In a Nutshell:

- Fintech security is not a one-time task; it’s an ongoing commitment that demands to be built into your app from the start, and shouldn’t be kept as an afterthought.

- Almost half of financial companies have faced a fintech data breach in the last two years, which makes security one of the most critical priorities for any fintech business.

- The four biggest fintech app security risks are identity theft, data breaches, online scams and phishing, and regulatory penalties. All are preventable with the right measures.

- Following fintech security best practices like multi-factor authentication, encryption, role-based access control, and regular penetration testing helps reduce your exposure to attacks.

- Fintech compliance is not just a legal requirement – frameworks like PCI DSS, GDPR, ISO 27001, and SOC 2 actively support your security posture and make you a more trusted partner for banks and enterprise clients.

- Regulations vary by region – US fintech regulations like KYC, AML, and EFTA, EU fintech regulations like GDPR, PSD2, and DORA, and global standards all apply based on where you operate.

- Building a secure fintech app starts at the architecture stage – access control, compliance alignment, and third-party integration security all need to be planned before development accelerates.

- Partnering with an experienced fintech app development company like Nimble AppGenie ensures security is handled at every layer of your product, from code to compliance.

Fintech development is a very intricate process, and security is one among those that you can’t afford to lack.

Start by thinking about what your app really holds – bank account details, personal identification, transaction history, and investment data.

Cybercriminals actively target this type of sensitive data and fintech platforms because of the high financial value of assets and transactions they handle, and remain among the most attractive targets across all industries.

Nearly half of fintech companies have experienced a security breach in the past two years. When it happens, they face severe damage far beyond the immediate financial loss; regulators come knocking; customer trust takes a hit; and recovery takes far longer than the breach itself.

Businesses can prevent most security failures, but those that are heavily impacted treat security as an afterthought, usually after launch.

This fintech security guide will help you to avoid them. Let’s talk about fintech apps’ biggest risks one may face, the best practices to follow to stay protected, the regulations to stay compliant with, and how to build security into your fintech product from scratch.

If you are building a fintech app or already running one, this is worth your time.

Fintech Security Glossary

Security comes with a set of terms that may leave you confused.

So, before we go deeper, let’s have a quick breakdown of the key fintech terms you will come across in this blog, explained in plain text.

1. Cybersecurity Attack

When someone attempts to break into an app, steal data, or cause damage to a system purposely. In fintech, such apps take place because of the involvement of valuable personal data or money.

2. Data Breach

When private information, such as a customer’s login credentials or bank details, gets into the wrong hands. Sometimes, the reason is that a small security gap is uncovered and exploited.

3. Zero-Trust Architecture

Imagine a building’s door where a keycard is needed to go in and out. Zero-trust works in the same manner. No system or user is trusted automatically, even if they are already inside the network. Every time, everyone should prove their existence there.

4. Multi-Factor Authentication (MFA)

When a fintech application asks for your identity verification in different ways before allowing you to log in, it’s MFA. A password and a code are sent to your phone, which is a common example. But with MFA, even if someone has your password, they can’t break in.

5. API Security

Apps consistently share data with other services and apps, out of public view. APIs act as the channels allowing this. API security ensures those channels are properly safeguarded so that only the exact person and system can access them.

6. Tokenization

Despite storing your real card number, tokenization replaces it with a random code that’s useless. So, even if someone manages to steal it, they can’t do anything with it.

7. Know Your Customer (KYC)

KYC is a process fintech companies use to confirm who their actual customers are. It generally involves ID verification or a background check before they give someone access to financial services. It keeps fraudsters from signing up under fake identities.

8. Know Your Business (KYB)

KYB’s idea is the same as KYC, but not for individuals, for companies. Before working with a client, a fintech platform should confirm the company is real, safe to work with, and above all, legally registered.

9. Fraud Detection System

This is a system that monitors transactions and user activity in real time, looking for anything that’s odd or seems off. If someone makes a suspicious transfer or logs in from an unusual location, the system blocks it or flags it immediately.

