Banking Software Development

Banking Software Development Our Work Process

Our Work Process Awards

Awards

Key Takeaways:

- With the growing use of fintech apps, fintech fraud types are increasing.

- The top fintech fraud types comprise social engineering, presentation attacks, account takeover, payment fraud, money muling, and first-party fraud.

- AI helps to catch fintech fraud types by evaluating the current user behavior, and helping fintech companies to identify fraud patterns and reduce them in advance.

- One should opt for AI-based fintech fraud detection rather than traditional fintech fraud detection, as it offers dynamic patterns to identify and mitigate fraud.

- Partner with Nimble AppGenie and build your own AI fraud detection system.

The diversified exposure area, such as speed, scaling, minimal physical friction, and new user bases unfamiliar with digital threats, all these risks are leading to an increase in fintech fraud types.

Additionally, zero physical branch verification, digital onboarding, and real-time payment rails result in fintech fraud.

Globally, the cyber-enabled fraud now costs the economy roughly $1.1 trillion a year, a figure equivalent to approximately 3% of the global GDP.

Additionally, the AI-enabled financial fraud detection is expected to exceed $10 billion by 2027. Well, with this growing spend on AI-enabled financial fraud detection, it can be stated that AI is not the future; it’s the current landscape.

If you are a fintech startup and an entrepreneur, looking forward to learning more about fintech fraud types and the AI role in it, it’s the right place to be.

In this guide, we’ll walk you through different types of fintech fraud and how AI catches them.

What is a Fintech Fraud?

Fintech fraud is any deceptive, illegal, or unauthorized activity targeting digital financial services, such as mobile wallets, peer-to-peer lending, online banking, and cryptocurrency platforms.

Fintech uses automation and machine learning to speed up transactions; additionally, scammers exploit digital pathways for performing unauthorized transactions and even money laundering activities.

The attackers typically combine different types of fintech fraud, including identity theft, payment abuse, system exploitation, and others, to bypass the modern financial apps and digital wallets.

Bonus Read: “What is Fintech?”

But why does this fintech fraud happen?

Why Fintech Fraud Happens?

The major reasons for fintech fraud are that digital platforms process the massive volumes of money instantly, store sensitive data, and rely on quick access rather than strict security.

Hence, fraudsters identify the gap in these streams, exploit this speed, use artificial intelligence, and social engineering to use the user credentials and to trick individuals.

Here’s the list of reasons why fintech fraud happens:

1. Weak KYC and AML Controls

When fintech startups and firms treat KYC and AML compliance as a checkbox rather than a security layer, it can compromise the overall security of a fintech app.

The fragmented and under-configured identity verification allows synthetic identities and fabricated documents to pass onboarding and opens the door to downstream fraud.

2. No Room for a Manual Check

The fintech apps, including UPI, RTP, Fednow and instant ACH, complete the transfers in seconds. Hence, when a suspicious activity is flagged, the funds have already moved.

Later, the reverse of funds becomes impossible, which offers fraudsters a near-zero window of exposure.

3. No Physical Verification

Through digital-first onboarding, fintech platforms use no face-to-face checks and no branch visits.

Hence, it creates a room for the fraudsters to submit fake, synthetic, and AI-generated identities during the complete sign-up process, which leads to fraud and cybercrimes.

4. Following the Rule-Based Detection Systems

The static rule engines catch the fraud patterns that were explicitly programmed to recognize. The fraud tactics evolve faster than the rules are updated.

When the fintech firms follow rule-based systems rather than implementing the advanced security patterns, it offers the fraudsters a window to actively exploit just below detection thresholds.

5. Rapid User Growth

The rapid use of fintech and online payment apps has resulted in outspending security infrastructure. Rather than focusing on the fraud controls, fintech startups are scaling their user base.

For instance, a platform built for 10,000 users often lacks monitoring capabilities to handle fraud at 10 million users. It creates a gap during hypergrowth phases.

Now, as you know why fintech fraud happens, you should know different types of fraud take place with fintech apps.

Let’s look at all the types of fintech fraud in the following section.

