AI Services

AI Services AI App Development

AI App Development Generative AI Development

Generative AI Development AI Chatbot Development

AI Chatbot Development AI Integration Services

AI Integration Services AI For Fintech

AI For Fintech AI Financial Assistant Solution

AI Financial Assistant Solution AI Insurance Agent Development

AI Insurance Agent Development Tech Stack

Tech Stack OpenAI / GPT-4

OpenAI / GPT-4 Claude / Anthropic

Claude / Anthropic Gemini / Google AI

Gemini / Google AI Llama / Open Source

Llama / Open Source LangChain / LlamaIndex

LangChain / LlamaIndex Pinecone / Pgvector

Pinecone / Pgvector AWS / Azure AI

AWS / Azure AI

Fintech Solution

Fintech Solution Fintech App Development

Fintech App Development Neobank App Development

Neobank App Development eWallet App Development

eWallet App Development Payment Integration

Payment Integration Lending Software

Lending Software Banking Software Development

Banking Software Development BNPL Solution

BNPL Solution Insurance App

Insurance App Investment App Dev

Investment App Dev Wealth Management App

Wealth Management App Crypto & DeFi

Crypto & DeFi DeFi App Development

DeFi App Development Crypto Wallet Dev

Crypto Wallet Dev Crypto Exchange Dev

Crypto Exchange Dev Trading Platform Dev

Trading Platform Dev Payments

Payments Compliance

Compliance Fintech & Digital Regulations

Fintech & Digital Regulations Fraud Detection

Fraud Detection Lending Ecosystem

Lending Ecosystem P2P Lending Platform

P2P Lending Platform Mortgage Lending

Mortgage Lending Engagement

Engagement Outsourcing Dev

Outsourcing Dev

Mobile Development

Mobile Development Mobile App Dev

Mobile App Dev iOS App Development

iOS App Development Android App Development

Android App Development React Native

React Native Flutter Development

Flutter Development Web Development

Web Development Node.js Development

Node.js Development React.js Development

React.js Development Angular Development

Angular Development PHP / Laravel

PHP / Laravel App Services

App Services UI/UX Design

UI/UX Design App Maintenance

App Maintenance By Stage

By Stage MVP Development

MVP Development Industry Solutions

Industry Solutions Healthcare App Dev

Healthcare App Dev Education App Dev

Education App Dev Travel App Dev

Travel App Dev Real Estate App Dev

Real Estate App Dev Logistics Software

Logistics Software Social Media App

Social Media App

Hire Mobile Developers

Hire Mobile Developers Hire iPhone Developers

Hire iPhone Developers Hire Android Developers

Hire Android Developers Hire React Native Devs

Hire React Native Devs Hire Flutter Developers

Hire Flutter Developers Hire Web Developers

Hire Web Developers Hire Node.js Developers

Hire Node.js Developers Hire Angular Developers

Hire Angular Developers Hire PHP Developers

Hire PHP Developers Hire Laravel Developers

Hire Laravel Developers How It Works

How It Works Pre-Vetted Developers

Pre-Vetted Developers Ready In 48 Hours

Ready In 48 Hours NDA From Day One

NDA From Day One Replace Guarantee

Replace Guarantee

Company

Company About Us

About Us Our Work Process

Our Work Process Portfolio

Portfolio Case Studies

Case Studies Blog / Insights

Blog / Insights Careers

Careers Contact Us

Contact Us Awards

Awards Recognition

Recognition

Offices

Offices

In a Nutshell:

- Klarna app makes money from merchant fees, Klarna cards, customer interest, late fees, and shopping applications.

- The major components of Klarna are pay later, pay in installments, financing plans, and the Klarna card.

- Klarna now offers banking services, savings accounts, debit cards, and AI-powered financial features, which strengthen its ecosystem and improve profitability.

- Klarna app development focuses on secure payments, KYC, fraud prevention, AI-based credit checks, and smooth merchant integration.

- Nimble AppGenie provides custom BNPL app solutions to deliver a user-friendly BNPL app, inspired by the Klarna business model that aligns with your particular project needs.

Klarna allows people to buy things now and pay later. No interest, no credit card needed. Sounds too good to be true. So how does Klarna make money? That’s the question most people have. And it’s a fair one.

Klarna makes most of its money from the retail shops. Every time a customer checks out using the Klarna app, the store pays Klarna a fee. That’s the core of the business.

