AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

TL;DR

- AI claim management software development typically costs between $60,000 and $450,000 in 2026, more than a traditional build, but the AI layer (fraud detection, document automation, predictive routing) is what drives most of the ROI.

- A traditional claims management system automates workflow; an AI-driven one also reads documents, flags fraud, and settles simple claims with little to no human involvement.

- Insurers using AI-powered claims automation report processing time drops of up to 40–50%, with well-documented cases (like Aviva) saving tens of millions annually.

- Build vs. buy still applies, but with AI in the mix, the deciding factor is often whether an off-the-shelf platform’s AI models were trained on data relevant to your lines of business.

- Nimble AppGenie builds custom AI claims management software for insurers who need a system that matches their business, not a generic AI layer bolted onto a template.

If you are evaluating AI claims management software development for your insurance business, you already know what’s at stake. Slow claims processing costs you, customers. Picking the wrong build strategy costs you a year and a six-figure budget.

This guide breaks down what an AI-driven claims system actually costs in 2026, how it differs from a traditional build, which AI features are worth paying for, and how to decide whether it’s worth it for your team.

Whether you’re an insurer modernizing legacy systems, an MGA scaling operations, or an insurtech founder scoping your first build, here’s what to know before you talk to a development partner.

What Is AI Claims Management Software?

AI claims management software is a claims management system with machine learning and AI models built into the core workflow, not appended afterward. Instead of only routing a claim through digital steps, it actively reads submitted documents, flags likely fraud, cross-checks claim details against historical data, and can fully settle simple, low-risk claims without a human touching the file.

A traditional claim management tool digitizes the paperwork. An AI-driven one also makes judgment calls on the routine cases, freeing adjusters to spend their time on the complex ones. That’s the real shift AI claim management software development represents: less “digitizing the process,” more “automating the decisions inside it.”

In 2026, that increasingly means AI doing the heavy lifting: reading documents, flagging fraud, and settling simple claims without a human touching them at all.

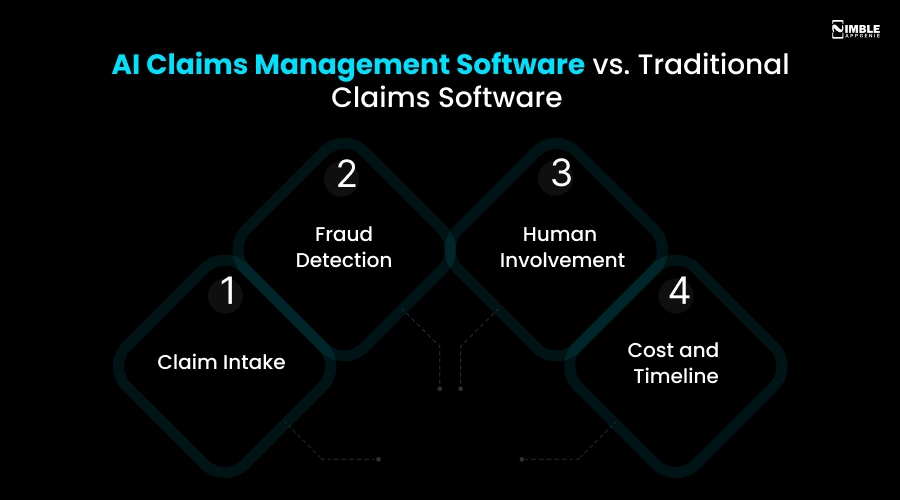

AI Claims Management Software vs. Traditional Claims Software

This is the difference most guides skip, and it’s the one that actually determines your budget and timeline.

- Claim Intake: Traditional systems capture structured form data. AI systems can also ingest PDFs, photos, and free-text descriptions and extract structured data from them automatically.

- Fraud Detection: Traditional systems flag claims based on static rules (e.g., claim amount above a threshold). AI systems detect behavioral and network patterns that a rules engine would never catch.

- Human Involvement: Traditional systems still route nearly every claim to an adjuster. AI systems can completely resolve a meaningful share of low-risk claims with no human step at all.

- Cost and Timeline: AI systems cost more upfront and take longer to train and validate, but generally pay that back through lower per-claim handling cost at scale.

