AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

In a Nutshell:

- Super app development means building a platform for payments, shopping, messaging, finance, and mobility under a single login and shared wallet. An MVP costs $150,000–$350,000 and takes 4-7 months; a full platform with a mini-app ecosystem runs $500,000–$1.5M over 10–18 months.

- The business case is structural: super app users generate 3 to10× higher lifetime value than single-service app users, with multiple revenue streams, lower amortized CAC, and a competitive moat that deepens with every service added.

- A production-grade super app needs microservices architecture, an API gateway, SSO, and a mini-app SDK from day one; retrofitting a monolith into a platform costs 3 to 5× more than creating the infrastructure correctly upfront.

- Development costs range from $150K for an MVP to $5M+ for an enterprise build across multiple markets, with hidden costs in third-party APIs at scale, regulatory licensing, and cloud infrastructure often exceeding 30% of the initial build budget.

- Nimble AppGenie has built production super apps for clients across the Middle East and Southeast Asia – if you are evaluating a super app build, the fastest next step is a free scoping call to get a cost estimate tailored to your market, service mix, and timeline.

The next billion-dollar platform is not a single-purpose app; it’s a super app, and the race to build one is speeding up in 2026.

Across the Middle East, Southeast Asia, Africa, and now the West, forward-thinking startups and enterprises are accelerating super app development, building digital ecosystems that don’t just serve users but also own their routines.

WeChat processes 1 billion+ monthly active users. Gojek manages everything from food delivery to insurance. Grab became a $15B (figures fluctuate with time) company by doing everything well within a single platform.

If you are a CEO, CTO, investor, or project leader reading this, the question is no longer “should we build a super app?” It’s “can we afford not to?”

This complete super app development guide covers all you need to make a sound decision and execute it – what a super app is, why the market weighs more than ever in 2026, what features and architecture you need, how to build one step-by-step, how much it costs, and how to monetize it.

Let’s get into it.

What is a Super App?

A super app is a single mobile or web platform that integrates multiple services – payments, transportation, healthcare, shopping, communication, food delivery, finance, and more into one unified experience, under a single identity layer (single sign-on), a mini app ecosystem, and a common wallet.

The term gained traction through Mike Lazaridis, the BlackBerry co-founder, but the concept was mastered by Tencent’s WeChat in China.

Today, the definition has expanded beyond messaging and payments. A true super app in 2026 is a digital ecosystem that’s more than a product with numerous features.

Super App vs Regular App: What’s the Real Difference?

| Dimension | Regular App | Super App |

| Core purpose | Solves one problem | Solves many problems across life verticals |

| User identity | Siloed login | Single sign-on (SSO) across all services |

| Business model | Single revenue stream | Multiple monetization layers |

| Third-party integration | Limited or none | Open mini-app ecosystem for partners |

| Switching cost | Low | Extremely high (locked-in daily habits) |

| Data advantage | Narrow behavioral data | 360° user profile across all life activities |

| Tech architecture | Monolithic or standard MVC | Microservices + modular app development |

| User retention | Dependent on a single use case | Naturally high — users return for everything |

| Market position | Feature competitor | Platform owner |

| Value to investors | Product | Infrastructure |

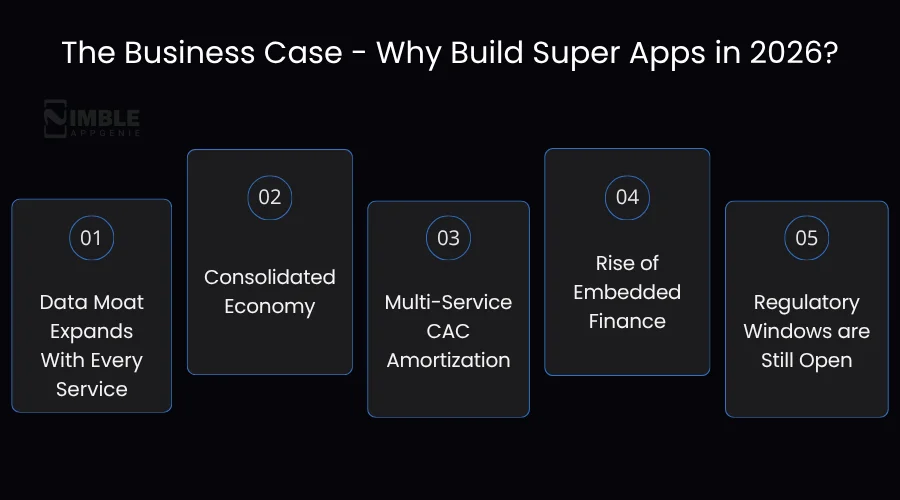

The Business Case – Why Build Super Apps in 2026?

Decision-makers usually ask: why now? Data moat expansion, consolidated economy, higher customer acquisition cost (CAC), increased financial service margins, and dynamic regulatory frameworks are the chief drivers that make 2026 the most compelling moment to start or accelerate super app development.

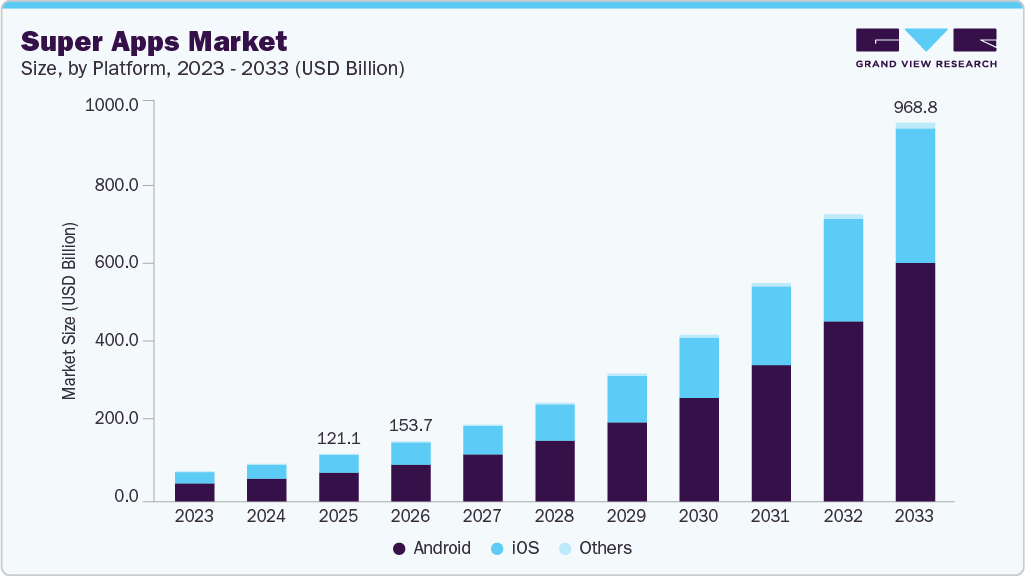

| The global super app market is predicted to be valued at $968.77 billion by 2033, rising at a CAGR of 30.1%. |

1. Data Moat Expands With Every Service

Every service you append to your super app cross-leverages behavioral data. A taxi-booking platform also sees your restaurant preferences, grocery orders, and financial transactions, enabling deeper personalization that single-service apps cannot match. This data benefit blends annually.

