AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Nearly half, or we can say 40% of Americans, have not stepped into a bank or credit union in the last six months.

This shows that people are moving away from traditional banking services and want faster, safer, and easier ways to manage their money.

That’s where blockchain in banking is playing a big role in making this happen. It is a new kind of technology that keeps records safe, reduces fraud, and removes the middlemen.

It also makes sending and receiving money a lot cheaper.

Many banks are now leveraging blockchain to improve their banking services and build more trust with customers.

As everything becomes more digital, blockchain in the banking industry is quickly becoming a key part of the industry’s future.

Therefore, in this blog, we will see how blockchain in the banking sector is changing the way banks work and what it means for businesses.

So, let’s begin!

What is Blockchain?

Blockchain is a system that stores information in a way that makes it almost impossible to change or tamper with.

It is just like a shared online ledger that many people or computers have access to.

Each piece of information, like a transaction or data entry, gets added to a block. When one block is full, it gets connected to the previous block. This is why it is called blockchain.

This chain of blocks makes it really hard to break with the data because changing one block would mean changing all the others, which would be noticed immediately by everyone else.

It is decentralized, and everyone can verify the information. That’s why it is used for things like cryptocurrencies, bitcoin, and secure record-keeping.

Role of Blockchain in the Banking Industry

Blockchain is transforming how banks work. It keeps records that cannot be changed and allows banks to share trusted data fast.

This makes things like loan approvals, transfers, and identity checks faster.

The blockchain market is booming, worth $31.28 billion in 2024, and it will hit $1,431.54 billion by 2030. At the same time, people are using mobile phones more for money than ever.

Mobile banking statistics show that by 2025, about 72% of US adults will use mobile banking apps.

By combining these trends, the blockchain and banking industry go hand-in-hand. It helps banks become faster and more effective.

You have to keep up with how people want to bank in this competitive market.

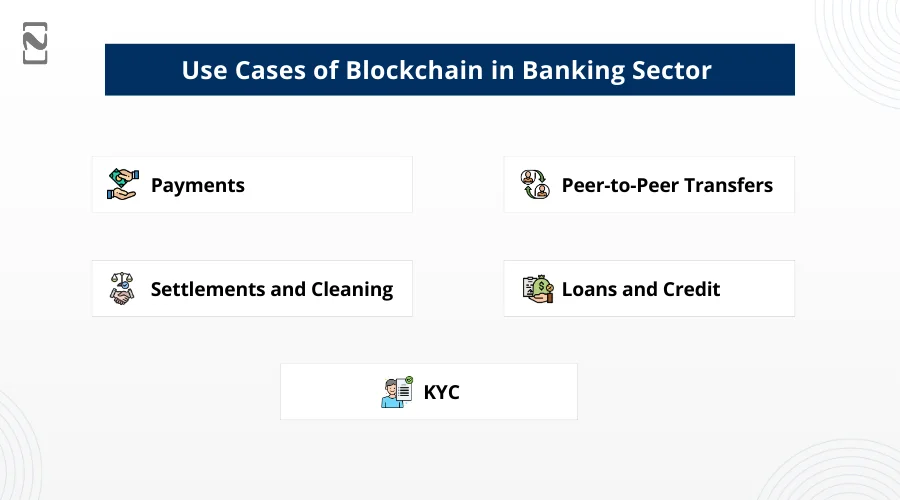

Use Cases of Blockchain in the Banking Sector

Blockchain might sound like a tech buzzword. But it is actually making banking a way better.

Let’s look at how it helps in real life.

-

Payments

Sending money from one country to another is usually slow and quite expensive. Banks charge high fees, and your money goes through multiple steps before it reaches the other side.

With blockchain, you can send money fast and cheaply. It is like sending a text message, but with money. Done in minutes, not days.

-

Peer-to-Peer Transfers

Banking apps like Venmo and Cash App allow you to pay your friends easily. But behind the scenes, blockchain and banks are still involved, which means delays and small fees.

Blockchain technology and banking can cut all that out. You can send money directly to your friend. No banks, no waiting, no extra costs. And it is safe too.

