AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

TL;DR

- Offshore fintech development can cut costs by 60–70%, with developers charging $20–$50/hr vs $100–$175/hr onshore.

- Onshore is best for highly regulated fintech projects requiring local legal compliance, real-time collaboration, and high security control.

- Offshore carries real risks: time zone gaps, communication overhead, and compliance gaps – all manageable with the right partner.

- A hybrid model (onshore strategy + offshore execution) is now the preferred approach for growth-stage fintechs in 2026.

- The real question is not just cost – it’s: which model helps you build faster, safer, and smarter?

- Nimble AppGenie offers fintech startups and scaleups an offshore-first, compliance-ready development approach – ISO-certified, PCI-compliant, and proven across 50+ fintech products worldwide.

Just imagine: You have a fantastic fintech idea. Maybe it’s a payment gateway, an investment app, or a lending platform. You are sure what you want to build. But next comes the big question – where and how do you build it?

Do you partner with a local mobile app development company (onshore) for seamless communication and compliance alignment? Or do you hire a talented offshore team in Eastern Europe, India, or Southeast Asia and potentially save 60% of your development budget?

Offshore vs onshore fintech development is one of the most crucial decisions a company can make. Get it wrong, and you will witness compliance violations, missed deadlines, or ballooning costs. Get it right, and you build faster, launch faster, and scale globally.

In this guide, we will break down everything – hidden risks, real costs, decision frameworks, and compliance factors – so you can confidently choose the model (offshore or onshore) that fits your fintech.

What Is Offshore Fintech Development? (And What It’s NOT)

Offshore fintech development means hiring a software development company or team located in a different country, usually fintech software development outsourcing, where developer salaries can notably be lower than in the US, UK, or Australia.

Top offshore destinations for fintech include:

- Eastern Europe (Romania, Ukraine, Poland) – Excellent for enterprise fintech and compliance-heavy projects

- India – Larger developer pool, robust AI/ML talent, and deep fintech expertise

- Southeast Asia (Philippines, Vietnam) – Expanding fintech hubs with competitive rates

- Latin America (for US companies) – Nearshore option with overlapping time zones

But here’s what offshore is NOT:

- It’s not only ‘cheap labor.’ Today’s offshore developers build for Fortune 500 companies and VC-backed fintechs. Not sure what building a fintech app actually involves? Read our complete guide on how to build a fintech app.

- It’s not one-size-fits-all. The right offshore approach relies on your product, stage, and compliance needs.

- It’s not always high-risk. With the right mobile app development company, offshore can be as compliant and secure as onshore.

| Quick Stat: Offshore development can reduce development costs by up to 60%, according to Verified Market Research. |

What Is Onshore Fintech Development?

Onshore development means working with a team in the same country as your business. If you are a US fintech startup, onshore means US-based developers.

The main benefits of choosing onshore fintech development are clear:

- Same time zone: Faster feedback loops and real-time collaboration

- Same legal framework: Easier IP protection, regulatory alignment, and data compliance

- Direct oversight: See progress in real time and meet in person

- Cultural alignment: Communication styles and shared business norms

Onshore fintech development disadvantages are:

- Hiring takes 3 to 6 months in competitive tech markets

- Onshore developers in the US charge about $100-$175/hour on average

- Limited specialized fintech talent in some local markets

- Challenging to scale quickly without significant cost increases

| Real-World Fact: A European fintech that developed a complex financial compliance system onshore achieved full legal control and faster iteration, but paid 3x as much as comparable offshore builds. The lesson? Onshore works, but the cost premium should be justified by project complexity and compliance requirements. |

The Real Cost Comparison: Offshore vs Onshore Fintech Development

Let’s talk numbers because this is where most fintech founders make assumptions that cost them money.

Developer Hourly Rates in 2026

| Factor | Offshore | Onshore | Hybrid |

| Hourly Cost | $20–$50/hr | $100–$175/hr | $40–$90/hr |

| Cost Savings | Up to 60–70% | Baseline | 30–50% savings |

| Time Zone | 8–12 hrs gap | Same time zone | Manageable overlap |

| Compliance | Needs extra vetting | Best for regulated apps | Balanced |

| Talent Pool | Global & vast | Local, competitive hiring | Best of both |

| Communication | Async-heavy | Real-time, seamless | Structured async+sync |

| Data Security | Needs a strong NDA | Easier legal control | Custom protocols |

| Best For | Well-scoped projects | Regulated, complex builds | Growth-stage fintechs |

What Does a Full Fintech Development Project Cost?

Let’s say you are building a mid-complexity fintech app (user auth, payment processing, compliance module, and dashboard).

