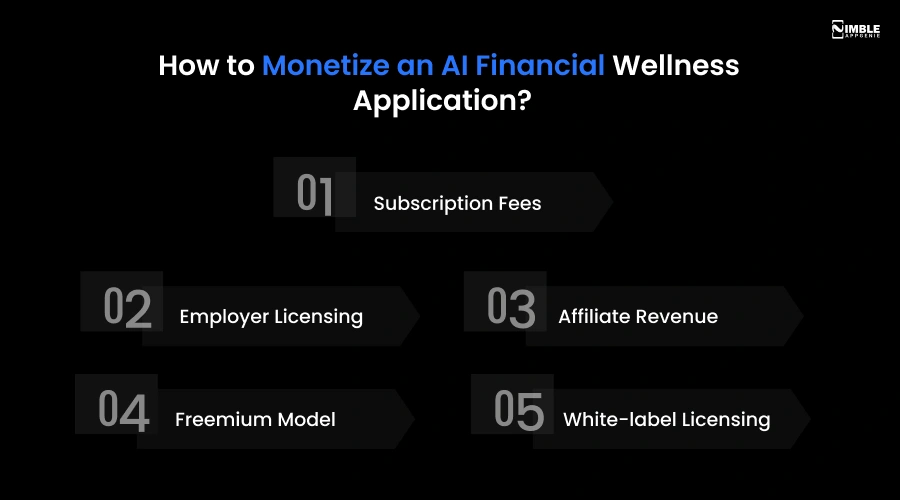

How to Monetize an AI Financial Wellness Application?

You can monetize your AI budgeting app with monthly subscription fees, employer licensing, affiliate commissions, premium features, and white-label licensing. These monetization models can help you earn a huge revenue from your fintech app.

Let’s check them out.

1] Subscription Fees

You can charge users $5-$15/month for premium features like predictive forecasts, investment tracking, and unlimited AI advisor access. Apps like Cleo and Wise use this monetization model.

2] Employer Licensing

You can charge companies $5-$20 per employee per month to offer the application as a benefit. Brightside and Origin use this model. Higher contract values and lower churn.

3] Affiliate Revenue

When the AI recommends a savings account, insurance product, or loan refinancing option, you earn a referral fee. Revenue scales with user engagement.

4] Freemium Model

Your app can provide basic features for free, and premium AI features behind a paywall. It drives downloads and converts a portion to paid.

5] White-Label Licensing

License your platform to banks or HR systems that want to provide financial wellness under their own brand. It gives high contract value and long-term relationships.

How Can Nimble AppGenie Help You Build an AI-Powered Financial Wellness App?

Nimble AppGenie is a trusted fintech app development company that specializes in AI integration, banking AI connections, security and compliance, and mobile app development.

Having 8+ years of experience, we have delivered 350+ projects, including fintech across the US, UK, Europe, and Asia. When you hire us to develop an AI financial wellness app, here is what we bring to the table:

- End-to-End Fintech Development: From MVP scoping to post-launch support, we handle the full development like mobile frontend, backend architecture, AI integration, and third-party APIs.

- AI and ML Integration: Our fintech team integrates AI models for chatbots, fraud detection, spending predictions, and personalized insights using custom models based on the budget.

- Compliance-First Architecture: We develop GDPR, PCI-DSS, and AML compliance into the app from day one. ISO-certified and NASSCOM-verified.

- Cross-Platform Mobile Apps: Flutter and React Native apps that work on both iOS and Android, cutting costs without sacrificing quality.

So, are you ready to build your AI financial wellness app? Talk to Nimble AppGenie. Share your idea and get a custom cost estimate.

Conclusion

Developing an AI financial wellness app comes down to a few real decisions: know who you are building for, pick the right features for version one, connect to real bank data, add AI that actually helps, and get compliance right from day one.

None of this is complicated once you break it down. The market is ready, the tools exist, and the path is clear; what’s left is execution.

Thus, if you want a development partner who can build an AI financial wellness app and understands both the AI and the compliance side, Nimble AppGenie can help you turn this plan into a working product.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.