10. DevSecOps

This is an application development approach where security is ensured from the start, not added at the end. The development, operations, and security teams will work collaboratively throughout the whole process, rather than in separate stages.

Why is Fintech Security Important?

Fintech apps manage sensitive personal data and real money. Thus, they are the biggest targets for cybercriminals.

When a user signs up on your fintech platform, they trust you with their identity information, bank details, and financial history. If that trust is hampered, even once, it’s hard to rebuild.

The major risk is not just losing customers, but also legal liability, security failure, and serious financial damage. This sort of setback can be hard for a growing fintech business, which would be even more challenging to come back from.

The businesses that avoid such obstacles take security seriously from the beginning as a crucial part of their operations, not as a technical requirement.

Common Risks in Fintech Apps

Knowing what risks to avoid is the first step to protecting your platform.

Below are the four most common security risks that fintech apps face.

• Data Breaches

Fintech apps store the most sensitive information, like account numbers, transaction history, and personal identification details. And this makes them a prime target.

When someone gets unauthorized access to the data, a data breach happens. It could be through an unsecured third-party service with which your app is connected, a vulnerability in your code, or even an internal leak.

When it happens, the consequences are severe – legal exposure, a damaged reputation, and financial loss that takes longer to recover.

• Identity Theft

When someone leverages stolen details to portray one of your customers, identity theft occurs. They enter the account and start making transactions, applying for credit, or transferring funds – with real customers having no idea.

Today, this is the most dangerous risk as methods are becoming sophisticated. Attackers use tactics like SIM swapping, where they seize a customer’s phone number to skip two-factor authentication, and credential stuffing, where they attempt thousands of leaked passwords until one unlocks.

• Online Scams and Phishing

Not all the attacks are aimed directly at your platform; some go after users also. The most common example is phishing.

A customer receives a message that seems to be coming from your app, clicks a link, and enters their details on a fake page without even realizing they have handed over their credentials to a scammer.

Fake support pages, spoofed emails, and cloned app interfaces all belong to the same playbook. Your platform doesn’t need to be compromised for the users to be affected. That’s why this risk is too tricky to manage.

• Regulatory Penalties and Operational Disruption

This risk is usually overlooked, but it can be damaging like the others.

When a fintech platform is not secure and doesn’t meet compliance standards, regulators step in. They force audits, impose heavy fines, or restrict their ability to process payments.

Above that, serious security incidents take place that lead to frozen transactions, stress your support team, and divert your engineering team from the routine work to deal with such fallout.

The financial cost is crucial, but the distraction it causes and the time lost can pull back the growing business.

15 Fintech Security Best Practices

Now you know the risk that can hinder your way. But, just knowing is not enough; you should also learn how to beat them if caught.

Below are the 15 best practices that every fintech app should be prepared for.

1. Regular Data Backup

Even if your security is robust, things can still go wrong. A severe failure, ransomware attack, or even a simple human error can delete critical data in seconds.

With regular backups, you can quickly restore everything, even if the worst happens, without bringing your platform to a deadlock or losing your customers’ data.

Pro Tip: Besides backing up your data, regularly test your recovery process. You can’t fully trust a backup that you have never tested.

2. Data Storage Encryption

Encryption converts your data into a coded format that no one can read entirely; only the one with the right key can unlock it. So, even if an attacker manages to obtain data, they can’t do anything with it.

Fintech apps should encrypt data end-to-end when it’s being stored and sent between systems.

Pro Tip: Ensure that encryption is applied everywhere – not only your main database, but also internal communications between your application’s services and backups.

3. Encryption Key Management

Encryption is as powerful as the keys used to lock and unlock it. If those keys are stored in the wrong place, poorly managed, or accessible to several individuals, your encryption provides very little protection.

Proper key management means managing who has access to encryption keys, storing them securely, and rotating them routinely, separate from the data they safeguard.

Pro Tip: Utilize a dedicated key management service despite manually managing keys. It diminishes human error and offers a complete, transparent audit trail of who accessed what and when.

