Banking Software Development

Banking Software Development Payroll Software Development

Payroll Software Development Our Work Process

Our Work Process Awards

Awards

Key Takeaways:

- A banking license is a legal permit issued by a national regulatory authority allowing organisations to operate like a bank.

- Your neobank needs a banking license because it will give a legal authority to offer banking services, build customer relationships, offer high profit margins, and provide access to payment infrastructure.

- The three licensing paths to be followed to integrate a banking license are a full banking license, an electronic money institution, and banking-as-a-service partnerships.

- You can get a banking license for your neobank app by evaluating different countries’ needs, such as the regulatory requirements of the US, UK, and European Union.

- Partnering with Nimble AppGenie can help you build your dream neobank app with a banking license.

Yes, a banking license for your neobank is not a compulsion, but it is a way you can avoid dependency on banks and help users to deposit funds, and have all banking services without including a bank in it.

If you are a fintech startup, or an entrepreneur with a neobank, or are thinking of entering this growing industry, learning about how to get a license will help you to set a scope for what you want your neobank app to be.

Here, in this guide, we’ll walk you through “how to get a banking license for your neobank?” and provide information about different regions to get your banking license on board.

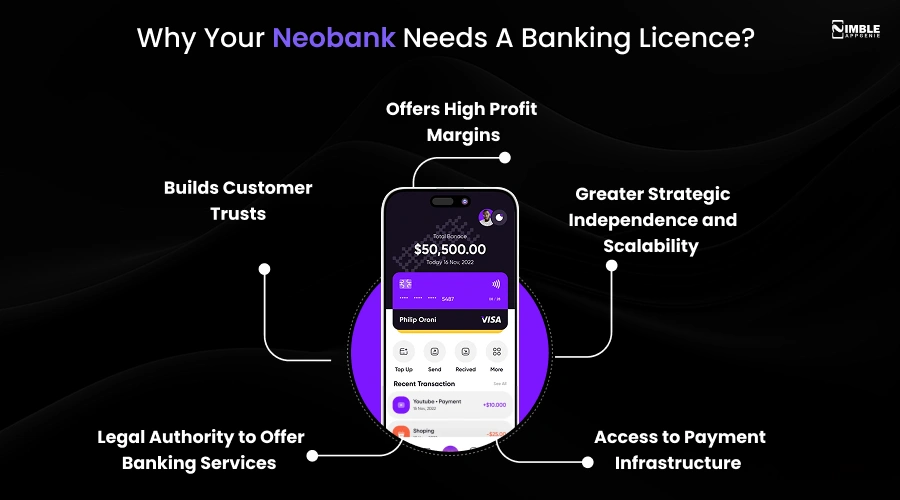

Why Your Neobank Needs A Banking Licence?

A neobank needs a banking license to become an independent financial institution. Without a license, a neobank is a software platform that depends on a traditional “partner bank” to hold customer deposits, manage the regulatory compliance, and even to process transactions.

Therefore, a license grants total control to the neobank to have key operational benefits:

1. Legal Authority to Offer Banking Services

With a licence, your neobank will have a legal authority to deposit funds, lend credit, and offer all banking services.

However, without a license, your neobank will rely on banks to deposit funds and will operate like a third-party fintech app connected to banks.

2. Builds Customer Trusts

A licensed neobank is subject to regulatory oversight, which reassures customers that their money is being handled safely and responsibly. This can significantly improve customer confidence and brand loyalty.

However, without a license, neobank apps cannot ensure that customers will put their surplus funds with them. This can even create trust issues among the users.

3. Offers High Profit Margins

A licensed neobank can offer high profit margins by generating revenue from lending, interest income, and other regulated banking activities. This creates more diversified and sustainable income streams compared to relying solely on partnerships.

A neobank without a license cannot offer high profit margins to you, and you will depend on the traditional banks for a source of income.

4. Greater Strategic Independence and Scalability

A banking license for your neobank transforms a company from a dependent financial facilitator into a fully recognized financial institution. Through a banking license, you offer strategic independence by eliminating reliance on the partner banks.