2. Consolidated Economy

App fatigue has been one of the major issues users are facing. The average smartphone has 80+ apps installed, but only 9 are used daily. Here, super apps win by becoming the primary platform in users’ daily lives – only one login, one wallet, and one interface.

3. Multi-Service CAC Amortization

Customer acquisition cost (CAC) for a single service is high and increasing. On a multi-service platform, a user is acquired once, and you can monetize them across five to ten touchpoints. The unit economics become favorable at scale.

4. Rise of Embedded Finance

In 2026, the most lucrative layer of any super app is financial service margins. Once you have a user’s payment rails, you can offer insurance, lending, BNPL, and investment products – all at near-zero marginal CAC.

If you are evaluating which financial products to layer in first, our fintech app development team can scope the licensing and architecture implications before you commit.

5. Regulatory Windows are Still Open

In the UK, the US, Southeast Asia, and the UAE, regulatory frameworks for super apps are still being defined. Early movers who develop compliant infrastructure now will be safeguarded by network effects before regulation becomes rigid.

What are the Types of Super Apps?

When it comes to super app development, you can choose any type to build, industry-wise, according to user type, or origin strategy.

Let’s get deeper:

1. By User Type

B2B Super Apps: Such apps serve businesses with a single platform for logistics, procurement, workforce management, payments, and compliance. Emerging players in the Middle East and Southeast Asia are intensively targeting this space.

Consumer Super Apps: These target end-users with routine lifestyle services: food, transportation, healthcare, entertainment, and payments. Grab, WeChat, and Gojek are the canonical examples.

Government/Civic Super Apps: These apps consolidate public services – tax filing, identity verification, healthcare access, and permits into a unified citizen-facing interface. Singpass in Singapore and UAEICP in the UAE are early leaders.

| In 2026, monolithic super app architectures are anticipated to account for about 55% of the market, driven by vertical monetization efficiency and integrated data control. |

2. By Origin Strategy

Payments-First: Foster trust through financial transactions, then scale into commerce and services. M-Pesa, Paytm, and Alipay followed this trajectory.

Messaging-First: Start with high-frequency communication, add payments, then services. WeChat’s playbook – high retention from day one, but demands a massive user base to monetize.

E-commerce-First: Begin with a marketplace, add logistics and payments, and move into financial services. Amazon is following this route in Western markets.

On-demand Super App Strategy: Roll out with only a high-frequency on-demand service (food, rides, payment rails, and proven logistics, then expand horizontally. Gojek and Grab are the definitive case studies.

3. By Industry Vertical

| Vertical | Leading Super App Example | Primary Services Bundled |

| Mobility + Lifestyle | Grab, Gojek | Rides, food, payments, insurance |

| Messaging + Finance | WeChat, KakaoTalk | Communication, payments, mini-apps |

| E-commerce + Finance | Alipay, Paytm | Shopping, lending, investment |

| Healthcare | Ping An Good Doctor | Telemedicine, pharmacy, insurance |

| Retail + Loyalty | Careem (post-Uber) | Rides, food, groceries, pay |

| Neobank + Lifestyle | Revolut (evolving) | Finance, travel, insurance |

Super App Business Model: The Strategic Architecture

First, you need to understand what kind of business you are building before you decide what to build.

Don’t confuse a super app with a product equipped with various features. Rather, it is a platform business, and this differentiation changes everything: how you structure partnerships, how you price, how you compete, and how you evaluate success.

► Platform Business vs. Service Aggregator: A Critical Distinction

Various companies planning super app development make one of two mistakes.

Either they develop a service aggregator – a single app that stacks several services but doesn’t create network effects between them. Or they build a product company that recognizes itself as a platform.

Neither creates a reliable competitive advantage that makes super apps worth the investment.

A real super app business model is a multi-sided platform that creates value, allows interactions between numerous distinct user groups – merchants, consumers, mini-app developers, and service providers – and it gets more value with each additional group.

| Model Type | How It Creates Value | Competitive Moat | Example |

| Single-service app | Solves one problem well | Feature quality | Uber (early) |

| Service aggregator | Bundles services under one brand | Convenience | Many failed super apps |

| Multi-sided platform | Connects users, merchants, and developers | Network effects + data | WeChat, Grab, Gojek |

| Digital ecosystem | Becomes infrastructure that others build on | Switching cost + platform ownership | WeChat (mature) |

Your target is the bottom row. Above that can be copied easily, except for the bottom two, because the collected data, relationships, and embedded habits are proprietary.

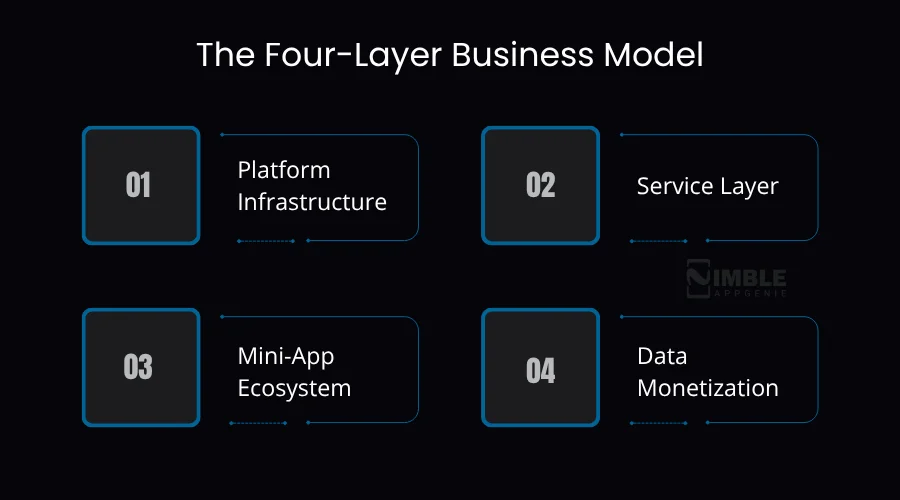

► The Four-Layer Business Model

A super app business model works across four interdependent layers that generate value for the above one and draw value from the below ones.

1. Platform Infrastructure

It’s the base that makes everything else possible: a unified digital wallet, single sign-on, push notifications, an API gateway, and analytics pipeline.

This layer doesn’t generate revenue directly, but it is the source of each competitive advantage that the platform holds. With it, you have a platform; it’s just a bundle of apps.

