Banking Software Development

Banking Software Development Payroll Software Development

Payroll Software Development Our Work Process

Our Work Process Awards

Awards

Key Takeaways:

- Legacy AML systems generate 85–95% false positives, creating major compliance costs.

- Hybrid AML monitoring (Rules + ML) is the industry standard for reducing false alerts while improving detection.

- AML transaction monitoring systems typically cost $50K–$500K+ to build, depending on scope.

- The biggest long-term expense is alert investigation and compliance operations, not development.

- Effective AML systems require customer risk segmentation, sanctions screening, audit trails, and analyst feedback loops.

- Off-the-shelf solutions can support early-stage fintechs, but growing platforms often need custom-built monitoring.

- Building compliance infrastructure correctly from day one helps avoid costly rework and regulatory issues later.

- Nimble AppGenie builds AML monitoring solutions with compliance-first architecture, hybrid detection models, and audit-ready workflows to help fintechs scale securely and meet regulatory requirements from day one.

An AML transaction monitoring system is software that scans every customer transaction for signs of money laundering and flags suspicious activity for a compliance team to review.

Most fintech companies need a transaction monitoring system before they can legally move money in the US, UK, and EU. Building one can cost anywhere from $50,000 for a basic setup to $500,000+ for a full enterprise-grade system.

This guide includes a part nobody tells founders upfront: most of these systems, once live, generate far more noise than signal. The majority of alerts your compliance team investigates turn out to be nothing, and that’s not a minor bug; it’s a default result of how most AML systems are developed. But, not to fret, it’s fixable if you know what to create uniquely from day one.

Scoping this for your team? Check this.

If you are researching this for a compliance review or an internal build decision, below has three bullet points:

- Legacy rule-based AML monitoring generates 85-95% false positives, costing the fintech industry over $200 billion annually in wasted investigative time.

- Hybrid systems (rules plus machine learning) cut that by up to 80% and are now the new build standards.

- A custom hybrid system for a mid-size fintech usually runs $120,000-$300,000 and takes 5-8 months to develop.

Read the blog for a complete breakdown and the engineering details.

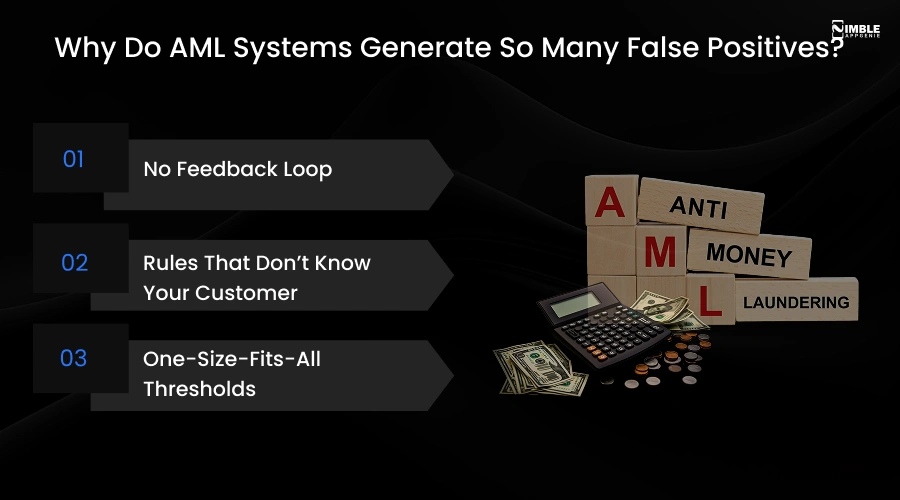

Why Do AML Systems Generate So Many False Positives?

Most fintech founders ask this question once their system is live, and the honest answer is awkward. Most AML monitoring systems are developed on one-size-fits-all rules. A rule might say, “Flag any transaction over $10,000.” That rule doesn’t distinguish between a small business owner making a routine payroll transfer and a money laundering structuring deposits. Both eat up an analyst’s time.

Industry research shows legacy rule-based systems produce false positive rates between 85% and 95%. That means out of every 100 alerts your compliance team investigates, somewhere between 85 and 95% turn out to be nothing. Across the industry, this wasted investigation time is predicted to cost financial institutions over $200 billion a year.

This is one of the biggest reasons AML projects go over budget after launch. The build cost is not the real expense. The ongoing cost of the compliance team drowning in false alerts is.

Choosing the right AML monitoring system from the start is what determines whether your compliance team spends their time on real threats or chasing noise.

The three usual culprits behind high false positive rates-

1. No Feedback Loop

When an analyst closes an alert as “not suspicious”, that information should retrain the system. Most legacy setups never feed that decision back in, so the same bad alert pattern repeats endlessly.

2. Rules That Don’t Know Your Customer

A $50,000 transfer is suspicious for a freelancer, entirely normal for an import-export business. Static rules can’t distinguish between them.

3. One-Size-Fits-All Thresholds

Leveraging the same trigger amount for a high-volume B2B platform and a small consumer wallet app ensures the consumer app gets buried in noise.

