Banking Software Development

Banking Software Development Payroll Software Development

Payroll Software Development Our Work Process

Our Work Process Awards

Awards

Key takeaways:

- P2P lending regulations by country are different in the US, UK, EU, and UAE, so there is no single set of rules that applies everywhere.

- The US regulates P2P lending through the SEC, CFPB, FTC, and state authorities, making it one of the most complex markets to enter.

- The UK requires FCA authorisation and investor protection measures, including an appropriateness test for new investors.

- The EU uses the ECSPR framework, allowing approved platforms to operate across multiple EU countries under one licence.

- The UAE follows different regulatory frameworks depending on whether the platform operates onshore, in DIFC, or in ADGM.

- Compliance requirements directly affect platform features, onboarding processes, payment flows, and data management.

- Building P2P lending compliance into your platform’s architecture early costs far less than rebuilding it after a regulator flags a gap.

P2P lending regulations by country are one of the first factors that can make or break a platform, long before funding or design come into play. These rules decide who is allowed to lend, how investor money is protected, and what license you need before a single loan goes live.

They are also far from uniform. A platform that complies with the rules in one country may face legal challenges in another. Ignoring these differences can lead to fines, delays, or a platform that cannot legally operate in the market you want to enter.

That gap is exactly where early-stage fintech teams get stuck. If you are building or running a P2P lending platform, these rules are not background reading. They influence your onboarding flow, fund management, and loan launch timeline.

This guide is built for fintech founders, CTOs, and COOs who want to avoid that mistake. It explains the key P2P fintech lending regulations by country across the US, UK, EU, and UAE, and what those needs mean for the platform you’re building.

What Is P2P Lending and Why Does Regulation Matter?

P2P lending connects a borrower with a lender directly through an app without a bank acting as the middleman. Fintech compliance and digital payment regulations are important because it decides who can lend, how investor money is protected, and what licence a platform needs before it takes a single loan.

How It Actually Works?

- A borrower applies through the platform.

- The platform runs a credit check and assigns a risk grade.

- Lenders browse loan listings and fund them, often spreading money across many borrowers to manage risk.

- Repayments flow back to lenders every month, minus the platform’s fee.

Regulators stepped in because this model can fail fast without rules. The UK’s Lendy collapsed in 2019 and froze investor funds. China’s P2P sector, once worth over $160 billion, fell apart after 2015 when platforms like Ezubao turned out to be running Ponzi schemes.

Every region responded differently, which is exactly why one global rulebook for P2P lending does not exist. In short, there are at least four separate security and compliance concerns for digital lending apps here, and each one shapes what you build and where you launch first.

How Does the US Regulate P2P Lending?

In the US, the SEC regulates the investor side of P2P lending, while the CFPB and FTC regulate the borrower side. Most platforms partner with a bank to issue the loan, then sell investor notes as registered securities.

Quick Facts: P2P Lending Regulations USA

| Regulators | SEC (investors) + CFPB and FTC (borrowers) + state regulators |

| License Needed | SEC registration or a valid exemption, plus state lending or broker licenses |

| Investor / Project Cap | No single national cap; varies by state usury law |

| Standout Rule | The “true lender” doctrine decides who is legally accountable for the loan |

| 2026 Watch | Fair-lending enforcement is shifting toward state attorneys general and private lawsuits. |

This setup dates back to 2008, when the SEC ruled that P2P notes were unregistered securities. Lending Club and Prosper had to register and start filing public disclosures, the same way a company files before going public.

That is still how most major platforms work. A bank originates the loan, the platform services it, and investors buy notes tied to its performance.

What Does This Mean for Your Development?

- Tiered onboarding for accredited versus retail investors, since note sales fall under securities law.

- Strong AML compliance software running quietly in the background, since regulators expect ongoing transaction monitoring, not a one-time KYC check at signup.

- A state-by-state licensing tracker, since rules and interest-rate caps differ from state to state.

How Does the UK Regulate P2P Lending?

The UK’s Financial Conduct Authority has regulated P2P lending since 2014 and tightened the rules in 2019. Platforms need full FCA authorisation, must run an appropriateness test on new investors, and must cap how much a first-year investor can lend.

Quick Facts: P2P lending Regulations UK

| Regulators | Financial Conduct Authority (FCA) |

| License Needed | Full authorisation to operate an electronic lending system |

| Investor Cap | Everyday investors capped at 10% of investable assets in year one |

| Standout Rule | Mandatory appropriateness test before a new investor’s first investment |

| 2026 Watch | FCA reviewing further changes; consultation closed March 2026, decision still pending |

The 2019 tightening followed Lendy’s collapse, a property-focused platform that left investors with real losses. The FCA responded by creating three investor tiers: everyday, sophisticated, and high-net-worth.

What Does This Mean for Your Build?

- An onboarding flow built around the appropriateness test, not a generic sign-up form.

- Investor categorisation logic that tracks who counts as everyday vs sophisticated, since the lending cap depends on it.

- Clean, well-designed loan lending app features for dashboards and risk disclosures, since the FCA expects investors to actually understand what they are seeing, not just click through it.

| Note: If you have completed your research and are ready to decide on features and development timelines, check out our guide on how to create a P2P lending app. It explains the process in easy step-by-step detail. |

How Does the EU Regulate P2P Lending?