2. Service Layer

The actual services users come for include food delivery, rides, shopping, payments, insurance, and healthcare. Here, the user habits form and the platform earns its first revenue.

The strategic target of this layer is not profit boost, but habit formation. Services with which users engage daily are worth subsidizing if essential because daily engagement is what makes the above layers valuable.

3. Mini-App Ecosystem

Here, third-party businesses and developers create services on top of your platform, leveraging your identity layer, distribution, and payment rails. This is the layer that converts a super app from a company into an industry.

When WeChat rolled out its mini-program platform, it shifted from “a company with many products” to “a platform that the Chinese digital economy runs on”.

The mini-ecosystem is how you expand to 50+ services without increasing your engineering team proportionally.

4. Data Monetization

The cross-service behavioral data generated by layers 1-3 empowers credit scoring, fraud detection, targeted advertising, personalization, and financial products.

On this layer, the highest-margin revenue lives, and it only exists because the three layers below are functioning.

► The Super App Business Model vs. A Regular App Business Model

| Dimension | Regular App Business Model | Super App Business Model |

| Value creation logic | Solve one problem for users | Facilitate interactions across multiple user groups |

| Revenue structure | One or two streams | Five to eight-layered streams |

| Competitive advantage | Product features | Network effects, data moat, switching costs |

| Growth dynamic | Linear (more users = more revenue) | Exponential (more users = more partners = more users) |

| CAC strategy | Acquire users for this product | Acquire users once, monetize across all products |

| Data strategy | Narrow use-case data | 360° behavioral profile across all life activities |

| Partnership model | Integrations | Developer ecosystem with revenue share |

| Strategic end state | Market share | Market infrastructure |

What are the Must-Have Features of a Super App?

The key features of a super app include a core platform, service layer, and trust & compliance features.

The right feature set makes the difference between a scaling platform and one that lags. Below are the core Super app features grouped by priority.

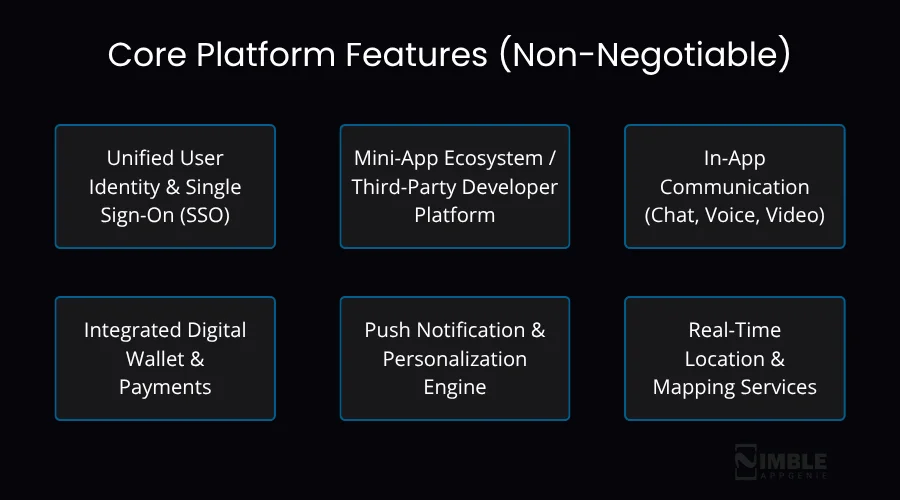

♦ Core Platform Features (Non-Negotiable)

1. Unified User Identity & Single Sign-On (SSO)

One account, one profile, one trust layer across all services; this is the base of the whole ecosystem. Without SSO, you don’t own a super app; actually, it’s a stack of apps wearing the same logo.

2. Mini-App Ecosystem / Third-Party Developer Platform

It’s the capability of external businesses to create and distribute lightweight applications within your super app. This creates network effects. It helps build a platform; without it, you are just building features.

3. In-App Communication (Chat, Voice, Video)

Mandatory in 2026. Users want to communicate with service providers, businesses, and each other while being on the app, and this super app feature helps them.

4. Integrated Digital Wallet & Payments

An in-app wallet that helps in seamless transactions across all peer-to-peer transfers, services, withdrawals, and top-ups. Payments create connectivity in a super app.

See how we approach this specifically through our eWallet app development

5. Push Notification & Personalization Engine

Cross-service notifications are context-aware and driven by behavioral data. The personalization layer is what makes a super app feel important rather than overwhelming.

6. Real-Time Location & Mapping Services

It’s necessary for any on-demand super app with mobility, delivery, or field service components.

♦ Service Layer Features (Tier-Dependent)

| Service Module | Required For | Complexity |

| Ride-hailing / Mobility | On-demand super apps | High |

| Food & Grocery Delivery | Lifestyle platforms | Medium-High |

| E-commerce Marketplace | Retail super apps | High |

| Micro-lending / BNPL | Finance-layer platforms | High (regulatory) |

| Insurance Products | Mature super apps | High (regulatory) |

| Healthcare / Telemedicine | Health-focused platforms | Very High |

| Loyalty & Rewards Engine | All types | Medium |

| Subscription Management | All types | Low-Medium |

If BNPL is part of your roadmap, our BNPL app development team can walk you through the underwriting and compliance groundwork before you

♦ Trust & Compliance Features

1. Multi-Layer Security

Device fingerprinting, biometric authentication, fraud detection ML models, and transaction monitoring.

2. KYC/AML Integration For Financial Service Components

Non-negotiable in regulated markets.

3. Ratings & Review System

Dual-side trust infrastructure for on-demand service providers and marketplaces.

4. Data Privacy Controls

Regulatory-compliant dashboards, GDPR, and PDPA for users.

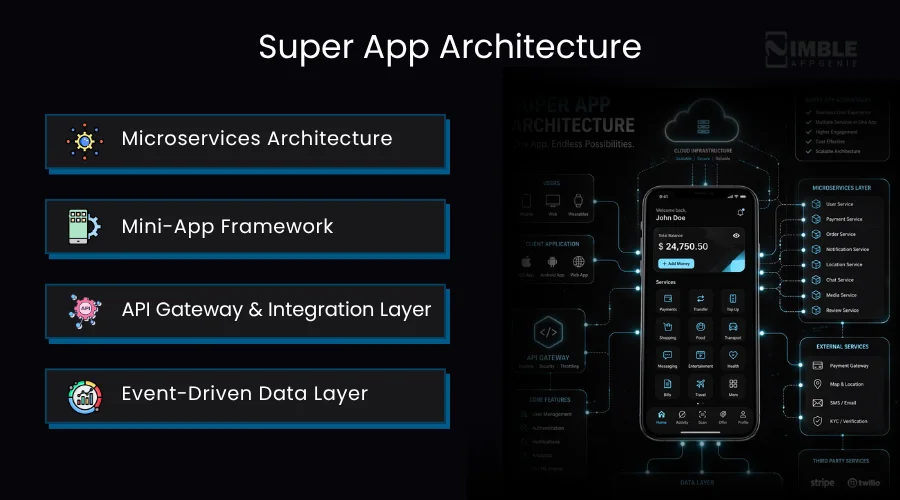

Super App Architecture

A production-level super app can’t run on a monolithic architecture. A single viable foundation is a microservice architecture in which every service (rides, food, payments, and messaging) runs as an independently deployable unit and interacts via APIs.

