In a Nutshell

- Loan origination software (LOS) automates the entire lending journey, from borrower application to loan disbursement in minutes, not days.

- Must-have features include digital onboarding, automated credit scoring, KYC/AML automation, AI-powered decisioning, and real-time analytics.

- Custom LOS development costs range from $20,000 for an MVP to $200,000+ for an enterprise platform.

- Building custom beats off-the-shelf for any FinTech startup planning to scale beyond 1,000 applications per month.

- A production-ready LOS takes 3 to 4 months for an MVP and 10 to 16 months for a full enterprise build.

- Compliance is not optional – KYC, AML, GDPR, and market-specific regulations must be built in from day one, not updated later.

The global loan origination software market is expected to expand from $4.16 billion in 2026 to $7.44 billion by 2034. The startups that are capitalizing on the growth aren’t opting for off-the-shelf tools; instead, they are building smarter.

A decade ago, processing a loan application meant manual credit checks, paperwork, and days of back-and-forth. Today, a well-crafted loan origination software (LOS) takes borrowers 10 minutes from application to approval, fully compliant, fully automated, and fully branded.

But here the problem is that most FinTech startups face challenges. Either they settle for generic software that’s inappropriate to their loan product, or they try to build one without a clear roadmap and go over budget before launch.

This guide solves both problems.

Whether you are building a personal lending app, an SME credit platform, or a BNPL solution, here you will get a complete breakdown of what loan origination software is, what it costs to build one, which features actually matter in 2026, and exactly how to go from idea to a compliant LOS.

Let’s build it right.

What is Loan Origination Software (LOS)?

Loan origination software is a digital platform that automates and manages the whole process of creating a new loan, from the point a borrower submits an application to the point the loan is approved and funded.

Think of it as the engine powering every lending decision your startup makes. A well-developed LOS handles everything, freeing your team from manually reviewing applications, managing documents, and running credit checks all accurately, automatically, and at scale.

A loan origination system is designed to automate and simplify the steps needed to process and approve a loan application, diminishing turnaround times, minimizing human error, and improving borrower satisfaction.

For FinTech startups, this holds more significance. Whether you are offering SME credit, personal loans, mortgage products, or BNPL, your LOS is the chief infrastructure that decides how compliant you stay, how fast you can lend, and how well your borrower experience holds up at scale.

Loan Origination Software vs Loan Management Software (LMS) – Key Differences

People usually get confused with these two terms; let’s analyze.

LOS applies before the loan is funded. LMS applies after.

A Loan Origination System manages the initiation of the loan process – application and approval, while a Loan Management System handles the loan after it’s funded, repayment schedules, tracking payments, and borrower communication.

Here’s the LOS vs LMS difference – a quick comparison:

| LOS | LMS | |

| Focus | Pre-disbursement | Post-disbursement |

| Key functions | Application, underwriting, and approval | Repayment tracking, collections, servicing |

| Primary users | Loan officers and underwriters | Servicing teams and collections staff |

| When it runs | Before the loan is funded | After the loan is funded |

| Goal | Fast, compliant lending decisions | Smooth repayment and borrower retention |

Initially, various fintech startups implement only a LOS with the target of customer acquisition. However, without a robust LMS, servicing becomes broken, which increases default risks and hinders customer support.

Also, it’s not like you should worry about servicing loans before they even originate.

