AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

Key Takeaways:

- A stablecoin payment platform lets a business accept, send, and settle payments in stablecoins like USDC or USDT, without anyone touching crypto directly.

- The build has four layers: custody and wallets, compliance, settlement and reconciliation, and API integration.

- The cost to build a stablecoin payment platform for MVP ranges between $30,000–$80,000. An enterprise-grade platform runs $150,000–$200,000 and takes 4–12 months.

- Most teams should not build every layer from scratch. Licensing, custody, and liquidity are usually bought, not built in-house.

- Nimble AppGenie helps fintech teams design and build stablecoin payment platforms without stitching together five separate vendors.

How do you build a stablecoin payment platform? You build a stablecoin payment platform by combining four layers: custody and wallets, compliance, settlement, and API integration, on top of a licensed partner who handles the actual movement of money.

None of the four works alone. Skip compliance and settlement has no legal ground to stand on. Skip custody, and there is no wallet to settle from.

This guide is written for the people who have to actually build this, not trade on it. If you’re a CTO, it walks through the architecture and the tech decisions. If you are a COO or founder, it walks through the budget, timeline, and the build-vs-buy call.

Every figure here is a real range, not a marketing estimate: what an MVP takes to launch, what an enterprise platform takes to run, and what breaks most projects before launch.

What is a Stablecoin Payment Platform?

A stablecoin payment platform is software that allows a business to accept, send, and settle payments using stablecoins instead of card networks or bank wires. It converts fiat to stablecoins and back automatically, so merchants and customers never have to touch crypto directly.

This is different from launching your own stablecoin. Issuing a new token means managing reserves, redemption, and a peg. Building payment infrastructure means using stablecoins that already exist as a settlement rail inside your product.

Why Are Fintech Companies Building Stablecoin Payment Platforms Now?

Stablecoin transaction volume passed $46 trillion in 2025, up from $27.6 trillion the year before, a 106% increase, according to a16z’s State of Crypto report. Monthly stablecoin volumes now exceed Visa and Mastercard combined.

Three problems push fintech teams toward stablecoins:

- Settlement speed: Cross-border transfers clear in seconds instead of 1–3 days through correspondent banks.

- Fees: Stablecoin processing typically runs under 0.5%, against 2–3% for card networks and up to 6% for some SWIFT/SEPA transfers.

- Regulatory clarity: The GENIUS Act, signed into US law in July 2025, sets the first federal rules for who can issue payment stablecoins and how reserves must be held. That clarity is why banks that avoided crypto for a decade are now building with it.

The common use cases: cross-border B2B settlement, marketplace and gig-worker payouts, payroll for distributed teams, and merchant checkout for global customers.

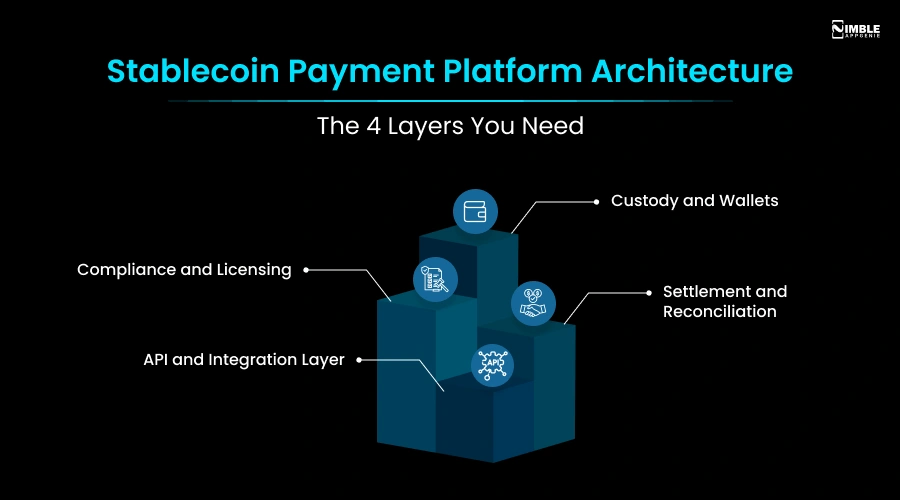

Stablecoin Payment Platform Architecture: The 4 Layers You Need

A stablecoin payment platform is built on four layers: custody and wallets, compliance and licensing, settlement and reconciliation, and API integration. Each layer is its own failure domain; keep the seams between them clean so any one layer can be swapped later.

