Banking Software Development

Banking Software Development Our Work Process

Our Work Process Awards

Awards

In a Nutshell:

- RTP (Real-time payments) can be defined as the real-time fund transfer process, and it provides real-time instant money availability.

- FedNow services do allows the financial institutions of all sizes to send and even receive payments instantly.

- The major difference between the RTP and FedNow lies in their ownership, settlement mechanisms, and even in the translation limits.

- You can create an RTP app through planning, securing RTP, integrating APIs, implementing the core technologies, and performing testing.

- Additionally, you can integrate FedNow services by determining connectivity options, connecting with the service providers, integrating ISO standards, and then testing it across the platforms.

- Partnering with Nimble AppGenie can help you select the right element for your business app.

RTP, FedNow, or Both!

Well, if you’re looking to implement RTP or FedNow services, learning about them all is an important step to undertake.

Real-time payments (RTP) refer to the instant fund transfer and are helpful to businesses to receive and send funds successfully. However, FedNow is an instant payment infrastructure that allows banks and credit unions to allow financial institutions to send and receive money.

In this detailed guide on RTP and FedNow, you can explore the rise of RTP, its working process, implementation steps, and differences.

Hence, without further ado, let’s begin.

The Rise of RTP and FedNow

Before you directly jump into understanding the RTP and FedNow, it’s important to evaluate where it all began.

The clearing house’s real-time payments network was the first payments network in the United States to offer near instant settlement and clearing.

In 1973, Japan’s Zengin system started processing payments in real-time, although it went 24/7 in 2018. It was further followed by Switzerland in 1987; this pace picked up after the turn of the 21st century.

Later, India launched its rapidly growing Unified Payments Interface real-time payments platform in 2016, which had the largest volume of payments with over 129.3 billion transactions.

When it comes to FedNow, these services went live on July 20, 2023, and are available to depository institutions in the United States, which enables businesses and individuals to send instant payments via their depository institution accounts.

The birth of RTP was in 2017, and FedNow steps in 2023; they are considered as two trails, and one evolution.

If you are building a banking app, proceeding with the real-time payments, or FedNow services, and even both, is essential.

Now, let’s get ahead with learning them.

What is RTP (Real-Time Payments)?

Real-time payments are instant funds transfers that provide near-instant money availability via payment networks that do operate around 24/7.

Unlike the traditional payment systems, which can take hours or days to complete a single transaction, the RTP systems can be used to transfer funds from one bank account to another immediately.

It further improves transparency and confidence in payments, helping consumers, banks, and even businesses manage their money. These systems are designed to enhance transactions and are initiated, cleared, and settled within seconds at any time of the day or week, including holidays and weekends.

One of the important roles of RTP is to optimize the complete cash flow, enhance overall liquidity, and then improve the complete customer experience via immediate payment confirmation. This is also a crucial mobile banking app feature that you cannot ignore for your app.

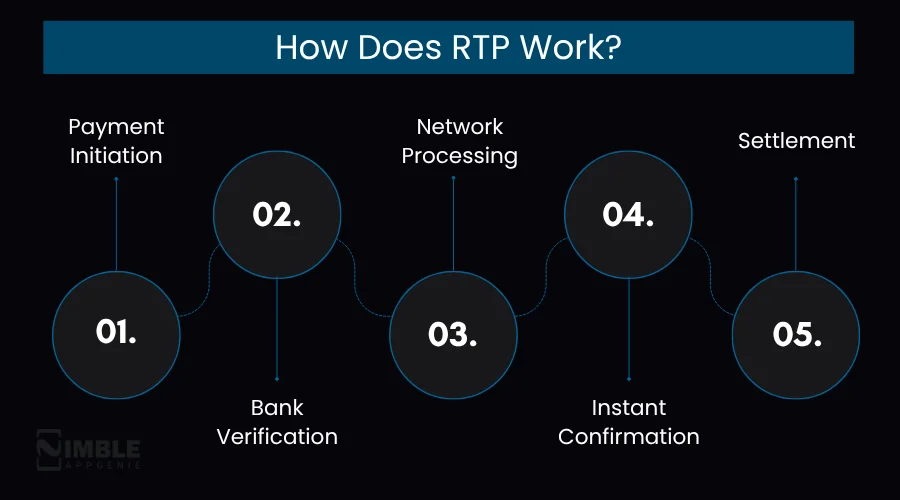

How Does RTP Work?