But Klarna also earns from interest on long-term payment plans, late fees, its Visa card, in-app advertising, and a subscription service called Klarna Plus. The scale makes a big difference here.

Klarna processed over $105 billion worth of purchases in 2024. It has 114 million users across 26 countries. And in 2024, it finally turned profitable by posting a net income of $21 million after years of losses. That kind of scale is exactly why its business model works so well.

In this blog, we will break down the Klarna revenue model, with real numbers, not vague estimates.

So, let’s begin!

What is Klarna?

Klarna is one of the best Buy Now Pay Later apps available right now. Klarna is a BNPL app, or buy now pay later app, that started in Sweden in 2005.

Today, it is used by more than 180 million people in 45 countries (now 26) and works with 500,000+ stores.

It easily tracks deliveries of your online orders, saves products you like in a wish list, and gets alerts about price drops. It is one of the best buy now, pay later apps so far. Additionally, the app allows you to shop online and pay in different ways.

- Pay Now which means to pay the full amount right away.

- Pay Later means you get the product and pay within 30 days.

- Pay in 3 or 4 parts means splitting your bill into smaller payments over weeks or months.

- The financing option means longer monthly plans with interest.

Facts About Klarna

- Headquarters: Stockholm, Sweden

- Founded: 2005

- Users: 114 million+ active users

- Merchants: 850,000+

- Valuation: Once around $45.6 billion in 2021, but dropped to about $6.7 billion in 2022 after market changes. As of late 2025, the valuation had recovered significantly, touching $14 billion.

- NYSE Listing: Ticker KLAR, listed in September 2025

- AI First Approach: Klarna has evolved significantly as it is now using AI assistants to expedite the process while saving millions of dollars that a workforce would cost.

The facts clearly indicate the turnaround that Klarna has been able to pull off, considering its valuation went down from $50 billion to $6.7 billion. At the current pace they have achieved, Klarna not only makes money but is also profitable.

Klarna by the Numbers (2025)

Before we get into how Klarna makes money, let’s quickly look at how big it actually is.

| Facts | Number |

| Total Revenue | $3.5 billion |

| Total Purchase Processed (GMV) | $127.9 billion |

| Active Users | 118 million |

| Merchant Partners | 966,000 |

| Daily Transactions | 3.4 million |

(Source: Klarna Full Year 2025 Results- investors.klarna.com

These figures really matter because they show why the Klarna business model works. When you are processing $127.9 billion worth of purchases every year in 966,000 stores, even a small fee per transaction adds up to billions. That is exactly what we will break down in the next section.

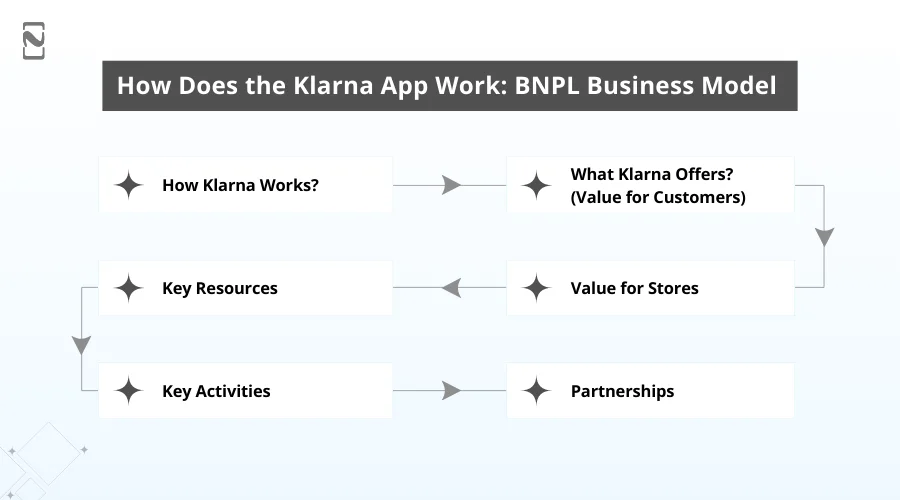

Klarna Business Model: How Does the App Work?

Once you know the components of Klarna, it is clear that its payment mode has different versions. Klarna allows people to pay later, split payments into smaller parts, and use longer financing.

Klarna’s business model is based on helping people shop more, while making it safe and profitable for stores. Let’s now understand the business model of Klarna.

♦ How Klarna Works?

