Banking Software Development

Banking Software Development Payroll Software Development

Payroll Software Development Our Work Process

Our Work Process Awards

Awards

In a Nutshell:

- Buy Now Pay Later is becoming a popular payment option for both customers and businesses because it improves purchase conversion and user experience.

- BNPL payment apps are no longer limited to ecommerce. They are now used in retail stores, travel bookings, healthcare services, and subscription payments.

- BNPL apps are shifting towards safer lending with better credit checks, user limits, and repayment tracking.

- Mobile-first BNPL solutions are important, as most users prefer managing BNPL payments through apps instead of websites.

- Integration with payment gateways and POS systems is a key trend, helping BNPL work smoothly for online and offline merchants.

- Collaborating with banks and fintech companies helps BNPL providers manage funds, reduce risk, and scale faster.

Buy Now, Pay Later has stormed the entire financial realm. In the past year, BNPL has been the fastest-growing and most in-demand financial service to have emerged.

Thanks to the convenience it brings along, several online users, especially new users and Gen Z customers, have started using BNPL services.

This rise in usage has certainly contributed to the overall growth that the BNPL market is witnessing.

Financial service providers and non-financial service providers are all interested in building their own BNPL application.

The market is certainly rewarding as the global BNPL market size was valued at $90.69 billion in 2020 and is expected to reach $3.98 trillion by 2030, growing at a compound annual growth rate (CAGR) of 45.7% from 2021 to 2030.

However, to capitalize on this growth, you need to be on the same page as the market and understand the latest BNPL trends.

In this post, let us take a look at all the trends that define the current BNPL market and also address potential trends that will shape the Buy Now, Pay Later landscape in the upcoming years.

Without further ado, let’s begin by learning about the current trends of the BNPL market.

Buy Now, Pay Later: Current Market Trends

If we take a look at the current trends, BNPL is a flourishing market with billions of dollars in revenue. The service has transitioned from a new and upcoming technology to an increasingly used solution, showing significant growth.

Currently, the market for BNPL services is showing slowed growth as the industry has already hit its maturity. What it means is that almost everyone knows about BNPL services and has already created their solution.

To draw a perspective, here are the current trends classified in terms of growth, adoption, & market visibility.

♦ Rapid Growth

The market for BNPL is experiencing significant growth with an increase in use. This has led to a rise in the number of loans that originated and the loan values.

♦ Increased Adoption

As every bank has started rolling out a BNPL service, it has certainly become mainstream in the past few years. This has led to an increase in the adoption of the service as people today use it for all types of transactions.

♦ Online Dominance

The key playground for BNPL lies in e-commerce and online transactions. The integration of BNPL into e-commerce platforms has certainly made it the most preferred payment method for users, especially Gen Z.

♦ Increased Offline Transactions

With the integration of the BNPL service in physical POS terminals, the use of the same in offline transactions has substantially increased in the past few years, making it fit for all sorts of expenses.

Given that these trends are taking over the entire market today, you can expect the future to be brighter for BNPL services and service providers.

This also means the chances of you succeeding in the BNPL business are higher. If you are planning to develop a BNPL application, this is the right time.

What Are the Latest BNPL Future Trends & Perspectives?

The Buy Now, Pay Later (BNPL) market is rapidly evolving, with significant trends shaping its growth and adoption.

Here are the top 11 BNPL trends to look out for:

1. Expanding Beyond Retail

Buy Now, Pay Later (BNPL) services are expanding beyond traditional retail into sectors like healthcare, travel, and education.

Consumers can now use BNPL options to finance medical treatments, vacations, and even educational courses, making high-cost services more accessible.

-

Healthcare

Companies like Walnut and Affirm are allowing patients to pay medical bills in installments. This includes not only elective procedures but also emergency services, dental work, and even veterinary care.

This flexibility helps patients manage large medical bills without immediate financial stress.

-

Travel

Travel platforms such as Expedia and Fly Now Pay Later offer BNPL options for booking flights, accommodation, and vacation packages.

This allows consumers to manage travel expenses more efficiently without upfront costs, making travel more accessible to a broader audience.

-

Education

BNPL providers are partnering with educational institutions to finance courses, certifications, and training programs. Companies like Climb Credit and EdAid offer installment plans for tuition fees, making education more accessible and affordable.

This trend is particularly significant as it supports continuous learning and skill development in a rapidly changing job market.