► Custody and Wallets

This is where private keys live. Most platforms use Multi-Party Computation (MPC) or multi-signature setups instead of a single key, so no one compromised credential can move funds. This layer also handles wallet creation, key recovery, and transaction signing.

► Compliance and Licensing

Every user needs KYC/KYB checks. Every qualifying transfer needs Travel Rule data — the sender and receiver details passed to the counterparty institution. You also need to know whether you’re operating under your own money transmitter license or through a licensed partner bank.

► Settlement and Reconciliation

On-chain settlement moves stablecoins wallet to wallet with blockchain finality. An off-chain ledger nets positions internally first, for speed and near-zero cost, before anything touches the chain. Reconciliation then matches every transaction against your books- unglamorous, but it’s what your auditors will ask for first.

► API and Integration Layer

This is the only layer your customers ever see: APIs and SDKs for wallet management, send or receive, on-ramp and off-ramp, webhooks for payment status, and an orchestration layer that decides which rail a payment takes.

Features of Stablecoin Payment Platform Development

| Feature | Description |

| Multi-Stablecoin Support | Supports popular stablecoins such as USDT, USDC, DAI, and PYUSD, allowing users to choose their preferred digital asset for payments. |

| Multi-Currency Wallet | Enables users to store, send, receive, and manage multiple stablecoins from a single secure wallet. |

| Instant Cross-Border Payments | Facilitates fast international transactions with lower fees compared to traditional banking systems. |

| Secure Payment Gateway | Processes stablecoin payments securely using blockchain technology, ensuring transparency and tamper-proof transactions. |

| QR Code Payments | Allows users to make and receive payments by scanning QR codes for faster and contactless transactions. |

| Real-Time Transaction Tracking | Provides live updates on payment status, confirmations, transaction history, and blockchain records. |

| Fiat-to-Stablecoin On/Off Ramp | Lets users buy stablecoins with fiat currency and convert stablecoins back into local currency through integrated payment providers. |

| Merchant Payment Dashboard | Gives businesses access to payment analytics, transaction history, settlement reports, and customer payment management tools. |

| Recurring Payments | Supports automated subscription billing, scheduled transfers, and recurring merchant payments using stablecoins. |

| Smart Contract Automation | Uses smart contracts to automate payment settlements, escrow services, refunds, and other transaction workflows. |

| Notifications and Alerts | Sends instant notifications for successful payments, failed transactions, wallet activity, and security events. |

| Transaction Reports and Analytics | Generates detailed financial reports, payment insights, and performance analytics for businesses and administrators. |

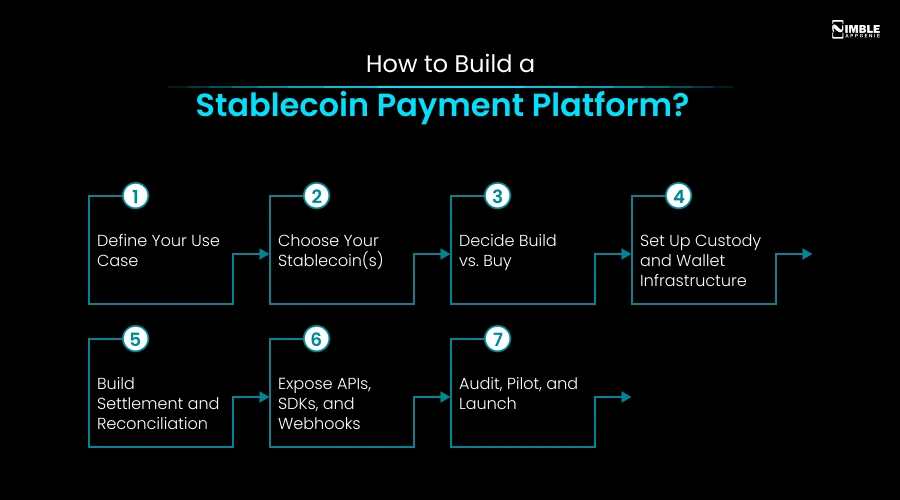

How to Build a Stablecoin Payment Platform?

Building a stablecoin payment platform takes seven steps: define the use case, choose your stablecoins, decide build vs. buy, set up custody, build settlement and reconciliation, expose APIs and SDKs, then audit, pilot, and launch.