The four architectural pillars are:

1. Microservices Architecture

Every service is a standalone module with its deployment pipeline, database, and scaling policy. This allows you to update the food delivery module without even interfering with the payment service.

2. Mini-App Framework

A sandboxed runtime environment, similar to a browser, allows third-party developers to create lightweight apps using your platform’s identity layer, APIs, and payment rails.

3. API Gateway & Integration Layer

The central nervous system that bridges requests between microservices, handles rate limiting, enforces authentication, and exposes endpoints for mini-app developers.

4. Event-Driven Data Layer

A real-time event streaming backbone (Apache Kafka or equivalent) enables fraud detection, cross-service personalization, and analytics without tight service coupling.

Note: We cover super app architecture in full technical depth, including infrastructure diagrams, database design, and scalability patterns in our dedicated Super App Architecture guide.

How Is AI Used in Super App Development in 2026?

By 2026, AI is not an add-on feature in a super app; it’s the layer that makes a 10-service platform feel like a 1-service app. Without it, more services only mean more clutter and rapid user drop-off.

1. Personalized Service Surfacing

Instead of revealing to every user all 10+ services, AI models rank and surface only the 4-5 services a specific user actually touches, based on behavioral data across the platform. This is the single biggest UX lever for reducing churn as a super app scales past 5 services.

2. Cross-Service Fraud and Risk Detection

One identity layer means one attack surface. AI fraud models trained on cross-service transaction patterns (a payment anomaly that correlates with a delivery address change, for example) catch fraud that single-service apps miss completely.

3. AI-Powered Mini-App Discovery

As mini-app ecosystems grow past a few hundred third-party apps, manual categorization breaks down. Recommendation models surface the right mini-app to the right user at the right moment, the same problem WeChat solved at 4M+ mini-programs.

4. Conversational and Agentic Interfaces

An increasing share of new super app builds are adding an AI assistant layer that can accomplish a task across services – book a ride and pay for it, or order food and apply a loyalty credit through one conversational interface instead of multiple screens.

5. Embedded Credit Scoring

Cross-service behavioral data feeds AI-driven credit and risk scoring for BNPL and micro-lending products, usually without traditional credit bureau data. That’s what allows fintech-originated apps to underwrite users that conventional lenders can’t.

| AI Use Case | Where It Lives | Business Impact |

| Personalized service ranking | App shell/home screen | Lower churn, higher daily engagement |

| Cross-service fraud detection | Event-driven data layer | Lower fraud losses, regulatory confidence |

| Mini-app recommendation | Mini-app ecosystem layer | Higher mini-app adoption at scale |

| Agentic task completion | Conversational interface | Fewer screens, higher conversion per session |

| Embedded credit scoring | Financial services layer | Underwriting extends beyond bureau data |

Note: Building this in-house means budgeting separately for model training data, ML engineering talent, and ongoing model monitoring, generally 10–15% on top of the core platform build cost in the first 18 months.

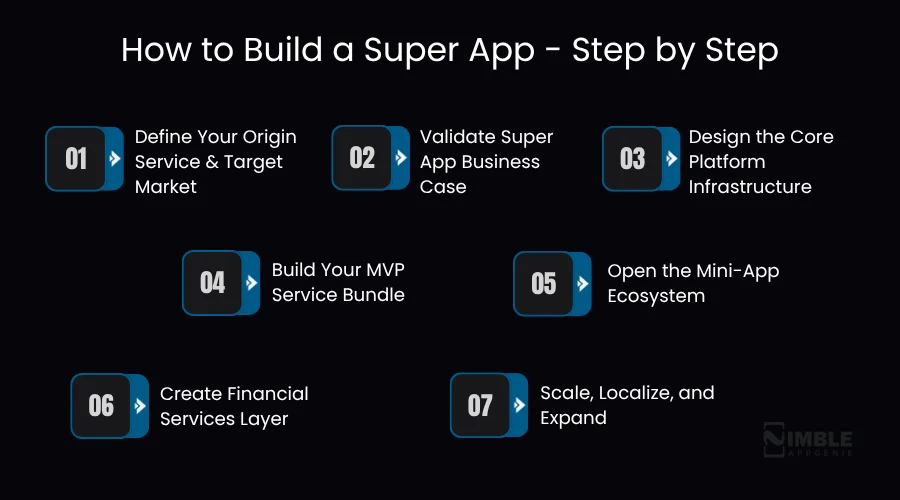

How to Build a Super App – Step by Step

A super app development is not only about adding features, but it’s also about creating a smooth digital ecosystem where users can access distinct services in one place.

Let’s walk through the step-by-step app development process to turn your mobile app idea into a user-centric platform.

1. Define Your Origin Service and Target Market

Do you know that every successful app began by mastering one high-frequency service in a particular geography?

You should also try not to launch all services at once. Only choose one where you have either a distribution advantage, existing infrastructure, or deep domain expertise.

Ask: What is the one service our target users need most frequently, where we can own the experience end-to-end?

If you’re a pre-seed or seed-stage team validating this, our startup app development services are built specifically for this stage.

2. Validate Super App Business Case

Before you start building the app, validate three things: sufficient Total Addressable Market (TAM) to justify your platform investment, user readiness to consolidate services in a single app, and regulatory feasibility of your target service mix.

3. Design the Core Platform Infrastructure

Here, most development teams underinvest and pay for it later. The core infrastructure – wallet, SSO, notification engine, API gateway, and analytics pipeline should be developed for horizontal scale from the start. Upgrading a monolithic app into a super app is 3 to 5 times more expensive than creating the platform accurately upfront.

This is also where most teams underinvest in design. Our UI/UX design team can help you get the platform shell right before development starts.

4. Build Your MVP Service Bundle

Roll out with your anchor service plus two to three adjacent services that share the exact user journey. A typical MVP stack: core services, chat, payment, and one additional service related to your vertical. Avoid feature bloating. The target of your MVP is to validate cross-service engagement – do users really use more than one service?

5. Open the Mini-App Ecosystem

Once your platform has popularity, open a developer SDK and mini-app framework to define your revenue share model, create a partner onboarding process, and developer documentation.

The mini-app ecosystem is the way you scale to 50+ services without expanding your engineering team.

6. Create Financial Services Layer

In any super app, the highest-margin services are financial products. Once you have enough transaction history and user trust, begin later in: BNPL, digital wallet with interest, insurance products, micro-lending, and investment tools.