4. Metadata Tracking

Every time a user logs into your app, it generates useful information, like their device ID, IP address, and login time. By tracking this metadata, businesses can spot unusual patterns that might be creating an issue.

For instance, if the same account logs in from two separate countries within an hour, that’s a red flag demanding investigation.

Pro Tip: Be cautious of what you track. Only accumulate the metadata that is actually useful for security purposes; gathering more than you require creates compliance risks.

5. Vulnerability Monitoring

At launch, the fintech app is secure, and the risk environment keeps changing. Vulnerability monitoring means consistently scanning platform weaknesses, whether in its code or in the third-party tools and libraries the app relies on. It’s always cheaper and less demanding to catch a vulnerability early than to deal with it later after it has been exploited.

Pro Tip: Set up automated scanning tools that scan for recognized vulnerabilities in your dependencies every time you make an update. Don’t wait for a scheduled review, as it could be late.

6. Multi-Factor Authentication (MFA)

A password alone is not sufficient protection now. Multi-factor authentication appends one more layer of verification, like a fingerprint scan or a one-time code sent to a phone. So, even if a password is stolen, an attacker still can’t invade. MFA is non-negotiable for a fintech app where accounts are directly linked to money.

Pro Tip: You should make MFA mandatory for all users, not optional. Various security breaches involving stolen credentials could have been prevented by MFA being switched on.

7. Role-Based Access Control

Not every member of your team should have access to everything. Role-based access control means every person, whether a customer support agent, a developer, or a finance manager, should have access to only the system parts they need to accomplish their job. This restricts the damage that can occur if an account is compromised or an insider acts maliciously.

Pro Tip: Regularly review access permissions, especially when someone leaves the company or changes roles. In growing teams, outdated access rights are the most overlooked security risks.

8. API Security and Rate Limiting

Your app almost certainly connects to other services through APIs – identity verification tools, banking integrations, and payment gateways like Square and PayPal. Every such connection is a possible entry point for attackers. Securing your APIs means handling who can access them, encrypting the data they carry, and setting limits on how many requests can be made in a particular time period. This safeguards the platform against automated attacks.

Pro Tip: You shouldn’t expose more data through an API, as the less information an endpoint uncovers, the less it is prone to being exploited.

9. Secure Mobile Development

If your fintech product has a mobile app, as most do, the app itself demands the development of security from the ground up. It means to make sure sensitive data is never stored in plain text on the device, every communication with your server is encrypted, and the app is protected from reverse engineering or tampering by bad actors.

Pro Tip: Conduct security testing on your mobile app specifically before every main release. Mobile apps are a standard entry point for attackers, as they are directly available to users.

10. Web Application Firewall (WAF)

A web application firewall acts as a filter between your app and incoming internet traffic. It stops common attacks, like cross-site scripting, where malicious code is injected into your pages, and SQL injection, where attackers attempt to manipulate your database through input fields. Think of it as a security guard at the front door that blocks known threats before they even reach your application.

Pro Tip: A WAF is a robust first line of defence, but it works best with secure coding practices, not as a substitute for them.

11. Biometric Authentication

Biometric authentication leverages users’ fingerprints, voices, or faces for their identity verification. For most users, it is rapid and more secure than a password, and adds a protection layer that’s very difficult to steal or fake.

Offering biometric login can significantly boost security and user experience for a fintech app.

Pro Tip: Biometrics must complement the current security measures, not replace them. Use it with MFA and secure session management for powerful protection.

12. Penetration Testing

Also known as pen testing, penetration testing is when you hire security experts to break into your platform in the same way an attacker would.

The target is to diagnose the weaknesses before others can. It goes in-depth beyond automated scanning tools, as real specialists can spot configuration mistakes, logic flaws, and creative attack paths that software fails to detect.

Pro Tip: Don’t address pen testing as a one-time exercise. For once a year, run it, and also after any significant changes to your platform, as payment gateway integrations and new features can unveil new vulnerabilities.