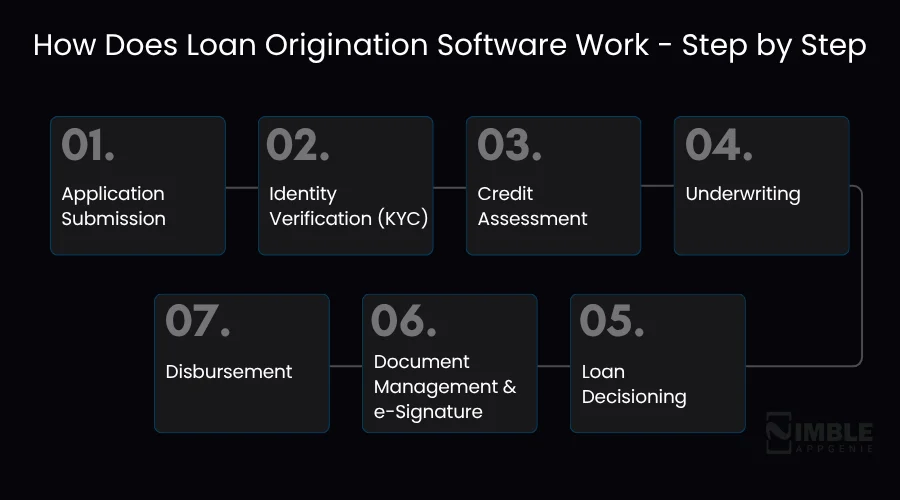

How Does Loan Origination Software Work – Step by Step

Before you build a loan origination software, you should understand its flow.

Below is what a modern loan origination process looks like

- Application Submission: Borrower fills out a digital application and uploads required documents.

- Identity Verification (KYC): System verifies the borrower’s identity and screens for AML compliance.

- Credit Assessment: Automated credit scoring pulls data from bureaus and assesses risk profile.

- Underwriting: System estimates eligibility based on predefined rules and risk models.

- Loan Decisioning: Approval, rejection, or counteroffer is generated automatically.

- Document Management & e-Signature: The loan agreement is sent, signed, and stored digitally.

- Disbursement: The approved loan amount is transferred to the borrower’s account.

When done manually, these steps can take days, but with a well-crafted LOS, they take minutes.

Why FinTech Startups Need a Dedicated LOS in 2026

Most startups see off-the-shelf lending software faster and cheaper. But, you should know, they almost always create hurdles as you scale.

On the contrary, with LOS tools, lenders can mitigate turnaround times by up to 80% and raise loan capacity by 3 to 5 times without hiring more staff.

These numbers showcase a direct competitive advantage in a market where borrowers prefer lenders that approve them faster.

Apart from speed, a dedicated LOS that’s developed for your specific loan product:

- Reduce customer drop-offs by around 40% through rapid decisions.

- Compliance flexibility to meet regulations across different markets

- Decrease error rates from 5 to 7% to under 0.5%, removing expensive correction cycles.

- Offers you scalability to manage 100 applications or 100,000 without rebuilding your stack

- Reduce processing cost through automation and digitization by 40-60% per loan.

- Provide full control over your underwriting logic and risk models.

Generic software doesn’t offer such benefits, but a custom-built LOS offers all, and this is where Fintech startups are ruling in 2026.

Types of Loan Origination Software

Not all LOS platforms are built the same; the type you want depends completely on your lending product and target borrower.

Here are the main types:

| Type | Best For | Key Characteristics |

| Consumer Lending LOS | Personal loans, salary advances, and credit lines | High application volume, fast decisioning, and simple eligibility criteria |

| SME / Business Lending LOS | Small business loans, working capital, and invoice financing | Complex underwriting, financial statement analysis, and longer approval cycles |

| Mortgage LOS | Home loans, property financing | Multi-stage workflows, heavy documentation, and strict regulatory compliance |

| BNPL LOS | Buy Now Pay Later, point-of-sale credit | Real-time decisioning, micro-ticket sizes, and merchant integrations |

| Microfinance LOS | Micro-loans, rural lending, and financial inclusion | Lightweight KYC, alternative credit scoring, and low-cost infrastructure |

| P2P Lending LOS | Peer-to-peer lending platforms | Borrower-lender matching engine, investor management, and risk pooling |

Most fintech startups launch with only one type and expand into others as they grow. Your LOS architecture must support that expansion from day one, which is why developing modular matters.

Benefits of Loan Origination Software for FinTech Startups

A well-developed loan origination system doesn’t just automate your lending process, but basically changes how competitive your fintech startup can be.