This step usually needs regulatory licensing, which must be started well before product launch.

7. Scale, Localize, and Expand

Localize for every market – language, regulatory compliance, payment methods, and culturally related services. Establish operations in every geography with local service provider networks. Expand your mini-app partner ecosystem geographically.

Super App Development Roadmap-

| Phase | Duration | Deliverable |

| Discovery & Architecture | 6–10 weeks | Tech blueprint, product spec, vendor selection |

| Core Platform MVP | 4–7 months | SSO, wallet, API gateway, 1 core service |

| Service Bundle Launch | 3–5 months | 3–4 integrated services, mini-app framework v1 |

| Financial Layer | 4–6 months | Wallet upgrade, lending, insurance integration |

| Ecosystem Expansion | Ongoing | Mini-app partners, new geographies, new services |

Understanding the Super App Tech Stack

Do you know what a critical architecture decision is? It’s choosing the right technology stack that impacts developer velocity, scalability, and long-term maintenance cost.

► Recommended Tech Stack (2026)

| Layer | Recommended Technologies | Notes |

| Mobile Frontend | React Native, Flutter | Cross-platform; React Native preferred for ecosystem |

| Web Frontend | Next.js, React | SSR for SEO; React for mini-app compatibility |

| API Gateway | Kong, AWS API Gateway, Nginx | Kong for on-premise; AWS for cloud-native |

| Backend Services | Node.js, Go, Python (FastAPI) | Go for high-throughput services; Node for rapid development |

| Mini-App Runtime | Custom WebView + JS SDK | WeChat-style sandboxed runtime |

| Database (Transactional) | PostgreSQL, MySQL | ACID compliance for financial services |

| Database (NoSQL) | MongoDB, DynamoDB | User profiles, session data, event logs |

| Cache Layer | Redis | Session management, rate limiting, feed caching |

| Message Queue | Apache Kafka, RabbitMQ | Event streaming, inter-service communication |

| Search | Elasticsearch | Product/service discovery, in-app search |

| Maps & Geolocation | Google Maps API, Mapbox, HERE | HERE for Middle East/Asia cost optimization |

| Payment Processing | Stripe, Adyen, regional gateways | Stripe for Western markets; regional for EM |

| Authentication | Auth0, Firebase Auth, custom OAuth2 | SSO foundation |

| Cloud Infrastructure | AWS, GCP, Azure | Multi-cloud for geo-redundancy |

| Containerization | Docker + Kubernetes (K8s) | Required for microservices orchestration |

| CI/CD | GitHub Actions, Jenkins, ArgoCD | GitOps-based deployment |

| Monitoring | Datadog, Prometheus + Grafana | Full-stack observability |

| Analytics | Mixpanel, Amplitude, custom DWH | Behavioral analytics + data warehouse |

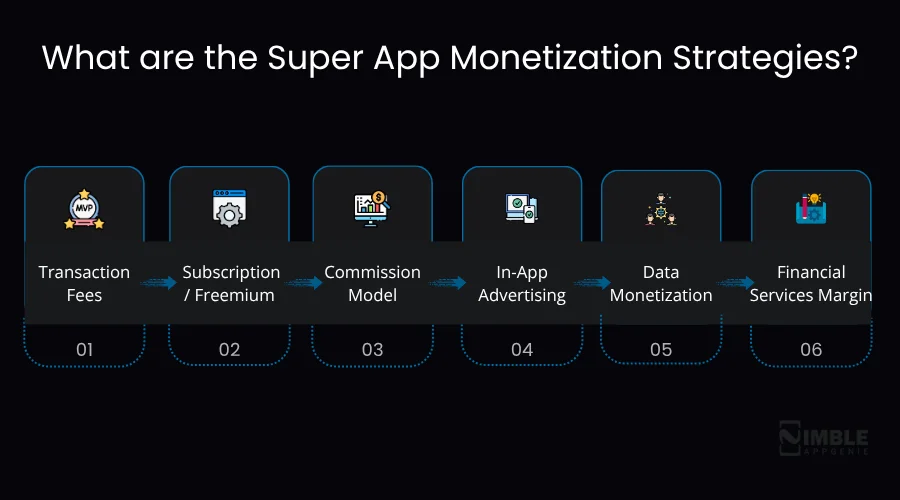

What are the Super App Monetization Strategies?

Here are the basic monetization models, how they work, and which business types each fits best.

1. Transaction Fees

How it works: Charge a flat fee or percentage on each transaction processed through your platform – food orders, rides, P2P transfers, and marketplace purchases.

Typical ranges: 1.5%–5% per transaction, depending on category.

Best for: On-demand super apps with high transaction volume (Grab, Gojek model).

Considerations: Needs volume at scale to be purposeful. Works poorly at sub-100K monthly transactions.

2. Subscription / Freemium

How it Works: Provide a free tier with core functionality and a premium tier with priority service, exclusive features, higher limits, or lower fees.

Typical Range: $3–$25/month, depending on market and value proposition.

Best For: Super apps with robust daily-use anchors (transportation, communication, finance).

Consideration: Subscription + cross discounts is the most impactful retention-monetization combination in 2026.

3. Commission Model

How it Works: Charge service providers, mini-app developers, or merchants a commission on revenue generated through your platform.

Typical Range: 10%–30% for food delivery; 15%–25% for marketplace; 15%–30% for mini-apps.

Best For: Marketplace and mini-app ecosystem operators.

Consideration: Commission rates bear download pressure as the ecosystem matures. WeChat took 0% commission to speed up mini-app adoption – a strategic option that paid off through payment fees and data.

4. In-App Advertising

How it Works: Sell ad inventory across the super app’s surfaces – sponsored mini-apps, feed ads, push notification sponsorship, and search result placements.

Typical Range: $5–$40 CPM depending on targeting precision.

Best For: Super apps with large, engaged user bases and rich behavioral data.

Consideration: Advertising monetization needs significant scale (5M+MAU) to be material. Carefully introduce, as aggressive ads hurt the user experience and raise churn.

5. Data Monetization

How it Works: Aggregate, anonymize, and sell behavioral insights to mobile app market research firms, enterprise clients, or government agencies. Alternatively, license the data infrastructure itself.

Best For: Super apps with 10M+MAU and cross-vertical data coverage.

Consideration: GDPR, PDPA, and similar laws need explicit consent frameworks. Pure data selling is becoming less viable; data-powered services are a more defensible form.

6. Financial Services Margin

How it Works: Origination fees, earn interest margin, and insurance premiums from embedded financial products – BNPL, investment products, insurance, and digital lending.

Typical Range: 8%–22% APR on lending; 2%–8% insurance margins; 0.25%–1% on AUM for investment products.

Best For: Any mature super app with KYC infrastructure and payment rails.