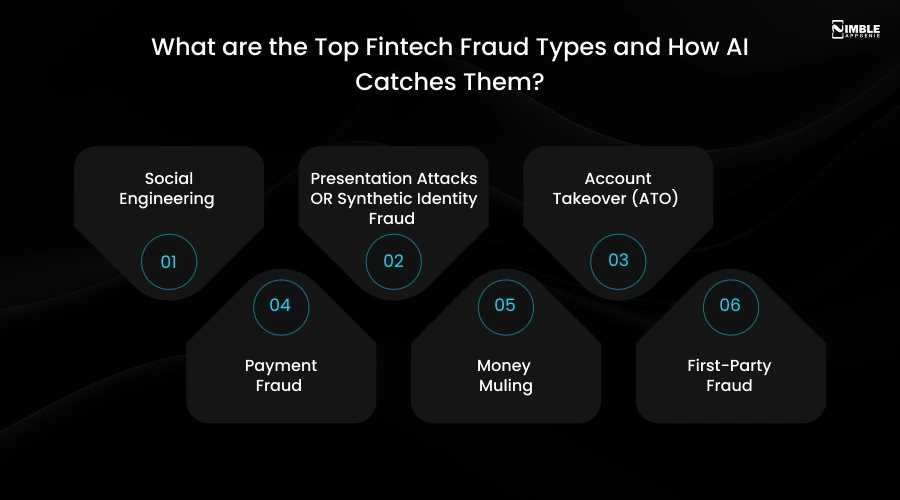

What are the Top Fintech Fraud Types and How AI Catches Them?

The key fintech fraud types are social engineering, account takeover, ACH fraud, money muling, chargeback fraud, and presentation attacks.

Let’s get ahead with the details:

1. Social Engineering

What is it?

Social engineering is a fintech fraud type that manipulates human psychology to trick people into giving away sensitive information and access to money.

Under this type of fintech fraud, the fraudsters track human behavior by exploiting emotions such as fear, curiosity, and instinct to help. Thus, they hand over the control of fintech security to the fraudsters, which leads fintech users to loss.

Why its Dangerous?

- Exploits Human Trust

- Bypass Technology

- Gateway to Larger Breaches

- Massive Financial Losses

- Amplified by AI

How AI Catches it?

- Perform Contextual Evaluation

- By deepfake detection

- Behavioral analysis

- AI systems from BioCatch identify the micro-latency patterns

2. Presentation Attacks OR Synthetic Identity Fraud

What is it?

This type of fraud takes place when the fraudster tries to fool the biometric pattern, such as facial recognition and voice authentication, by presenting a fake, altered, and manipulated copy.

This act is also known as spoofing, which is created to bypass KYC onboarding and to initiate unauthorized financial transactions.

Why its Dangerous?

- Offers scalable automation

- Direct monetary fraud

- Bypass KYC in fintech apps

- Scalable automation

How AI Catches it?

- Liveness detection through micro-texture analysis

- Document tampering detection

- Deepfake video and audio detection

- Screen flipping and Emulators

3. Account Takeover (ATO)

What is it?

Account takeover is among the top fintech fraud types and cybercrime where the unauthorized party takes complete control over a legitimate account. This takes place mainly through credential stuffing, phishing, and SIM swapping.

Once inside the account, the fraudster impersonates the real user, stealing all the sensitive data, and through making fraudulent transactions.

Why its Dangerous?

- The attackers control a real account with a verified identity

- Makes traditional fraud rules blind to the threat.

- A hijacker impersonates you to send scam messages to trick your friends.

- A hacker can easily reset the passwords of other accounts connected to your attacked account.

How AI Catches it?

- Opt for behavioral analysis

- Device & network fingerprint

- Perform Velocity Analysis

- Through continuous verification

4. Payment Fraud

What is it?

The increasing use of ACH (Automated Clearing House) and other real-time payments, including RTP, SWIFT, and UPI. It is a kind of illegal or unauthorized transaction committed by a criminal to steal money and sensitive data from individuals.

This happens because fintech relies on rapid digital transfers, including UPI, digital wallets, and mobile apps. It is among the top fintech fraud types where fraudsters gain financial interest by manipulating the payment gateway.

Why its Dangerous?

- It creates immediate, irreversible financial loss.

- Destroys trust in the digital economy.

- Business and reputational damage.

- Identity and data compromise.

How AI Catches it?

- Real-Time Risk Scoring

- Anomaly Detection

- Behavioral biometric

- Device fingerprinting

- Ensemble AI Models

5. Money Muling

What is it?

Money Muling is a form of money laundering that hides the money’s source, makes it hard to trace, and makes the ordinary person’s account a gateway for money laundering.