Below is what the right LOS unlocks for a FinTech startup in 2026:

| Benefits | What It Means for Your Startup |

| Faster loan processing | Reduce application-to-approval time from days to minutes, giving you a direct edge over traditional lenders |

| Lower operational costs | Automation replaces manual underwriting, document chasing, and data entry, cutting overhead significantly |

| Reduced default risk | AI-powered credit scoring and risk assessment catch bad loans before they are approved |

| Scalability | Handle 100 or 100,000 applications without adding headcount or rebuilding your stack |

| Regulatory compliance | Built-in KYC, AML, and audit trails keep you compliant across every market you operate in |

| Better borrower experience | A frictionless digital application flow increases conversion and borrower retention |

| Data-driven decisions | Real-time analytics and portfolio dashboards give you actionable insight into your lending performance |

| Competitive advantage | Lend faster, smarter, and more safely than competitors, who still rely on manual processes. |

Must-Have Features of Loan Origination Software in 2026

LOS platforms are not built equally, and not all the features matter equally to a fintech startup.

Your goal is not to develop a feature-heavy system, but to create the right features for your loan product, the market you are entering, and your borrowers.

Here are the loan origination software features you should consider in 2026:

| Features | What It Does | Why It Matters for Startups |

| Digital Borrower Onboarding | Mobile-friendly application portal with a multi-step form and document upload | First impression of your product – friction here kills conversions |

| Automated Credit Scoring | Pulls bureau data and alternative sources to score borrowers instantly | Replaces slow manual underwriting – scales with your loan volume |

| KYC / AML Automation | Verifies identity, screens watchlists, flags suspicious activity | Keeps you compliant without slowing down your application flow |

| Document Management & e-Signature | Requests, validates, and stores documents – fully paperless | Cuts loan turnaround from days to minutes |

| AI-Powered Loan Decisioning | Analyzes behavioral and alternative data for smarter approvals | Gets more accurate with every loan you originate |

| Third-Party API Integrations | Connects to credit bureaus, payment gateways, and core banking | Plug in best-in-class tools without rebuilding your stack |

| Real-Time Reporting & Analytics | Full visibility over pipeline, approvals, defaults, and portfolio health | Helps founders and investors make data-driven lending decisions |

| Multi-Product Support | Handles personal loans, SME, BNPL, and mortgages in one platform | Let’s you expand loan products without rebuilding your system |

Build vs Buy Loan Origination Software – What’s Right for Your FinTech Startup?

Every lending startup looks for an answer to this question before they move ahead to development.

Off-the-shelf loan origination software is rapid to deploy, whereas a custom-built LOS is faster to expand.

It is an expensive mistake to choose the inaccurate one at this stage.

Let’s have an unbiased breakdown of both:

Off-the-Shelf LOS – Pros & Cons

Ready-made, top loan origination systems such as LendFoundry, Turnkey Lender, or Nucleus Software offer an out-of-the-box working system.

This can be a valid starting point for startups demanding a quick launch and validating their loan product.

But the limitations arise fast.

| Pros | Cons |

| Fast to deploy (weeks, not months) | Limited customization for your loan product |

| Lower upfront cost | Monthly licensing fees add up quickly |

| Vendor handles maintenance | You depend on their roadmap, not yours |

| Built-in compliance for standard products | Poor fit for niche or innovative loan products |

| Good for MVP validation | Hard to differentiate your borrower experience |

Custom Loan Origination Software – Pros & Cons

A custom LOS development means you have all the essentials – the logic, data, experience, and roadmap.

This is mostly the right lasting move for fintech startups with a unique lending product.

| Pros | Cons |

| Built exactly for your loan product | Higher upfront development cost |

| Full control over underwriting logic | Longer time to first launch |

| Unique borrower experience | Requires a reliable development partner |

| No recurring licensing fees | Ongoing maintenance responsibility |

| Scales without platform restrictions | Needs clear product requirements upfront |

When Does Building Custom Make Business Sense?

When you are testing a loan product and want something to live fast, an off-the-shelf solution works.