Klarna works as a link between customers and stores. It is vital to know that customers have to do KYC in fintech apps like Klarna. When customers buy something online or in a store and choose Klarna, they pay the store right away.

The customer then pays Klarna later. They can either pay the full amount after 30 days or split it into smaller payments. If the customer does not pay on time, Klarna may charge a late fee.

One of the key questions that often emerges is how Klarna makes money without charging interest. The answer to that question is simple: late charges and the merchant fees paid by retailers are the core income sources of Klarna, but more on that later!

♦ What Klarna Offers? (Value for Customers)

Klarna gives customers different ways to pay. They can buy now and pay later, pay in a few small instalments, or use longer financing options. The last one is just for the expensive products only.

The Klarna app helps customers track their orders, save their favorite products, and get notifications when prices drop. It also offers a card that brings BNPL integration to stores that do not directly partner with the service. This makes it convenient for shopping anywhere.

♦ Value For Stores

Stores also benefit from Klarna because it is the only one that gives customers a BNPL option. They get their money instantly, so they do not have to wait for customers to pay.

When stores provide the Klarna payment mode, it attracts more and more people to shop. Stores can also showcase their products inside the Klarna app, which helps them reach millions of customers.

♦ Key Resources

Klarna depends on its technology to manage payments, check for fraud, and run the app. It also uses data to understand customer behaviour and reduce risk.

It is vital to know that partnerships with banks, card networks, and online stores are essential. Lastly, Klarna’s trust and reputation are key, since people and stores need to feel safe using it.

♦ Key Activities

Klarna does many things every day to keep its business running. It manages payments, checks credit, detects payment fraud, and supports customers.

It also updates the app, works with new stores, runs marketing campaigns, and follows financial rules in different countries. To stay updated, Klarna follows the latest BNPL trends like providing flexible instalment options and using AI to make smart credit decisions.

♦ Partnerships

Klarna works with banks, card networks like Visa, and online platforms like Shopify. It also partners with giant stores like eBay, Nike, Walmart, and IKEA. These partnerships help Klarna reach more users and earn trust.

How Does Klarna Make Money?

Klarna allows you to buy now and pay later for free. It does not charge any interest or hidden charges. So the obvious question is. Where does the money actually come from? The simple answer is that most of the money comes from the stores.

Each time a customer uses the Klarna app at checkout, the retail store pays Klarna a fee or a commission. On top of that, Klarna earns from the interest on longer payment plans, late fees, its Visa card, in-app ads, and a subscription service.

The table below shows the revenue of the year 2024.

| Revenue Stream | Amount (2024) | Share of Total |

| Merchant Fees | ~$1.6 billion | 57% |

| Interest Income | ~$675 million | 24% |

| Late Fees / Consumer Fees | ~$254 million | 9% |

| In-App Advertising | ~$180 million | 6% |

| Klarna Card (Interchange) | ~$84 million | 3% |

| Total | $2.81 billion | 100% |

(Source: Klarna IPO Prospectus, SEC Filing 424B4 — September 2025)

What Are the Klarna Revenue Streams?

Now let’s look at each one of the revenue streams of Klarna.

1. Merchant Fees

This is where most of Klarna’s money comes from. Around 57% of everything it earns. So, how does Klarna work? When a customer purchases something with the Klarna app, the store pays Klarna a fee. Customers pay nothing extra, and the store pays.

The exact fee is $0.30 flat per transaction, plus between 3.29% and 5.99% of the purchase amount. So on a $200 purchase, the store is paying Klarna roughly $7 to $10. That is higher than a regular credit card fee. So why do stores agree to it?

Since Klarna assists them in selling more products. Retail stores that use Klarna see customers spend 20–30% more per order, and up to 44% more people actually complete their purchase instead of leaving the website.

For most stores, the extra sales are worth the higher fee. In 2024, merchant fees brought Klarna roughly $1.6 billion.

2. Interest on Longer Payment Plans

Most Klarna options like Pay in 4 and Pay in 30 days, are completely interest-free. But Klarna also provides longer financing if a customer purchases bigger or more costly items. Things like a $1,500 laptop or a $2000 sofa.

These plans run from 6 months up to 36 months, and they do charge interest, up to 19.99% APR, depending on your credit. This is where Klarna earns like a traditional lender.

The customer pays back a little each month, and Klarna earns interest on the outstanding balance until it’s fully paid off.

In 2024, this brought in $675 million, 24% of total revenue. Also, it is the fastest-growing stream right now in the US, where Klarna is pushing these longer plans hard.