RTP goes through a complete working procedure, starting from payment initiation, authentication, request routing, interbank communication, and then settlement between the banks.

Let’s learn the complete working process below:

1. Payment Initiation

The first step that RTP takes is payment initiation via the digital banking platform, such as a bank website, and even the payment amount. It includes a transfer request that has been submitted by the payer and received by the bank.

Here, the payer provides details related to the recipient’s bank accounts. This might include the traditional account numbers or even modern aliases such as mobile numbers or email addresses, and even QR codes.

2. Bank Verification

This is the security step undertaken by banks where a financial institution confirms the translation details, account ownership, and even fund availability. Additionally, the bank confirms that the account has sufficient funds for transfer.

It is a process of confirming that a bank account is authentic, active, and even belongs to the person or business claiming ownership. Here, the verification was made via a two-factor authentication system.

3. Network Processing

Network processing in the context of RTP refers to the core infrastructure that enables the instantaneous clearing and settlement of funds directly between institutions.

The key aspects of network processing include real-time credit transfers with enhanced data capabilities. The RTP’s process transactions individually and even continuously, helping the systems to handle transactions.

4. Instant Confirmation

Even after the payment is processed, the payer and the receiver receive a payment confirmation notification or a payment failed notification, based on the RTP’s network processing.

This notification can be received via email, SMS, or even through the push notification from a banking app, depending on how the payment was initiated.

5. Settlement

Settlement is the last step in the RTP process. Unlike in traditional payment systems, which occur at the end of the day, in RTP, settlement happens almost immediately.

Here, the payer’s bank transfers funds to the payee bank, and the money gets immediately available for use in the payee’s account.

Now, if you are a business owner or an investor, thinking of getting ahead with the RTP app, it is the right time. In this guide to RTP and FedNow, we have covered it too.

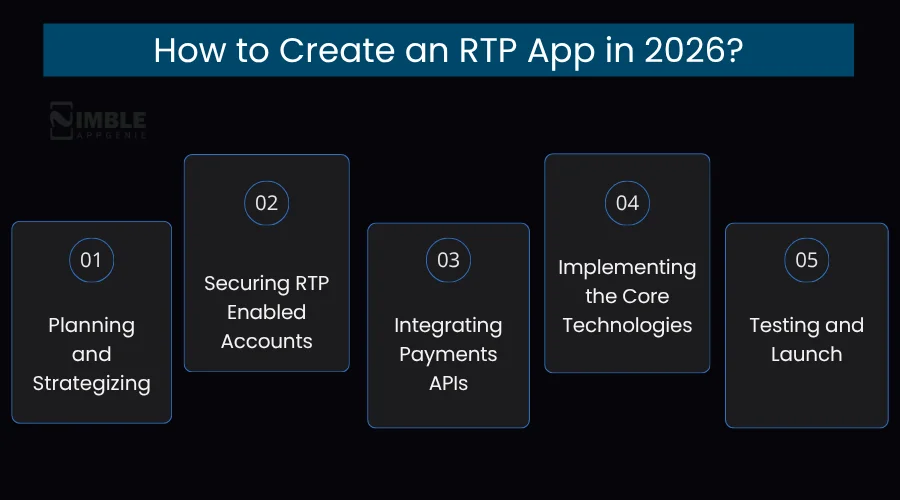

How to Create an RTP App in 2026?

You can create an RTP app beginning with planning, securing RTP-enabled accounts, integrating payments APIs, and implementing the core technologies, further you need to get ahead with security and testing landscape.

Let’s learn it all in simple steps:

Step 1: Planning and Strategizing

When you proceed with the RTP app, one of the foremost steps to undertake is planning, where you identify the market demands and the current technologies in online banking.

Here, you can assess the complete payment process, customer preferences, and security risks for identifying the value of instant payments.

Step 2: Securing RTP-Enabled Accounts

Under this step, you can enable accounts that require a focus on preventing immediate fraudulent transactions. Here, the key security measures comprise employing multi-factor authentication and real-time transaction monitoring.

Here, the key security measures to adopt for RTP accounts are account validation, real-time monitoring, and even the credit push transactions.

Step 3: Integrating Payments APIs

Now, you should proceed with integrating the payment APIs. Here, you should use the financial services APIs to facilitate the bank account linking and verification, and payment routing.