When you develop a stablecoin payment platform, you should consider the steps we follow.

1. Define Your Use Case

Every stablecoin payment platform starts with one use case, not five. Cross-border B2B settlement, payroll for distributed teams, marketplace payouts, and merchant checkout each need different architecture, different compliance scope, and different stablecoin liquidity.

Picking one narrows your licensing requirements, your integration partners, and your first target market. Teams that try to serve every use case at once usually delay launch by months and dilute the compliance work any single flow needs. Start narrow, ship it, then expand into adjacent use cases once the first one is stable and fully compliant.

2. Choose Your Stablecoin(s)

USDC, USDT, and PYUSD are not interchangeable. USDC offers monthly reserve attestations and regulator-friendly transparency, which suits US-facing fintech products. USDT carries the deepest global liquidity, useful for emerging-market payouts and remittance corridors.

PYUSD fits products already built on PayPal or Venmo rails. Most enterprise platforms end up supporting more than one stablecoin, since counterparties rarely standardise on a single token. Decide this early: your custody and settlement layers need multi-stablecoin logic from day one, not as a later retrofit.

3. Decide Build vs. Buy

Before writing any code, map each of the four layers- custody, compliance, settlement, and API- against build or buy. Licensing, custody, and liquidity take years and real capital to build in-house, so most teams buy or partner for these.

The API and orchestration layer is usually where a platform actually differentiates, so build that one yourself. Getting this decision wrong early is the single biggest cause of blown budgets and missed launch dates in stablecoin payment projects, more so than any technical mistake.

4. Set Up Custody and Wallet Infrastructure

Custody holds the private keys controlling every stablecoin your platform touches. Most platforms use Multi-Party Computation (MPC) or multi-signature wallets instead of a single key, so no one compromised credential can move funds.

You can partner with an MPC wallet-as-a-service provider to launch in weeks, or build your own with hardware security modules if wallet security is your actual product. This layer also handles wallet creation, key recovery, and transaction signing, and it must be live before any settlement logic can work.

5. Build Settlement and Reconciliation

On-chain settlement moves stablecoins wallet to wallet with blockchain finality. An off-chain ledger nets positions internally first, for speed and near-zero cost, before anything touches the chain.

Reconciliation then matches every transaction against your internal books and produces the audit trail your compliance team and auditors will ask for.

This is the least visible layer to customers and the most important to get right; errors here surface as missing funds, duplicate payouts, or failed audits months after launch.

6. Expose APIs, SDKs, and Webhooks

This is the only layer your customers and partners interact with directly. Build APIs for wallet management, send and receive, on-ramp and off-ramp, plus webhooks that report payment status in real time.

An orchestration layer sits on top, deciding which rail, stablecoin, or chain a given payment should use. Clean, documented APIs here are what let a partner offer stablecoin payments to their own customers without touching any of the infrastructure sitting underneath.

7. Audit, Pilot, and Launch

Smart contracts and infrastructure need a third-party security audit before real funds touch the system, no exceptions. Launch in one market or with one use case first, watch transaction volume and failure rates closely, then expand.

Skipping the audit to save time is the fastest way to lose customer funds and trust in a single incident. A staged rollout also gives your compliance and support teams room to catch problems before they scale into something much bigger.

Build vs Buy: Should You Build Your Own Stablecoin Rails?

Most dedicated development teams should not build every layer. Licensing, custody, and liquidity take years and real capital to build in-house. Build the layers that are your actual product, checkout experience, orchestration logic, customer-facing features. Buy or partner for the layers that are regulated infrastructure, not your competitive edge.

| Layer | Build In-House If | Buy / Partner If |

| Custody & wallets | Wallet security is your core product | You want to launch in months, not years |

| Licensing & compliance | You already hold a money transmitter license | You’re new to regulated payments |

| Settlement & reconciliation | You need custom logic for a niche use case | Standard rails cover your volume and geography |

| APIs & orchestration | Almost always, this is where you differentiate | Rarely; keep this layer in-house |

How Much Does It Cost to Develop a Stablecoin Payment Platform?

The cost to build a stablecoin payment platform ranges between $30,000-$200,000, depending on the platform’s features, supported blockchain networks, security requirements, compliance needs, and third-party integrations.

