AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

TL;DR

- A white label lending platform is pre-built loan software you rebrand as your own, no coding an entire lending stack from zero.

- Launch timelines run 6 to 16 weeks for white label vs. 6 to 12+ months for fully custom builds.

- Costs typically range from $15,000 to $80,000 for white label setup and $80,000 to $300,000+ for custom lending platform development.

- Compliance (KYC, AML, state lending laws) is the single biggest risk area; get this checked before signing any vendor contract.

- Non-financial brands can legally offer loans through white label lending without holding a lending license, as long as the licensed partner behind the platform handles the regulated parts.

- Nimble AppGenie builds and customizes white label lending platforms for banks, NBFCs, and fintech startups, handling everything from compliance-ready architecture to KYC/credit bureau integrations. So, you can launch under your own brand without the 12-month build cycle.

White label lending platform development is how most banks, fintech startups, and NBFCs are entering digital lending in 2026, without spending a year and a seven-figure budget building loan software from scratch. Instead, you license a proven pending engine, put your logo and brand on it, and go live in weeks.

Industry estimates put the global digital lending market at about $507 billion in 2025, growing toward $890 billion by 2030, so the pressure to launch fast is real.

If you are evaluating whether to build custom, do a hybrid, or buy white label, this guide walks through the real costs, the features that matter, the exact steps, and the compliance traps to launch. If you would rather skip the research and get a scoped quote, talk to our fintech team; it’s free and no-obligation.

What Is a White Label Lending Platform?

A white label lending platform is ready-made loan software, covering underwriting, origination, repayments, and servicing, that you rebrand and launch as your own product. The vendor owns and maintains the backend; you own the brand, the customer relationship, and the loan terms.

Think of it the way a franchise works. Someone else already built the recipe, the supply chain, and the back-office systems. You bring the brand, storefront, and the customer base. In lending, that “storefront” is your app or web portal; the “recipe” is the underwriting engine, compliance checks, and payment rails running behind it.

White Label vs. Custom Lending Platform Development

This is one of the most common questions we get, so we have written a dedicated comparison of white label vs custom fintech solutions covering cost, time, and risk across all of fintech.

For lending specifically, here’s the short version:

| Factor | White Label | Custom Build |

| Time to launch | 6 to 16 weeks | 6 to 12+ months |

| Upfront cost | $15,000 to $80,000 | $80,000 to $300,000+ |

| Ownership of tech | Vendor owns core, you own brand | You own everything |

| Compliance burden | Mostly handled by vendor | You own it fully |

| Best for | Fast market entry, validating demand | Proprietary credit models, long-term differentiation |

If you are pre-revenue and testing a lending idea, white label gets you live fast. If you already have volume and need a credit model or workflow no vendor offers off the shelf, custom development, or a hybrid (white label now with a migration path later), makes more sense.

One exception worth flagging: if you are specifically building a P2P lending platform, custom development tends to win more often than white label, since borrower-lender matching, regulatory requirements, and credit-scoring are usually too specific to fit a generic template well. Our P2P lending app development guide covers that build in detail.

Is White Label Lending Profitable?

Yes, when the unit economics are set up right. Revenue usually comes from origination fees, servicing fees, interest spread, or referral commissions if you are routing to third-party lenders. Because white label cuts your upfront tech speed by around 60 to 70 percent compared to custom builds, you reach profitability faster.

But margins are generally thinner than a fully custom platform since you are paying ongoing license or transaction fees to the vendor. Run the math on your expected loan volume before committing to a pricing model (flat license fee vs. per-transaction).

Do You Need a Lending License to White Label?

Not necessarily. Non-financial brands routinely embed lending into their product using white label platforms without holding a lending license themselves; the licensed bank or NBFC partner behind the platform handles the regulatory activity (funding, collection, and underwriting).

Your job is the distribution, branding, and customer experience. That said, licensing requirements vary by loan type (BNPL, personal loans, mortgages, and business loans), by country, so confirm this with legal counsel before launch rather than assuming it.