These networks use chains of accounts to layer and move the fraudulent firms into their own accounts. They try to make the fraudulent funds to cash out proceeds from scams or cyber attacks, making the fraudulent funds looks normal, and regular.

Why its Dangerous?

- Makes you move stolen funds so they can hide their identities.

- You can be sentenced to prison.

- Federal or state prosecution for money laundering.

- Each transaction appears legitimate.

How AI Catches it?

- By analyzing hundreds of data points in milliseconds to spot abnormal behavior.

- AI continuously learns from historical data to adapt to new scams in real-time.

- Network and graph analytics.

- By analyzing a vast network of transactions and user behavior.

6. First-Party Fraud

What is it?

The first-party fraud is committed by real, verified users. Here, the common types of first-party fraud include chargeback abuse, loan stacking, and intentional default.

This type of fraud takes place when a genuine person or identity opens an account or secures a loan, but does so with the deliberate intention to deceive the financial institution and steal money.

Why its Dangerous?

- First-party fraud is hard to detect early

- Damages the reputation of an individual

- The perpetrator has a real identity and passes all the KYC checks

- Hides as regular debt.

How AI Catches it?

- AI-enabled financial fraud detection identities frauds via behavioural analytics and biometrics

- Predictive machine learning models

- By building detailed behavioral profiles and analyzing the complicated hidden patterns.

- Cross-referencing unstructured data

Here’s the table defining fraud types, how fraud takes place, and its AI detection technique in brief:

| Fraud Type | Attack Method | Primary Target | AI Detection Technique |

| Account Takeover (ATO) | Credential stuffing, phishing, SIM swap | Login + transactions | Behavioral biometrics, device fingerprinting |

| Synthetic Identity Fraud | Real SSN + fake profile data | Digital onboarding, lending | Graph analysis, behavioral pattern ML |

| Payment Fraud | Stolen card data, unauthorized transfers | Payment rails | Real-time transaction scoring, anomaly detection |

| Deepfake / AI Identity Fraud | AI-generated face/voice/documents | KYC onboarding | Liveness detection, document forensics AI |

| Money Muling / AML Evasion | Layered transactions through Mule accounts | Fund transfers | Graph network analysis, AML ML models |

| First-Party Fraud | Chargeback abuse, loan stacking | Lending, payments | Behavioral history modeling, credit graph analysis |

| Phishing & Social Engineering | Fake comms to extract credentials | Users + staff | NLP-based phishing detection, email analysis AI |

| Insider Fraud | Employee misuse of access | Internal systems | User behavior analytics (UBA), access anomaly detection |

| Friendly Fraud | Legitimate users disputing valid transactions | Chargeback process | Transaction history ML, device + behavioral match |

| Bot Attacks / Credential Stuffing | Automated login attempts at scale | Authentication layer | Bot fingerprinting, velocity checks, CAPTCHA ML |

Well, why do you need an AI-based detection? Why can’t you opt for a rule-based fraud detection?

The following section will determine the same.

Rule-Based Fraud Detection vs. AI – What’s Changed?

The rule-based fraud detection uses a simple “if/then” logic for automatically flagging suspicious transactions. This type of fraud detection in fintech is based on a set of unusual attributes, comprising unusual time stamps and transaction types.

However, the AI fraud detection is an automated process that uses AI and machine learning to identify and prevent fake transactions or malicious activities. Here’s a table defining the complete differences:

| Capability | Rule-Based Systems | AI / ML Systems |

| Adaptability | Static — rules require manual updates | Dynamic — models retrain on new fraud patterns automatically |

| False positive rate | High — blocks legitimate users | Lower — nuanced risk scoring reduces friction |

| Detection speed | Batch processing (hours/days) | Real-time (sub-200ms per transaction) |

| Synthetic identity detection | Blind — each data point looks valid | Strong — detects behavioral and network patterns over time |

| Deepfake detection | Impossible | Liveness + document forensics AI |

| Explainability | Easy to audit | Requires explainable AI (XAI) design for regulatory compliance |

| Scale | Degrades at high volume | Improves with more data |

| New fraud types | Requires manual rule addition | Detects anomalies even without a predefined rule |

Well, opting for the top fintech APIs can be an effective pattern to minimize fintech fraud along with AI integration.