To understand the full onshore and offshore fintech development cost, you need to look beyond hourly rates and factor in the complete project scope.

| Cost Element | Offshore (India) | Onshore (USA) |

| Dev Team (6 months) | $30,000–$60,000 | $120,000–$200,000 |

| Project Management | $5,000–$10,000 | $20,000–$40,000 |

| QA & Testing | $5,000–$8,000 | $15,000–$25,000 |

| Compliance Setup | $3,000–$6,000 | $8,000–$15,000 |

| Total Estimate | $43,000–$84,000 | $163,000–$280,000 |

For a detailed breakdown by app type and feature set, see our guide on fintech app development cost.

The Hidden Costs Nobody Talks About

Before you get attracted to offshore savings, be aware of the hidden costs:

- Management Layer: You will need a robust project manager or technical lead to bridge gaps.

- Communication Overhead: Expect 20-30% extra time for revisions, async reviews, and miscommunications.

- Time Zone Delays: A question that takes 5 minutes onshore can take around 24 hours offshore.

- Rework Cycles: Requirements misunderstood early lead to expensive rework later.

The smart move? Budget an extra 30-40% buffer on offshore engagements for QA and management. Even with that, offshore can still deliver strategic savings and scalability advantages over onshore.

Offshore Fintech Development Risks – And How to Beat Them

The fintech industry is one of the most regulated ones in the world. Financial data breaches cost an average of $6.08 million, according to GSB Capital Ltd.

Risk management is not optional; it’s a business survival skill. This is why fintech app security must be non-negotiable regardless of which development model you choose.

Below are the key offshore fintech development risks and how leading companies diminish them:

| Risk | Level | Mitigation Strategy |

| Data Breach / IP Theft | High | Sign NDA, use GDPR/SOC2-compliant vendors, restrict data access |

| Regulatory Non-Compliance | High | Vet vendor’s knowledge of PCI-DSS, GDPR, and local financial laws |

| Time Zone Delays | Medium | Establish overlapping hours; use async-friendly tools (Jira, Slack) |

| Communication Gaps | Medium | Weekly video calls, documented sprints, shared project boards |

| Quality Issues | Medium | Run a 2-week pilot, request fintech-specific references |

| Vendor Dependency | Low–Medium | Keep key architecture knowledge in-house; use phased contracts |

One way to reduce vendor dependency risk is to keep your core fintech app architecture documented in-house.

What About Onshore Risks?

Onshore fintech development risks are what rarely get talked about:

- Cost overruns: Onshore projects with scope creep can become very costly, very fast.

- Talent shortage: Specialized fintech developers are limited in many markets, resulting in long hiring cycles.

- Single point of failure: Over-reliance on a small local team creates operational risk.

- Slow scaling: Adding 5 developers onshore takes months; offshore can be achieved in weeks.

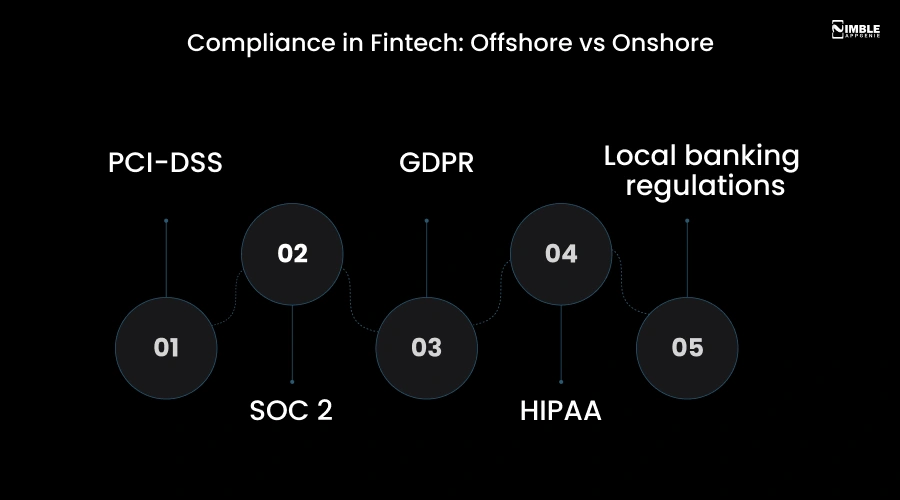

Compliance in Fintech: Offshore vs Onshore

This is where fintech stands apart from other industries. You are dealing with people’s money, their financial data, and heavily regulated systems. Compliance is non-negotiable.