What Does It Cost to Build an AML Transaction Monitoring System?

Below is a realistic breakdown of the building AML transaction monitoring system cost in 2026.

| Scope | Approximate Cost | What It Covers |

| Basic rules-based system | $50,000 – $120,000 | Core threshold rules, basic alerting, and manual case review |

| Hybrid system (rules + ML) | $120,000 – $300,000 | Behavioral risk scoring, sanctions screening integration, and case management workflow |

| Enterprise-grade system | $300,000 – $500,000+ | Multi-jurisdiction rules, real-time monitoring, graph-based entity analysis, full audit infrastructure |

Transaction monitoring for neobanks typically sits in the hybrid tier, since a digital-first customer base with varied transaction patterns quickly exposes the limits of a rules-only system.

These numbers cover the build itself. They don’t cover the ongoing cost of compliance staff to review alerts, the cost of tuning thresholds as your transaction patterns evolve, and periodic independent model validation that regulators expect. Budget for those as recurring costs, not one-time line items.

► Build vs. Buy Transaction Monitoring: Which Makes Sense For You?

Off-the-shelf AML platforms exist and can get you compliant faster if you run a small operation with simple, low-volume transaction flows. But most growing fintechs outgrow them quickly, because generic platforms can’t be tuned to your specific customer base, your specific transaction patterns, and your specific risk profile, which is exactly what drives those false positive rates down.

A custom-built system costs more upfront but is the only path to genuinely low false positive rates at scale, because it’s calibrated to how your actual customers behave, not a generic template.

Most off-the-shelf AML transaction monitoring solutions are built for average transaction profiles, which is exactly why they underperform once your platform develops its own distinct customer behavior patterns.

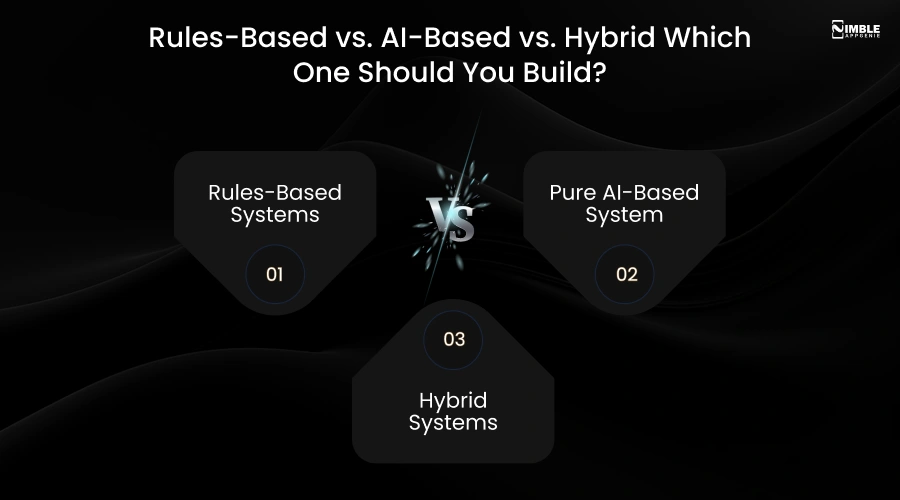

Rules-Based vs. AI-Based vs. Hybrid: Which One Should You Build?

Founders usually ask whether they should create a rules-based system, an AI-based one, or pay for a third-party platform.

Below is the genuine comparison:

► Rules-Based Systems

These are simple to explain to regulators and reasonable to build, but they are the systems generating that 85-95% false positive rate we just covered. They work perfectly for very small, very simple platforms in their first year of operation. They stop working once you have real transaction volume.

► Pure AI-Based System

These systems learn customer behavior patterns over time and detect things rules miss completely, like a customer’s spending unexpectedly shifting in a way that doesn’t follow any predefined rule. The issue is that they are challenging to explain to a regulator. If a model flags something and nobody can clearly say why, that’s a real audit risk.

► Hybrid Systems

Hybrid systems use rules for clear-cut, well-understood red flags and machine learning for subtler behavioral patterns, which almost every serious fintech institution is moving toward in 2026.

Production deployments using hybrid architecture report reducing false positives by 50% to 80% compared to rules-only systems, while catching more suspicious activity, not less. That is not a compromise between fewer false alarms and weaker detection. If done right, you get both.

Most serious AML transaction monitoring software built in 2026 uses this hybrid approach as its baseline, not as a premium tier. If you are building an AML transaction monitoring software today, hybrid is the right starting point, not an upgrade you bolt on two years from now.