If your claim volume is low or your lines of business are highly non-standard, a traditional system may still be the smarter starting point – AI earns its cost back through volume and repeatable patterns.

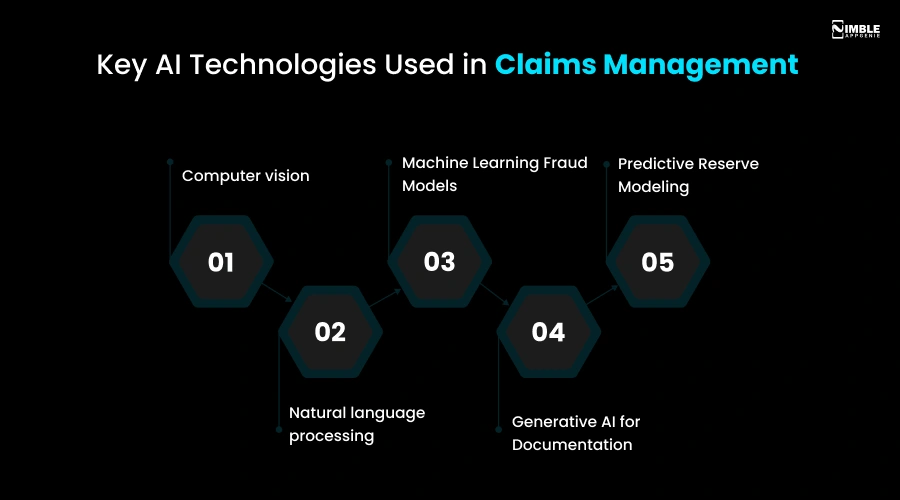

Key AI Technologies Used in Claims Management

- Computer vision: Assesses damage from submitted photos or video for auto and property claims, often the fastest way to speed up FNOL-to-estimate time.

- Natural language processing (NLP): Reads adjuster notes, claim forms, and medical or repair documents and extracts the structured data a claims engine needs. We cover this in more depth in our intelligent document processing guide.

- Machine Learning Fraud Models: Score claims against historical fraud patterns and flag anomalies that a static rules engine would miss.

- Generative AI for Documentation: Drafts claim summaries, denial letters, and correspondence for adjuster review, cutting administrative time.

- Predictive Reserve Modeling: Forecasts likely claim payout early in the lifecycle, improving reserve accuracy.

Whatever you call it, the goal is the same: one connected system instead of ten disconnected ones.

For the fuller picture of how these pieces fit together across an entire insurance operation, not just claims, see our guide on AI-powered insurance automation software development.

Why This Matters Right Now: The Business Case

Claims handling is where insurers either win or lose customer trust. A slow, confusing claims experience is one of the fastest ways to lose a policyholder for good, and it’s expensive to run, too.

- The global claims management market size is expected to grow by $17.09 billion by 2034, up from the $6.54 billion at the end of 2026.

- According to a report by McKinsey & Company, AI-enabled claims management can lower claims-processing time by around 70% and reduce the cost of claims handling by 30%.

- Additionally, Gartner predicts that by 2025, AI will enable insurers to improve customer satisfaction and diminish claims processing times by 30% while diminishing the cost of claims processing by up to 40%.

- 79% of insurance companies say their old systems slow them down.

Simply put: If your claims experience is still manual, you are paying for it twice: once in operational cost, and next, in customer churn.

Is AI in Claims Management Worth It?

For most mid-size and larger insurers, yes, but the outcomes are earned through a real commitment across the claims process, not a single plug-and-play tool.

- According to McKinsey, AI is increasingly used to evaluate claims accuracy in real time by cross-referencing adjuster notes, submitted documents, damage images, and claim histories – cutting into the manual review work that traditionally slows claims down.

- UK insurer Aviva deployed more than 80 AI models across its claims domain, improving claims-sourcing accuracy by 30%, cutting liability assessment time on complex cases by 23 days, and reducing customer complaints by 65%; saving over £60 million ($82 million) in 2024 alone.

- Generative AI is also strengthening fraud detection for property and casualty insurers by surfacing patterns in claims data that manual review tends to miss.

The honest caveat: Results as Aviva’s come from committing to AI across the entire claims domain, not bolting on one point tool, and the payoff compounds over months, not weeks. Smaller claims operations still see real operational benefits, but the scale of savings tends to track with claim volume.