Without a banking license, you cannot eliminate intermediaries, cannot have direct network access, and cannot scale your banking operations.

5. Access to Payment Infrastructure

A banking license grants direct, authorized access to a country’s core payment networks and central bank clearing systems.

Without a banking license, your neobank needs to partner with a traditional, licensed financial institution and a specialized banking-as-a-service (BaaS) provider.

Now, if you’re still wondering about “Should You Get A License Or Partner With A Bank?”

Then, the answer depends on what you are looking for: are you looking to be an independent entity that has a license to act as a bank, or do you want to depend on a bank to be a third-party app?

Well, if you want to build a neobank app, it is quite important to get a banking license through a valid license path.

Now, let’s get ahead with the three licensing paths in the following section.

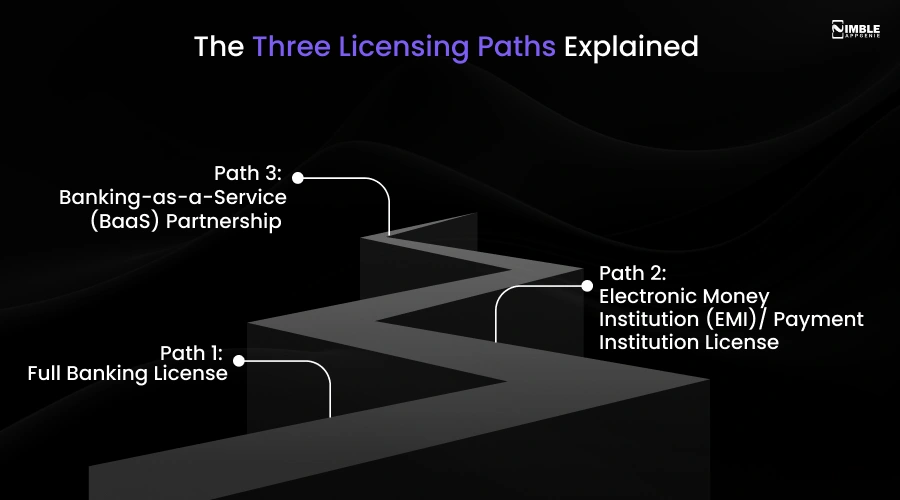

The Three Licensing Paths Explained

There are three licensing options and paths that you can choose:

Path 1: Full Banking License

The full banking license is a type of license that lets you accept deposits, lend money, and offer a complete range of banking services. This is a path that promotes an institution to offer a comprehensive, unrestricted suite of retail and corporate financial services to the general public.

Here, the capital requirements are high, that is typically EUR 5 million to EUR 25 million in Europe, more in the US and Singapore.

This application takes 12 to 36 months, and you are supervised as a bank with full reporting, liquidity ratios, and stress testing.

Path 2: Electronic Money Institution (EMI)/ Payment Institution License

This path of licence helps you to issue electronic money, provide payment services, and issue payment cards; however, you cannot accept deposits in the banking sense or lend from the customer funds.

A payment institution license permits the processing of transactions, but it restricts the entity from storing customer funds over time.

Here, the capital requirements are much lower, at EUR 350,000 in the EU/UK. Here, the timeline runs from 6 to 18 months.

Path 3: Banking-as-a-Service (BaaS) Partnership

It is the contractual and regulatory framework where a licensed financial institution allows non-bank businesses to offer banking products and services. The licensed bank handles the regulations, while the partner manages the customer experience.

This licensing partnership allows companies to legally deploy financial services by “borrowing” the bank’s charter and regulatory compliance umbrella.

The majority of US neobanks (Chime, Current, and dozens of others) don’t hold their own bank charters; they partner with chartered banks that provide FDIC-insured deposit accounts, debit card issuance, and ACH access, while the neobank provides the customer-facing app and experience.

Apart from these three paths of licenses, there is one more license available as the fourth intermediate option, but restricted in regions such as Singapore and the UK. This offers more capability than EMI, less than a full bank, often with an upgrade pathway.

Well, you can get a license for your Neobank via these pathways; however, based on the country, these pathways differ. Let’s get ahead with learning how to get a banking license for your Neobank in the following section.