Key Regulatory Frameworks to Consider:

- PCI-DSS: Payment Card Industry Data Security Standard (mandatory for any app handling card payments)

- SOC 2: Security, availability, and confidentiality standard (expected by enterprise clients)

- GDPR: Applies to any fintech serving European users

- HIPAA: If your fintech intersects with healthcare payments

- Local banking regulations: Varies by country (RBI in India, FCA in the UK, and CFPB in the US)

Your fintech tech stack choices directly impact how easily you can meet these compliance standards.

Offshore + Compliance: The Truth

Can offshore development teams handle fintech compliance? Yes – but you need to evaluate them carefully. Understanding KYC and AML compliance for fintech in depth is critical before you brief any offshore or onshore vendor.

Ask any offshore vendor:

- Have they built PCI-DSS-compliant products before?

- Can they provide audit documentation and traceable codebases?

- Do they have ISO 27001 certification (information security)?

- Do they have experience with GDPR data handling?

- Do they use NDAs and secure data sharing protocols?

Not familiar with all the fintech regulations that apply to your product? Start here before you hire anyone.

| Pro tip: Ask for 2-3 references, particularly from fintech clients, not only general software clients. Fintech compliance questions need a financial services context to be vetted meaningfully. |

The Hybrid Model: Why Most Fintechs in 2026 Are Choosing Both

Here’s what smart fintech companies have figured out: it’s not offshore OR onshore. It’s offshore AND onshore – strategically combined.

The hybrid fintech development model works like this:

| Onshore Team Handles | Offshore Team Handles |

| Product strategy & roadmap | Core engineering & development |

| Stakeholder communication | QA and automated testing |

| Compliance oversight | DevOps and CI/CD pipelines |

| UI/UX direction | Backend infrastructure |

| Regulatory liaison | Feature development at scale |

This model is specifically effective for growth-stage fintechs because it balances cost savings with strategic regulation. You get a talent pool of offshore and speed at 40-60% savings, while keeping compliance and high-stakes decisions work close to home.

How to Choose: A Simple Decision Framework for Fintech Leaders

Stop searching ‘offshore vs onshore’ – check the specifications below:

Choose Offshore If:

- Your fintech software development project has well-defined, documented specs and requirements.

- You need to scale the team fast

- Budget optimization is your top priority

- You have a robust internal technical lead who can bridge communication gaps.

- Your product targets markets with moderate compliance complexity

- Budget is your primary constraint.

Fintech software development outsourcing gives you the most leverage at the early stage.

New to outsourcing altogether? Start with our beginner’s guide to outsourcing software development before you evaluate vendors.

Choose Onshore If:

- Your fintech needs daily real-time collaboration and frequent pivot decisions

- Data sovereignty laws in your region do not permit cross-border data sharing

- You are operating in a highly regulated sector (government contracts, banking licenses)

- You are creating a flagship product where UX depends on local market nuance

- Budget is secondary to quality, speed, and compliance control

Choose Hybrid If:

- You are at the growth stage with active compliance needs and budget constraints

- You want to shrink timelines with near-24/7 development cycles

- You are scaling globally and need diverse technical talent

- You need product ownership onshore, but engineering capacity offshore

What to Look For in a Fintech App Development Company (Offshore or Onshore)

The model matters less than a fintech app development company. Here’s what to evaluate before you sign any contract:

Non-Negotiables for Fintech Development Partners

- Fintech domain expertise: Check if they have actually built payment apps, banking solutions, or lending platforms? Not just ‘mobile apps’. A partner who understands how fintech apps make money will build your architecture around revenue, not just features.

- Security certification: SOC 2 compliance, ISO 27001, and PCI-DSS experience are table stakes.

- Audit-ready documentation: Fintech codebases need complete traceability for PCI-DSS audits and SOC 2.

- Fintech client references: Ask for 2-3 fintech-specific references. A healthcare app reference won’t tell you what you need to know.

- Transparent sprint process: Weekly demos, visible progress boards, documented sprints

- IP ownership clarity: Who owns the code? All IP should transfer to you. Get this in the contract.