Custom is the right call when:

| Situation | Go Custom? |

| Your loan product has unique eligibility criteria or risk models | Yes |

| You are operating in a regulated market with specific compliance needs | Yes |

| You plan to scale to thousands of applications within 12-18 months | Yes |

| Your borrower experience is a core part of your competitive advantage | Yes |

| You have raised funding and need infrastructure built for long-term growth | Yes |

| You are still validating your loan product and need something live fast | Not yet – start with off-the-shelf |

| You have a very limited budget and no clear product-market fit | Not yet – validate first |

Note: Most fintech startups that begin with off-the-shelf software end up redeveloping custom within two years anyhow, after exceeding the platform’s limitations. Custom loan origination software development from the start with the right development partner saves you from that costly turn.

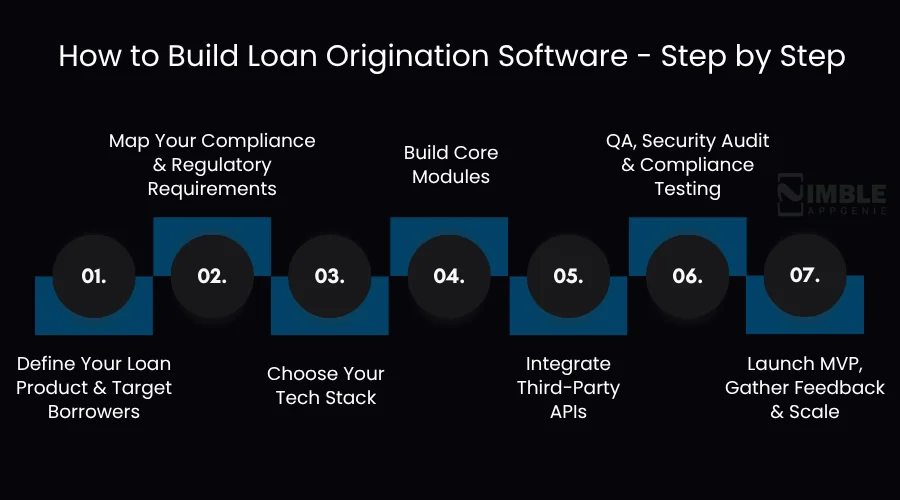

How to Build Loan Origination Software – Step by Step

Developing a loan origination system is actually a product decision, not only a development project.

Every choice you make here, from a compliance framework to a tech stack, directly impacts the lending speed, scaling safety, and maintenance costs.

Here is the exact process, step by step.

Step 1: Define Your Loan Product & Target Borrowers

Before you start writing the code, you need ultimate clarity on what you are creating and who you are building it for.

The answers to these questions structure every technical decision that follows.

Ask yourself:

- What type of loan are you offering – personal, SME, BNPL, mortgage, or microfinance?

- Who is your target borrower – salaried employees, self-employed individuals, or small businesses?

- What is your average loan size, tenure, and repayment structure?

- What markets are you launching in, and what regulations apply?

A personal lending application for salaried borrowers demands a very unique LOS compared to an SME credit platform created for small business owners.

You should get this clarity in advance, and your complete development becomes cheaper, faster, and more focused.

Step 2: Map Your Compliance & Regulatory Requirements

Worldwide, lending is one of the most regulated industries, and the compliance needs vary notably by market.

If you skip this step, you should know that the day is not far when your platform will shut down before scaling.

| Region | Key Regulations to Address |

| USA | ECOA, FCRA, TILA, and CFPB guidelines |

| UK | FCA regulations, GDPR, Open Banking, and PSD2 |

| India | RBI digital lending guidelines and KYC norms |

| EU | GDPR, AML Directive, and PSD2 |

| Global | AML, KYC, data privacy, and consumer protection |

Before you finalize your LOS feature list, you should map your loan origination software compliance requirements. Thus, you can determine the integrations you need, the way your data must be stored, and how your audit trail should appear.

Step 3: Choose Your Tech Stack

Your tech stack decides how rapidly your LOS performs, how easily it expands, and how rapidly your team can create and iterate.