Bonus Read: Neobank Vs Digital Banks

How to Get a Banking License for Your Neobank: Country-By-Country Classification

Licensing is not just choosing the path; it’s about navigating the particular regulator, capital threshold, and the timeline of the country you are launching in.

Even with these three licensing paths, such as partnering with a sponsor bank, obtaining an electronic money institution license, and acquiring a complete banking charter, you need to evaluate which path is suitable and required for which country.

Here is the country-by-country classification:

1. United States (US)

- Regulator(S): In the United States, the neobanks are not directly regulated by the federal banking agencies; they are regulated via sponsor banks and are increasingly overseen by consumer protection agencies.

- License Paths: Different paths adopted are specialized registrations, sponsor bank or backend-as-a-service partnership model, and deposit insurance approval.

- Capital Requirements: The overall capital requirements for a banking licence are $15 million to $30 million+ in the initial capitalization and liquid reserves.

- Timeline: 18–36 months for a full charter; 2–6 months for BaaS launch.

- 2026 Note: Obtaining a banking license in the United States is highly rigorous; instead of building it from scratch, most of the fintechs initially bypass licensing via banking-as-a-service (BaaS) platforms to partner with the sponsor banks.

2. United Kingdom

- Regulator(S): To launch a fully licensed neobank in the United Kingdom, you must secure authorization from the two primary bodies, including the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) for full banks.

- License Paths: Full UK banking license, electronic money institution (EMI) authorization, and mobilisation, with limits while the bank builds out operations.

- Capital Requirements: Here, the initial minimum capital requirement is £5 million for a banking license, which is referred to as the initial capital requirement or ICR.

- Timeline: The overall timeline is almost 6 to 24 months. Where 6-12 months for EMI; 12-24 months for full bank authorization.

- 2026 Note: The UK’s mobilisation regime remains one of the most founder-friendly full-license pathways globally, which lets a neobank operate with restrictions while completing final regulatory requirements.

3. European Union

- Regulator(S): Neobanks in the European Union are primarily regulated by two critical layers of authority, including supranational European regulators and national-level authorities.

- License Paths: The license paths that you can obtain are an electronic money institution (EMI) license, a full banking license, and banking-as-a-service (BaaS).

- Capital Requirements: EUR 5 million to 25 million for a full bank, EUR 350,000 for EMI.

- Timeline: 12–24 months for full bank; 6–12 months for EMI

- 2026 Note: Launching a neobank in the European Union requires making key regulatory, technological, and compliance decisions.

4. United Arab Emirates (UAE)

- Regulator(s): The primary regulator for launching a consumer-facing neobank app in the UAE is the Central Bank of the United Arab Emirates.

- License Paths: Neobanks in the UAE do follow three distinct licensing paths, including direct full banking licences, payment and e-money licenses, and sponsorship models.

- Capital Requirements: Here, the minimum paid-up capital typically ranges from AED 15 million to AED 50 million+.

- Timeline: 9–18 months, depending on license type and free zone vs. mainland UAE application

- 2026 Note: To launch a neobank in the UAE, operators generally choose between pursuing a full banking license or operating as a stored-value facility.

5. Australia

- Regulator(s): The regulatory authority of the banking licence for your Neobank in Australia is the Australian Prudential Regulation Authority (APRA) and the Australian Securities and Investments Commission (ASIC).

- License Paths: The two main regulatory bodies comprise the Australian Prudential Regulation Authority (APRA) and the Australian Securities and Investment Commission (ASIC).

- Capital requirement: Minimum AUD 3 million paid-up capital for a Restricted ADI, rising substantially for a full ADI license

- Timeline: 12–24 months for full ADI; 6–12 months for Restricted ADI.

- 2026 Note: The licensing pathway obtained by the Australian government is a restricted ADI pathway that was introduced specifically to help Neobanks to enter the market, which remains a useful staged model for founders not ready for full ADI capital requirements.