Consideration: This is the highest-barrier, highest-margin layer. Regulatory licensing is needed in most markets. Begin the licensing process early.

For a deeper cost breakdown specific to standalone fintech features, see our fintech app development cost guide.

➤ Super App Monetization Strategies (Deep Dive Reference Table)

| Monetization Layer | Revenue Mechanism | Typical Margin | Required Scale | Timeline to Activate |

| Transaction fees | % per order/ride/transfer | 15%–40% net | 50K+ MTU | Launch |

| Commission (merchants) | % of GMV from platform merchants | 10%–30% | 5K+ merchants | 3–6 months |

| In-app advertising | CPM/CPC on feed + search | 40%–70% | 500K+ MAU | 12–18 months |

| Subscription/premium | Monthly/annual fee | 60%–80% | 100K+ MAU | 6–12 months |

| Financial services | Interest margin + origination fees | 20%–40% | 1M+ MAU + license | 18–36 months |

| Mini-app developer fees | Listing + revenue share | 15%–30% rev share | Active developer community | 12–24 months |

| Data products | Anonymized insights / API access | 70%–90% | 5M+ MAU | 24–36 months |

➤ Monetization Model by Business Type

| Business Type | Primary Model | Secondary Models | Avoid |

| On-demand mobility platform | Transaction fees | Subscription, advertising | Pure commission early-stage |

| Messaging-first platform | Mini-app commissions | Advertising, financial services | Transaction fees (kills adoption) |

| Fintech-origin super app | Financial services margin | Transaction fees, subscription | Heavy advertising |

| E-commerce super app | Commission | Advertising, financial services | Subscription (friction to purchase) |

| B2B super app | Subscription (SaaS) | Transaction fees, data products | Advertising |

| Government super app | Government licensing fee | Transaction fees (limited) | Advertising (trust issue) |

What is the Super App Development Cost in 2026?

Most business plans go wrong due to a lack of understanding of the real cost of super app development. How? They plan the MVP cost and meet unexpected platform costs.

♦ Cost Range Overview

| Build Scope | Cost Range | Timeline |

| MVP (1 core service + payments + SSO) | $150,000 – $350,000 | 4–7 months |

| Full Super App (3–5 services + mini-app ecosystem) | $500,000 – $1,500,000 | 10–18 months |

| Enterprise Super App (5+ services, financial layer, 2+ markets) | $1,500,000 – $5,000,000+ | 18–36 months |

♦ Cost Breakdown Table

| Component | MVP Cost | Full Build Cost |

| Product Design (UX/UI) | $15,000 – $40,000 | $50,000 – $120,000 |

| Core Platform (SSO, wallet, API gateway) | $40,000 – $80,000 | $80,000 – $200,000 |

| Mobile App (iOS + Android) | $50,000 – $100,000 | $120,000 – $300,000 |

| Backend Services (per service module) | $20,000 – $50,000 | $30,000 – $80,000 each |

| Mini-App Framework & SDK | N/A | $60,000 – $150,000 |

| Payment & Wallet Integration | $20,000 – $40,000 | $40,000 – $100,000 |

| Admin Panel & Merchant Dashboard | $15,000 – $30,000 | $40,000 – $80,000 |

| QA & Security Testing | $15,000 – $30,000 | $40,000 – $100,000 |

| DevOps & Cloud Infrastructure Setup | $10,000 – $25,000 | $30,000 – $80,000 |

| Total | $150K – $350K | $500K – $1.5M |

♦ Development Cost by Region

| Region | Hourly Rate Range | Full Build Estimate | Notes |

| United States | $150 – $250/hr | $2M – $5M+ | Highest quality, highest cost |

| United Kingdom | $120 – $200/hr | $1.5M – $4M | Strong fintech expertise |

| UAE / Middle East | $80 – $150/hr | $800K – $2M | Growing tech talent pool |

| Eastern Europe | $50 – $100/hr | $500K – $1.5M | Strong engineering, good timezone overlap |

| India | $25 – $60/hr | $250K – $800K | Large talent pool; requires strong PM oversight |

| Southeast Asia | $30 – $70/hr | $300K – $900K | Deep super app domain expertise |

♦ MVP vs Full Build: What You Actually Get

| Feature | MVP | Full Super App |

| Number of services | 1–2 | 5–10+ |

| Mini-app ecosystem | No | Yes |

| Financial services layer | Basic wallet | Full lending, insurance, and investment |

| Third-party developer SDK | No | Yes |

| Multi-market support | Single market | Multi-market |

| Real-time analytics dashboard | Basic | Advanced |

| White-label capability | No | Optional |

| Estimated MAU capacity | Up to 100K | 1M+ |

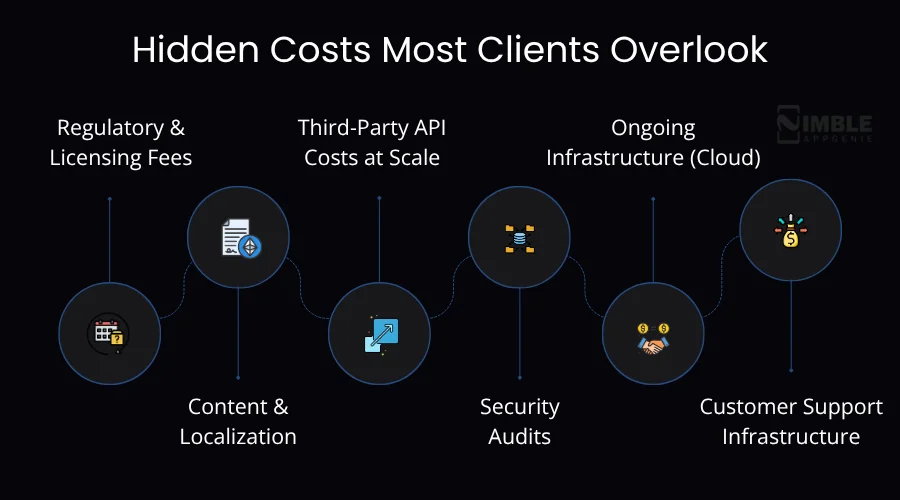

♦ Hidden Costs Most Clients Overlook

1. Regulatory & Licensing Fees

Financial services licenses in regulated markets (UK, US, UAE, and Singapore) cost $50,000–$500,000+ in fees, compliance infrastructure, and legal work before you launch a single financial product.

2. Content & Localization

Culturally adapting, legally reviewing, and translating your app for each new market costs $30,000–$100,000 per market.

3. Third-Party API Costs at Scale

KYC verification services, SMS gateways, payment processing, and Google Maps fees add up. Budget $0.10–$0.50 per active user per month for infrastructure APIs at scale.

4. Security Audits

SOC2 compliance, PCI-DSS certification, and penetration testing are needed for financial service components. Budget $30,000–$80,000 per audit cycle.