13. Incident Response Plan

Even by maintaining the best security, no platform is entirely safe from incidents. An incident response plan is a transparent, documented guide for what happens when anything goes wrong unexpectedly, how the team communicates, who takes charge, how normal operations are restored, and how regulators and customers are notified.

Having a set plan before you even need it means that you quickly and calmly respond despite running into a crisis.

Pro Tip: With your team, run a practice drill at least once annually. Knowing the plan on paper and knowing the way to execute it even under pressure are two different edges.

14. Single Entry Point Control

Consider this as the one front door to your system. So, despite having several ways to access your internal infrastructure, one controlled entry end, typically a secure gateway or a VPN, means every access goes through a single place that can be monitored and locked down. If something unusual happens, you only have to look at one place and act there only.

Pro Tip: Whether successful or not, log each access attempt through your entry point. Suspicious patterns in failed attempts are usually an early warning sign of an attack in progress.

15. Compliance Readiness

It’s not only a legal need to stay compliant with financial regulations, but a security practice. Frameworks like PCI DSS, ISO 27001, and SOC 2 compel you to audit your controls, document your processes, and fix gaps before they become issues.

If you are compliance-ready, you become a more trusted partner for payment processors, banks, and enterprise clients.

Pro Tip: Don’t wait for an audit to order up your documentation. Constantly keep your records and security policies updated; it’s more effective and less stressful.

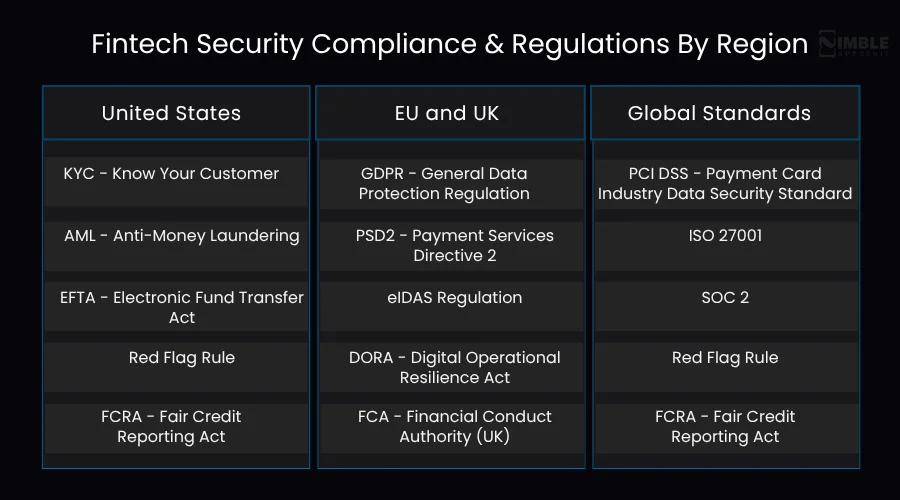

Fintech Security Compliance & Regulations

A secure fintech solution is not only about safeguarding your platform from attackers. It’s also about meeting the legal and regulatory standards that control how financial data is managed.

Falling short of these needs can lead to forced shutdowns, heavy fines, and a loss of the banking and payment partnerships on which your business depends.

Below is a breakdown of the core regulations you should be aware of, arranged by region.

1. United States

• KYC – Know Your Customer

KYC needs fintech companies for their customers’ identity verification before they give them access to financial services. It states running background checks, monitoring accounts for doubtful activity, and checking IDs.

It’s one of the most basic compliance requirements in fintech that prevents fraud and financial crime.

• AML – Anti-Money Laundering

AML regulations need fintech platforms to have systems ready that can address and report suspicious financial activity, specifically anything that seems like a try to hide illegally obtained money.

Failing to comply not just leads to fines, but results in criminal liability for the business and its leadership.

• EFTA – Electronic Fund Transfer Act

The EFTA protects consumers when they make e-payments, covering things like online bank transfers, debit card transactions, and automatic bill payments.