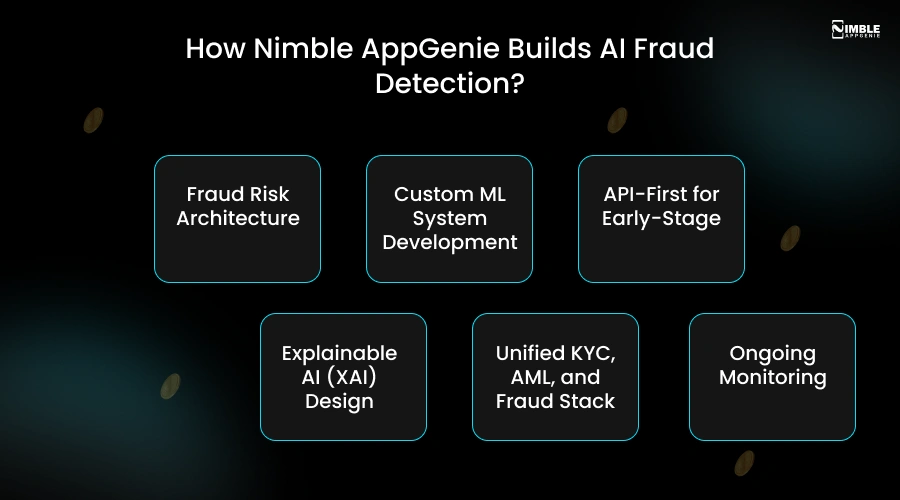

How Nimble AppGenie Builds AI Fraud Detection?

Nimble AppGenie specializes in offering AI-based fraud detection, as we are ISO certified company, and have delivered 350+ fintech products. We are the best fintech software development company offering services such as:

1. Fraud Risk Architecture

Scoping your threat surface by platform type, such as neobank, payment app, lending, and crypto. We map the fraud detection stack to your specific attack vectors.

2. Custom ML System Development

Nimble AppGenie builds proprietary transaction scoring models, behavioral biometrics layers, and graph analysis engines on your own data.

3. API-First for Early-Stage

We offer rapid integration of Sift, SEON, Sardine, or Onfido for fintech app development. Here, we offer production-ready fraud detection without a 6-month custom build.

4. Explainable AI (XAI) Design

Every fraud decision that we take for your software is auditable and accompanied by reason codes, satisfying regulators under the EU AI Act and DORA.

5. Unified KYC, AML, and Fraud Stack

We built a single integrated compliance and fraud intelligence layer for the unified KYC, AML, and fraud stack, not three separate tools talking to each other.

6. Ongoing Monitoring

Our experts offer regular mobile app maintenance and support services, where we provide a post-deployment model drift detection, regular testing, and restraining pipelines to keep the detection rates high as fraud evolves.

Conclusion

AS the demands of fintech apps and platforms rise, the variants of fintech fraud are rising too. These frauds are unable to be controlled via traditional fraud detection tools and techniques.

The different types of fintech fraud that might impact your fintech business are social engineering and identity theft. Account takeover, payment fraud, money muling, and first-party fraud.

In social engineering fintech fraud, the fraudsters trick humans psychologically by playing on their emotions. In the presentation attacks, the fraudsters try to fool the biometric by creating a fake identity. While in account takeover, the fraudsters take over the account credentials to steal money. Payment fraud is a kind of unauthorized transaction conducted to steal money.

Here, AI helps to detect the consumer behavior pattern and then controls the authorized activities. Connecting with the team of experienced experts can be helpful.

FAQs

The diversified fintech frauds that might impact you and your fintech business are social engineering, presentation attacks, account takeover, money muling, and first-party fraud.

AI identifies fintech fraud after evaluating the user’s behaviour, analyzing the different types of queries, and using thousands of data points in real time. Additionally, instead of simple rules, AI builds behavioral baselines for users and flags unusual activities in milliseconds.

Yes, you can. At this stage, you cannot ignore implementing the AI fraud detection parameters. A team of experienced fintech app developers can help you in opting for the best APIs and an AI protection layer that supports your transaction volume and provides an effective AI fraud detection layer.

Well, you can opt for multi-jurisdiction compliance. Here, you might come across fintech fraud. Thus, connecting with the team of experts who understand compliance is where most fintech fraud breaks.

The answer is continuous model retraining, cross-institution threat intelligence, and adversarial testing. Build fraud protection systems that improve as fraud evolves, not ones that need a manual update every time a new attack type emerges.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.