3. Late Fees

If you miss a payment, Klarna charges a late fee. In the US, that’s $7 per missed payment, capped at 25% of the order value. In 2024, late fees and other small consumer charges brought in around $254 million.

Worth noting, Klarna says 99% of payments are made on time. So most customers never pay a late fee. But for the small percentage who do, it’s still a meaningful revenue stream.

4. In-App Advertising

This one surprises most people. Klarna has millions of users opening its app regularly to track orders, browse products, and manage payments. That’s a huge audience of active shoppers, and brands pay to reach them.

Stores pay Klarna for sponsored placements, featured listings, and targeted ads inside the app. Since Klarna knows exactly what its users buy, when, and how much they spend, these ads are very precise and effective.

In 2024, advertising brought in $180 million. That is up 15x since 2020. Klarna is quietly building something that looks a lot like Amazon’s advertising business, using shopping data to sell ad space.

5. The Klarna Card

In 2022, Klarna launched a physical Visa card. It works anywhere that accepts Visa, not just online stores that partner with Klarna, but with the same pay-later features built in.

Every time someone uses the Klarna Card, the merchant pays an interchange fee of between 1% and 3%. Klarna gets a cut of that, just like any card issuer does.

The card has taken off fast. By Q3 2025, it had 4 million active users. This makes up 15% of all Klarna transactions globally. In 2024, interchange fees brought in $84 million, and that number is growing quickly, given how fast card signups are accelerating.

6. Klarna Plus Subscription

Klarna also has a paid subscription called Klarna Plus, priced at $7.99 per month in the US. Subscribers get perks like waived fees, extra cashback, and exclusive deals with partner brands.

This is still a newer revenue stream, and Klarna has not broken out the exact contribution yet. A small percentage paying $7.99 a month adds up to significant recurring revenue.

That is every stream. The stores fund the free experience for shoppers. And as Klarna grows its card, its financing products, and its advertising business, it is becoming less dependent on any single one of them.

Klarna vs Affirm vs Afterpay: How Do They Compare?

Klarna is not the only BNPL company out there. Affirm and Afterpay are its two biggest competitors. On the surface, they all do the same thing.

They allow customers to use the buy now, pay later service. But the way they make money is quite different. Take a look at the table below for comparison.

| Components | Klarna | Affirm | AfterPay |

| Merchant Fee | $0.30 + 3.29% – 5.99% | 2% – 8%, depending on the merchant | $0.30 + 4%–6% |

| Interest in plans | Up to 19.99% APR (long-term only) | 0%–36% APR | No interest ever |

| Late Fees | $7 per missed payment | None, zero late fees ever | $10 first miss, then $7 |

| Pays in How Many Parts | 4 payments, 30 days, or up to 36 months | 4 payments or up to 60 months | 4 payments only |

| Charges Consumers Interest | Only on long-term plans | Yes, on most monthly plans | Never |

| Has a Physical Card | Yes, Klarna Visa Card | Yes, Affirm Card | No |

| In-App Advertising | Yes, growing fast | No | No |

| Subscription Product | Yes, Klarna Plus ($7.99/mo) | No | No |

| Active Users | 118 million | More than 21 million | More than 24 million |

| Merchants | 966,000 | 335,000+ | 144,000+ |

| 2024 Revenue | $2.81 billion | More than $2.32 billion | Part of Block, not reported separately |

| Is this profitable in 2024? | Yes, $21M net profit | No, still loss-making | Part of Block |

Now, here is what actually separates them, because the table alone does not tell the full story.

1. Affirm Never Charges Late Fees

That is a real difference, and they are very proud of it. Affirm only earns money when customers pay back their loan, so they are very careful about who they lend to.

The trade-off is that Affirm charges interest on most of its monthly plans, which can go up to 36% APR. So you do not get hit with late fees, but you can end up paying more overall if you choose a longer plan.

2. Afterpay is the Simplest of the Three

Afterpay pays in 4 instalments without any interest, long-term plans, a Visa card, or a subscription. It is a pure BNPL product and nothing else.

The downside is that it is more limited; customers can only split into 4 payments, and they cannot do financing any longer. Also, if they miss a payment, they get hit with a $10 fee.

3. Klarna Sits in the Middle and Expands

It has more payment options than either competitor, including a physical card, advertising revenue, a subscription, and banking products. It is the most complex business of the three, which is partly why it took longer to become profitable.