- Pilot project policy: Any good partner will let you start with a 2-week paid pilot before committing long-term

| Pro Tip from the Industry: One pattern repeated across successful offshore fintech engagements: companies that moved from pure offshore to hybrid arrangements witnessed measurable reductions in ticket rework within a few months, not because engineers changed, but because same-day communication replaced overnight wait times. Structure matters as much as location. |

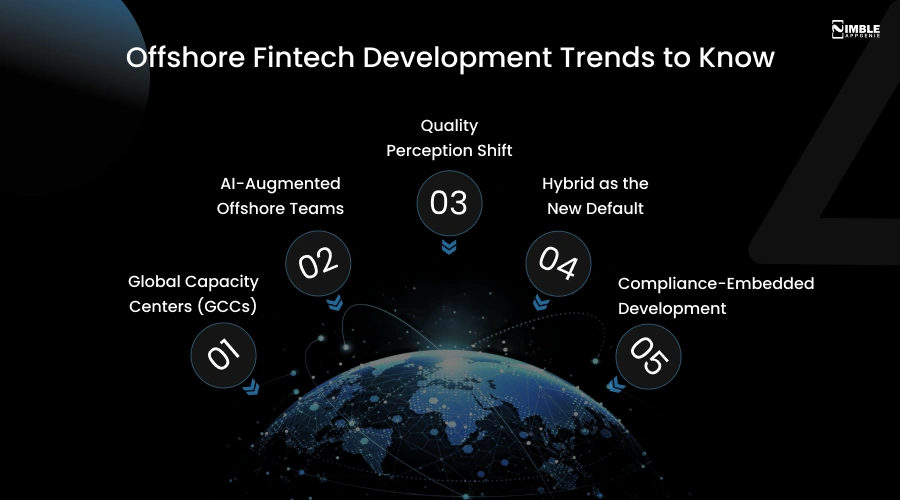

Offshore Fintech Development Trends to Know in 2026

The offshore vs onshore fintech development debate has surfaced significantly. Here’s what’s shaping the landscape right now, driven by fast-moving IT outsourcing trends that are redefining how fintech teams are built.

1. Global Capacity Centers (GCCs)

Besides outsourcing, companies are setting up strategic offshore innovation hubs. India alone in 2026 hosts over 2,117 GCCs, accounting for almost 60% of the world’s total. These are no longer just support centers; they are full-fledged product development command centers.

2. AI-Augmented Offshore Teams

With tools like GitHub CoPilot increasing developer output by 55%, offshore teams are delivering more output per hour than ever before. An offshore developer leveraging AI tools now competes directly with onshore developers at a fraction of the cost.

3. Quality Perception Shift

The old narrative of ‘offshore = lower quality’ is dead. In 2026, offshore teams routinely build for regulated industries like healthcare, fintech, and defense. Quality is no longer the primary concern – choosing the right operating model is what matters.

4. Hybrid as the New Default

The IT outsourcing market is expected to reach $638.65 billion globally. Growth is no longer centered around pure onshore or pure offshore models; it is happening in hybrid models that blend the best of both, strategically aligned to compliance requirements and project phase.

If you are a startup deciding how to create a fintech app in today’s market, the hybrid model is worth understanding from day one.

5. Compliance-Embedded Development

The EU’s DORA regulation (Digital Operational Resilience Act) went live in 2025. Combined with the EU AI Act, fintech teams now demand RegTech embedded directly into their development pipeline.

Top offshore vendors have adapted. Vendors who embed AI fraud detection directly into their development pipeline are the ones worth evaluating.

How Nimble AppGenie Approaches Fintech Development

As a fintech app development company, Nimble AppGenie, we have spent years building fintech products that are scalable, secure, and compliant for startups and established financial institutions.

Here is how we think about the offshore vs onshore fintech development question for our clients:

- We begin with your compliance needs, not your budget. Compliance shapes architecture, so we get it right first.

- We offer ISO-certified, PCI-DSS-compliant fintech app development with complete audit-ready documentation.

- We have developed 50+ fintech solutions, including banking platforms, eWallets, payment gateways, and investment apps.

- We structure engagements as hybrid by default – engineering execution managed by our experts and strategic oversight aligned with your team. Curious about how much your fintech app will cost before you decide on a model? Get a realistic estimate here.

- Each engagement starts with a free consultation and a scoped project proposal – no lasting commitment required upfront.

Whether you are deciding between offshore, onshore, or hybrid, we will give you an honest recommendation based on your market, product, and budget.

Conclusion

When it comes to the offshore vs onshore debate, there is no universal winner, and anyone who says otherwise is probably selling something.

What’s important is to align your development model with your compliance requirements, product stage, team capabilities, and budget realities.

If you are an early-stage fintech with a lean budget and a well-scoped product, offshore enables you to build smart and fast. If you are in a heavily regulated market with daily stakeholder collaboration needs and complex compliance requirements, onshore or hybrid is likely the smarter play.

And if you are like most growth-stage fintechs in 2026, you will find that a well-structured hybrid model offers you the best of both worlds: control where it counts, and cost efficiency where it matters.

The key is choosing the right fintech app development company that understands fintech deeply, not just software development.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.