It’s also worth being clear on what AI actually replaces. AI increasingly supports claims decisions rather than making them outright; most carriers keep a human in the loop for final determinations, specifically as regulators push for documented oversight of AI-driven claims decisions.

For an insurer building a claims management system in 2026, AI is not an optional add-on anymore; it’s closer to what cloud deployment was five years ago: the baseline, not the differentiator.

The smarter move is treating it as a phased investment, starting with the areas that create the fastest, most measurable wins, rather than buying into a one-shot “fully AI-powered platform” pitch.

If you are weighing where AI agents specifically fit into that roadmap, our AI insurance agent development guide breaks down real cost ranges by capability level.

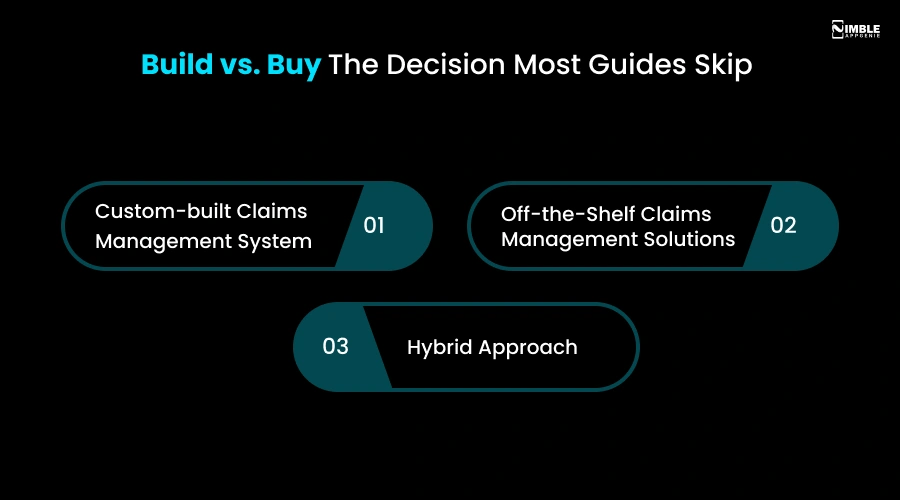

Build vs. Buy: The Decision Most Guides Skip

Most writeups on this topic jump straight to “here’s what a custom build costs.” That’s only half the decision.

Before you spec out AI claims management software, you need to know whether building is even the right call for your situation and size or whether an established claims management company already has an AI-enabled platform close enough to what you need.

- Custom-built Claims Management System: It makes sense once your workflows are complex or specialized enough that a template starts working against you – think niche commercial lines, a business model (like peer-to-peer insurance or usage-based), or multi-region compliance needs that generic claims management systems were not built for.

- Off-the-Shelf Claims Management Solutions: They tend to make sense if you are running standard claim types (homeowners, personal auto, and small commercial), have limited in-house engineering, and need something running fast. This is where many auto claims management software products and other line-specific tools live – check whether their AI models were actually trained on data relevant to your lines of business, not just a generic dataset.

- Hybrid Approach: A proven core plus custom-built AI modules for the parts that actually differentiate your business (reserve modeling, fraud scoring, and a specific claim workflow) is what most growing insurers land on. You are not rebuilding the wheel, just the parts that matter to you.

| If you are unsure which bucket you are in, that’s exactly the kind of conversation worth having with a development partner before you commit a budget. Nimble AppGenie’s insurance app development team can walk through your claim volume and existing systems and tell you honestly whether a custom AI claims management system is worth it for you, not just sell you a build. |

AI Claims Management Software Development Cost in 2026

Cost depends heavily on scope, but here’s a realistic range based on current market data for building AI claims management software or a full AI insurance claims management system.

| Project Type | Estimated Development Cost |

| Basic AI-assisted system

Core claim workflow, single line of business, document automation only |

$60K–$130K |

| Mid-complexity system

Multi-channel intake, AI-driven adjudication, fraud scoring, payment integration |

$130K–$280K |

| Enterprise-grade system

Full AI fraud detection, computer vision, predictive reserve modeling, multi-line, deep integrations |

$280K–$450K+ |

The biggest cost drivers are not the obvious ones. It’s rarely the UI. It’s the integrations (policy admin systems, payment gateways, and CRM), the compliance work (state-by-state regulatory variation, data privacy), and, specific to AI builds, how much model training and validation your fraud and adjudication models need before they are reliable enough to trust with real claims.