-

Settlements and Cleanings

When banks send money to each other, it is a slow and messy process. It often requires people to check things manually.

With blockchain in the financial industry, everything is automatic and tracked in real time. No delays, fewer mistakes, and no need for so many people in the middle.

-

Loans and Credit

Right now, getting a loan means filling out forms, waiting for your credit to be checked, and hoping the bank says yes.

Blockchain in fintech is changing that by making this process faster and transparent. Your financial information is stored safely and cannot be changed.

Banks can see it clearly and make faster decisions. There is also something called a SoulBound Token.

You carry it with you, and any bank can quickly see your past loans, payments, and how reliable you are.

-

KYC

When you open a bank account or sign up for a new app, you have to prove who you are. It is annoying and slow.

Blockchain can save your details safely. Once it is verified, you do not have to keep sending it again and again.

And those SouBound tokens? They work here too. They can hold your ID information securely. So banks can trust it is really you without wasting time.

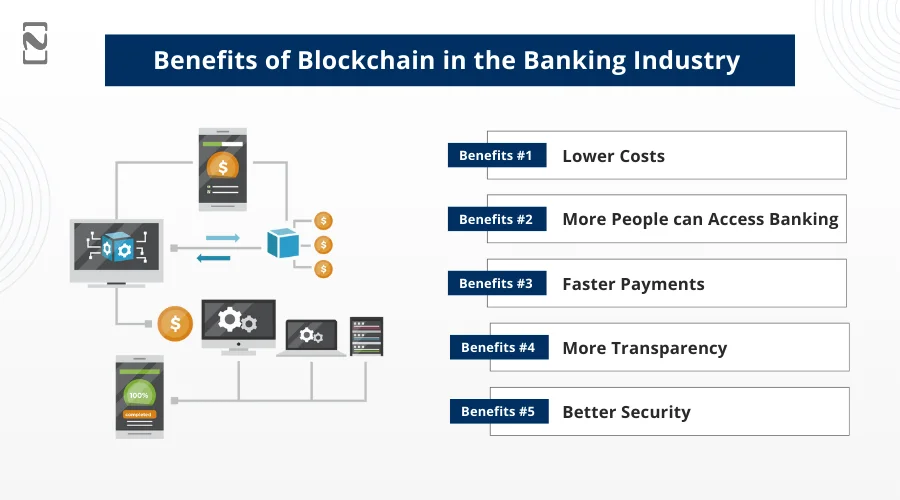

Benefits of Blockchain in the Banking Industry

Let’s take a look at how blockchain is helping by leveraging Banking as a Service (BAAS).

It’s kind of amazing when you think about it, a technology that started with Bitcoin is now changing how banks work.

By understanding the real benefits, it is easy to see that blockchain is not just a trendy word; it is making a huge difference.

So, let’s see how blockchain is changing the game in the banking industry.

1. Lower Costs

Blockchain helps banks save money by removing the middlemen usually needed in financial transactions. That means very few steps, less paperwork, and lower fees.

It is for both banks and for customers. It makes things quicker and cheaper for everyone.

2. More People Can Access Banking.

Since Blockchain in banking makes core banking software easy and cheaper to run, it can help bring banking services to people who have never had access before.

This is a big deal for communities that have been left out of the traditional banking system.

3. Faster Payments

Usually, sending money between banks can take a few days. This can be frustrating. But with blockchain, those same transactions can happen in just a few minutes, sometimes even seconds.

It makes money a lot faster and smoother.

4. More Transparency

When you build a blockchain app for the banking sector, all transactions are recorded in a way that they can be traced and verified.

This helps build trust between banks and customers. That’s because everything is clear and out in the open with no hidden fees.

5. Better Security

Blockchain is developed in a way that makes it very hard for hackers to mess with. Every transaction is recorded and locked in place.

This makes it super secure and safe. This means your money and data are much safer compared to older systems.