What Sets Klarna’s Business Model as a Differentiator?

As you can see, Klarna is already a leader in this BNPL space. Not just because it started early, but because the company grew smartly. It uses smart technologies while keeping its operation slow.

Overall, Klarna provides a mix of BNPL + digital banking + AI financial tools. While most competitors’ apps, like Affirm, as we mentioned above, are limited to a few countries, Klarna has expanded to 26 countries. With this massive reach, Klarna not only makes money but also creates a global impact.

Additionally, its large network and partnerships with major brands like eBay, Walmart, Nike, IKEA, and Sephora have helped Klarna build trust among its competitors. Its strong reputation and reliable service make it a preferred choice for many shoppers worldwide.

Is Klarna Actually Profitable?

Yes, Klarna is profitable. But the honest answer depends on how you see it. Let’s break it down.

In the year 2022, Klarna lost $1 billion dollars in a single year. But the company has scaled so fast. You can see that the interest rates went up, and investors panicked.

Klarna’s valuation crashed from $45.6 billion all the way down to $6.7 billion, an 85% drop in less than a year. Most companies, including many apps like Klarna that boomed during the same period, never recovered from that kind of fall. But Klarna did.

By 2024, Klarna posted its first net profit since 2019, $21 million. That is not a huge number if we compare it to $2.81 billion in revenue, but it was a turning point. It proved the business model actually works.

Then came 2025. Revenue hit $3.5 billion. It increased 25% compared to 2024. Klarna posted an adjusted operating profit of $65 million for the full year. And in Q4 2025, it delivered its first-ever billion-dollar quarter, which was $1.08 billion in revenue in just three months.

The table below showcases the revenue, net profit, and loss of Klarna in consecutive years.

| Year | Revenue | Net Profit/Loss |

| 2022 | $1.9 billion | -$1 billion loss |

| 2023 | $2.27 billion | -$244 million loss |

| 2024 | $2.81 billion | +$21 million profit |

| 2025 | $3.5 billion | +$65 million adjusted operating profit |

(Source: Klarna Full Year 2025 Results — investors.klarna.com & Klarna Q4 2025 SEC Filing)

So yes, Klarna is profitable, but there is a catch worth knowing.

The net profit figures are still relatively small compared to the size of the business. Klarna is growing really fast at a rapid pace in the USA, and it is spending a lot to do that. It is a deliberate trade-off that grows now and increases profit later.

One more thing that makes Klarna’s story so interesting is that it is doing all of this with very few people than before. From the year 2022, Klarna’s revenue has increased 104% while its layoff was 49%.

Additionally, sales per employee hit $1.24 million in 2025. That is largely because of AI. Klarna replaced large parts of its customer service team with AI tools, which cut costs dramatically without slowing growth.

Why Choose Nimble AppGenie to Build a BNPL App like Klarna?

Creating a BNPL app like Klarna is not an easy task. It is not just about payments. You need to handle approvals, repayments, user data, and security at the same time. If this is not managed in a proper way, your mobile application can face issues.

As a recognized fintech app development company, Nimble AppGenie understands how this model works in real life. We majorly focus on developing custom BNPL apps, so people can clearly see what they need to pay and when.

Additionally, we assist in adding the main features that actually matter, like split payments, reminders, user verification, and a smooth checkout process. Instead of making things complex, we keep the flow easy and clear.

Besides, security is also a big part of it. Since users are dealing with money, your BNPL product needs to be safe and follow proper rules. This is something we take care of from the beginning.

Our experts also do not follow a fixed approach. Every BNPL app is different, so we build a high-performing app based on your idea, your users, and how you plan to earn.

So, if you are planning to create a BNPL app, Nimble AppGenie can save time, reduce mistakes, and help you build something that actually works.

Conclusion

Klarna make money in a smarter way than most people think. Stores pay the fees. Shoppers get the free experience. And on top of that, Klarna earns from interest, late fees, its Visa card, in-app ads, and a subscription service.

But what is the result? Well, $3.5 billion in revenue in 2025 and a successful IPO on the New York Stock Exchange. The model works because it benefits everyone. For example, shoppers get flexibility, stores sell more, and Klarna earns from multiple streams at once.

If this revenue model has inspired you and you are thinking about how to develop an app like Klarna, the biggest lesson is simple: build multiple revenue streams from day one, not just one. That is exactly what makes Klarna work.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.