The table below shows the estimated stablecoin payment platform development cost.

| Tier | What’s Included | Price Range | Timeline |

| MVP | Single stablecoin, one chain, basic KYC, hosted checkout | $30,000–$80,000 | 6–10 Weeks |

| Mid-market | Multi-currency support, white-label option, standard compliance stack | $80,000–$150,000 | 2–4 Months |

| Enterprise | Multi-chain, embedded wallets, in-house settlement engine, ERP integration | $150,000–$200,000+ | 4–12 Months+ |

If you are launching a new payment product, it is best to start with an MVP that helps validate the business idea while keeping costs under control. As your transaction volume grows, you can expand the platform with features.

Working with an experienced DeFi app development company also helps reduce development risks and ensures the platform meets security and regulatory requirements from the beginning.

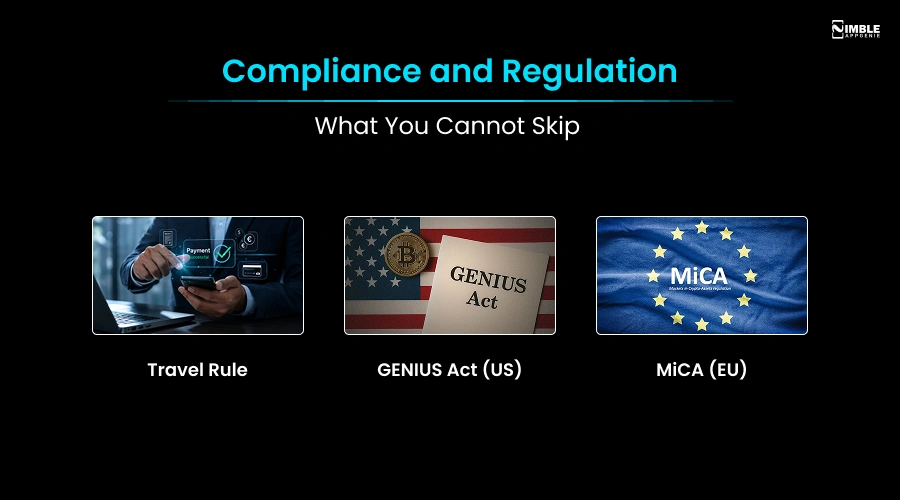

Compliance and Regulation: What You Cannot Skip

Three things matter most: KYC/KYB on every user, Travel Rule reporting on qualifying transfers, and knowing exactly which license or bank partner legally covers your money movement.

♦ Travel Rule

For every qualifying transfer, you collect originator and beneficiary details, pass them to the counterparty institution over a secure channel, and keep an audit trail. Close to 100 jurisdictions now enforce some version of this, build it in from day one.

♦ GENIUS Act (US)

Signed into law in July 2025, it is the first federal framework for payment stablecoins. It sets rules for who can issue a stablecoin, how reserves must be backed, and which regulator oversees which issuer. Most provisions phase in over 18 months, with rulemaking still ongoing through 2026.

♦ MiCA (EU)

Whether your platform is MiCA compliant depends on your specific model. MiCA sets reserve, safeguarding, transparency, and governance rules, and your exact duties differ depending on whether you issue a token or just move someone else’s.

Get legal input tied to your specific business model before you launch. Compliance requirements differ by jurisdiction, by whether you touch issuance or only payments, and by transaction size.

Which Stablecoin Should You Support: USDC vs USDT vs PYUSD?

USDC is the more regulator-friendly option, with monthly reserve attestations from Circle. USDT has the deepest liquidity and widest use worldwide. PYUSD makes the most sense if you already run on PayPal or Venmo rails.

| Stablecoin | Issuer | Best For |

| USDC | Circle | Regulated fintechs, US enterprise, teams that need transparent monthly attestations. |

| USDT | Tether | Global reach, highest liquidity, emerging-market remittance and payouts. |

| PYUSD | PayPal / Paxos | Products already integrated with PayPal or Venmo. |

Most enterprise platforms end up supporting more than one stablecoin, since customers and counterparties do not all standardize on the same token.

You can build the orchestration layer to be stablecoin-agnostic from the start, so adding a second or third one later does not mean a rebuild.