Key Features a White Label Lending Platform Needs

Below are the features you can consider for your white-label lending platform development.

| Feature | What It Includes | Business Benefit |

| Borrower Application Flow | Mobile-first application, minimal fields, save-and-resume functionality | Reduces application abandonment and increases completed loan submissions |

| Automated KYC/AML Verification | Identity verification, KYC/AML checks, sanctions screening, document capture | Accelerates onboarding, ensures compliance, and keeps your lending platform audit-ready |

| Credit Decisioning Engine | Credit bureau integration, alternative data sources, configurable risk rules | Improves approval accuracy while minimizing default risk |

| Decline Waterfall Routing | Automatic routing of declined applications to secondary and tertiary lenders | Increases loan approvals, preserves revenue, and minimizes lost opportunities |

| Loan Servicing & Repayment Tracking | Repayment schedules, reminders, auto-debit, late-fee management | Simplifies servicing, improves repayment rates, and reduces manual effort |

| Admin & Analytics Dashboard | Approval metrics, portfolio performance, delinquency tracking, operational insights | Enables data-driven decisions and early identification of portfolio risks |

| API Integration Layer | Credit bureaus, bank verification, payment gateways, core banking integrations | Simplifies third-party integrations and supports future platform expansion |

| White-Label Branding | Custom logo, colors, domain, and notification templates without backend changes | Delivers a fully branded lending experience with faster deployment |

For a broader look at features and roadmap beyond white label specifically, our guide on building a loan app covers the same ground for fully custom builds.

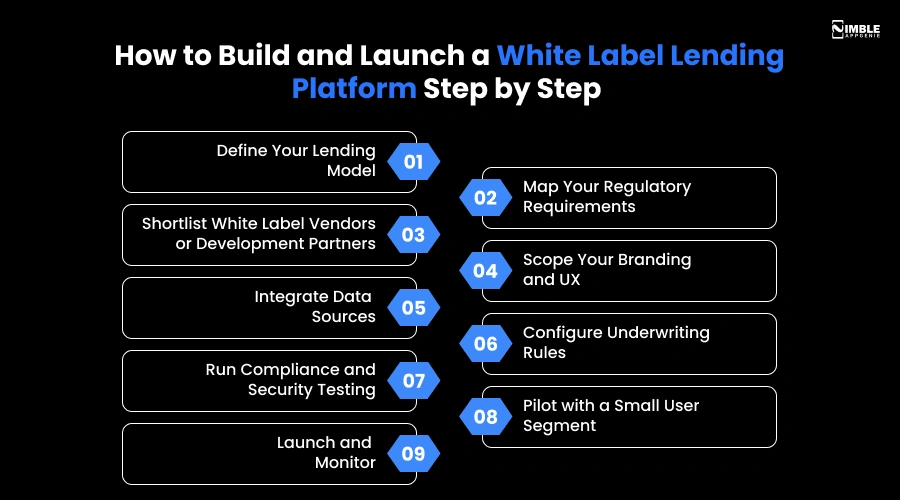

How to Build and Launch a White Label Lending Platform: Step by Step

Here is the process to develop a white label lending platform:

1. Define Your Lending Model

Personal loans, business loans, BNPL, or P2P. This decides which vendors and compliance rules apply.

2. Map Your Regulatory Requirements

State/country lending laws, data privacy rules (GDPR, CCPA), KYC/AML obligations.

3. Shortlist White Label Vendors or Development Partners

Evaluate on customization depth, security certifications (PCI DSS, SOC 2), integration options, and pricing model.

4. Scope Your Branding and UX

How much do you want to customize beyond colors and logo? Borrow journey, checkout experience, and consent flows all vary by vendor.

5. Integrate Data Sources

Bank verification, credit bureaus, identity providers, through the platform’s API layer.

6. Configure Underwriting Rules

Loan terms, risk thresholds, interest rates, and the decline waterfall if you are using multiple lenders.

7. Run Compliance and Security Testing

This is not optional; a single gap here can shut down your launch.