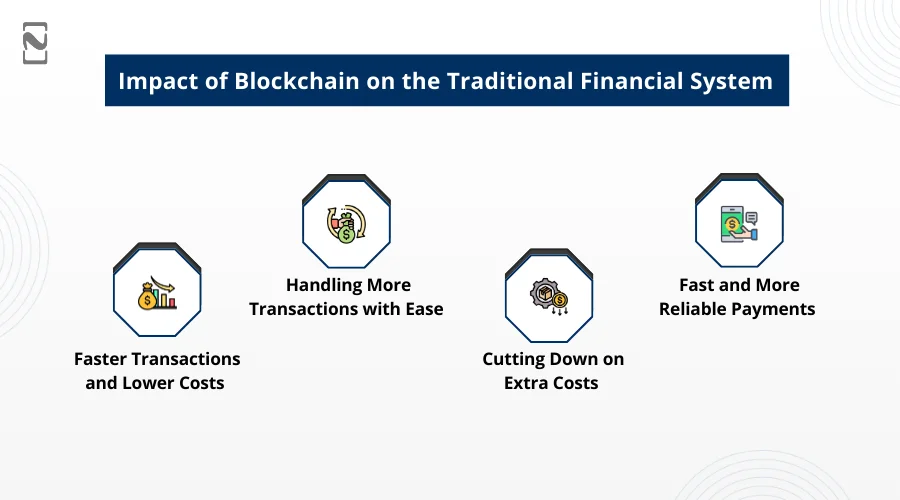

Impact of Blockchain on the Traditional Financial System

As a banking app development company begins to utilize Web3 and blockchain technology, we can expect significant changes in how the financial world operates.

Through our custom fintech app development services, we tailor blockchain integration to your existing banking stack instead of forcing a rebuild.

♦ Faster Transactions and Lower Costs

Blockchain helps fintech companies in developing a mobile app like Chase or others that are way quicker and cheaper than what banks use today.

With blockchain technology, transactions do not need people to approve them, and the app can run 24/7. That means things get done faster and at much lower cost.

♦ Handling More Transactions with Ease

Most banks can only handle a limited number of transactions because their systems are old and need people to step in often. Blockchain changes that.

You can build apps with the integration of AI in banking. It handles tons of transactions at once, smoothly and without slowing down. It also removes the need for a middleman.

♦ Cutting Down on Extra Costs

Blockchain allows banks to use smart contracts, which are like digital agreements that run automatically.

These do not need people to manage them, so banks save money on operations. In the long run, this helps them lower their costs and still offer a great experience to customers.

♦ Fast and More Reliable Payments

People today want things done fast, and companies get that. That’s why more of them are using blockchain in their banking apps.

It lets them skip third-party checks and process transactions almost instantly. On top of that, every transaction is safely recorded in a public system, which builds trust and adds transparency for users.

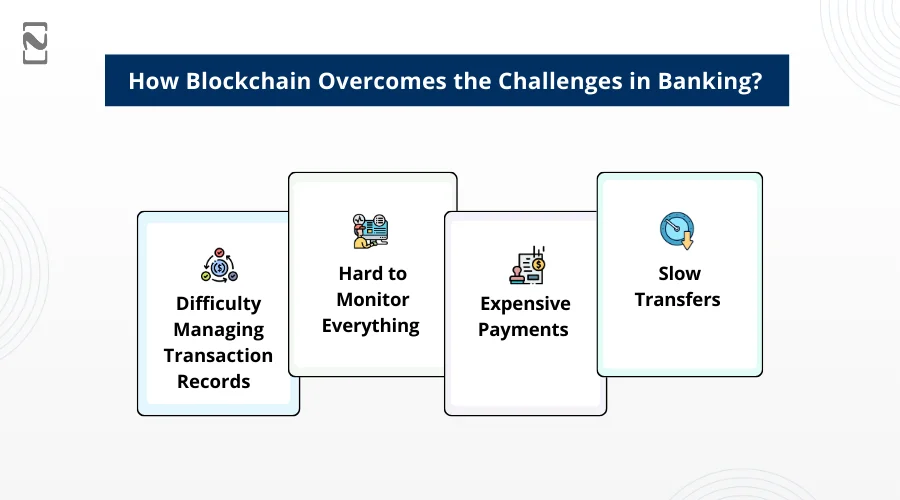

How Blockchain Overcomes the Challenges in Banking?