Here is what a production-ready LOS stack should look like in 2026:

| Layer | Recommended Tools |

| Frontend | React.js, Angular, Vue.js |

| Backend | Node.js, Python (Django), Java Spring Boot |

| Database | PostgreSQL, MongoDB, Redis |

| Cloud Infrastructure | AWS, Google Cloud, Microsoft Azure |

| APIs & Integrations | Plaid, Stripe, Twilio, Experian, Equifax |

| Security | OAuth 2.0, SSL/TLS, AES-256 Encryption |

| DevOps | Docker, Kubernetes, CI/CD pipelines |

Note: Choose a tech stack your development team understands well and that has robust community support. Switching stacks in the middle is costly and disruptive.

Step 4: Build Core Modules

This stage actually shapes the product.

A loan origination system is created as a sequence of interconnected modules, each managing a particular stage of the lending journey.

Build them in the following order:

- Borrower Application Module: The front-end portal where borrowers apply.

- KYC & identity verification module: Automated ID checks and compliance screening.

- Credit assessment module: Bureau integrations and scoring engine

- Underwriting & decisioning module: Approval logic and risk rules

- Document management module: Collection, validation, and e-signature

- Disbursement module: Payment gateway integration and fund transfer

- Reporting & analytics module: Dashboard and portfolio tracking

Create modularly. Each module should perform independently, so you can replace, update, or scale individual components without interrupting the rest of the system.

Step 5: Integrate Third-Party APIs

No LOS is developed completely from the ground up. The smartest startups leverage the top-class third-party APIs for the heavy lifting – identity verification, credit bureau data, communication, and payment processing.

This considerably reduces your development time and keeps your main team focused on your distinctive lending logic.

Prioritize the below integrations in your first build:

- Credit bureau APIs (Experian, Equifax, CIBIL)

- Open banking APIs (Plaid, TrueLayer)

- KYC/identity verification (Onfido, Jumio)

- Payment gateway (Stripe, Razorpay)

- Communication (Twilio for SMS, SendGrid for email)

Step 6: QA, Security Audit & Compliance Testing

A lending platform that doesn’t pass a security audit or incorrectly processes loans is a liability – legally and reputationally.

Before launch, you should run the following rounds of testing:

- Functional QA – Every feature works as expected across all devices and browsers.

- Security audit – Penetration testing, data encryption validation, and access control review.

- Compliance testing – Verify KYC flows, AML screening, audit trails, and regulatory reporting to meet your market’s requirements.

Conduct this step to save your time, as even a single compliance failure post-launch costs far more compared to thorough testing pre-launch.

Step 7: Launch MVP, Gather Feedback & Scale

Your first version may not be perfect; it’s fine, but it should be compliant, functional, and fast enough to begin originating loans.

Launch your MVP with your core modules live, onboard your first borrowers, and use real data to prioritize what to build next.

The best LOS platforms in 2026 are the ones that launched rapidly, learned quickly, and iterated consistently.

How Much Does It Cost to Build Loan Origination Software?

The cost to build loan origination software ranges between $20,000 to $200,000+, depending on what you create.

A basic MVP LOS created for early validation appears to be distinct from an enterprise-grade platform processing a huge number of applications a day.

Here is a realistic loan origination software cost breakdown across three tiers.

Cost by Development Tier

| Tier | What You Get | Estimated Cost | Timeline |

| MVP / Basic LOS | Core modules – application portal, basic credit scoring, KYC, document management, simple dashboard | $20,000 – $50,000 | 3–4 months |

| Mid-Tier LOS | All MVP features + AI decisioning, advanced underwriting, full API integrations, multi-product support, analytics | $50,000 – $80,000 | 5–8 months |

| Enterprise LOS | Full-scale platform — custom risk models, multi-market compliance, white-label capability, high-volume processing, dedicated infrastructure | $80,000 – $200,000+ | 10–16 months |

Key Factors That Affect Your Development Cost

Two startups can build an LOS with similar feature lists and end with very unique invoices.