All you need is to select the right API provider, or hire mobile app developers, who can not only build your RTP app, but can also find the right API services for your app.

Step 4: Implementing the Core Technologies

After evaluating APIs, you should examine the fintech app tech stack. These technologies comprises of flutter and react native for the frontend, Java, Python, and Go for the backend.

Along with this, you should use PostgreSQL and MySQL for the relational databases, helpful for handling large volumes of data in networks.

Step 5: Testing and Launch

This is the last step in the process to create an RTP app, which requires simulating the network conditions and validating packet streams via tools for ensuring low-latency delivery. You can proceed with the fintech app testing landscape and can ensure auditing.

Under testing, you get through multiple testing landscapes such as performance testing, compatibility testing, functional testing, and even usability testing. Further, you can launch it on the defined platforms.

After evaluating the RTP, let’s learn about FedNow in this detailed guide on RTP and FedNow.

What is FedNow?

The FedNow service is a new instant payment structure developed by the Federal Reserve that allows eligible depository institutions of diverse sizes across the U.S. to provide real-time payment services.

At the most fundamental level, this service does provide interbank clearing and settlement that enables funds to be transferred from the sender’s account to the receiver’s account in real-time.

Well, how does it work?

Let’s get ahead with the following section.

How Does FedNow Work?

FedNow works simply:

Step 1: The payer uses the bank’s app or website to initiate the payment.

Step 2: The sender’s FI submits a payment request to the FedNow Services

Step 3: The FedNow Services confirms the request. And evaluate that the sender’s bank has enough funds.

Step 4: The FedNow services sends the payment request to the receiver’s FI.

Step 5: The receiver accepts the FI requests and sends them back to the FedNow Services.

Step 6: The FedNow services verify the requests and perform the transaction by debiting the sender’s account and crediting the receiver’s account.

Step 7: The receiver’s FI credits the receiving customer’s account.

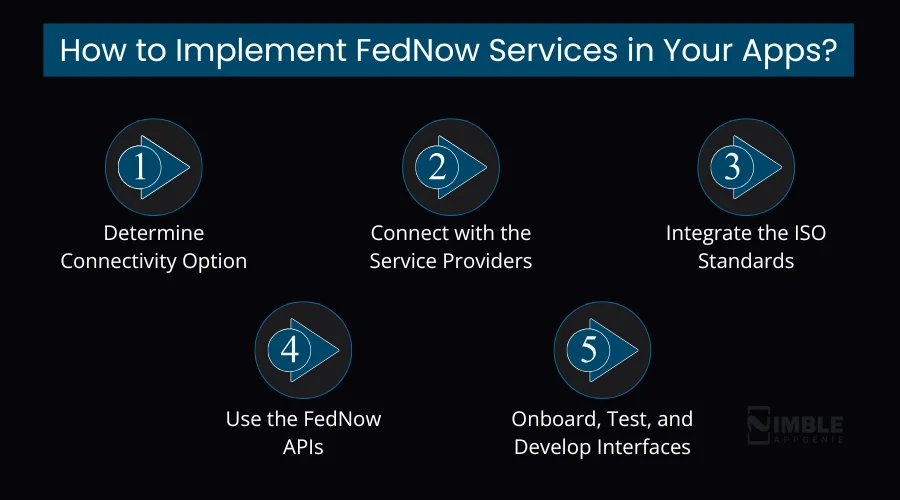

How to Implement FedNow Services in Your Apps?

You can implement the FedNow Services by following the key steps:

1. Determine Connectivity Option

You need to examine whether your institution will connect to the FedNow services, such as FedLine Direct, for high-speed messaging, or even the VPN-based solutions.

It further requires a partnership with a participating financial institution because the Federal Reserve does not provide a standalone app for consumers and businesses.

2. Connect With the Service Providers

Now, the financial institutions can connect with the service providers and can showcase on the FedNow explorer website.

This step serves as a centralized resource for identifying payment errors and connecting with the certified service providers that act as agents for financial institutions to manage payment processing and connectivity.

3. Integrate the ISO Standards

You should integrate the respective ISO 20022 message types, implemented within XML syntax, for diversified aspects of transaction processing.

When it comes to the clearing house (TCH), the RTP network uses ISO 20022 for enabling rich data exchange, which comprises remittance information for the B2B payments.

4. Use the FedNow APIs

The FedNow APIs do enable financial institutions to effectively request data, monitor accounts, and even process instant payments with the help of FedLine solutions.