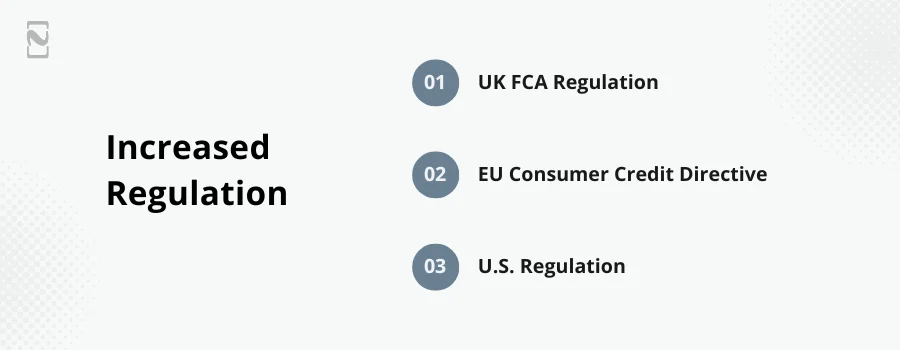

2. Increased Regulation

As the BNPL market grows, fintech regulators are paying closer attention.

In regions like the EU, UK, and USA, the new regulations aim to protect consumers from over-borrowing and ensure transparent terms.

-

UK FCA Regulation

The UK’s Financial Conduct Authority (FCA) is introducing stricter rules for BNPL providers. These include mandatory credit checks and clear communication of terms and potential impacts on credit scores.

The move is aimed at preventing consumers from accumulating unmanageable debt.

-

EU Consumer Credit Directive

The European Union is revising its Consumer Credit Directive to include BNPL services. The law ensures consumer protection and responsible lending practices by implementing standardized disclosure requirements, caps on late fees, and enhanced consumer rights.

-

U.S. Regulation

The Consumer Financial Protection Bureau (CFPB) in the U.S. is also scrutinizing BNPL providers to ensure they adhere to fair lending practices and transparency.

This includes monitoring the reporting of BNPL loans to credit bureaus and ensuring that terms and conditions are clearly communicated to consumers.

3. Integration with Traditional Financial Institutions

Banks and credit card companies are increasingly integrating BNPL options into their offerings.

This trend is driven by the need to compete with fintech startups and meet consumer demand for flexible payment solutions.

-

Partnerships

Goldman Sachs has partnered with Apple to offer BNPL through Apple Card, allowing users to split their purchases into monthly installments directly from their Apple devices.

This integration leverages the trust and user base of established financial institutions while providing modern payment flexibility.

-

In-House BNPL Services

Major banks like HSBC and Barclays are developing their own BNPL solutions to offer alongside traditional credit products. These banks are leveraging their existing customer base and infrastructure to provide a seamless BNPL experience.

For example, HSBC’s “Splitit” allows users to divide purchases into interest-free installments, providing a competitive edge in the digital payment landscape.

Also Read: BNPL vs Credit Cards

4. Growth in Emerging Markets

BNPL is gaining traction in emerging markets, providing access to credit for underserved populations and boosting local economies.

-

Latin America

Companies like Kueski and MercadoPago are expanding BNPL services in Mexico and Brazil.

These services cater to the needs of the growing middle class, providing flexible payment options for consumers who may have limited access to traditional credit facilities.

This expansion supports economic growth and financial inclusion in these regions.

-

Southeast Asia

Fintech startups in countries like Indonesia, the Philippines, and Vietnam are introducing BNPL options to cater to the increasing demand for flexible payment solutions.

These services help bridge the gap for consumers who have limited access to traditional credit, fostering greater financial inclusion and enabling more people to participate in the digital economy.

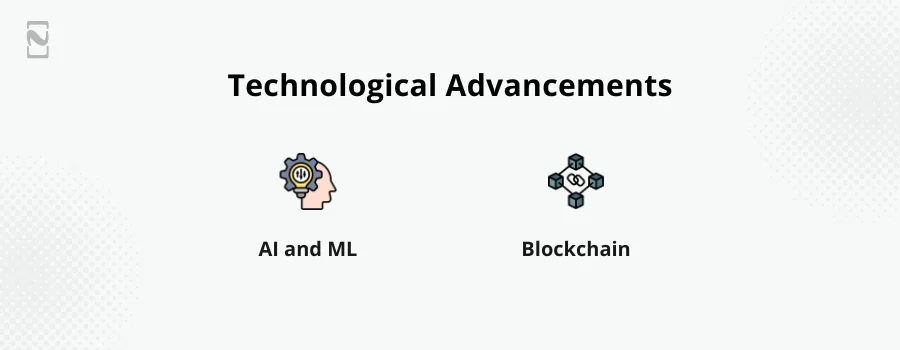

5. Technological Advancements

Advancements in technology are driving innovation in the BNPL sector.

Artificial intelligence (AI) and Machine Learning (ML) are being used to enhance credit assessments and fraud detection.

-

AI and ML

These technologies help BNPL providers assess creditworthiness more accurately and prevent fraudulent activities, ensuring safer transactions for both consumers and merchants.