8. Pilot with a Small User Segment

Monitor approval rates and drop-off points, then scale.

9. Launch and Monitor

Track loan volume, customer feedback, and delinquency, then iterate.

Most of this timeline compresses to 6 to 16 weeks with an experienced implementation partner, versus 6 to 12+ months building the same stack from zero. Our loan management software guide breaks down the servicing side of this deeper if that’s your focus.

Cost of White Label Lending Platform Development

Let’s check the cost breakdown with the timeline and scope you need to know for your digital lending platform.

| Scope | Estimated cost | Timeline |

| Basic white label (single lender, standard KYC, hosted UI) | $15,000 to $35,000 | 6 to 8 weeks |

| Mid-tier (multi-lender waterfall, custom branding, dashboards) | $35,000 to $80,000 | 8 to 14 weeks |

| Advanced/hybrid (white label core + custom modules layered on top) | $80,000 to $150,000+ | 12 to 20 weeks |

| Fully custom lending platform (for comparison) | $150,000 to $400,000+ | 6 to 12+ months |

Cost shifts based on the number of loan products, geographic compliance scope, lender integrations, and how deep your branding and workflow customization needs to go. Ask any vendor for the total cost of ownership, implementation, license fees, and ongoing maintenance, not only the upfront number.

Compliance and Security Checklist

- KYC and AML verification built into onboarding, not bolted on after, so you are not caught exposed the first time a regulator asks.

- PCI DSS compliance if you are handling card data, so a breach doesn’t turn into a brand-damaging headline.

- Data encryption at rest and in transit, so borrower trust is not a single security gap away from disappearing.

- Audit trails for each credit decision, which is what protects you if a regulator or a rejected borrower challenges a decision.

- SOC 2 Type II certification from your platform vendor, the quickest signal that a vendor’s security practices have actually been checked, not just claimed.

- State-by-state or country-by-country lending law compliance, specifically for interest rate caps and disclosure requirements, since one overlooked jurisdiction can pause your launch completely.

- A documented process of handling FCRA disputes and consumer credit report data if you are in the US, so disputes get resolved without turning into legal exposure.

For relevant infrastructure decisions, like whether to route lending through a Banking-as-a-Service partner, see our BaaS explainer and our breakdown of embedded finance platform development.

Common Mistakes to Avoid During White Label Platform Development

- Choosing a vendor based on price without checking compliance certifications.

- Skipping a pilot phase and launching straight to full volume.

- Underestimating how much “customization” actually costs beyond colors and logo.

- Assuming white label means zero compliance responsibility on your end; it doesn’t; you still own distribution-side obligations like disclosures and fair lending practices.

- Not asking about vendor lock-in, can you migrate your data if you outgrow the platform?

Why Work With Nimble AppGenie?

Nimble AppGenie is a fintech development company with 8+ years building secure lending platforms for NBFCs, banks, and startups across the UK, US, and UAE. We offer both ready-to-launch white label lending platforms and custom builds, including a hybrid path if you want to start white-label and layer in proprietary features later.

Our team handles credit bureau connections, multi-lender waterfall logic, PCI DSS and GDPR-aligned architecture, and KYC/AML integrations, so your platform is compliant from day one, not retrofitted after a regulator flags.

If you are also exploring BNPL or embedded lending alongside a core platform, we build those too; see our lending app development services and full lending software development solutions.

Book a free 30-minute discovery call to get a scoped cost and timeline for your white-label lending platform.

Conclusion

White-label lending platform development gets you to market in weeks instead of months, at a fraction of the cost of a custom build, as long as you pick the right vendor, scope compliance correctly, and know upfront what you are trading off in customization and margin.

If you are validating a lending idea or need to move fast against competitors already in the market, white-label is very likely the right first step. If you later need proprietary credit models or full platform ownership, a hybrid or custom migration path keeps that door open.

Ready to scope your platform? Book your free 30-minute discovery call and walk away with a real cost and timeline for your project, no obligation.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.