With the help of FedNow APIs, you can enable financial institutions to have instant payment requirements. It includes establishing connectivity, accessing FedNow DevRel, obtaining credentials, and then testing the connectivity.

5. Onboard, Test, and Develop Interfaces

At this step, you can onboard the FedNow service in your app, then test it under different circumstances, and then can create interactive interfaces.

You can begin with the design mockups that can further clarify behaviors, inputs, and outputs. Along with this, you can build the reusable components and can test the methodologies throughout.

Now, with these steps lets opt for differentiation in the following section.

RTP Vs FedNow: What’s the Core Difference?

If you are confused between RTP and FedNow, then the following table can help.

| Factor | RTP | FedNow |

| Full Name | Real-Time Payments | FedNow Service |

| Operated By | The Clearing House (TCH) | Federal Reserve |

| Ownership | Private (large banks) | U.S. Government |

| Launched | November 2017 | July 20, 2023 |

| Transaction Limit | $1,000,000 | $500,000 |

| Availability | 24/7/365 | 24/7/365 |

| Settlement | Instant | Instant |

| Who Can Join | Large banks & members | All depository institutions |

| Best For | High-value B2B payments | Consumer & small business payments |

| Interoperable | No | No |

| Industry | Fintech / Banking | Fintech / Banking |

| Transaction Fee | Varies by bank | $0.043 per transaction |

| Reach | 71% of U.S. DDAs | 1,000+ institutions & growing |

| Governed By | Private consortium | Federal Reserve Board |

| Primary Users | Large enterprises & corporates | Banks, credit unions, and small businesses |

Connecting with the leading banking software development company can help you with selecting the best option in RTP Vs FedNow.

How To Select Between RTP and FedNow Services?

Selecting between RTP and FedNow services can be a challenging pathway. Hence, here is a series of steps to evaluate for selecting between RTP and FedNow Services.

You can find when to select RTP and in what conditions you should select FedNow services, via a defined table, below:

| Condition | Choose RTP | Choose FedNow |

| Institution Size | Large banks & enterprises | Small banks & credit unions |

| Transaction Limit | Up to $1,000,000 | Up to $500,000 |

| Customer Type | Corporate & B2B clients | Individual consumers & SMBs |

| Use Case | Payroll, real estate, and large transfers | Utility bills, e-commerce, P2P |

| Network Access | TCH member institutions | Any U.S. depository institution |

| Government Payments | Not ideal | Best fit |

| High-Value Transfers | Best fit | Not ideal |

| Nationwide Reach | 71% of U.S. DDAs | 1,000+ growing institutions |

| Established Network | Since 2017 | Rapidly growing since 2023 |

| Best Overall Strategy | Use Both for Maximum Coverage | Use Both for Maximum Coverage |

Partner With Nimble AppGenie and Build your Platform

If you want to integrate one or both, it’s crucial to connect with the right partner.

No need to go anywhere, Nimble AppGenie provides the best fintech app development services to integrate either RTP or FedNow, and even both, in your business app.

Our developers analyse the complete app requirements and then help you with the right service. We offer you the end-to-end services that enable financial institutions and startups to create integrated solutions.

We help you to go for seamless workflow and communication, which our clients find instrumental in ensuring the overall project success and satisfaction. Our team helps you to utilize modern technologies such as AI-driven recommendation engines, machine learning algorithms, and IoT solutions.

Nimble AppGenie offers quality assurance and even helps to maintain partnerships with tech entities such as Intel and AWS. You can connect with our partners and can integrate RTP, FedNow, or even both in your app.

Conclusion

RTP and FedNow have fundamentally transformed the way money moves across America from days to seconds. Whether you are a large enterprise leveraging RTP’s high-value transaction capabilities or a small business embracing FedNow’s inclusive reach, instant payments are no longer a luxury; they are a necessity.

As the fintech landscape continues to evolve rapidly, integrating real-time payment solutions into your business app is the smartest move forward.

FAQs

Niketan Sharma, CTO, Nimble AppGenie, is a tech enthusiast with more than a decade of experience in delivering high-value solutions that allow a brand to penetrate the market easily. With a strong hold on mobile app development, he is actively working to help businesses identify the potential of digital transformation by sharing insightful statistics, guides & blogs.

Table of Contents

No Comments

Comments are closed.