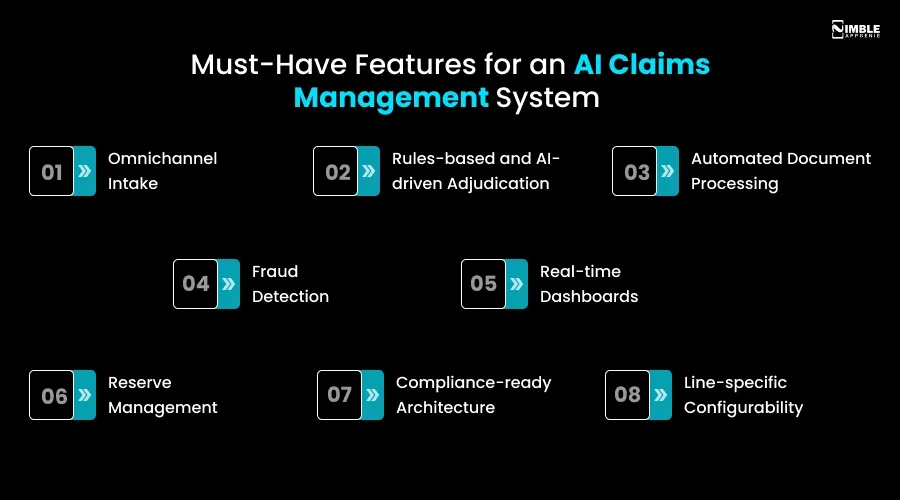

Must-Have Features for an AI Claims Management System in 2026

Below are features you can consider including during AI claims management software development for your business.

- Omnichannel Intake: Claims filed via mobile, web, call center, or agent all land in a structured claims management software.

- Rules-based and AI-driven Adjudication: Routine, low-risk claims settle with little to no human involvement; complex ones get flagged and routed to an adjuster.

- Automated Document Processing: AI reads and verifies submitted documents instead of a human doing it manually.

- Fraud Detection: Pattern recognition that catches suspicious claims early, before payout. If this is a priority for you, we have written a deeper breakdown in our insurance fraud detection software guide.

- Real-time Dashboards: Adjuster workload, cycle time, and settlement trends visible at a glance.

- Reserve Management: Precise, auditable tracking of what is set aside for open claims.

- Compliance-ready Architecture: Built to handle GDPR, CCPA, and regional insurance regulations without a redesign every time a rule changes.

- Line-specific Configurability: Whether you are building a general insurance claims management system or something specialized like auto claims software, the rule engine should flex to your line of business, not force you into someone else’s template.

How the Development Process Actually Works

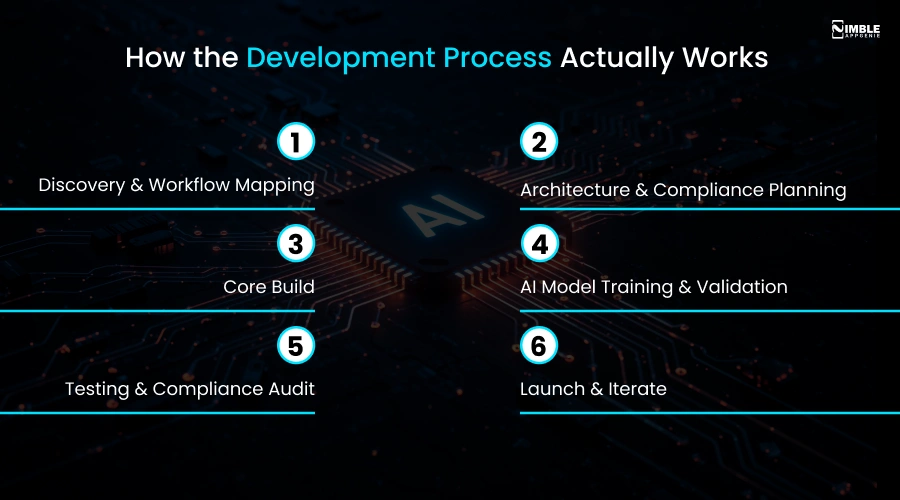

Here’s a step-by-step AI claims management software development process to consider.