5. Ongoing Infrastructure (Cloud)

Cloud costs for a super app expand non-linearly. Budget 15%-25% of your initial development cost yearly for cloud infrastructure.

6. Customer Support Infrastructure

At scale, support costs for a multi-service platform are 3-5x those of single-service apps.

Build vs. Buy: Should You Build Custom or Start With a White-Label Super App?

Every founder evaluating super app development eventually asks this. There’s no universally right answer – it relies on how proprietary your service mix and market positioning actually need to be.

| Factor | Custom Build | White-Label / Pre-Built |

| Time to launch | 4–18 months | 4–10 weeks |

| Upfront cost | $150K–$5M+ | $15K–$80K typically |

| Source code ownership | Full | Varies by vendor – confirm before signing |

| Differentiation ceiling | None – build anything | Limited to the vendor’s module set |

| Regulatory flexibility | Full control over compliance architecture | Constrained by the vendor’s existing licensing setup |

| Best for | Funded startups, enterprises, and regulated fintech plays | Validating demand fast, bootstrapped founders, single-market launches |

A genuine framework: If your edge is the service mix and the brand, white-label can get you to market and validate demand without burning your seed round. If your edge is the architecture – a proprietary mini-app SDK, a regulated financial layer, or a data moat you plan to defend for a decade – custom is the only way, because a white-label platform’s source code is shared infrastructure that other founders are running too.

Most clients who come to us evaluating white-label have already hit their ceiling: they validated demand, then required financial services licensing or a mini-app ecosystem that the off-the-shelf platform can’t support. If that’s where you are, a scoping call will inform you in 30 minutes whether you have outgrown white-label or whether it can still carry you for another 12 months.

What are the Challenges of Super App Development & How to Actually Solve Them

When it comes to super app development, various specifications you should consider to avoid problems coming your way.

Below are common mobile app development challenges you face while building super apps, with possible solutions to beat them.

1. Architecture Debt From Moving Too Fast

The Problem: Teams release a monolithic backend to move swiftly, then face an expensive and risky situation when they demand to scale or add services.

The Solution: From the start, invest in microservices and a microservices architecture, even if your initial service count is small. Utilize an API gateway and well-defined service boundaries. The upfront cost is 20-30% higher, but saves 200%-400% in the replatforming costs layer.

2. Building a Mini-App Ecosystem With No Developers

The Problem: A mini-app framework is of no use without developer adoption.

The Solution: Launch with 5-10 first parity mini-apps created by your team to showcase the framework’s capabilities. Provide zero-commission periods (6-12 months) to early third-party developers. Invest in SDKs, developer documentation, and direct outreach to SMBs in your target verticals.

3. Payment Regulation Varies by Market

The Problem: What’s acceptable in Singapore (MAS licensing) differs from India (RBI), the UAE (CBUAE), the US (FinCEN), and the UK (FCA). Various super apps have rolled out financial products and have been compelled to shut them down due to non-compliance.

The Solution: Hire a regulatory counsel for each target market before creating financial features, not later. In the early days, engage regulators – various central banks (specifically Singapore, the UAE, and the UK) have sandbox programs, particularly for super app models.

4. UX Complexity at Scale

The Problem: With services getting multiplied, the app becomes tough to navigate. Users feel overwhelmed, and engagement with secondary services goes down.

The Solution: Implement personalized app shells that bring the most relevant services to the front per user based on their behavioral data. Utilize bottom navigation for anchor services (3 to 5 max), and demote everything else to a discoverable service directory. Study Grab and WeChat’s navigation architecture meticulously.

For a full breakdown of navigation patterns, clutter reduction, and accessibility standards for super app interfaces, see our dedicated Super App Design Principles guide.

5. Multi-Side Network Effects Are Hard to Bootstrap

The Problem: Super apps need merchant/service providers, mini-app developers, and users simultaneously. Each side waits for the others.

The Solution: Leverage your robust existing asset to hold one side. If you have merchant relationships, use them. If you have consumer traffic, monetize it for merchants. In the launch phase, subsidize the supply side aggressively.

What are the Top Super Apps to Learn From (With Lessons)?

Various super apps worldwide, like Gojek, WeChat, AliPay, and Grab, have ruled by combining finance, messaging, and logistics into a unified ecosystem to drive enormous user engagement.

Let’s get deeper to unveil the names and the lessons you should learn before you start with super app development.

1. Gojek

Origin: Indonesian motorcycle taxi booking service (2010), Gojek evolved into a complete on-demand super app with 20+ services across Southeast Asia.

Scale: 190M users; operations across Vietnam, Singapore, and Thailand; valued at $10B+.

What made it win: Gojek was created for the infrastructure limitations of Southeast Asian cities – underbanked populations, traffic congestion, and cash-dependent economies. It didn’t copy WeChat; it resolved local issues with a super app model. Its driver-partner ecosystem became the logistics support for everything.

Key Takeaway for builders: Market-focused super apps beat generic ones. Understand payment behavior and infrastructure of your target market before crafting your service.

2. WeChat

Origin: Messaging app launched by Tencent in 2011, WeChat became the world’s first real super app by adding payments (WeChat Pay), then rolled out the mini-program ecosystem in 2017.

Scale: 400< daily mini-program users; 1.3 billion monthly active users; $250B+ in annual payments volume.

What made it win: WeChat didn’t fight for market share – it created the market. By owning the Chinese consumers’ communication layer, it has an indisputable distribution channel for each service it adds. The mini-app ecosystem expanded the platform to 4M+ mini-programs without any proportional headcount.

Key takeaway for builders: First, own a high-frequency communication or payment channel. Rest, you can layer on top later also. Avoid changing commission too early – WeChat’s zero-commission mini-app strategy was the smartest expansion move in tech history.

3. Careem

Origin: Dubai-based ride-hailing service (2012), Careem was acquired by Uber for $3.1B in 2019, then reprocessed to create an independent super app for the MENA region.

Scale: Operations in 13+ countries across the Middle East, North Africa, and South Asia.

What made it win: Careem realized that the MENA market is underserved by the world’s tech platforms. It is deeply localized – Arabic-first UX, prayer time awareness in driver algorithms, and cash payment options. After re-independence from Uber, it extensively expanded into Careem Pay, food delivery, and grocery delivery.

Key takeaway for builders: Regional super apps outshine global ones on cultural intelligence. If you are developing a super app for an emerging market, mobile app localization is your competitive moat, more than a nice-to-have.

4. Grab

Origin: Malaysian ride-hailing app (2012), Grab became the leading super app across Southeast Asia after acquiring Uber’s regional operations in 2018.

Scale: Operations in 8 countries; GrabPay processed billions in transactions annually; $40B valuation at IPO.