Challenges and Solutions in Building a Stablecoin Payment Platform

Most stablecoin payment projects fail for the same handful of reasons. Here is each challenge next to the fix, so you can check your own build plan against it.

| Challenge | Solution |

| Compliance gets treated as a phase-two task | Build KYC/KYB, sanctions screening, and Travel Rule reporting into the architecture from day one, not after the MVP ships. |

| Locking into one stablecoin and one chain | Design the orchestration layer to be stablecoin- and chain-agnostic from the start, so adding USDC, USDT, or a new chain later doesn’t require a rebuild. |

| Reconciliation and support workload gets underestimated | Staff and tools for failed payments, disputes, and refunds before launch, not after the first incident forces the issue. |

| On/off-ramps get confused with full payment infrastructure | Know the difference early: a ramp converts fiat to crypto for one user; a payment platform moves money between two unrelated parties, a more regulated, more complex job. |

| Smart contract and infrastructure audits get skipped to save time | Budget for a third-party audit before real funds touch the system; treat this as non-negotiable, not optional. |

| Legacy system integration gets underscoped | Set aside $30,000–$100,000 and an extra timeline for connecting stablecoin rails to systems like SAP, Oracle, or Dynamics; this is usually harder than the blockchain part. |

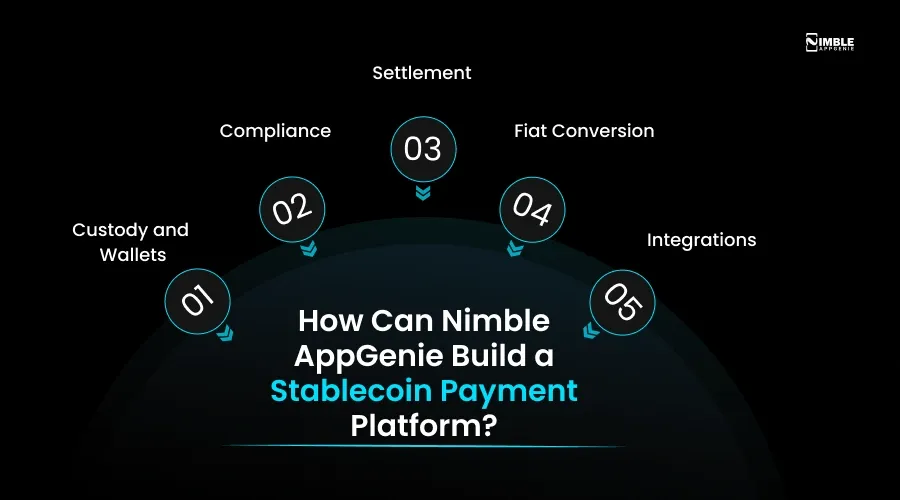

How Can Nimble AppGenie Build a Stablecoin Payment Platform?

Nimble AppGenie builds a stablecoin payment platform across all four layers- custody, compliance, settlement, and API integration– as one system, not five vendors stitched together.

➤ Custody and Wallets

MPC-based wallet infrastructure with multi-chain support (Ethereum, Solana, and others), built on ISO 20022 messaging with end-to-end encryption.

➤ Compliance

KYC/KYB, AML screening, and Travel Rule reporting built into the platform from day one, not bolted on before launch.

➤ Settlement

On-chain and off-chain settlement logic, reconciliation, and audit trails, plus DeFi features like stablecoin yield or tokenized assets when a product needs them.

➤ Fiat Conversion

On-ramp and off-ramp connections through Stripe, BVNK, Coinbase Commerce, and BitPay, supporting USDC, USDT, Bitcoin, Ethereum, and Binance Pay, with a white-label checkout option.

➤ Integrations

25+ payment, KYC, and card APIs (Stripe, PayPal, Adyen, Razorpay, and others), plus Circle’s API for USDC issuance and redemption.

We are ISO 9001:2015 certified, have delivered 350+ projects, and have built 20+ DeFi apps and 10+ crypto on-ramp/off-ramp solutions to date. If you are deciding between building from scratch and working with a development partner, that’s the conversation to have.

Conclusion

A stablecoin payment platform is not a single product you buy off a shelf, and it’s not something you need to build entirely from scratch either. It’s four layers, and the right call is usually to build the layer that’s your product and partner for the layers that are regulated infrastructure.

If you are evaluating this for your fintech product, start with the use case, get the compliance conversation done early, and bring in a development partner who has actually shipped this stack before.

Consult with a company that has built fintech, DeFi, and crypto on-ramp products for worldwide clients. Get in touch to scope your stablecoin payment platform.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.