Banks today face many problems, such as slow processes, high costs, and security risks. Blockchain technology provides a smart way to solve these problems.

Let’s have a look at how it can help make banking on blockchain faster, safer, and more reliable.

1. Difficulty Managing Transaction Records

As more people use online banking services, it is quite challenging to keep track of every transaction. Traditional systems often get slow and messy. This delays payment and increases errors.

How Blockchain Helps:

- Once data is added to a blockchain, it cannot be changed. This keeps records safe and trustworthy.

- Also, blockchain can check and confirm data without showing personal details, thanks to special tech like zero-knowledge proofs.

- Public keys allow everyone to see basic information, while private keys protect sensitive details. This keeps data both private and transparent at the same time.

2. Hard to Monitor Everything

Banks now work mostly online, but it is tricky to keep an eye on digital activity like loan usability. They often depend on third parties, which brings risks like fraud or misuse.

How Blockchain Helps:

- People can deal directly with each other through the blockchain network.

- Every action is recorded automatically, so it is easy to follow the money.

- The mobile banking app security is managed through smart contracts. It’s like digital agreements that run on their own to make sure everything happens as planned.

3. Expensive Payments

Every time a payment goes through, banks pay fees to third parties and spend money on maintaining large systems. All these costs add up, and customers often feel the impact too.

How Blockchain Helps:

- Fewer middlemen mean lower transaction costs or fees.

- Smart contracts handle tasks automatically and reduce paperwork.

- When combined with digital onboarding in banking, it creates a faster and cost-efficient process.

4. Slow Transfers

Some payments, like international ones, can take many days to go through. That is because they pass through many hands before reaching the final destination. This can make the money transfer process very slow.

How Blockchain Helps:

- Through blockchain mobile payment technology, transactions happen directly between users, without any kind of delay.

- Smart contracts can take care of approvals instantly.

- No need for multiple steps or third parties, so money moves fast.

What’s the Future of Blockchain in Banking?

The future of blockchain in banking is already taking shape. A major blockchain financial industry is already planning to create a mobile banking app with blockchain technology.

But to keep up with the speed of change, banks need to go beyond just testing.

They need to focus on automating more tasks and delivering a smoother, more seamless digital experience for their users.

A big part of this progress will come from partnerships. When banks collaborate with a blockchain app development company, they can overcome technical challenges, close knowledge gaps, and build the solid infrastructure needed to fully embrace blockchain banking technology.

With the right approach, blockchain in financial services and banks can reduce operational expenses, speed up payment processing and settlements, and boost overall security in their systems.

Let Nimble AppGenie Transform Your Banking App with Blockchain!

Banking is changing fast, and customers expect more than just the basics. That’s where Nimble AppGenie comes in.

We help turn regular banking apps into smart and secure platforms by using blockchain technology.

We integrate blockchain technology into a blockchain app that can make a huge difference, not just in how it works, but in how it feels to use.

It makes waiting less, has fewer errors, and gives more peace of mind.

Nimble AppGenie brings this kind of upgrade to life that helps banking apps do more without making things so complicated.

It’s a smart step forward for any app that handles money. So, what are you waiting for? Get in touch with Nimble AppGenie for cutting-edge blockchain banking software development.

Conclusion

Blockchain could become a huge part of how banks and businesses work in the future.

Right now is a great time for financial companies and startups to start looking into how blockchain can help them grow or work better.

For new businesses, blockchain development for startups can open the door to faster, safer, and more affordable ways to run things.

But because it is still a growing technology, it is vital to be careful and use blockchain in the finance industry in the right ways.

FAQs

You can integrate blockchain in a banking app by following the steps below:

- Identify Use Cases

- Develop proof of concept

- Check the blockchain platform and architecture

- Develop smart contracts

- Connect with the existing system

- Pilot, measure, and iterate

- Phased rollout and training

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.