AI-driven models can analyze vast amounts of data to predict consumer behavior and assess risk, reducing the likelihood of default.

-

Blockchain

Some BNPL platforms are exploring blockchain technology to offer transparent and secure transactions, reduce the risk of fraud, and improve the efficiency of payment processing.

Blockchain can provide immutable records of transactions, enhancing trust and security in the BNPL ecosystem.

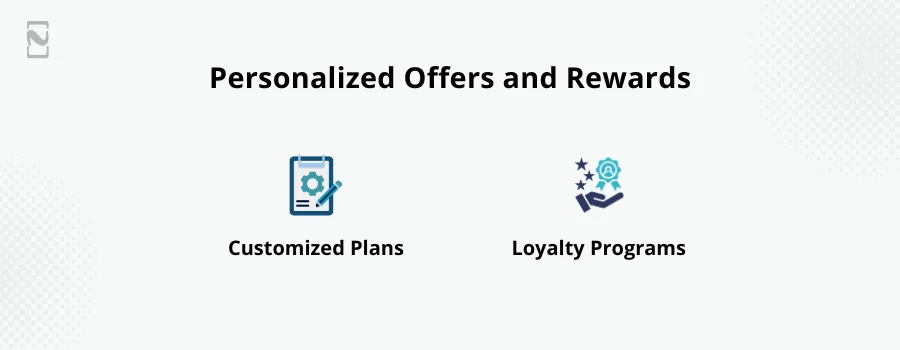

6. Personalized Offers and Rewards

BNPL providers are leveraging data analytics to offer personalized financing options and rewards to users. This enhances the user experience and loyalty.

-

Customized Plans

Users receive personalized installment plans based on their spending habits and financial behavior, making repayment easier and more convenient.

This tailored approach ensures that consumers are offered payment plans that align with their financial capabilities.

-

Loyalty Programs

BNPL services introduce loyalty programs where users earn rewards and discounts for using the service regularly.

This includes cashback offers, discounts on future purchases, and exclusive deals. By incentivizing repeat use, BNPL providers can foster long-term customer loyalty and engagement.

7. Enhanced Consumer Education

To promote responsible borrowing, BNPL providers are focusing on educating consumers about the implications of using these services.

-

Financial Literacy Programs

Educational resources and tools are provided to help consumers understand how BNPL works, manage their finances better, and avoid excessive debt.

These programs often include webinars, online courses, and interactive tools that guide consumers through the basics of credit management and responsible borrowing.

-

Transparent Communication

Clear communication about fees, interest rates, and repayment terms is being prioritized to ensure consumers make informed decisions and understand the full cost of their purchases.

BNPL providers are investing in user-friendly interfaces and communication strategies that demystify financial terms and conditions.

8. Sustainability Initiatives

BNPL providers are incorporating sustainability initiatives to appeal to environmentally conscious consumers.

-

Eco-Friendly Purchases

Partnerships with eco-friendly brands and products encourage users to make sustainable choices, aligning their spending habits with their environmental values.

BNPL providers are collaborating with sustainable brands to offer exclusive deals and incentives for eco-friendly purchases.

-

Carbon Offsetting

Some Buy Now, Pay Later (BNPL) platforms offer carbon offset programs where a portion of each transaction is used to fund environmental projects, helping to mitigate the carbon footprint of consumer purchases.

These initiatives appeal to consumers who are conscious of their environmental impact and seek to support businesses that prioritize sustainability.

The idea of using BNPL to pay for costly goods and services is definitely a game-changer, and we can see it happening in the upcoming years. With all these trends and prospects of the service, you might have made up your mind about launching your own application.

If you are wondering what it would cost to develop a BNPL app, you must know that it all depends on different factors, your choice of fintech development company being the primary one.

Why Choose Nimble AppGenie for BNPL App Solution?

The ideal step to take for any financial service provider is to integrate BNPL services into their banking/financial app.

If you plan to do so, Nimble AppGenie can be the perfect partner. Not only do we have experience in fintech app development solutions, we also have a team of highly capable analysts and developers who can help you with research and development..

With extensive experience and a team of expert developers, we ensure that your Buy Now, Pay Later (BNPL) app integrates the latest technologies, adheres to regulatory standards, and provides an exceptional user experience.

Our end-to-end BNPL app development services cover everything from initial consultation and design to deployment and ongoing maintenance.

Conclusion

The BNPL sector is poised for significant growth and transformation, driven by technological advancements, regulatory changes, and expanding market opportunities.

For businesses looking to capitalize on these trends, understanding the factors influencing the development cost and strategies for cost optimization are essential.

As the market evolves, staying informed and agile will be key to leveraging the full potential of BNPL services.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.