For fintech apps, it’s crucial to understand and comply with EFTA, which manages any sort of electronic fund movement.

• Red Flag Rule

Set to prevent identity theft, the Red Flag Rule requires financial institutions and fintech platforms to stay prepared with a written programme that recognizes and responds to warning signs or identity theft in customer accounts.

• FCRA – Fair Credit Reporting Act

If your fintech platform uses credit details to make decisions, such as for lending, the FCRA controls how that information can be gathered, used, and shared. It offers consumers rights over their credit information and sets rigid rules for how businesses manage it.

2. EU and UK

• GDPR – General Data Protection Regulation

One of the strictest data protection laws globally, GDPR, governs how businesses accumulate, store, and use people’s personal data in the EU.

GDPR is not optional for fintech platforms serving customers or operating in Europe.

Penalties for violations can reach up to 4% of your annual global revenue.

• PSD2 – Payment Services Directive 2

PSD2 handles electronic payments across the EU and raised a necessity called Strong Customer Authentication, which means online payments should be verified leveraging at least two independent factors, like a fingerprint and a password. It also unlocked the door to open banking, which brings its unique set of security responsibilities.

• eIDAS Regulation

eIDAS sets the standards for digital signatures and electronic identification across the EU. It ensures that electronic signatures and digital contracts are legally valid, specifically for fintech platforms that manage digital agreements or onboard customers remotely.

• DORA – Digital Operational Resilience Act

DORA is a rather new EU regulation that focuses particularly on the resilience of financial platforms. It needs fintech companies to have powerful systems for handling technology risks, reporting incidents, and ensuring that third-party providers, like payment processors or cloud services, also meet stringent security standards.

• FCA – Financial Conduct Authority (UK)

In the UK, the FCA supervises financial services and sets expectations around consumer protection, security, and operational resilience. Fintech platforms operating in the UK require meeting FCA standards or risk losing their capability to provide regulated financial services.

3. Global Standards

• PCI DSS – Payment Card Industry Data Security Standard

If your fintech app processes, transmits, or stores payment card data, PCI DSS applies to you – regardless of where you are based. It sets out specific operational and technical requirements for securing cardholder information, from network security to access control. Non-compliance can result in higher transaction costs, fines, or losing the power to accept card payments altogether.

• ISO 27001

ISO 27001 is an internationally acknowledged standard for information security management. Achieving certification states that your organization has an audited, well-structured approach to addressing and handling security risks.

It’s not a legal requirement, but increasingly anticipated by enterprise clients, investors, and banking partners as a sign that your security practices are deep.

• SOC 2

SOC 2 is an audit framework that seamlessly assesses how perfectly a company safeguards customer data across five areas – availability, security, privacy, processing integrity, and confidentiality. It’s commonly needed by financial partners and large business clients as part of their vendor due diligence process.

If you are planning to work with enterprise customers or banks, prioritizing SOC 2 readiness early is the key.

Regularly review your compliance needs, as regulations are dynamic and what was enough earlier may not be sufficient today.

If you are in a dilemma about which regulations would suit your platform, partner with a legal or compliance expert at the start, only to save an expensive U-turn later.