Here is what actually drives the custom LOS development cost up or down:

| Factors | Impact on Cost |

| Number of loan products supported | More products = more complex decisioning logic = higher cost |

| Level of AI & automation | Basic rule-based scoring costs less than ML-powered underwriting |

| Number of third-party integrations | Each API integration adds development and testing time |

| Compliance requirements | Multi-market compliance (US + UK + India) is significantly more complex |

| UI/UX complexity | A polished, branded borrower experience costs more than a functional one |

| Development team location | Onshore teams (US, UK) cost more than offshore teams (India, Eastern Europe) |

| Ongoing maintenance & support | Factor in 15–20% of build cost annually for post-launch maintenance |

Bonus Tip: How to Build a High-Quality LOS Without Overspending?

Cost control in LOS development is about building smarter.

Below is how fintech startups constantly get more for less:

- Start with an MVP: First, build the core modules required to originate loans. Next, validate your product in the market before you invest in advanced features like AI decisioning or multi-product support.

- Use third-party APIs instead of building from scratch: instead of developing, integrate the top-class APIs, which saves months of development time.

- Choose the right development partner: An experienced fintech development company brings regulatory knowledge, pre-built components, and lending domain expertise to your project, diminishing costly mistakes and saving time.

- Build modularly: A modular architecture means you only pay for what you need now and can add features later without redeveloping your entire system.

Compliance & Security Essentials for LOS in 2026

Building a loan origination system with a compliance-first mindset will save you from legal and existential risk.

Regulators across each major market are tightening their digital lending platforms’ supervision, and even a single compliance failure leads to license revocation, fines, or complete shutdown.

If compliance is built correctly, it appears as a competitive advantage, making your borrowers confident and investors comfortable.

Regulatory Frameworks You Must Address

| Regulation | What It Covers | Who It Applies To |

| GDPR | Borrower data privacy and consent | EU markets |

| CCPA | Consumer data rights and transparency | US (California) markets |

| KYC Norms | Borrower identity verification | Global – all lending platforms |

| AML Directives | Anti-money laundering screening | Global – all lending platforms |

| PSD2 | Open banking and payment services | UK & EU markets |

| RBI Digital Lending Guidelines | Digital lending conduct and data storage | India markets |

| FCRA / ECOA | Fair credit reporting and equal lending | US markets |

Before you finalize your compliance architecture, you should map your target markets. When you launch in multiple markets, it demands layering multiple regulatory frameworks. So, plan for this in your starting build, don’t keep it for later.

Data Security Standards Your LOS Must Meet

A company holds borrower data, which is the most sensitive thing, including identity documents, financial records, bank statements, and credit history.

In a lending platform, a security breach is not only a PR problem, but a regulatory one.

| Security Measures | Why It Matters |

| AES-256 Data Encryption | Protects borrower data at rest and in transit |

| OAuth 2.0 Authentication | Secure access control for all platform users |

| SSL / TLS Protocols | Encrypts all data exchanged between the borrower and the platform |

| Role-Based Access Control | Ensures only authorized staff can access sensitive data |

| Penetration Testing | Identifies vulnerabilities before attackers do |

| Audit Trails | Logs every action on the platform for regulatory review |

| Data Residency Compliance | Stores borrower data in the correct geographic location per regulation |

LOS Development Timeline – What FinTech Startups Should Expect

Most fintech startups underestimate how long a production-ready LOS takes to build.

Rushed timelines result in buggy features, compliance gaps, and expensive post-launch fixes.

Here is a realistic timeline across all three development tiers:

Development Timeline by Tier

| Tier | Scope | Timeline |

| MVP / Basic LOS | Core modules – application portal, KYC, basic credit scoring, document management | 3–4 months |

| Mid-Tier LOS | MVP features + AI decisioning, advanced integrations, analytics dashboard | 5–8 months |

| Enterprise LOS | Full-scale platform – multi-market compliance, custom risk models, high-volume infrastructure | 10–16 months |

What Happens in Each Phase

| Phase | What Gets Done | Duration |

| Discovery & Planning | Requirements gathering, compliance mapping, and architecture design | 2–4 weeks |

| UI/UX Design | Borrower portal design, admin dashboard wireframes, and user flows | 3–4 weeks |

| Core Development | Building and integrating all modules | 8–24 weeks (depends on tier) |

| QA & Security Audit | Functional testing, penetration testing, and compliance validation | 3–4 weeks |

| UAT & Launch | User acceptance testing, soft launch, feedback collection | 2–3 weeks |

| Post-Launch Iteration | Bug fixes, performance optimization, feature additions | Ongoing |