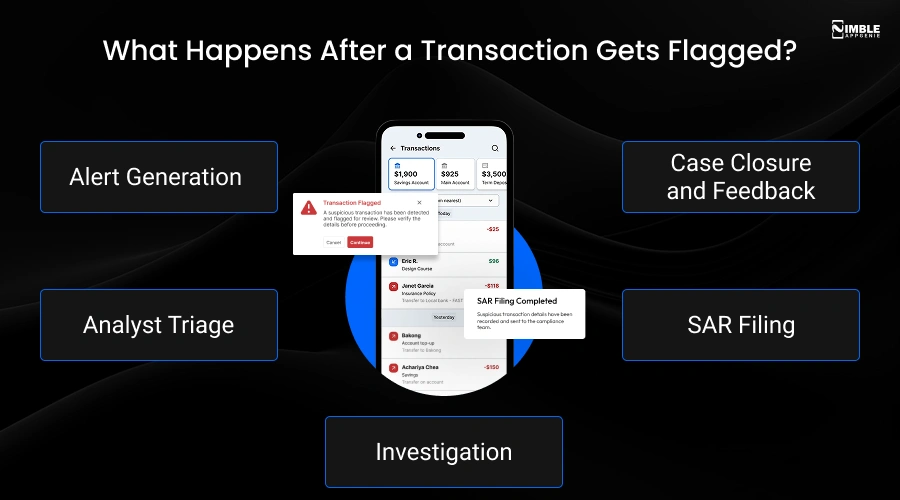

What Happens After a Transaction Gets Flagged?

Understanding this workflow holds significance because it molds what your system actually demands to do, not just detect.

♦ Alert Generation

The system flags a transaction or pattern and assigns it a risk score.

♦ Analyst Triage

A compliance analyst reviews the alert, generally within a set time window needed by regulation, and decides if it needs in-depth investigation.

♦ Investigation

If it looks really suspicious, an investigator gets deeper into the customer’s full account history, relevant accounts, and any previous alerts.

♦ SAR Filing

If the investigation confirms suspicious activity, the company files a SAR with FinCEN with a complete record of why the decision was made. US financial institutions filed 4.7 million SARs with FinCEN in fiscal year 2024, up 51.8% from 2020, at an average of 12,870 per day. Only around 4% of those SARs receive any law enforcement follow-up, which is why SAR quality matters as much as SAR volume when building your monitoring workflow.

♦ Case Closure and Feedback

Whatever the result, that decision should flow back into the system to improve future detection.

A system that just conducts step one, generating alerts, is not actually finished. The case management, audit trail, and feedback loop around that alert are only as essential as the detection logic itself, and they are usually the part that founders forget to budget for.

What Your Development Partner Needs to Get Right From Day One?

If you are evaluating a team to build AML transaction monitoring systems, the following pointers will separate a system that works from one that becomes a compliance issue within six months.

➤ An Audit Trail For Every Single Decision

Regulators will ultimately ask why a specific transaction was not flagged or why one was cleared. If your system can’t show its work, that’s an actual examination risk.

➤ Customer Risk Segmentation Built in From the Start

A B2B payments platform and a consumer wallet app should not run the same thresholds. This should be a base design decision, not a future patch.

➤ Sanctions Screening Wired in From Launch

Real-time checks against OFSI, OFAC, and EU sanctions lists should be part of the core architecture, not an add-on integrated later under deadline pressure.

➤ A Feedback Loop Between Analyst Decisions and the Detection Model

Without this, your false positive rate never improves, no matter how sophisticated the initial model is.

➤ Room to Add Machine Learning Later, Even if You Launch Rules-Only

Most fintech institutions start with a rule-based MVP to get compliance fast, then layer in behavioral modeling once they have real transaction history to train on. That just works if the underlying architecture was developed to support it from day one.

Moving to a hybrid model with proper customer risk segmentation reduced that into the 30-40% range within the first few months of live data, without impacting genuine detection. That gap, between a system that technically works and one your compliance team can actually live with, is completely about these five decisions being precisely at the start.

The difference between AML monitoring software that passes an examination and one that embarrasses you during one comes down to these five decisions being made before a line of code is written.

How Nimble AppGenie Can Help?

Building an AML transaction monitoring system is not only a compliance checkbox, but it’s also a piece of major infrastructure that has to perform alongside your ledger, your KYC and AML compliance flow, and your entire product architecture from day one.

AML compliance software development is one of the most specification-sensitive builds in fintech, where the gap between what you scoped and what regulators actually expect shows up fast, and usually at the worst possible moment.

That’s exactly the sort of build we focus on as part of our broader fintech app development work.

We design transaction monitoring systems with sanctions screening, customer risk segmentation, and audit trails built in from the start, not added later after a regulator asks for them. If you are also working through licensing, our guide on the money transmitter license process covers how that timeline should run alongside your compliance build.

If you are scoping a build and want a realistic timeline and cost for your specific transaction volume and risk profile, talk to our team. We will tell you honestly what you need now and what can wait.

The Bottom Line

A high false positive rate is not something you fix later; it’s something you avoid by getting the architecture right from the beginning. Rules alone won’t get you there. A hybrid system, created with customer segmentation, sanctions screening, and a real feedback loop from day one, is a monitoring system your compliance team can actually live with. Budget for it accordingly, build it that way the first time, and you won’t be rebuilding it eighteen months from now.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.