What made it win: When Grab acquired Uber’s APAC business, it was the crucial moment when it got the chance to justify a payment infrastructure investment. It then empowered GrabFood, GrabFinance, GrabHealth, and GrabMart. The lesson: strategic M&A can compress 3 to 5 years of organic growth.

Key takeaway for builders: Payments are an important point. Once you regulate a market’s payment rails, each adjacent service becomes notably easier to monetize and scale.

5. Alipay

Origin: Escrow payment service for Alibaba’s Taobao marketplace (2004), Alipay became China’s ruling digital wallet, and then emerged as a complete financial super app.

Scale: 1 billion+ users; Ant Group, the parent company, handles trillions in assets; Alipay processes more annual transactions than Mastercard and Visa combined.

What made it win: Alipay solved a trust issue – early Chinese e-commerce buyers didn’t trust sellers. Alipay fostered the trust layer by holding payment in escrow until confirmed delivery, which opened the door wide open for Chinese eCommerce. That trust, simulated at scale, became the basis for Yu’ebao (China’s largest money market fund, built inside Alipay), lending products, and the complete financial ecosystem.

Key takeaway for builders: The deepest super apps are created on the trust infrastructure. If you can solve a basic trust problem in your market, you earn the right to scale into financial services.

➤ Summary: What Made Them All Win

| Super App | Origin Advantage | Super App Catalyst | Defining Moat |

| Communication monopoly | WeChat Pay + Mini-programs | Distribution of Chinese internet life | |

| Gojek | Logistics network | GoPayment + GoPay wallet | Physical driver network in underserved markets |

| Grab | Ride-hailing dominance | Uber APAC acquisition | Regional payment infrastructure |

| Careem | MENA localization | Careem Pay | Cultural and operational depth in MENA |

| Alipay | E-commerce trust layer | Yu’ebao + lending | Financial data and trust at scale |

The common thread: Each winning super app started by solving one particular, high-frequency problem better than anyone else, then leveraged that daily touchpoint to expand into payments, then into a full ecosystem.

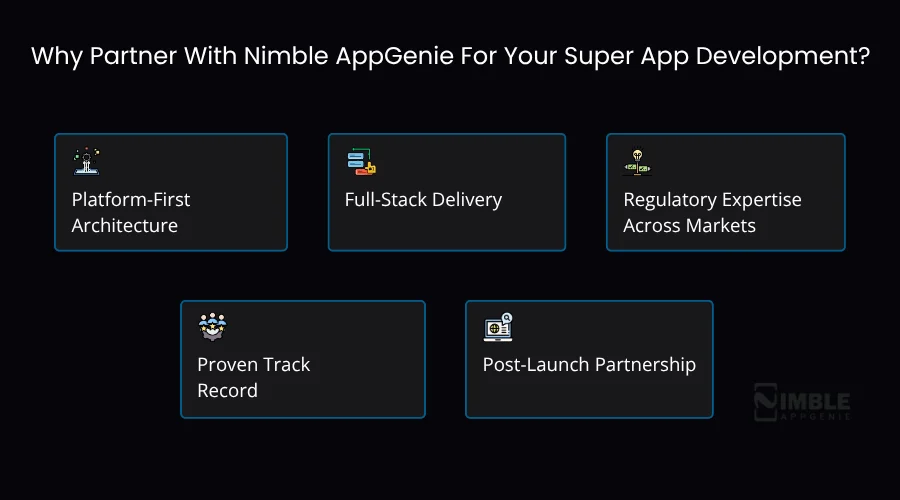

Why Partner With Nimble AppGenie For Your Super App Development?

Nimble AppGenie specializes in building super apps with deep proficiency in creating multi-service digital ecosystems for funded startups, enterprises, and government entities.

Super app development is not a feature project; it’s a platform investment that will define the competitive position of your company for the next decade. The super app development company you choose for this build should be a direct determinant of your success.

Here’s what it means practically:

► Platform-First Architecture

We design for the complete super app vision from day one, not an MVP that needs to be rebuilt later at Series B. We test microservices architecture and mini-app framework at production scale.

► Full-Stack Delivery

From product strategy and UX research through mobile development, backend engineering, DevOps, QA, and launch – we cover the comprehensive build without the coordination expenses of multi-vendor arrangements.

► Regulatory Expertise Across Markets

We have in-house knowledge of fintech licensing needs in the UK, UAE, Southeast Asia, the US, and India – the markets where the super app opportunity is highest in 2026.

► Proven Track Record

Our portfolio involves on-demand super apps, marketplace ecosystems, and fintech platforms serving millions of users across the Middle East, South Asia, and Southeast Asia.

You can review specific outcomes in our case studies.

► Post-Launch Partnership

Super apps don’t end at launch. We offer ongoing engineering support, ecosystem development, and product iteration as your product grows.

If you are evaluating super app development and want a technical and strategic partner who has done this before, we should talk.

How to Choose a Super App Development Company: 7-Point Checklist

The wrong technical partner on a super app build doesn’t just cost money; it costs the 12-18 months you needed to beat a competitor to market.

Before you sign with anyone, confirm these seven things:

- Have they shipped a mini-app ecosystem before, not just a multi-feature app?

Ask for the SDK documentation or a live third-party integration example. Most agencies have built “apps with many features,” but far fewer have built a real third-party developer platform.

- Do they have in-house regulatory knowledge for your target market’s financial licensing?

If the answer is “we will bring in a consultant,” budget extra time and expect coordination friction.

- Will they show you their microservices architecture diagram before you sign?

If a vendor can’t whiteboard the API gateway, event layer, and service boundaries on a call, they are going to build you a monolith with microservices branding.

- What is their post-launch model?

Super apps need continuous service additions and ecosystem growth. A vendor optimized for “ship and walk away” is the wrong fit.

- Can they show a reference client in a comparable region or vertical?

Generic portfolio examples don’t tell you whether they understand your market’s payment behavior and regulatory environment.

- Do they separate MVP scope from full-platform scope clearly in the proposal?

Vague scoping is the #1 cause of the 30-40% timeline overruns that founders report industry-wide.

- Who owns the IP and source code?

Get this in writing before the first invoice, not after the MVP ships.

If you want a second opinion on a proposal you have already received, or you are starting from zero, a free scoping call will give you a cost range and an architecture outline specific to your service mix, no commitment required.

Conclusion

The window to build a super app is open, but not forever.

The platforms that will outshine in the next decade will be those that start today with a high-frequency service advantage, open an ecosystem for third-party developers, create a safe payment and identity layer, and put financial services on top.

The businesses executing the same sequence well create infrastructure. The ones that try to combine it later become acquisition targets.

So, the market is proven, the technology is available, and the monetization models are developed. The question is whether your company has the confidence to start with super app development now – before your competitors enter.

If this guide has helped clear up your thoughts, the next step is a technical scoping session with our skilled mobile app development team, who hold the expertise in creating such platforms for worldwide clientele.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.