1. Discovery & Workflow Mapping

Understanding your pain points, current claim management process, and specifically where an AI model would actually save time versus where rules-based logic is enough.

2. Architecture & Compliance Planning

Deciding the data model, tech stack, and how the AI-enabled claims management system will meet regulatory requirements from day one, not as an afterthought.

3. Core Build

Adjudication, intake, reporting, and payment logic, built and tested in stages, not all at once.

4. AI Model Training & Validation

Document processing, fraud detection, and predictive models trained on relevant historical data and tested against real claim scenarios before going live; this stage is unique to AI builds and is where most of the extra timeline and cost lives.

5. Testing & Compliance Audit

Load testing (claim volume spikes during catastrophic events), security testing, and a compliance review, including bias and accuracy checks on the AI models specifically.

6. Launch & Iterate

Go live, then refine based on policyholder feedback and real adjusters, and retrain models as new claim data comes in.

This is the same approach Nimble AppGenie used in a recent AI-driven claims automation project for a health insurance provider; you can read how that played out in our digital transformation in insurance case study.

Where Nimble AppGenie Fits In for Claims Management Software Development

Nimble AppGenie has spent years building fintech and insurtech products. Our roots are in fintech app development. On the insurance side, that same depth extends into full insurance software solutions, and claims automation sits right at the intersection of both.

We are not a generic development firm bolting “AI features” onto a template. We build AI claims management software around how your team actually works: your claim types, your existing tech stack, and your compliance requirements.

Conclusion

AI claim management software development is not only an IT upgrade, but it’s also the difference between a claims experience that builds customer loyalty and one quietly erodes it through friction.

Whether you build custom, buy an AI-enabled off-the-shelf platform, or opt for a hybrid approach, the goal is the same: faster settlements, fewer errors, and a system your team can actually work with. Get the scoping right upfront, and the rest gets a lot easier.

FAQs

It’s a digital platform that automates the full claims lifecycle, from first notice of loss through document verification, payment, adjudication, and reporting – replacing manual, spreadsheet-driven processes.

Most projects run between $60,000 and $450,000+, depending on complexity. A basic system with document automation only sits at the lower end; an enterprise system with full fraud detection, computer vision, and predictive modeling sits at the top.

At minimum: automated document processing and AI-assisted fraud detection – these two consistently deliver the fastest, most measurable ROI. Computer vision for damage assessment and predictive reserve modeling are worth adding once your claim volume justifies the extra build cost.

Typically 30–50% more than a non-AI build of the same scope, mostly due to the time spent training and validating models against real claims data before they are trusted with production decisions.

It can be, but compliance must be designed in from the start. Most regulators need human oversight on adverse claim decisions, so AI models should support and accelerate adjuster decisions rather than make final determinations autonomously.

It depends on your claim volume and how standard your workflows are. Off-the-shelf claims management solutions work well for standard personal lines with limited engineering resources. A custom-built claims management system makes more sense once your workflows, compliance needs, or business model don’t fit a generic template. Many insurers land on a hybrid: a proven core plus custom modules for what actually differentiates them.

A mid-complexity AI-enabled build typically takes 6–12 months from discovery to launch – longer than a non-AI system, mostly due to the model training and validation stage.

Yes. A well-built claims management system should integrate with your policy administration system, CRM, payment gateways, and third-party data providers like verification and fraud-screening services.

It’s the full journey a claim takes through a claims management system: incident capture, first notice of loss (FNOL), intake and registration, adjudication, payment, and final closure, with reporting happening throughout.

Claims management software is the technology platform itself. Claims management services usually refer to a company or team that handles claims processing on your behalf, sometimes using their own proprietary claims management systems. Many insurers use software in-house rather than outsourcing to a claims management company, specifically to keep full control over data and customer experience.

Modern insurance claims management systems can usually handle multiple lines of business through configurable rules, so you don’t necessarily need a separate auto claims software product, but if auto is your dominant line, a system tuned specifically for that workflow (photo-based damage assessment, telematics data, repair shop integrations) can process claims faster than a generic multi-line platform.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.