The EU regulates P2P lending under ECSPR, one license valid across all 27 member states. It caps funding at €5 million per project owner per year and requires a standardized disclosure document, the KIIS, for every loan offer.

Quick Facts: EU P2P Lending Rules

| Regulator | National regulator + ESMA, under Regulation (EU) 2020/1503 |

| License Needed | One ECSP license, passportable across the whole EU |

| Project Cap | €5 million per project owner per 12 months |

| Standout Rule | A KIIS disclosure document is required for every loan offer |

| 2026 Watch | DORA cybersecurity rules now apply to every ECSP-licensed platform |

Before ECSPR took full effect in 2023, a platform needed a separate license in every country it served. Now it applies once, gets listed on ESMA’s public register, and passports that license everywhere else.

What Does This Mean for Your Build?

- Full GDPR compliance is baked into your data architecture, since every EU platform handles investor and borrower data under it.

- A KIIS-generation module that auto-fills past returns, default rates, and borrower risk profile for each loan.

- A built-in four-day reflection period for non-sophisticated investors before their investment becomes binding.

How Is P2P Lending Regulated in the UAE?

The UAE has no single P2P lending regulator. Onshore mainland platforms fall under the Central Bank’s Circular 7/2020. Platforms in the DIFC need a DFSA license. Platforms in ADGM need an FSRA license. Securities-linked models fall under the SCA.

Quick Facts: P2P Lending Regulations UAE by Zone

| Zone | Regulator | License / Activity | Approx. Capital |

| Onshore (mainland) | Central Bank of the UAE (CBUAE) | Circular 7/2020 (Loan-Based Crowdfunding) + banking license | Set by CBUAE banking rules |

| DIFC | Dubai Financial Services Authority (DFSA) | Crowdfunding platform license | ~$140,000 base capital (typical) |

| ADGM | Financial Services Regulatory Authority (FSRA) | “Private financing platform” regulated activity | ~$250,000 in practice (typical) |

| Capital markets models | Securities and Commodities Authority (SCA) | Securities-linked crowdfunding license | ~AED 1 million paid-up (typical) |

This four-way split is the part most guides skip entirely. Beehive became the first P2P lending platform licensed by the DFSA back in 2017, the first P2P lending regulatory framework in the GCC. These figures shift as regulators update their rulebooks, so confirm current numbers with a UAE-licensed advisor before you lock in a budget.

What Does This Mean for Your Build?

- Choose your zone before your app tech stack. Onshore, DIFC, and ADGM each expect different data residency and reporting setups.

- Budget for security and audit infrastructure early. All four UAE regulators expect real cybersecurity controls and audit trails, not just a working app.

US vs UK vs EU vs UAE: How Do P2P Lending Regulations Compare?

Each market regulates P2P lending differently. The US splits oversight by function, the investor side versus the borrower side. The UK uses one regulator with strict investor caps.

The EU uses one passportable license in 27 countries. The UAE splits oversight by location and P2P lending license type. Let’s take a look at the below table of comparison of P2P lending regulations by country.

| Market | Main Regulator(s) | License Needed | Investor / Project Cap | Standout Requirement |

| US | SEC (investors), CFPB/FTC (borrowers), and state regulators | SEC registration for notes sold as securities; state lending or broker licenses | No single national cap; varies by state usury laws | The “true lender” test determines who is legally responsible for the loan. |

| UK | FCA | Full FCA authorization to operate an electronic lending system | Everyday investors are capped at 10% of investable assets during their first year | Mandatory appropriateness test before the first investment. |

| EU | National regulators and ESMA under ECSPR | One ECSP license that can be used across all 27 EU member states | €5 million per project owner within 12 months | Standardized KIIS (Key Investment Information Sheet) disclosure document required for every loan offer. |

| UAE | CBUAE (Onshore), DFSA (DIFC), FSRA (ADGM), and SCA | Depends on the zone: Circular 7/2020 license, DFSA crowdfunding license, or FSRA private financing platform license | No single cap; capital requirements vary by regulator | Four possible regulators depending on where and how the platform operates. |

What is the common thread across all four? Every regulator cares about the same two things: protecting investor money and keeping the platform accountable for the loans it facilitates. They just enforce it through different paperwork.

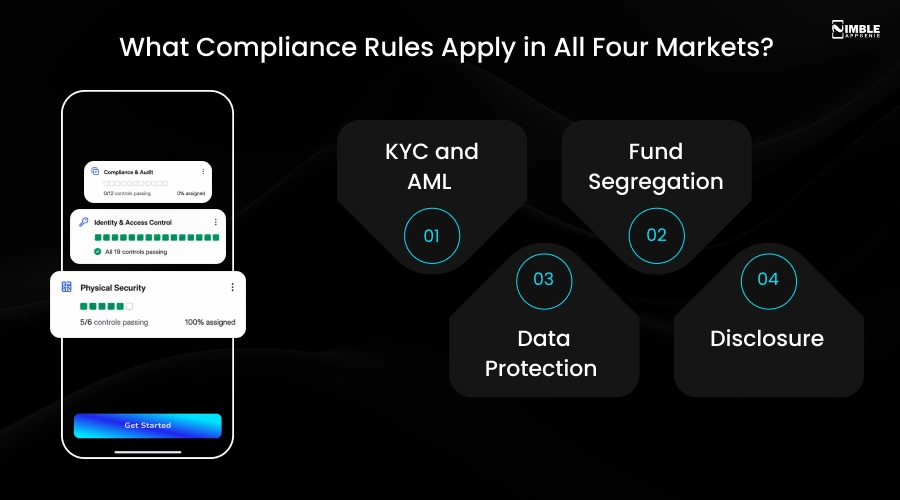

What Compliance Rules Apply in All Four Markets?