What Speeds Up or Slows Down Your Timeline

| Speeds It Up | Slows It Down |

| Clear product requirements from day one | Changing requirements mid-build |

| Experienced fintech development partner | Generic development team with no lending domain knowledge |

| Modular architecture approach | Monolithic build with tightly coupled features |

| Using third-party APIs for standard functions | Building every component from scratch |

| Single market launch | Multi-market compliance from day one |

Common Challenges in Loan Origination Software Development – And How to Solve Them

Developing a custom LOS comes with various hurdles. Every fintech firm faces at least a few of them on its way to software launch.

Below are the challenges you can expect and get ahead of by resolving them.

| Challenge | Solution |

| Compliance complexity across multiple markets | Before development begins, map regulatory requirements in the discovery phase. Build compliance as a module, not an afterthought |

| Integration failures with third-party APIs | Use well-documented, widely adopted APIs. Create with error handling and fallback logic from day one |

| Slow loan decisioning at scale | Implement asynchronous processing and caching at the decisioning layer. Avoid synchronous API calls in the critical approval path |

| Data security vulnerabilities | Conduct penetration testing before launch and schedule quarterly security audits post-launch |

| Scope creep is blowing the budget | Lock your MVP feature set before development starts. Every addition mid-build costs 3x what it would have cost upfront |

| Poor borrower experience leading to drop-offs | Invest in UX research before UI design. Test your application flow with real borrowers before launch |

| Scaling bottlenecks under high loan volume | Build on cloud infrastructure with auto-scaling from day one. A monolithic architecture that works at 100 applications per day breaks at 10,000 |

| Finding a development team with lending domain knowledge | Work with a fintech-specialized development company rather than a generalist agency; the domain knowledge pays for itself in avoiding mistakes |

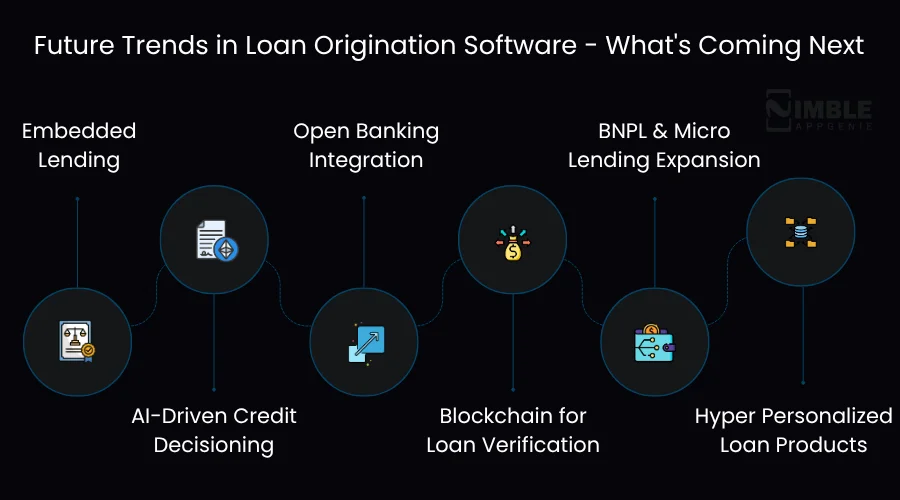

Future Trends in Loan Origination Software – What’s Coming Next

As the lending technology landscape is evolving fast, the startup that considers tomorrow will have a considerable head start over those playing catch-up.

Below are the trends reshaping loan origination software through 2026 and beyond:

1. Embedded Lending

Loan origination is not a standalone app; in fact, a platform that borrowers already use at eCommerce checkouts, payroll platforms, accounting software, and marketplaces.

Embedded lending APIs permit any platform to offer credit whenever needed.

This unlocks a completely new distribution model for fintech startups, originating loans without requiring borrowers to visit your app ever.