Here is the summarized comparison table stating how to get a banking license for your Neobank:

| Country | Regulator | Fastest Path | Capital (Fastest Path) | Timeline (Fastest Path) | Full License Capital |

| USA | OCC, Fed, FDIC | BaaS Partnership | Program fees only | 2–6 months | $15M–$30M+ |

| UK | FCA, PRA | EMI Authorization | ~£300,000 | 6–12 months | Higher (full bank) |

| EU | ECB, National Authorities | EMI/PSD2 License | EUR 350,000 | 6–12 months | EUR 5M–25M |

| UAE | CBUAE, DIFC, ADGM | SVF / Free Zone License | Varies (lower than full) | 9–18 months | Higher (CBUAE full) |

| Singapore | MAS | Major Payment Institution | Lower than DFB | 6–12 months | SGD 15M rising to 1.5B |

| Australia | APRA, ASIC | Restricted ADI | AUD 3M | 6–12 months | Substantially higher |

Fintech and neobank startups often ask, “How much does it cost to get a banking license for a neobank?”

Well, getting a banking licence for a neobank depends on the region and country. However, this can range from $50,000 to $30 million+.

For the companies that have faced and gone through a challenge to get a banking license, this is how they met their requirements with Nimble AppGenie.

Pain Points And How Nimble AppGenie Solves Them

Here is the list of the pain points that we have come across, and this is how our team has solved them:

“We don’t know if our product idea even needs a banking license or if BaaS is sufficient.”

This is one of the most common issue that most of the founders faces, and getting the license path wrong can waste months, and even a lot of resources.

The team of Nimble AppGenie has helped in delivering the product’s specific feature set against the regulatory paths available in the target market.

We have helped them to discover the license paths, which helped the company’s legal advisors to make valid decisions with full technical context.

“With the changing regulatory landscape, our neobank app was unable to scale accordingly”

As the leading fintech software development company, our experts know that with the changing regulatory landscape, you need a scalable neobank platform.

With the tightening regulatory landscape, including the FDIC, OCC, and the Federal Reserve, the banking license needs to be built for compliance flexibility, not a single static regulatory snapshot.

We have architected the neobank platforms with modular security layers, including two-layer encryption, KYC, and AML compliance.

“We want to add crypto/stablecoin features, but don’t understand how MiCA affects our neobank”

Our team came across a company that is looking forward to adding crypto/stablecoin features to their neobank. They bothered about MiCA impacts.

Enabling an additional feature of crypto/stablecoin requires compliance with MiCA’s full authorization deadline. We are the leading crypto wallet development service provider, who knows how to comply with the MiCA regulations.

Team Nimble AppGenie has deep experience building MiCA-aware DeFi and crypto features that integrate cleanly alongside traditional neobank functionality.

Nimble AppGenie: Your Ultimate Partner To Build A Neobank App

Nimble AppGenie is the best neobank development company, which knows how to comply with the regulations and practices related to fintech. Our team can help you to provide end-to-end solutions from building the app to helping you to get a banking licence.

Here’s why you should choose us:

1. Proven Track Record

Nimble AppGenie has already served 350+ fintech solutions, which means we have a proven track record and have a niche in the fintech software industry. We are experts in creating fintech apps across the globe.

2. Offer End-to-End Support

Our company does offer end-to-end support for creating a neobank app through managing the entire lifecycle from initial ideation and compliance to UI/UX design, testing, and post-launch support.

3. Compliance and Security

We do follow a compliance and security landscape, integrating strict frameworks, multi-currency wallets, and AI-powered financial insights for maintaining the rigid backend infrastructure.

4. Specialization in Fintech Services

Nimble AppGenie does offer effective fintech services such as building eWallets, creating cryptowallets, and neobanks as per the tailored requirements of the clients.

Conclusion

Neobanks should get a banking license because it will help them to have legal authority to offer banking services, build customer trust, offer high profit margins, provide greater strategic independence, and provide access to payment infrastructure.

Here, three licensing paths that you can follow are a full banking license, an electronic money institution license, and a banking-as-a-service partnership license.

To get a banking license for a neobank app, you need to evaluate the rules and regulations that are offered by different countries, including the United States, the United Kingdom, the European Union, Australia, and the United Arab Emirates. Connecting with the right team of developers, you can build your engaging neobank.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.