Across the US, UK, EU, and UAE, every regulated P2P lending platform needs four things in place: identity verification (KYC), anti-money-laundering checks (AML), segregated client funds, and clear, standardized disclosure to investors before they commit money.

1. KYC and AML

Identity checks at onboarding, plus ongoing transaction monitoring. How deep the check goes usually depends on loan size and investor type. We cover this in detail in our guide to KYC and AML compliance.

2. Fund Segregation

Client money cannot sit in the platform’s operating account in any of the four markets. It needs to sit in a separate, ring-fenced account, often through an independent custodian or e-money provider.

3. Data Protection

GDPR in the EU, a mix of state laws like the CCPA in the US, and the UAE’s own PDPL alongside DIFC- and ADGM-specific rules. Most of this falls under mobile app data privacy compliance, regardless of which region you build for first.

4. Disclosure

The EU’s KIIS is the most standardized version of this, but the UK’s appropriateness test and the US’s securities disclosures serve the same purpose: making sure an investor understands the risk before they commit.

Thus, if you only build one thing the same way everywhere, build a flexible KYC and disclosure layer. It’s the one requirement every regulator here shares.

What Does This Mean for Your P2P Lending App?

Each of the P2P lending regulations by country turns into a specific development decision. Tiered KYC means different verification depths per investor type.

Fund segregation means a ledger that physically separates client money from company money. Disclosure rules mean a document generator that updates per region.

Most first-time founders get this backwards. They develop the loan marketplace first and treat P2P lending compliance like a feature to add at the end. By the time they get to it, the data model is already wrong and fixing it costs far more than building it right from the start.

Development Priorities, in Order

- Design your fund segregation model and KYC tiers before you touch the matching engine.

- Use AI in lending for credit risk scoring, but keep the model explainable. Every regulator we covered above expects a reason behind a credit decision.

- If your platform touches card payments anywhere in the loan or repayment flow, develop PCI compliance for fintech apps from day one.

Which Country Should You Launch Your P2P Lending Platform In First?

Choose your first market by capital and target users, not by preference. The EU offers the lowest entry capital and one license for 27 countries.

The UK offers a mature investor base with stricter first-year caps. However, the US offers the biggest market with the most fragmented licensing. The UAE offers fast GCC access if you pick the right zone. Let’s take a look:

- Tight budget, want maximum reach? You can start in the EU. It needs one license, lowest entry capital, 27 countries covered.

- Mostly UK-based users? You can start in the UK, but plan for a stricter onboarding flow from day one.

- Already have US banking partnerships? The market size can outweigh the licensing complexity.

- Targeting GCC investors or SME borrowers? The UAE’s free zones move fast, but only if you choose the right zone upfront.

How Nimble AppGenie Helps You Build a Compliant P2P Lending Platform?

Nimble AppGenie is a trusted P2P lending platform development company that creates P2P lending platforms with KYC, AML, fund segregation, audit logging, and region-specific disclosure modules built into the architecture from the first sprint.

One thing we are upfront about: getting licensed by the SEC, the FCA, an EU regulator, or the DFSA, FSRA, and SCA in the UAE is a legal process. You need a regulatory lawyer for that part.

What we handle is the technology side, developing a platform where the data model, the ledger, and the disclosure logic are already shaped for whichever rulebook you are building toward.

What We Build In, From Sprint One?

- Modular KYC and AML integrations you can swap or layer per region.

- A segregated-funds ledger architecture, designed the first time correctly.

- Audit logs on every credit decision and every disbursement.

- Region-specific disclosure templates generated from the same underlying data.

- Fraud detection and risk-monitoring layers that scale as your loan volume grows.

If you are scoping a P2P lending platform and want the compliance architecture mapped out before development starts, our fintech-dedicated development team is happy to walk through your target markets with you.

Conclusion

Now that you know P2P lending regulations by country. It is time to choose your first market based on capital and target users, not preference. A few quick pointers. If your budget is tight and you want one license to cover the most ground, start in the EU.

But if your users are mostly UK-based and you can handle a stricter onboarding flow, start in the UK. Besides, if you already have US banking partnerships lined up, the US market size can outweigh the licensing complexity.

Lastly, if you are targeting GCC investors or SME borrowers, the UAE’s free zones move faster than most people expect, but only with the right zone chosen upfront. However, if you are confused, a fintech software development company can assist you with P2P lending regulations and launch the best platform.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.