2. AI-Driven Credit Decisioning

Based on bureau data, traditional credit scoring is opening the doors for AI models that analyze thousands of alternative data points, spending behavior, social signals, cash flow patterns, and psychometric data.

In 2026, the most competitive LOS platforms leverage machine learning models that boost their accuracy with each loan originated, notably reducing default rates while increasing access to credit for underserved borrowers.

3. Open Banking Integration

Open banking APIs are reshaping how lenders assess borrower creditworthiness. Regardless of depending on static bureau scores or self-reported income, lenders can now access real-time bank transaction data with borrower consent to make more precise lending decisions.

This is a significant opportunity for fintech companies to serve borrowers whom traditional credit scoring systematically ignores.

4. Blockchain for Loan Verification

Blockchain is starting to distinguish itself in the lending space, specifically for identity management, document verification, and cross-border loan origination. Smart contracts on blockchain networks can streamline loan agreement execution, diminish fraud, and create tamper-proof audit trails that please regulators across various jurisdictions.

5. BNPL & Micro-Lending Expansion

Buy Now Pay Later and micro-lending products are witnessing fierce growth globally, specifically in emerging markets across Africa, Southeast Asia, and South Asia.

The LOS platforms strengthening these products should manage excessively high application volumes, ultra-short decisioning windows, and small ticket sizes. If your startup is developing in this space, your LOC architecture should be crafted for volume and speed from day one.

6. Hyper-Personalized Loan Products

One-size-fits-all loan products are falling behind in personalized lending, where repayment schedules, loan terms, and interest rates are dynamically modified based on individual borrower profiles.

The LOS platforms empowering this personalization level are crafted on real-time data pipelines and flexible decisioning engines that traditional software simply can’t support.

How Nimble AppGenie Can Help You Build Your LOS

Developing a loan origination system is a high-stakes fintech build where a missed compliance requirement, the wrong architecture, or an incorrectly integrated API can cost you thousands of dollars and months of rework.

The difference between a platform that expands and one that falls mostly depends on one thing – the development partner you choose.

Real Fintech. Real Challenges. Real Results.

The Client:

MaxPay, a cross-border payment platform targeting freelancers and businesses across global markets.

The Challenge:

The client required a multi-currency eWallet that could send and receive payments across 50+ countries with enterprise-grade security, instant transaction settlements, and a seamless user experience that worked across extensively different regulatory environments. No off-the-shelf platform could handle it.

What Nimble AppGenie Built:

A fully custom fintech platform with real-time settlement infrastructure, multi-currency transaction logic, 2-FA and multi-layer security, and compliance architecture created for international markets, delivered by a dedicated team of 8 in just 6 months.

The Result:

Today, MaxPay is a top name in multi-currency eWallets, widely used by freelancers and businesses for cross-border payments with some of the lowest processing fees in the market.

The same scalable architecture, compliance-first thinking, and the same obsession with developing fintech products that really work at scale, that’s exactly what Nimble AppGenie brings to each loan origination platform we create.

Whether you are beginning from scratch with an MVP LOS or scaling an existing lending platform to manage thousands of applications every day, we have the fintech expertise to develop it right, within budget, and on time.

Conclusion

Loan origination software is not a back-office tool now, but the competitive infrastructure that distinguishes fintech startups that scale from those that slow down progress.

The businesses winning in 2026 are not the ones with the biggest budgets, but the ones that made early smart decisions, choosing the right features, creating on the right architecture, staying compliant, and partnering with a team of fintech developers that understands fintech from the inside out.

Whether you are ready to start loan origination software development or mapping your existing loan product, the roadmap ahead is the same, define your borrower, map your compliance, build modularly, launch lean, and scale fast.

And if you want a lending software development partner who has already solved the hardest fintech problems, from multi-currency payment infrastructure to enterprise-grade security and real-time decisioning, Nimble AppGenie is ready to build it with you.

Your loan origination software is not just a product. It is the basis of your entire lending business. Build it right.

FAQs

Development costs range from $20,000 – $30,000 for a basic MVP, $30,000 – $80,000 for a mid-tier platform, and $80,000 – $200,000+ for an enterprise-grade LOS.

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.