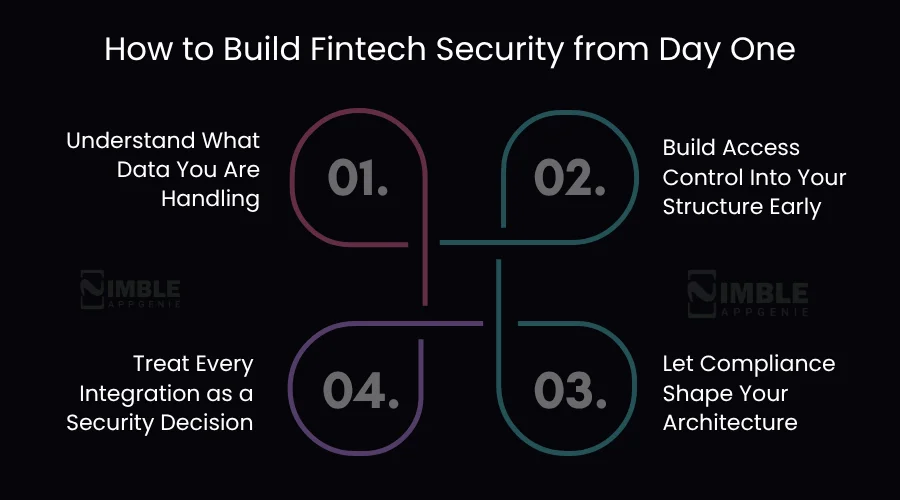

How to Build Fintech Security from Day One

Most fintech security issues occur not because of the team’s carelessness, but because they never began with a properly planned security aspect.

But, do you know, it’s much simpler and cheaper to start with it than to fix it later when something goes wrong.

Here are four steps to approach fintech security correctly from day one.

Step 1. Understand What Data You Are Handling

Before you secure your platform, you should know what you are protecting. Initiate by mapping all sorts of data your app will collect, store, and process.

Identity documents, investment data, transaction records, and payment details all bear different risk levels and bring distinct compliance obligations.

The clearer you are with the data you carry, the easier it is to decide what security measures you really need and where to target first.

Step 2. Build Access Control Into Your Structure Early

Before your platform starts scaling, decide who can access what. This means setting clear roles for your fintech team who can see customer data, access financial records, and modify the system, ensuring those permissions are limited to an extent.

Getting this set in the first place shields you from a very common problem: platforms that scale quickly and result in too many individuals having access to too much.

That is a serious compliance headache and security risk that’s challenging to manage later.

Step 3. Let Compliance Shape Your Architecture

If you are aware where your platform will operate: the US, Europe, or numerous regions, the applicable regulations should influence how your system is developed – not only how it’s documented.

Things such as encryption standards, data storage locations, breach notification processes, and audit logging should all be handled at the architecture level.

At the design stage, bringing compliance into it is comparatively less disruptive and far less costly than upgrading it once your platform is live.

Step 4. Treat Every Integration as a Security Decision

Various fintech platforms are connected with a wide range of third-party services – identity verification tools, payment gateways, analytics platforms, and cloud providers. Each one of these is a possible exposure.

So, before you integrate any external service, ask how to manage your data, what security standards it meets, and what the consequences are if it gets compromised.

From the start, carefully check your integrations that are most effective and the most overlooked aspects you can consider to protect your users.

Nimble AppGenie – Your Partner in Secure Fintech Solutions

Fintech security is not something you determine; you must plan, build, and maintain it with care. This demands a development team that has knowledge of the technical side and the compliance landscape.

At Nimble AppGenie, we have almost a decade of experience building fintech applications that are feature-rich and actually secure. From encryption and access control to KYC compliance and API protection, we create security in each layer of the product, as a foundation, not as an afterthought.

We understand that fintech security can be overwhelming for most business owners and founders. The stakes are high, and there’s a lot to get right.

We help clients with complexities and deliver a fintech product that can confidently present to end users and regulators.

If you are building a fintech app and want to get the security right from day one, our team is ready to help. Hire app developers from Nimble AppGenie and build something your users can truly trust.

Conclusion

Fintech security is not a one-time job; it’s a continuous commitment that holds significance in every part of how your platform is developed, operated, and scaled.

The risk is real – identity theft, regulatory penalties, data breaches, and everything in between. But as we showed in this guide, they are also manageable.

You can build a fintech app that users trust, and regulators respect, with the right practices, the right team you partnered with, and the right compliance standards met.

Businesses that struggle with fintech security are mostly the ones that acknowledge it as an afterthought. And the ones that get it right are the ones who prioritize it from the very beginning.

If you are ready to build a fintech app the right way, secure, compliant, and built to last, Nimble AppGenie is here to help you get there.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.